Sandstorm Gold Business Model Canvas

Sandstorm Gold: Compact Business Model Canvas for Scalable, De-risked Streaming Revenue

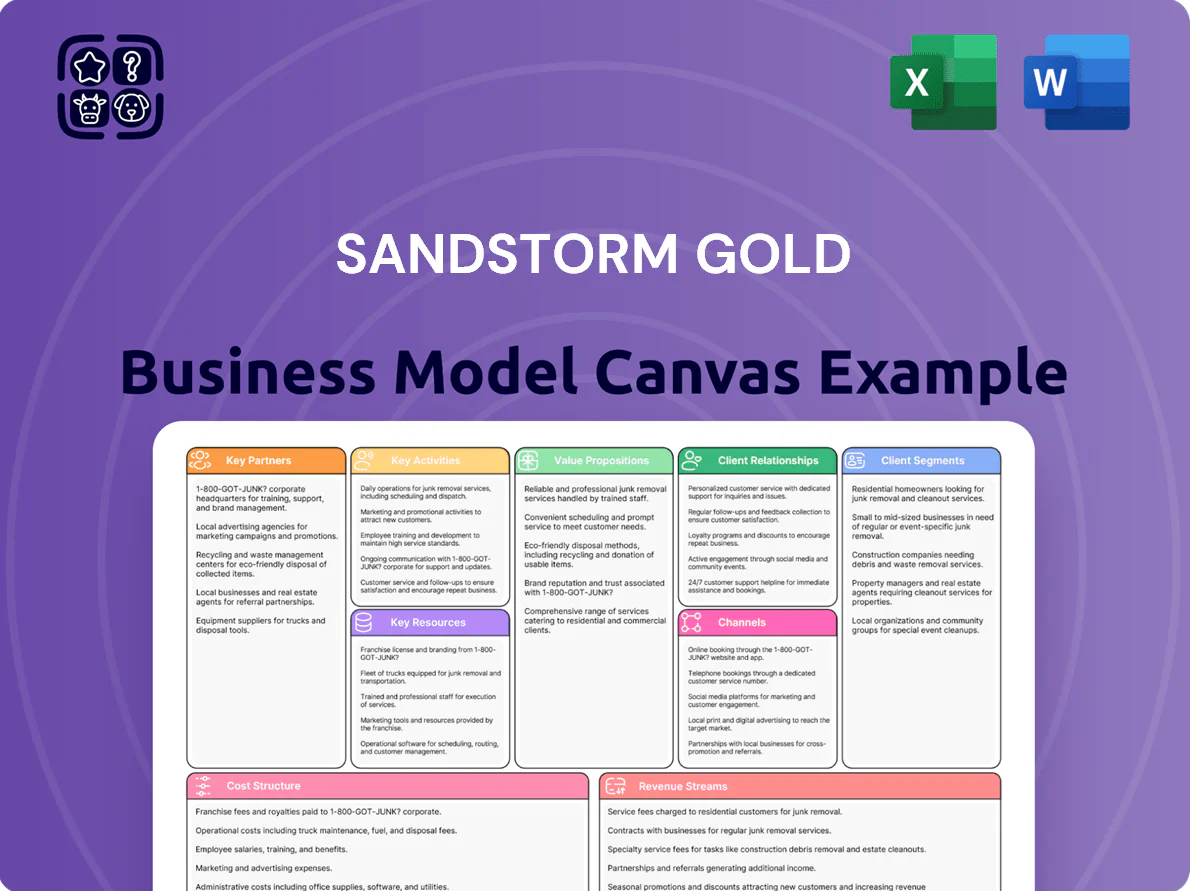

Unlock the full strategic blueprint behind Sandstorm Gold’s business model—this concise Business Model Canvas shows how streaming royalties, low operating overhead, and targeted partnerships drive scalable, de-risked revenue for investors and operators; download the complete Word/Excel canvas for a section-by-section playbook you can use for benchmarking, investor decks, or strategic planning.

Partnerships

Primary Mining Operators

Primary mining operators manage on-site extraction and Sandstorm depends on their technical teams and local permitting skills to sustain production; by Q4 2025 Sandstorm’s streaming and royalty portfolio covers interests in over 40 operating mines and advanced projects, securing roughly 120–150 koz annual attributable gold equivalent ounces (GEOs).

Financial Institutions and Lenders

Financial institutions and lenders supply revolving credit lines and access to debt markets, enabling Sandstorm Gold to fund large upfront royalty purchases; for example, Sandstorm’s 2024 revolving facility capacity reached US$150m, supporting quick deals. These partners demand a strong balance sheet and steady cash flow—Sandstorm’s 2024 adjusted EBITDA of ~US$75m and net cash position underpin its borrowing capacity and timely execution.

Technical and Geological Consultants

Technical and geological consultants provide independent validation of reserves and project viability during due diligence, reducing Sandstorm Gold’s deal failure risk; in 2024 independent reserve revisions changed NPV estimates by up to 18% on comparable junior deals, so their input directly affects valuation of prospective streams.

The specialists flag engineering or environmental hurdles before capital is committed and their assessments support long-term sustainability of partner mines; Sandstorm typically budgets ~0.5–1.5% of deal value for such studies, cutting downstream remediation or redesign costs that can exceed 10% of capex.

Legal and Jurisdictional Advisors

Legal and jurisdictional advisors guide Sandstorm Gold across 12 countries, helping interpret cross-border mining laws and tax treaties to secure after-tax cash flows; they draft royalty agreements that include creditor-priority clauses and transfer protections to survive operator insolvency or 2025 ownership changes.

Advisors also map and certify ESG compliance—covering TC/ESG reporting, Scope 1–3 emissions alignment, and 2025 mandatory disclosures—to limit regulatory fines and protect royalty valuation.

- Cover 12 countries

- Draft creditor-priority royalty clauses

- Protect against operator insolvency

- Ensure 2025 ESG and Scope 1–3 reporting

Syndication and Co-Investment Partners

By 2025 Sandstorm Gold frequently syndicates with other royalty firms and private equity to underwrite very large streams, letting it access higher-value projects while capping exposure to any single mine; syndications accounted for roughly 20% of announced stream financing in 2024–25, helping keep Sandstorm’s single-asset exposure below 15% of NAV.

- Access large deals otherwise unaffordable

- Diversifies project and counterparty risk

- Reduced single-asset NAV exposure to <15%

- ~20% of stream financings via syndicates (2024–25)

Diversified Sandstorm: 40+ operators, US$150M revolver, 120–150koz GEOs, <15% asset risk

Sandstorm relies on 12-country legal/advisors, 40+ operator partners, banks (US$150m revolver, 2024), technical consultants (due-diligence budget ~0.5–1.5% of deal), and syndicates (≈20% of stream financings 2024–25) to secure ~120–150 koz attributable GEOs and keep single-asset NAV exposure <15%.

| Partner | Key Metric | 2024–25 |

|---|---|---|

| Operators | Mines covered | 40+ |

| Banks | Revolver | US$150m |

| Output | Attributable GEOs | 120–150 koz |

| Syndication | Share of financings | ≈20% |

| Exposure | Single-asset NAV | <15% |

What is included in the product

A concise, investor-ready Business Model Canvas for Sandstorm Gold outlining customer segments, channels, value propositions, key partners, activities, resources, cost structure, and revenue streams aligned with its streaming/royalty model and growth strategy.

High-level one-page Business Model Canvas for Sandstorm Gold that condenses royalty-stream monetization, deal sourcing, investor relations, and risk mitigation into an editable, shareable layout—ideal for quick strategy reviews, team workshops, or investor presentations.

Activities

Capital Allocation and Investment

Capital allocation focuses on sourcing and valuing mining deals that need non-dilutive financing for future gold/silver production; management targets opportunities that boost NAV per share while capping exposure—Sandstorm reported $511.6m of cash and equivalents and 144 streaming/royalty interests as of Dec 31, 2024, guiding deployment decisions.

Decisions use disciplined DCF (discounted cash flow) valuation, scenario analysis, and commodity outlooks—gold averaged $2,078/oz in 2024—so teams balance IRR targets against portfolio risk, aiming for diversified geography and mine-stage mix to protect long-term returns.

Rigorous Due Diligence

Before signing deals, Sandstorm Gold runs exhaustive financial, technical and environmental reviews of the target mine and operator to spot red flags that could cut future gold deliveries or harm reputation; in 2024 the company reviewed 18 projects and rejected 7 for material risks. By 2025 Sandstorm increasingly adds advanced analytics and satellite monitoring—reducing due-diligence time by ~30% and improving early detection of operational shortfalls versus ground reports.

Portfolio Management and Monitoring

After acquiring a royalty or stream, Sandstorm Gold actively monitors operator performance via monthly production reports, quarterly site visits, and direct management calls; in 2024 the company reviewed 18 producing assets and received CAD 80m in streaming/royalty cash flows, so close tracking of reserve depletion and exploration progress is used to model forward cash flows and update NAV and payback timing.

Investor Relations and Capital Raising

Investor relations and capital raising keep Sandstorm Gold’s stock valuation and equity access intact; management highlights Q3 2025 revenue of US$32.4m and US$1.1bn market cap to show scale and liquidity.

They explain the royalty model to institutions and retail via quarterly reports, 12 investor conferences/year, and by stressing low G&A (US$28m FY2024) and asset growth from 220 royalties/streams.

- Q3 2025 revenue US$32.4m

- Market cap ~US$1.1bn

- FY2024 G&A US$28m

- 220 royalties/streams

- ~12 investor events/year

Strategic Acquisition of Royalties

- Purchased royalties accelerate cash flow vs. greenfield—typical deal adds US$2–10M annual EBITDA;

- Competition rose in 2025—royalty deal multiples up ~25% vs. 2022;

- Team must source, close quickly—average time-to-close for secondary royalties fell to 60 days in 2024.

Sandstorm: $511.6M cash, 144 royalties, Q3'25 rev $32.4M — market cap ~$1.1B

Sandstorm sources and values streaming/royalty deals, runs DCF and enviro/technical due diligence, closes secondary royalties fast, then monitors operator performance and updates NAV; as of Dec 31, 2024 cash US$511.6m, 144 interests, FY2024 G&A US$28m, 2024 cash flows CAD80m; Q3 2025 revenue US$32.4m, market cap ~US$1.1bn.

| Metric | Value |

|---|---|

| Cash | US$511.6m (12/31/2024) |

| Interests | 144 |

| FY2024 G&A | US$28m |

| 2024 cash flows | CAD80m |

| Q3 2025 rev | US$32.4m |

| Market cap | ~US$1.1bn |

Full Document Unlocks After Purchase

Business Model Canvas

The preview shown is the actual Sandstorm Gold Business Model Canvas—no mockup, no sample pages—it's a direct extract from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get this exact document in its full, editable form (Word and Excel where applicable), formatted and structured exactly as seen here for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Sandstorm Gold: Compact Business Model Canvas for Scalable, De-risked Streaming Revenue

Unlock the full strategic blueprint behind Sandstorm Gold’s business model—this concise Business Model Canvas shows how streaming royalties, low operating overhead, and targeted partnerships drive scalable, de-risked revenue for investors and operators; download the complete Word/Excel canvas for a section-by-section playbook you can use for benchmarking, investor decks, or strategic planning.

Partnerships

Primary Mining Operators

Primary mining operators manage on-site extraction and Sandstorm depends on their technical teams and local permitting skills to sustain production; by Q4 2025 Sandstorm’s streaming and royalty portfolio covers interests in over 40 operating mines and advanced projects, securing roughly 120–150 koz annual attributable gold equivalent ounces (GEOs).

Financial Institutions and Lenders

Financial institutions and lenders supply revolving credit lines and access to debt markets, enabling Sandstorm Gold to fund large upfront royalty purchases; for example, Sandstorm’s 2024 revolving facility capacity reached US$150m, supporting quick deals. These partners demand a strong balance sheet and steady cash flow—Sandstorm’s 2024 adjusted EBITDA of ~US$75m and net cash position underpin its borrowing capacity and timely execution.

Technical and Geological Consultants

Technical and geological consultants provide independent validation of reserves and project viability during due diligence, reducing Sandstorm Gold’s deal failure risk; in 2024 independent reserve revisions changed NPV estimates by up to 18% on comparable junior deals, so their input directly affects valuation of prospective streams.

The specialists flag engineering or environmental hurdles before capital is committed and their assessments support long-term sustainability of partner mines; Sandstorm typically budgets ~0.5–1.5% of deal value for such studies, cutting downstream remediation or redesign costs that can exceed 10% of capex.

Legal and Jurisdictional Advisors

Legal and jurisdictional advisors guide Sandstorm Gold across 12 countries, helping interpret cross-border mining laws and tax treaties to secure after-tax cash flows; they draft royalty agreements that include creditor-priority clauses and transfer protections to survive operator insolvency or 2025 ownership changes.

Advisors also map and certify ESG compliance—covering TC/ESG reporting, Scope 1–3 emissions alignment, and 2025 mandatory disclosures—to limit regulatory fines and protect royalty valuation.

- Cover 12 countries

- Draft creditor-priority royalty clauses

- Protect against operator insolvency

- Ensure 2025 ESG and Scope 1–3 reporting

Syndication and Co-Investment Partners

By 2025 Sandstorm Gold frequently syndicates with other royalty firms and private equity to underwrite very large streams, letting it access higher-value projects while capping exposure to any single mine; syndications accounted for roughly 20% of announced stream financing in 2024–25, helping keep Sandstorm’s single-asset exposure below 15% of NAV.

- Access large deals otherwise unaffordable

- Diversifies project and counterparty risk

- Reduced single-asset NAV exposure to <15%

- ~20% of stream financings via syndicates (2024–25)

Diversified Sandstorm: 40+ operators, US$150M revolver, 120–150koz GEOs, <15% asset risk

Sandstorm relies on 12-country legal/advisors, 40+ operator partners, banks (US$150m revolver, 2024), technical consultants (due-diligence budget ~0.5–1.5% of deal), and syndicates (≈20% of stream financings 2024–25) to secure ~120–150 koz attributable GEOs and keep single-asset NAV exposure <15%.

| Partner | Key Metric | 2024–25 |

|---|---|---|

| Operators | Mines covered | 40+ |

| Banks | Revolver | US$150m |

| Output | Attributable GEOs | 120–150 koz |

| Syndication | Share of financings | ≈20% |

| Exposure | Single-asset NAV | <15% |

What is included in the product

A concise, investor-ready Business Model Canvas for Sandstorm Gold outlining customer segments, channels, value propositions, key partners, activities, resources, cost structure, and revenue streams aligned with its streaming/royalty model and growth strategy.

High-level one-page Business Model Canvas for Sandstorm Gold that condenses royalty-stream monetization, deal sourcing, investor relations, and risk mitigation into an editable, shareable layout—ideal for quick strategy reviews, team workshops, or investor presentations.

Activities

Capital Allocation and Investment

Capital allocation focuses on sourcing and valuing mining deals that need non-dilutive financing for future gold/silver production; management targets opportunities that boost NAV per share while capping exposure—Sandstorm reported $511.6m of cash and equivalents and 144 streaming/royalty interests as of Dec 31, 2024, guiding deployment decisions.

Decisions use disciplined DCF (discounted cash flow) valuation, scenario analysis, and commodity outlooks—gold averaged $2,078/oz in 2024—so teams balance IRR targets against portfolio risk, aiming for diversified geography and mine-stage mix to protect long-term returns.

Rigorous Due Diligence

Before signing deals, Sandstorm Gold runs exhaustive financial, technical and environmental reviews of the target mine and operator to spot red flags that could cut future gold deliveries or harm reputation; in 2024 the company reviewed 18 projects and rejected 7 for material risks. By 2025 Sandstorm increasingly adds advanced analytics and satellite monitoring—reducing due-diligence time by ~30% and improving early detection of operational shortfalls versus ground reports.

Portfolio Management and Monitoring

After acquiring a royalty or stream, Sandstorm Gold actively monitors operator performance via monthly production reports, quarterly site visits, and direct management calls; in 2024 the company reviewed 18 producing assets and received CAD 80m in streaming/royalty cash flows, so close tracking of reserve depletion and exploration progress is used to model forward cash flows and update NAV and payback timing.

Investor Relations and Capital Raising

Investor relations and capital raising keep Sandstorm Gold’s stock valuation and equity access intact; management highlights Q3 2025 revenue of US$32.4m and US$1.1bn market cap to show scale and liquidity.

They explain the royalty model to institutions and retail via quarterly reports, 12 investor conferences/year, and by stressing low G&A (US$28m FY2024) and asset growth from 220 royalties/streams.

- Q3 2025 revenue US$32.4m

- Market cap ~US$1.1bn

- FY2024 G&A US$28m

- 220 royalties/streams

- ~12 investor events/year

Strategic Acquisition of Royalties

- Purchased royalties accelerate cash flow vs. greenfield—typical deal adds US$2–10M annual EBITDA;

- Competition rose in 2025—royalty deal multiples up ~25% vs. 2022;

- Team must source, close quickly—average time-to-close for secondary royalties fell to 60 days in 2024.

Sandstorm: $511.6M cash, 144 royalties, Q3'25 rev $32.4M — market cap ~$1.1B

Sandstorm sources and values streaming/royalty deals, runs DCF and enviro/technical due diligence, closes secondary royalties fast, then monitors operator performance and updates NAV; as of Dec 31, 2024 cash US$511.6m, 144 interests, FY2024 G&A US$28m, 2024 cash flows CAD80m; Q3 2025 revenue US$32.4m, market cap ~US$1.1bn.

| Metric | Value |

|---|---|

| Cash | US$511.6m (12/31/2024) |

| Interests | 144 |

| FY2024 G&A | US$28m |

| 2024 cash flows | CAD80m |

| Q3 2025 rev | US$32.4m |

| Market cap | ~US$1.1bn |

Full Document Unlocks After Purchase

Business Model Canvas

The preview shown is the actual Sandstorm Gold Business Model Canvas—no mockup, no sample pages—it's a direct extract from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get this exact document in its full, editable form (Word and Excel where applicable), formatted and structured exactly as seen here for immediate use.