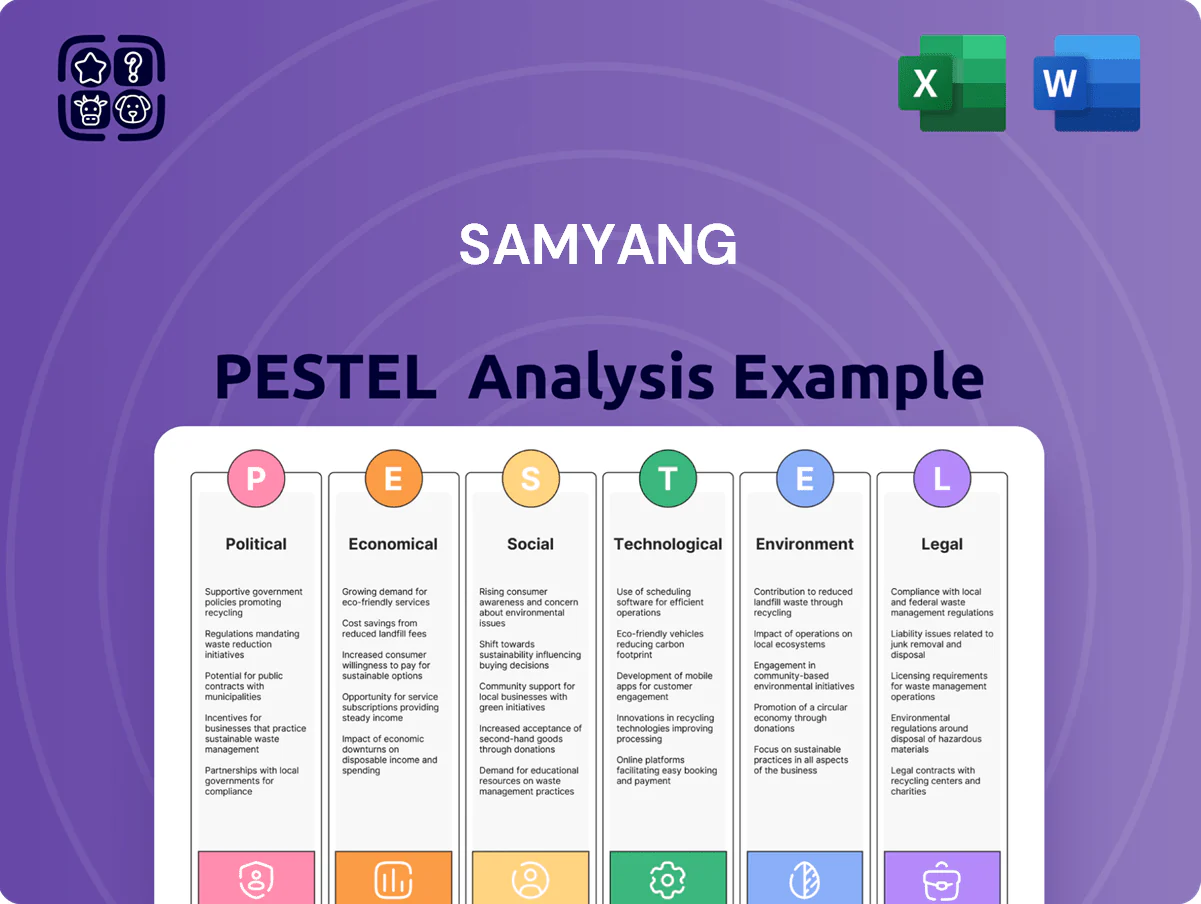

Samyang PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological advances are reshaping Samyang’s prospects in our concise PESTLE snapshot—built for investors and strategists who need fast, actionable insight; purchase the full analysis to access detailed risks, opportunities, and ready-to-use recommendations.

Political factors

Geopolitical Trade Dynamics

The 2024-25 escalation in US-China trade measures has raised tariffs on select polymers by up to 15%, pressuring Samyang's engineering plastics export margins as exports to China and the US account for roughly 42% of segment sales in 2024.

Tariff volatility and renegotiated regional trade pacts have pushed management to diversify raw material sourcing; imports from Southeast Asia rose 28% in 2025 to reduce exposure to China-origin feedstocks.

Supply-chain diversification efforts target a 20% reduction in single-country sourcing risk by end-2025, supported by CAPEX reallocation of KRW 120 billion toward alternative procurement and localized production capacity.

South Korean Industrial Policy

The South Korean government allocated 315 trillion won (2023–2027) to advanced industries, with targeted subsidies and R&D tax credits boosting high-tech materials and specialty chemicals; Samyang reported R&D support of about 28 billion won in 2024, benefiting semiconductor materials and EV component lines.

Food Security and Price Controls

As a dominant player in Korea's sugar and flour markets, Samyang faces tight government oversight to curb food inflation; in 2025 authorities target food CPI stabilization after food inflation hit 4.1% in 2024. Regulators have pressured conglomerates to cap margins, forcing Samyang to reconcile FY2024 gross margin of 18.5% with mandated price controls. The political push increases compliance costs and limits pricing power while elevating social responsibility expectations.

Global Supply Chain Resilience

Political instability in the Red Sea and Horn of Africa corridors has increased shipping insurance premiums by roughly 35% since 2022, prompting Samyang to reroute shipments and diversify suppliers to protect its chemical and food lines.

Samyang has entered public-private partnerships securing at least 120,000 tonnes of critical feedstock annually, stabilizing procurement costs and supporting 2024 production targets despite geopolitical supply shocks.

- 35% rise in insurance costs since 2022

- 120,000 tonnes secured via partnerships

- Diversified shipping routes to sustain production

Corporate Governance Reform

The South Korean government’s push for chaebol transparency has led Samyang to bolster board oversight and internal audits; in 2024 the company increased independent directors to 40% and expanded audit committee meetings by 30% year‑over‑year.

These governance reforms aim to uphold investor confidence—Samyang’s foreign ownership rose to 22.5% in 2024—and reduce risks of fines or reputational damage under stricter regulatory scrutiny.

- Independent directors: 40%

- Audit meetings: +30% YoY (2024)

- Foreign ownership: 22.5% (2024)

Tariffs, CAPEX shift and supply diversification cut China/US risk—SE Asia imports +28%

US-China tariff hikes (up to 15% on polymers) cut export margins as China+US = 42% of engineering plastics sales in 2024; imports from SE Asia rose 28% in 2025 to diversify feedstock sourcing.

KRW 120bn CAPEX reallocated to cut single-country sourcing risk by 20% by end‑2025; R&D support ~KRW 28bn in 2024 under Korea’s KRW 315tn advanced industries plan.

Shipping insurance +35% since 2022 due to Red Sea instability; 120,000 tpa secured via public‑private partnerships; independent directors 40%, foreign ownership 22.5% (2024).

| Metric | Value |

|---|---|

| China+US share (2024) | 42% |

| SE Asia import rise (2025) | +28% |

| CAPEX reallocated | KRW 120bn |

| R&D support (2024) | KRW 28bn |

| Insurance cost rise since 2022 | +35% |

| Secured feedstock | 120,000 tpa |

| Independent directors (2024) | 40% |

| Foreign ownership (2024) | 22.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Samyang across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify actionable threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary of Samyang that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Commodity Price Volatility

Samyang faces significant exposure to volatile global raw material prices—sugar up 18% YoY and corn up 12% in 2025, while Brent-linked feedstock costs spiked 27% amid climate-driven supply shocks.

Erratic 2025 price movements were driven by extreme weather in Southeast Asia and shifting demand from processed-food exporters, tightening spreads and raising COGS by an estimated 6–8% for the sector.

To protect margins, Samyang uses derivatives hedging covering roughly 70% of expected commodity needs and negotiates multi-year supply contracts that have reduced input-cost volatility by an estimated 40%.

Currency Exchange Rate Sensitivity

With roughly 55% of 2024 revenues from international chemical sales, Samyang’s results are highly sensitive to the KRW/USD rate; a 5% won appreciation in 2024 would have cut export competitiveness materially, while a 5% depreciation would raise imported raw material costs in won terms. Volatile won movements in 2023–24 (KRW ranged ~1,250–1,350 per USD) amplified margin risk. The company employs a centralized treasury, hedging ~60–75% of short-term FX exposure and netting global cash flows to stabilize earnings.

Electric Vehicle Market Expansion

The global EV fleet surpassed 25 million vehicles in 2024, and EV sales grew about 40% year-on-year, bolstering demand for Samyang’s engineering plastics used in lightweighting and battery housings. Lightweight, high-strength polymers can cut vehicle weight by 10–20%, directly improving battery range and efficiency—supporting higher margins for specialty chemical suppliers. This structural shift is expected to sustain a multi-year revenue tailwind for Samyang’s plastics division, with automotive materials demand projected to grow double digits through 2030.

Domestic Consumer Spending Trends

Economic cooling and a 3.5% domestic CPI in 2024, alongside Bank of Korea policy rates near 3.5%–3.75%, shifted Korean consumers toward lower-cost processed foods and private-label items; Samyang has expanded value-focused SKUs while retaining premium lines to capture trade-down and premium segments.

Adapting the portfolio is key to defend 2025 domestic share amid slower real retail sales growth (0.8% y/y in 2024) and rising price sensitivity among households.

- 2024 CPI 3.5%, policy rate ~3.5%–3.75%

- Retail sales growth 0.8% y/y (2024)

- Strategy: expand value SKUs + maintain premium ingredients

Capital Expenditure and Interest Rates

The prevailing interest rate environment in late 2025, with South Korea's base rate around 3.5% and global corporate borrowing costs elevated, raises Samyang's weighted average cost of capital for capex and R&D, pressuring project IRRs.

Samyang must time debt issuance and capital deployments to preserve financial viability for sector expansion, keeping debt-to-equity near its 2024 level of ~0.6 while targeting high-growth advanced materials.

- Base rate ~3.5% (late 2025)

- WACC pressure lowers project IRR

- Target D/E ~0.6

- Prioritize timing of debt and capex

Samyang faces rising input costs and FX risk despite 70% hedges; exports drive sensitivity

Samyang faces input-cost pressure from 2025 commodity moves (sugar +18% YoY, corn +12%, Brent-linked feedstocks +27%), hedges ~70% of commodities and 60–75% FX, with exports ~55% of 2024 revenue making results sensitive to KRW/USD swings (KRW ~1,250–1,350 in 2023–24). Domestic CPI 3.5% and retail sales +0.8% (2024) drove value-SKU expansion; base rate ~3.5% (late 2025) raises WACC, target D/E ~0.6.

| Metric | 2024–25 |

|---|---|

| Commodity moves | Sugar +18%, Corn +12%, Feedstock +27% |

| Hedging | Commodities ~70%, FX 60–75% |

| Export revenue | ~55% (2024) |

| KRW/USD range | ~1,250–1,350 (2023–24) |

| CPI / Retail | CPI 3.5%, Retail +0.8% (2024) |

| Rates / leverage | Base rate ~3.5% (late 2025), target D/E ~0.6 |

Preview Before You Purchase

Samyang PESTLE Analysis

The preview shown here is the exact Samyang PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

What you’re previewing is the final, professionally structured file—ready for analysis, presentation, or integration into your strategic work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological advances are reshaping Samyang’s prospects in our concise PESTLE snapshot—built for investors and strategists who need fast, actionable insight; purchase the full analysis to access detailed risks, opportunities, and ready-to-use recommendations.

Political factors

Geopolitical Trade Dynamics

The 2024-25 escalation in US-China trade measures has raised tariffs on select polymers by up to 15%, pressuring Samyang's engineering plastics export margins as exports to China and the US account for roughly 42% of segment sales in 2024.

Tariff volatility and renegotiated regional trade pacts have pushed management to diversify raw material sourcing; imports from Southeast Asia rose 28% in 2025 to reduce exposure to China-origin feedstocks.

Supply-chain diversification efforts target a 20% reduction in single-country sourcing risk by end-2025, supported by CAPEX reallocation of KRW 120 billion toward alternative procurement and localized production capacity.

South Korean Industrial Policy

The South Korean government allocated 315 trillion won (2023–2027) to advanced industries, with targeted subsidies and R&D tax credits boosting high-tech materials and specialty chemicals; Samyang reported R&D support of about 28 billion won in 2024, benefiting semiconductor materials and EV component lines.

Food Security and Price Controls

As a dominant player in Korea's sugar and flour markets, Samyang faces tight government oversight to curb food inflation; in 2025 authorities target food CPI stabilization after food inflation hit 4.1% in 2024. Regulators have pressured conglomerates to cap margins, forcing Samyang to reconcile FY2024 gross margin of 18.5% with mandated price controls. The political push increases compliance costs and limits pricing power while elevating social responsibility expectations.

Global Supply Chain Resilience

Political instability in the Red Sea and Horn of Africa corridors has increased shipping insurance premiums by roughly 35% since 2022, prompting Samyang to reroute shipments and diversify suppliers to protect its chemical and food lines.

Samyang has entered public-private partnerships securing at least 120,000 tonnes of critical feedstock annually, stabilizing procurement costs and supporting 2024 production targets despite geopolitical supply shocks.

- 35% rise in insurance costs since 2022

- 120,000 tonnes secured via partnerships

- Diversified shipping routes to sustain production

Corporate Governance Reform

The South Korean government’s push for chaebol transparency has led Samyang to bolster board oversight and internal audits; in 2024 the company increased independent directors to 40% and expanded audit committee meetings by 30% year‑over‑year.

These governance reforms aim to uphold investor confidence—Samyang’s foreign ownership rose to 22.5% in 2024—and reduce risks of fines or reputational damage under stricter regulatory scrutiny.

- Independent directors: 40%

- Audit meetings: +30% YoY (2024)

- Foreign ownership: 22.5% (2024)

Tariffs, CAPEX shift and supply diversification cut China/US risk—SE Asia imports +28%

US-China tariff hikes (up to 15% on polymers) cut export margins as China+US = 42% of engineering plastics sales in 2024; imports from SE Asia rose 28% in 2025 to diversify feedstock sourcing.

KRW 120bn CAPEX reallocated to cut single-country sourcing risk by 20% by end‑2025; R&D support ~KRW 28bn in 2024 under Korea’s KRW 315tn advanced industries plan.

Shipping insurance +35% since 2022 due to Red Sea instability; 120,000 tpa secured via public‑private partnerships; independent directors 40%, foreign ownership 22.5% (2024).

| Metric | Value |

|---|---|

| China+US share (2024) | 42% |

| SE Asia import rise (2025) | +28% |

| CAPEX reallocated | KRW 120bn |

| R&D support (2024) | KRW 28bn |

| Insurance cost rise since 2022 | +35% |

| Secured feedstock | 120,000 tpa |

| Independent directors (2024) | 40% |

| Foreign ownership (2024) | 22.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Samyang across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify actionable threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary of Samyang that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Commodity Price Volatility

Samyang faces significant exposure to volatile global raw material prices—sugar up 18% YoY and corn up 12% in 2025, while Brent-linked feedstock costs spiked 27% amid climate-driven supply shocks.

Erratic 2025 price movements were driven by extreme weather in Southeast Asia and shifting demand from processed-food exporters, tightening spreads and raising COGS by an estimated 6–8% for the sector.

To protect margins, Samyang uses derivatives hedging covering roughly 70% of expected commodity needs and negotiates multi-year supply contracts that have reduced input-cost volatility by an estimated 40%.

Currency Exchange Rate Sensitivity

With roughly 55% of 2024 revenues from international chemical sales, Samyang’s results are highly sensitive to the KRW/USD rate; a 5% won appreciation in 2024 would have cut export competitiveness materially, while a 5% depreciation would raise imported raw material costs in won terms. Volatile won movements in 2023–24 (KRW ranged ~1,250–1,350 per USD) amplified margin risk. The company employs a centralized treasury, hedging ~60–75% of short-term FX exposure and netting global cash flows to stabilize earnings.

Electric Vehicle Market Expansion

The global EV fleet surpassed 25 million vehicles in 2024, and EV sales grew about 40% year-on-year, bolstering demand for Samyang’s engineering plastics used in lightweighting and battery housings. Lightweight, high-strength polymers can cut vehicle weight by 10–20%, directly improving battery range and efficiency—supporting higher margins for specialty chemical suppliers. This structural shift is expected to sustain a multi-year revenue tailwind for Samyang’s plastics division, with automotive materials demand projected to grow double digits through 2030.

Domestic Consumer Spending Trends

Economic cooling and a 3.5% domestic CPI in 2024, alongside Bank of Korea policy rates near 3.5%–3.75%, shifted Korean consumers toward lower-cost processed foods and private-label items; Samyang has expanded value-focused SKUs while retaining premium lines to capture trade-down and premium segments.

Adapting the portfolio is key to defend 2025 domestic share amid slower real retail sales growth (0.8% y/y in 2024) and rising price sensitivity among households.

- 2024 CPI 3.5%, policy rate ~3.5%–3.75%

- Retail sales growth 0.8% y/y (2024)

- Strategy: expand value SKUs + maintain premium ingredients

Capital Expenditure and Interest Rates

The prevailing interest rate environment in late 2025, with South Korea's base rate around 3.5% and global corporate borrowing costs elevated, raises Samyang's weighted average cost of capital for capex and R&D, pressuring project IRRs.

Samyang must time debt issuance and capital deployments to preserve financial viability for sector expansion, keeping debt-to-equity near its 2024 level of ~0.6 while targeting high-growth advanced materials.

- Base rate ~3.5% (late 2025)

- WACC pressure lowers project IRR

- Target D/E ~0.6

- Prioritize timing of debt and capex

Samyang faces rising input costs and FX risk despite 70% hedges; exports drive sensitivity

Samyang faces input-cost pressure from 2025 commodity moves (sugar +18% YoY, corn +12%, Brent-linked feedstocks +27%), hedges ~70% of commodities and 60–75% FX, with exports ~55% of 2024 revenue making results sensitive to KRW/USD swings (KRW ~1,250–1,350 in 2023–24). Domestic CPI 3.5% and retail sales +0.8% (2024) drove value-SKU expansion; base rate ~3.5% (late 2025) raises WACC, target D/E ~0.6.

| Metric | 2024–25 |

|---|---|

| Commodity moves | Sugar +18%, Corn +12%, Feedstock +27% |

| Hedging | Commodities ~70%, FX 60–75% |

| Export revenue | ~55% (2024) |

| KRW/USD range | ~1,250–1,350 (2023–24) |

| CPI / Retail | CPI 3.5%, Retail +0.8% (2024) |

| Rates / leverage | Base rate ~3.5% (late 2025), target D/E ~0.6 |

Preview Before You Purchase

Samyang PESTLE Analysis

The preview shown here is the exact Samyang PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

What you’re previewing is the final, professionally structured file—ready for analysis, presentation, or integration into your strategic work.