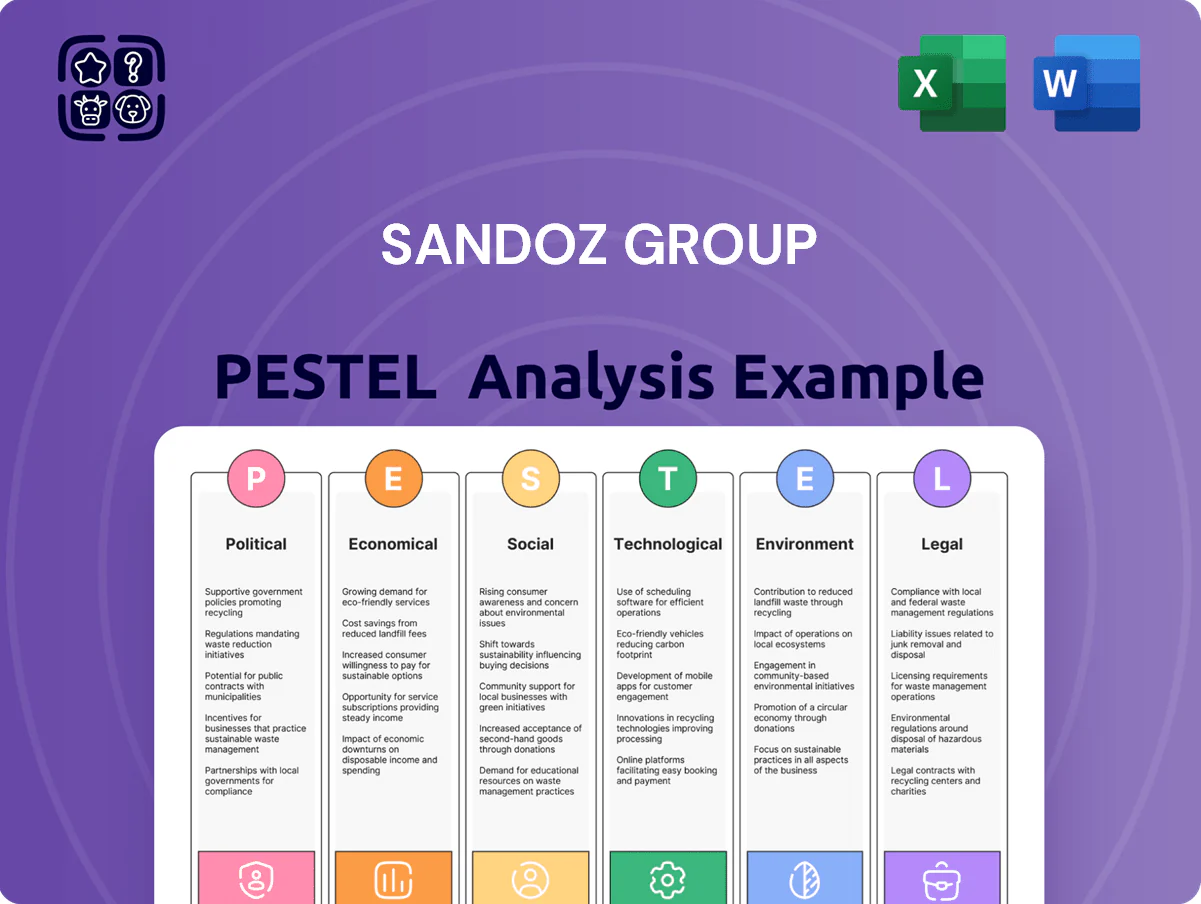

Sandoz Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how regulatory shifts, market pricing pressures, and biotech innovation converge to shape Sandoz Group’s strategic path—our PESTLE snapshot highlights the external risks and opportunities driving future growth. Ideal for investors, strategists, and advisors, the full PESTLE delivers actionable insights and ready-to-use slides to inform decisions. Download the complete analysis now for a data-backed competitive edge.

Political factors

Government Pricing Interventions

National governments are imposing price controls and mandatory discounts to curb healthcare spending, with OECD countries reporting average medicine price reductions of 5–12% in 2023–2024; the US Inflation Reduction Act’s drug price negotiation framework, targeting high-cost biologics, pressures list prices and accelerates biosimilar uptake—projected to save Medicare $98 billion 2024–2033—forcing Sandoz to adapt reimbursement strategies to protect margins while advancing affordable access.

Geopolitical Supply Chain Security

Political tensions between China, the US and EU have driven policies favoring domestic pharma manufacturing; 2024 EU and US subsidies for reshoring reached over €8.5bn and $6.2bn respectively to secure critical supply chains.

Governments in Europe and North America are incentivizing reshoring of API production—EU estimates aim to double local API capacity by 2027 to cut reliance on single-source regions from ~60% to under 35%.

Sandoz, with ~70% of its manufacturing in Europe, is well positioned to capture reshoring demand but faces margin pressure as Western production costs are typically 20–30% higher than Asian alternatives; careful cost management is required.

Healthcare Reform and Universal Access

Political moves toward universal healthcare in emerging markets are expanding the TAM for generics; WHO estimates 2 billion people gained improved access to essential medicines initiatives by 2024, boosting generics demand by ~6–8% CAGR in those regions. Legislative pushes to cut out-of-pocket costs increasingly favor biosimilars; biosimilar uptake grew 22% globally in 2023 as payers sought lower-cost biologic alternatives. Sandoz has secured multiple national tenders and state partnerships—supplying essential medicines in over 40 countries and capturing double-digit share in several public markets—positioning it as a preferred provider amid policy shifts.

Regulatory Harmonization Initiatives

Regulatory cooperation between FDA and EMA, including ICH and pilot reliance pathways, is reducing duplicative trials for complex generics and biosimilars, cutting approval timelines—EMA reported reliance use rose ~25% in 2024—supporting Sandoz’s faster multi-jurisdiction launches and potential revenue gains from quicker market access.

Protectionist policy shifts in some markets (tariff or local-data requirements) still cause regional delays, necessitating targeted government affairs; 2024 trade-restrictive measures increased 8% globally per WTO, raising compliance costs.

- FDA–EMA harmonization up ~25% reliance use (2024)

- Reduces duplicative trials, speeds time-to-market

- WTO: trade-restrictive measures +8% (2024)

- Requires targeted government affairs to mitigate local hurdles

Trade Policies and Tariff Barriers

Changes in international trade agreements and tariffs on chemical precursors can raise Sandoz’s COGS; for example, a 5-10% tariff on key APIs could add millions to annual costs given Sandoz’s 2024 revenues of about €8.0bn for Novartis’s Sandoz division.

Sandoz continuously monitors EU trade relations—notably EU-US and EU-India talks—to anticipate import duties and regulatory shifts that affect supply chains.

Strategic sourcing and supplier diversification reduce exposure; in 2023 Sandoz expanded Asian and European supplier contracts to lower single‑supplier risk.

- Tariff shock (5–10%) risks raising COGS

- 2024 pro forma revenue context: ~€8.0bn

- Active monitoring of EU trade partners

- Supplier diversification to mitigate duty-driven disruptions

Sandoz: Reshoring boosts biosimilar growth but squeezes margins amid rising Western costs

Price controls and IRA-led US negotiations pressure margins while boosting biosimilar uptake (global biosimilar growth 22% in 2023); reshoring subsidies (€8.5bn EU, $6.2bn US in 2024) favor Sandoz’s Europe-heavy manufacturing (~70%) but raise costs (Western production +20–30%); API reshoring aims to cut single-source reliance from ~60% to <35% by 2027; FDA–EMA reliance ↑25% (2024) speeds launches.

| Metric | Value |

|---|---|

| 2024 pro forma revenue (Sandoz) | ~€8.0bn |

| Biosimilar growth (2023) | 22% |

| Reshoring subsidies (2024) | EU €8.5bn; US $6.2bn |

| Western production cost premium | +20–30% |

| FDA–EMA reliance change (2024) | +25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Sandoz across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Sandoz that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market drivers—editable for region- or business-line–specific notes.

Economic factors

Global Inflationary Pressures

Persistent inflation in energy, labor, and raw material costs—energy prices up ~18% y/y in 2024 and global generic API costs rising ~12%—squeezes the thin margins of the generic pharma sector where gross margins often sit in the mid-20s%. Sandoz leans on operational excellence and centralized procurement, citing €300m+ cost-savings targets in 2024–25 to offset input inflation. With many markets subject to fixed government pricing, ability to pass costs is constrained, leaving efficiency as the main margin lever.

Currency Exchange Rate Volatility

As a Swiss-based firm, Sandoz faces FX risk from CHF/EUR and CHF/USD swings; a 10% CHF appreciation vs EUR in 2024 would compress reported Euro revenues materially given ~40% EU sales. The group used hedges covering roughly 60–70% of short-term exposure in 2024 and levers geographic revenue mix—45% North America, 40% Europe in 2024—to offset CHF strength and protect margins.

Growth in Emerging Markets

Interest Rate Environment

The higher global interest rates—US Fed funds at 5.25–5.50% (2024) and ECB policy around 4.00%—raise Sandoz’s debt servicing costs and make funding new manufacturing sites more expensive, pressuring capex timing.

Sandoz’s disciplined capital allocation prioritizes sustainable biosimilar R&D, limiting net debt growth (Novartis Group net debt/EBITDA target range maintained through 2024 guidance).

Elevated rates compress valuations for acquisition targets in generics, reducing deal activity and lowering expected purchase multiples versus 2021–22 levels.

- Higher rates increase capex borrowing costs and extend payback periods

- Capital allocation preserves R&D funding while constraining large one‑off investments

- Acquisition valuations down, reducing M&A volume and pricing expectations

Cost Containment in Healthcare Systems

- Global projected biosimilar savings > USD 100bn by 2028

- Cost reductions per biologic 20–40%

- Payers favor biosimilars after major patent expiries

Sandoz combats input inflation with €300M+ cuts, 65% FX hedge as biosimilars surge

Inflationary input costs and fixed pricing squeeze mid-20s% gross margins; Sandoz targets €300m+ savings (2024–25) and hedged ~65% FX exposure in 2024 to protect ~45% NA/40% EU revenue. Emerging markets grew ~4.5% (SE Asia) and 3.2% (LatAm) in 2024, boosting generics demand 6–8%. Fed/ECB rates (2024) raised capex costs; biosimilars projected >USD100bn savings by 2028.

| Metric | 2024 |

|---|---|

| Energy inflation | +18% y/y |

| Generic API costs | +12% y/y |

| Hedge coverage | ~65% |

| Cost savings target | €300m+ |

| Biosimilar savings | >USD100bn by 2028 |

Preview the Actual Deliverable

Sandoz Group PESTLE Analysis

The preview shown here is the exact Sandoz Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how regulatory shifts, market pricing pressures, and biotech innovation converge to shape Sandoz Group’s strategic path—our PESTLE snapshot highlights the external risks and opportunities driving future growth. Ideal for investors, strategists, and advisors, the full PESTLE delivers actionable insights and ready-to-use slides to inform decisions. Download the complete analysis now for a data-backed competitive edge.

Political factors

Government Pricing Interventions

National governments are imposing price controls and mandatory discounts to curb healthcare spending, with OECD countries reporting average medicine price reductions of 5–12% in 2023–2024; the US Inflation Reduction Act’s drug price negotiation framework, targeting high-cost biologics, pressures list prices and accelerates biosimilar uptake—projected to save Medicare $98 billion 2024–2033—forcing Sandoz to adapt reimbursement strategies to protect margins while advancing affordable access.

Geopolitical Supply Chain Security

Political tensions between China, the US and EU have driven policies favoring domestic pharma manufacturing; 2024 EU and US subsidies for reshoring reached over €8.5bn and $6.2bn respectively to secure critical supply chains.

Governments in Europe and North America are incentivizing reshoring of API production—EU estimates aim to double local API capacity by 2027 to cut reliance on single-source regions from ~60% to under 35%.

Sandoz, with ~70% of its manufacturing in Europe, is well positioned to capture reshoring demand but faces margin pressure as Western production costs are typically 20–30% higher than Asian alternatives; careful cost management is required.

Healthcare Reform and Universal Access

Political moves toward universal healthcare in emerging markets are expanding the TAM for generics; WHO estimates 2 billion people gained improved access to essential medicines initiatives by 2024, boosting generics demand by ~6–8% CAGR in those regions. Legislative pushes to cut out-of-pocket costs increasingly favor biosimilars; biosimilar uptake grew 22% globally in 2023 as payers sought lower-cost biologic alternatives. Sandoz has secured multiple national tenders and state partnerships—supplying essential medicines in over 40 countries and capturing double-digit share in several public markets—positioning it as a preferred provider amid policy shifts.

Regulatory Harmonization Initiatives

Regulatory cooperation between FDA and EMA, including ICH and pilot reliance pathways, is reducing duplicative trials for complex generics and biosimilars, cutting approval timelines—EMA reported reliance use rose ~25% in 2024—supporting Sandoz’s faster multi-jurisdiction launches and potential revenue gains from quicker market access.

Protectionist policy shifts in some markets (tariff or local-data requirements) still cause regional delays, necessitating targeted government affairs; 2024 trade-restrictive measures increased 8% globally per WTO, raising compliance costs.

- FDA–EMA harmonization up ~25% reliance use (2024)

- Reduces duplicative trials, speeds time-to-market

- WTO: trade-restrictive measures +8% (2024)

- Requires targeted government affairs to mitigate local hurdles

Trade Policies and Tariff Barriers

Changes in international trade agreements and tariffs on chemical precursors can raise Sandoz’s COGS; for example, a 5-10% tariff on key APIs could add millions to annual costs given Sandoz’s 2024 revenues of about €8.0bn for Novartis’s Sandoz division.

Sandoz continuously monitors EU trade relations—notably EU-US and EU-India talks—to anticipate import duties and regulatory shifts that affect supply chains.

Strategic sourcing and supplier diversification reduce exposure; in 2023 Sandoz expanded Asian and European supplier contracts to lower single‑supplier risk.

- Tariff shock (5–10%) risks raising COGS

- 2024 pro forma revenue context: ~€8.0bn

- Active monitoring of EU trade partners

- Supplier diversification to mitigate duty-driven disruptions

Sandoz: Reshoring boosts biosimilar growth but squeezes margins amid rising Western costs

Price controls and IRA-led US negotiations pressure margins while boosting biosimilar uptake (global biosimilar growth 22% in 2023); reshoring subsidies (€8.5bn EU, $6.2bn US in 2024) favor Sandoz’s Europe-heavy manufacturing (~70%) but raise costs (Western production +20–30%); API reshoring aims to cut single-source reliance from ~60% to <35% by 2027; FDA–EMA reliance ↑25% (2024) speeds launches.

| Metric | Value |

|---|---|

| 2024 pro forma revenue (Sandoz) | ~€8.0bn |

| Biosimilar growth (2023) | 22% |

| Reshoring subsidies (2024) | EU €8.5bn; US $6.2bn |

| Western production cost premium | +20–30% |

| FDA–EMA reliance change (2024) | +25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Sandoz across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Sandoz that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market drivers—editable for region- or business-line–specific notes.

Economic factors

Global Inflationary Pressures

Persistent inflation in energy, labor, and raw material costs—energy prices up ~18% y/y in 2024 and global generic API costs rising ~12%—squeezes the thin margins of the generic pharma sector where gross margins often sit in the mid-20s%. Sandoz leans on operational excellence and centralized procurement, citing €300m+ cost-savings targets in 2024–25 to offset input inflation. With many markets subject to fixed government pricing, ability to pass costs is constrained, leaving efficiency as the main margin lever.

Currency Exchange Rate Volatility

As a Swiss-based firm, Sandoz faces FX risk from CHF/EUR and CHF/USD swings; a 10% CHF appreciation vs EUR in 2024 would compress reported Euro revenues materially given ~40% EU sales. The group used hedges covering roughly 60–70% of short-term exposure in 2024 and levers geographic revenue mix—45% North America, 40% Europe in 2024—to offset CHF strength and protect margins.

Growth in Emerging Markets

Interest Rate Environment

The higher global interest rates—US Fed funds at 5.25–5.50% (2024) and ECB policy around 4.00%—raise Sandoz’s debt servicing costs and make funding new manufacturing sites more expensive, pressuring capex timing.

Sandoz’s disciplined capital allocation prioritizes sustainable biosimilar R&D, limiting net debt growth (Novartis Group net debt/EBITDA target range maintained through 2024 guidance).

Elevated rates compress valuations for acquisition targets in generics, reducing deal activity and lowering expected purchase multiples versus 2021–22 levels.

- Higher rates increase capex borrowing costs and extend payback periods

- Capital allocation preserves R&D funding while constraining large one‑off investments

- Acquisition valuations down, reducing M&A volume and pricing expectations

Cost Containment in Healthcare Systems

- Global projected biosimilar savings > USD 100bn by 2028

- Cost reductions per biologic 20–40%

- Payers favor biosimilars after major patent expiries

Sandoz combats input inflation with €300M+ cuts, 65% FX hedge as biosimilars surge

Inflationary input costs and fixed pricing squeeze mid-20s% gross margins; Sandoz targets €300m+ savings (2024–25) and hedged ~65% FX exposure in 2024 to protect ~45% NA/40% EU revenue. Emerging markets grew ~4.5% (SE Asia) and 3.2% (LatAm) in 2024, boosting generics demand 6–8%. Fed/ECB rates (2024) raised capex costs; biosimilars projected >USD100bn savings by 2028.

| Metric | 2024 |

|---|---|

| Energy inflation | +18% y/y |

| Generic API costs | +12% y/y |

| Hedge coverage | ~65% |

| Cost savings target | €300m+ |

| Biosimilar savings | >USD100bn by 2028 |

Preview the Actual Deliverable

Sandoz Group PESTLE Analysis

The preview shown here is the exact Sandoz Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.