Sandvik Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

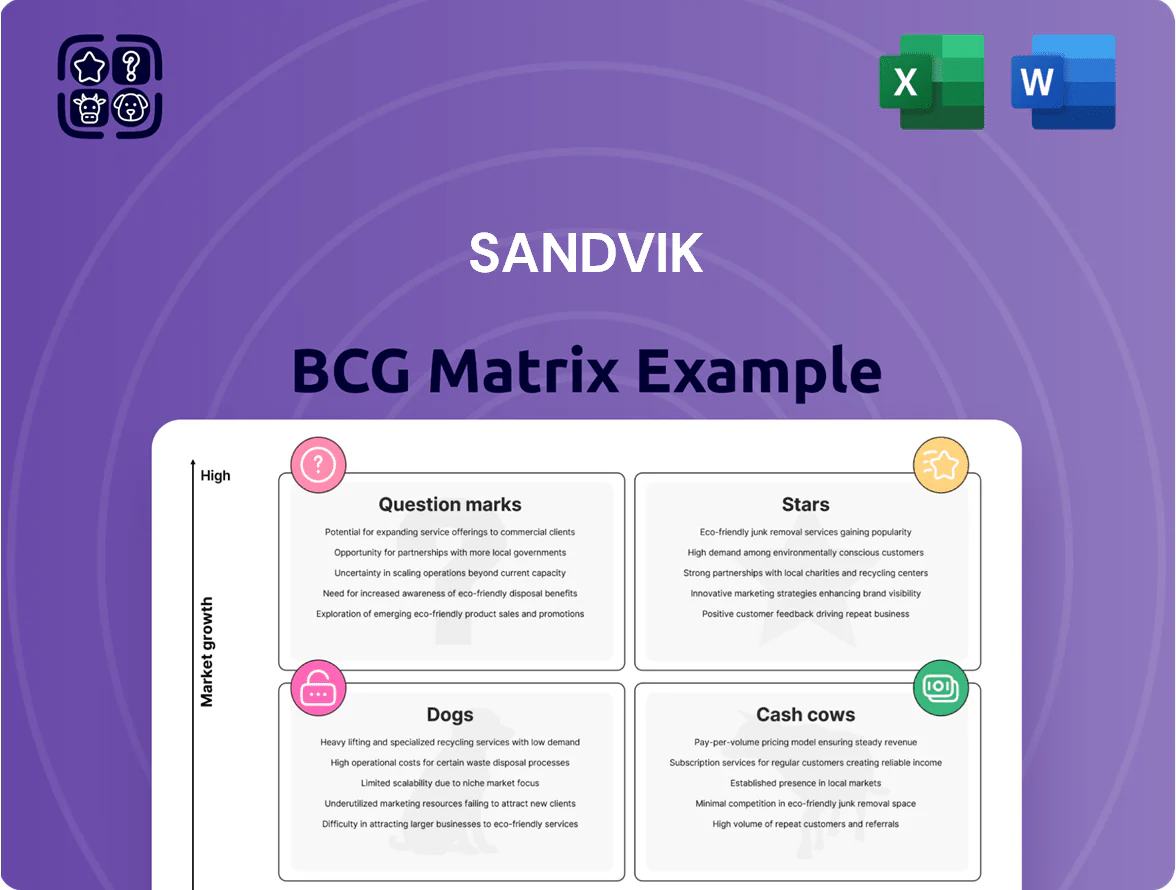

Sandvik’s BCG Matrix snapshot highlights where key product lines sit amid shifting industrial demand—identifying potential Stars in high-growth segments, resilient Cash Cows financing R&D, underperforming Dogs, and high-risk Question Marks that need strategic bets. This concise preview points to strategic imbalance and opportunity across tooling, mining, and material technologies. Purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide allocation and growth decisions.

Stars

Battery-Electric Mining Vehicles

Sandvik reinforced leadership in electrification with record BEV orders in 2025, booking ~SEK 3.2bn (Q1–Q3 2025 cumulative orders for electrified equipment), driving strong revenue mix in Mining and Rock Solutions.

BEVs capture high-growth demand as miners push decarbonization and cut underground ventilation costs by 30–60%, boosting total cost of ownership vs diesel.

These products need heavy R&D and capex—Sandvik spent SEK 4.1bn on R&D 2024 and increased BEV program capex in 2025—yet they signal the division’s future.

Digital Mining Technologies

Digital Mining Technologies posted double-digit organic growth in 2025, with Sandvik reporting ~12–15% unit growth as AutoMine autonomous platforms and Deswik mine-planning software saw accelerated adoption across 40+ major underground sites.

As a market leader in underground automation, Sandvik now captures a substantial share of the fast-growing digital mine ecosystem, with TAM expansion estimated at ~8–10% CAGR through 2028.

The high growth requires continuous capex and R&D spend—Sandvik increased digital R&D by mid-single digits of revenue in 2025—but a shift to subscription recurring revenue raised gross margins by ~200–400 basis points versus product sales.

Aerospace Machining Solutions

In 2025 the aerospace machining segment was a Star for Sandvik, growing ~12% y/y vs industrials ~4%, driven by global aircraft deliveries rising 8% and defense spending up 6% (IATA/Stockholm Intl. Aero stats).

Sandvik’s specialty tools and powder-metallurgy alloys held an estimated 28% global market share in aero machining, with segment EBIT margins near 18%, outperforming group average.

Ongoing fleet renewal and narrowbody demand support high growth and high share, keeping this Star despite broader macro risk.

Advanced Powder Solutions

Advanced Powder Solutions sits as a Star in Sandvik’s BCG matrix after double-digit revenue growth in 2025, with powder sales up 18% year-on-year and EBITDA margin around 22%, driven by global tungsten scarcity and rising demand for specialty alloys.

Sandvik’s integrated supply chain — owning European tungsten mines plus downstream processing — cuts lead times and price exposure, securing critical feedstock for high-end cutting tools and additive manufacturing parts.

- 2025 sales growth: +18%

- EBITDA margin: ~22%

- Advantages: own mines + Europe processing

- Uses: premium tooling, AM components

Surface Drilling Automation

In 2025 Sandvik advanced surface drilling automation, rolling out intelligent rotary blasthole drills and autonomous rigs that helped push surface mining revenue toward the company’s goal to double by 2028; surface segment sales grew ~18% year-over-year in 2025 to roughly SEK 12.6 billion, driven by automation demand.

Surface mines are adopting tech once limited to underground operations, expanding the addressable market—analysts estimate automated surface rig penetration rising from 6% in 2023 to 22% by 2028.

Sandvik leads this shift, investing capital and R&D to keep a first-to-market edge in automated surface platforms, with R&D spending in 2025 up ~14% to SEK 4.2 billion and targeted capex for surface automation projects of SEK 1.1 billion.

- 2025 surface sales ~SEK 12.6bn (+18%)

- R&D 2025 ~SEK 4.2bn (+14%)

- Targeted surface automation capex 2025 ~SEK 1.1bn

- Penetration forecast: 6% (2023) → 22% (2028)

Sandvik growth stars: BEV SEK3.2bn, Digital +12–15%, Aero +12% (EBIT18%), Powder +18%

Sandvik Stars: BEV orders ~SEK 3.2bn (Q1–Q3 2025), R&D SEK 4.1bn (2024) + capex 2025; Digital Mining growth ~12–15% units, TAM ~8–10% CAGR to 2028; Aerospace +12% y/y, 28% market share, EBIT ~18%; Advanced Powder +18% sales, EBITDA ~22%; Surface sales ~SEK 12.6bn (+18%), R&D 2025 SEK 4.2bn, surface capex SEK 1.1bn.

| Star | 2025 metric |

|---|---|

| BEV | SEK 3.2bn orders |

| Digital | 12–15% unit growth |

| Aero | +12% y/y, EBIT 18% |

| Powder | +18% sales, EBITDA 22% |

| Surface | SEK 12.6bn, +18% |

What is included in the product

Comprehensive BCG review of Sandvik’s portfolio with strategic guidance per quadrant—invest, hold, or divest—plus trend-driven risks and advantages.

One-page overview placing each Sandvik business unit in a quadrant for quick strategic decisions and stakeholder alignment

Cash Cows

Standard Metal-Cutting Tools

Sandvik Machining Solutions leads the global metal-cutting tools market, delivering Sandvik Group’s steadiest cash flow—about SEK 18.4 billion operating profit from tooling in 2024, roughly 28% of group EBIT.

Market maturity and slower general-engineering demand limit growth, but >30% global market share and strong brand loyalty sustain high margins with low incremental capex.

Free cash from tooling funded ~40% of Sandvik’s SEK 10.5 billion R&D and M&A spend on digital and electrification initiatives in 2024.

Mining Aftermarket Services

The parts, services, and consumables business for Sandvik’s global mining fleet delivers a highly predictable, profitable revenue stream, generating about SEK 25–28 billion in annual aftermarket revenue in 2024 (roughly 35–40% of Mining Division sales). With an aging installed base—global mining fleet average age rising and installed machines up ~6% year-on-year—this segment sees high customer retention and recurring sales. It’s the primary cash generator that helped cover fixed costs during the 2020–2023 equipment downturns and supported EBITDA margin stability above 15% in 2024.

Underground Hard-Rock Excavation

Sandvik’s underground hard‑rock drilling and loading holds a dominant, mature share—about 25–30% global market share in 2024—driving steady aftermarket revenue; 2024 segment EBITDA margins exceeded 20%, reflecting scale and service income.

Rock Processing Equipment

Sandvik Rock Processing Equipment is a cash cow: traditional crushing and screening for infrastructure and aggregates delivered steady revenue, with 2024 aftermarket sales ~45% of segment sales supporting margins near Sandvik Mining and Rock Technology’s 2024 adjusted EBITA margin of ~18%.

The mature market and a global installed base of tens of thousands of units ensure continuous service and spare-part orders, funding R&D and sustaining the Rock Processing Solutions strategy.

- Stable demand: infrastructure & aggregates

- Aftermarket ~45% of segment sales (2024)

- Adjusted EBITA margin ~18% (2024)

- Large global installed base → recurring service revenue

Round Tools for General Engineering

As a co-leader in global round tools, Sandvik captures roughly 18% of a $10.5bn global metalcutting market (2024), with steady demand from automotive, aerospace, and energy—making this a classic cash cow.

The mature product line needs limited R&D vs digital suites; focus is on yield improvement, supply-chain efficiency, and aftermarket channels to preserve margins around 16–18% EBITDA.

Net cash from this segment funds dividends and services corporate debt—estimated annual free cash flow contribution ~SEK 6–8bn (2024), cushioning cyclical swings.

- Market share ~18% of $10.5bn (2024)

- EBITDA margin ~16–18%

- Free cash flow ~SEK 6–8bn (2024)

Sandvik’s tooling, aftermarket & rock processing: steady cash cows funding growth

Sandvik tooling, aftermarket parts, and rock processing are core cash cows, generating steady free cash flow (tooling ~SEK 18.4bn op profit; aftermarket mining SEK 25–28bn revenue; rock processing EBITA ~18% in 2024) and funding R&D/M&A (~SEK 10.5bn) plus dividends and debt service.

| Segment | 2024 key metric | Margin/FCF |

|---|---|---|

| Tooling | SEK 18.4bn op profit | Funds ~SEK 6–8bn FCF |

| Mining aftermarket | SEK 25–28bn revenue | EBITDA >15% |

| Rock processing | Aftermarket ~45% sales | Adj EBITA ~18% |

What You’re Viewing Is Included

Sandvik BCG Matrix

The file you're previewing is the exact Sandvik BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic decision-making and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Sandvik’s BCG Matrix snapshot highlights where key product lines sit amid shifting industrial demand—identifying potential Stars in high-growth segments, resilient Cash Cows financing R&D, underperforming Dogs, and high-risk Question Marks that need strategic bets. This concise preview points to strategic imbalance and opportunity across tooling, mining, and material technologies. Purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide allocation and growth decisions.

Stars

Battery-Electric Mining Vehicles

Sandvik reinforced leadership in electrification with record BEV orders in 2025, booking ~SEK 3.2bn (Q1–Q3 2025 cumulative orders for electrified equipment), driving strong revenue mix in Mining and Rock Solutions.

BEVs capture high-growth demand as miners push decarbonization and cut underground ventilation costs by 30–60%, boosting total cost of ownership vs diesel.

These products need heavy R&D and capex—Sandvik spent SEK 4.1bn on R&D 2024 and increased BEV program capex in 2025—yet they signal the division’s future.

Digital Mining Technologies

Digital Mining Technologies posted double-digit organic growth in 2025, with Sandvik reporting ~12–15% unit growth as AutoMine autonomous platforms and Deswik mine-planning software saw accelerated adoption across 40+ major underground sites.

As a market leader in underground automation, Sandvik now captures a substantial share of the fast-growing digital mine ecosystem, with TAM expansion estimated at ~8–10% CAGR through 2028.

The high growth requires continuous capex and R&D spend—Sandvik increased digital R&D by mid-single digits of revenue in 2025—but a shift to subscription recurring revenue raised gross margins by ~200–400 basis points versus product sales.

Aerospace Machining Solutions

In 2025 the aerospace machining segment was a Star for Sandvik, growing ~12% y/y vs industrials ~4%, driven by global aircraft deliveries rising 8% and defense spending up 6% (IATA/Stockholm Intl. Aero stats).

Sandvik’s specialty tools and powder-metallurgy alloys held an estimated 28% global market share in aero machining, with segment EBIT margins near 18%, outperforming group average.

Ongoing fleet renewal and narrowbody demand support high growth and high share, keeping this Star despite broader macro risk.

Advanced Powder Solutions

Advanced Powder Solutions sits as a Star in Sandvik’s BCG matrix after double-digit revenue growth in 2025, with powder sales up 18% year-on-year and EBITDA margin around 22%, driven by global tungsten scarcity and rising demand for specialty alloys.

Sandvik’s integrated supply chain — owning European tungsten mines plus downstream processing — cuts lead times and price exposure, securing critical feedstock for high-end cutting tools and additive manufacturing parts.

- 2025 sales growth: +18%

- EBITDA margin: ~22%

- Advantages: own mines + Europe processing

- Uses: premium tooling, AM components

Surface Drilling Automation

In 2025 Sandvik advanced surface drilling automation, rolling out intelligent rotary blasthole drills and autonomous rigs that helped push surface mining revenue toward the company’s goal to double by 2028; surface segment sales grew ~18% year-over-year in 2025 to roughly SEK 12.6 billion, driven by automation demand.

Surface mines are adopting tech once limited to underground operations, expanding the addressable market—analysts estimate automated surface rig penetration rising from 6% in 2023 to 22% by 2028.

Sandvik leads this shift, investing capital and R&D to keep a first-to-market edge in automated surface platforms, with R&D spending in 2025 up ~14% to SEK 4.2 billion and targeted capex for surface automation projects of SEK 1.1 billion.

- 2025 surface sales ~SEK 12.6bn (+18%)

- R&D 2025 ~SEK 4.2bn (+14%)

- Targeted surface automation capex 2025 ~SEK 1.1bn

- Penetration forecast: 6% (2023) → 22% (2028)

Sandvik growth stars: BEV SEK3.2bn, Digital +12–15%, Aero +12% (EBIT18%), Powder +18%

Sandvik Stars: BEV orders ~SEK 3.2bn (Q1–Q3 2025), R&D SEK 4.1bn (2024) + capex 2025; Digital Mining growth ~12–15% units, TAM ~8–10% CAGR to 2028; Aerospace +12% y/y, 28% market share, EBIT ~18%; Advanced Powder +18% sales, EBITDA ~22%; Surface sales ~SEK 12.6bn (+18%), R&D 2025 SEK 4.2bn, surface capex SEK 1.1bn.

| Star | 2025 metric |

|---|---|

| BEV | SEK 3.2bn orders |

| Digital | 12–15% unit growth |

| Aero | +12% y/y, EBIT 18% |

| Powder | +18% sales, EBITDA 22% |

| Surface | SEK 12.6bn, +18% |

What is included in the product

Comprehensive BCG review of Sandvik’s portfolio with strategic guidance per quadrant—invest, hold, or divest—plus trend-driven risks and advantages.

One-page overview placing each Sandvik business unit in a quadrant for quick strategic decisions and stakeholder alignment

Cash Cows

Standard Metal-Cutting Tools

Sandvik Machining Solutions leads the global metal-cutting tools market, delivering Sandvik Group’s steadiest cash flow—about SEK 18.4 billion operating profit from tooling in 2024, roughly 28% of group EBIT.

Market maturity and slower general-engineering demand limit growth, but >30% global market share and strong brand loyalty sustain high margins with low incremental capex.

Free cash from tooling funded ~40% of Sandvik’s SEK 10.5 billion R&D and M&A spend on digital and electrification initiatives in 2024.

Mining Aftermarket Services

The parts, services, and consumables business for Sandvik’s global mining fleet delivers a highly predictable, profitable revenue stream, generating about SEK 25–28 billion in annual aftermarket revenue in 2024 (roughly 35–40% of Mining Division sales). With an aging installed base—global mining fleet average age rising and installed machines up ~6% year-on-year—this segment sees high customer retention and recurring sales. It’s the primary cash generator that helped cover fixed costs during the 2020–2023 equipment downturns and supported EBITDA margin stability above 15% in 2024.

Underground Hard-Rock Excavation

Sandvik’s underground hard‑rock drilling and loading holds a dominant, mature share—about 25–30% global market share in 2024—driving steady aftermarket revenue; 2024 segment EBITDA margins exceeded 20%, reflecting scale and service income.

Rock Processing Equipment

Sandvik Rock Processing Equipment is a cash cow: traditional crushing and screening for infrastructure and aggregates delivered steady revenue, with 2024 aftermarket sales ~45% of segment sales supporting margins near Sandvik Mining and Rock Technology’s 2024 adjusted EBITA margin of ~18%.

The mature market and a global installed base of tens of thousands of units ensure continuous service and spare-part orders, funding R&D and sustaining the Rock Processing Solutions strategy.

- Stable demand: infrastructure & aggregates

- Aftermarket ~45% of segment sales (2024)

- Adjusted EBITA margin ~18% (2024)

- Large global installed base → recurring service revenue

Round Tools for General Engineering

As a co-leader in global round tools, Sandvik captures roughly 18% of a $10.5bn global metalcutting market (2024), with steady demand from automotive, aerospace, and energy—making this a classic cash cow.

The mature product line needs limited R&D vs digital suites; focus is on yield improvement, supply-chain efficiency, and aftermarket channels to preserve margins around 16–18% EBITDA.

Net cash from this segment funds dividends and services corporate debt—estimated annual free cash flow contribution ~SEK 6–8bn (2024), cushioning cyclical swings.

- Market share ~18% of $10.5bn (2024)

- EBITDA margin ~16–18%

- Free cash flow ~SEK 6–8bn (2024)

Sandvik’s tooling, aftermarket & rock processing: steady cash cows funding growth

Sandvik tooling, aftermarket parts, and rock processing are core cash cows, generating steady free cash flow (tooling ~SEK 18.4bn op profit; aftermarket mining SEK 25–28bn revenue; rock processing EBITA ~18% in 2024) and funding R&D/M&A (~SEK 10.5bn) plus dividends and debt service.

| Segment | 2024 key metric | Margin/FCF |

|---|---|---|

| Tooling | SEK 18.4bn op profit | Funds ~SEK 6–8bn FCF |

| Mining aftermarket | SEK 25–28bn revenue | EBITDA >15% |

| Rock processing | Aftermarket ~45% sales | Adj EBITA ~18% |

What You’re Viewing Is Included

Sandvik BCG Matrix

The file you're previewing is the exact Sandvik BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic decision-making and professional presentation.