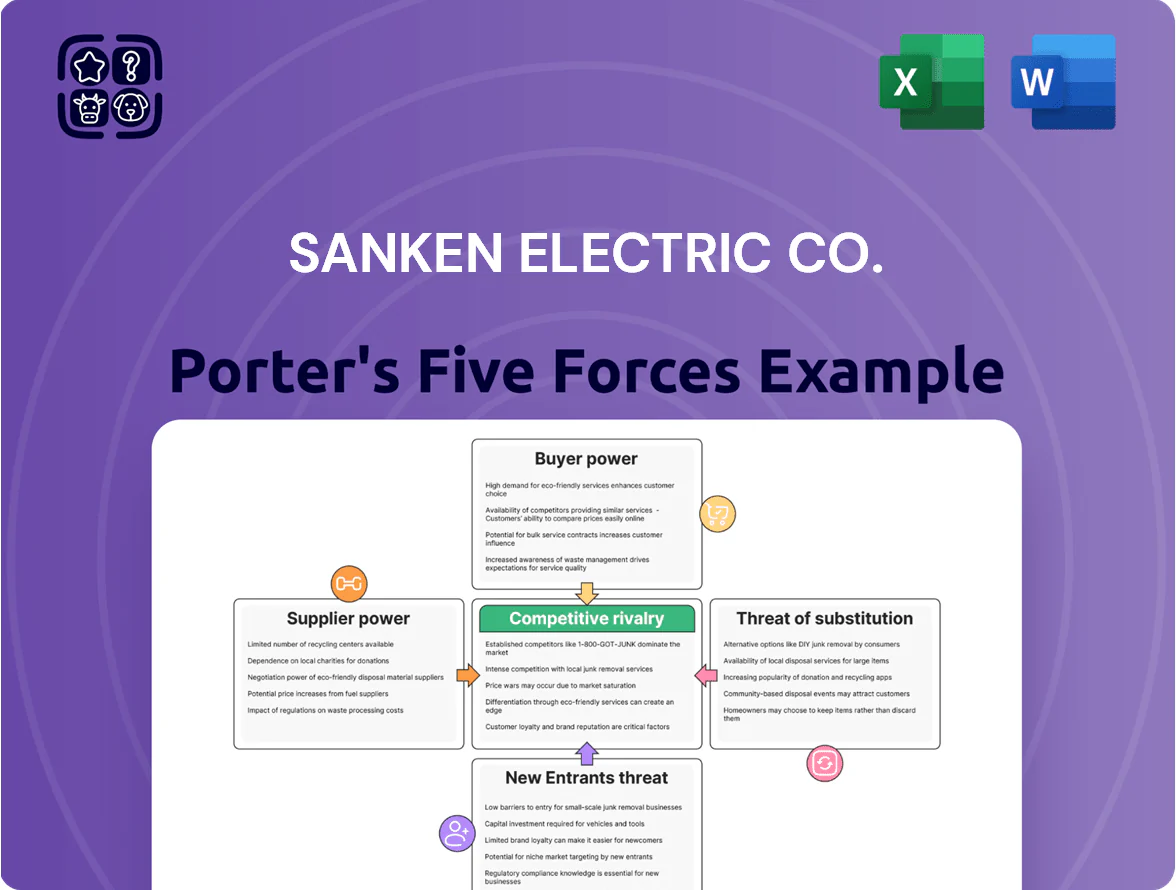

Sanken Electric Co. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sanken Electric faces moderate competitive rivalry driven by specialized power electronics and tight OEM relationships, while supplier power is tempered by component commoditization and supplier diversification.

Buyer power varies—large industrial clients demand customization and price sensitivity, and barriers to entry remain moderate due to capital and technical requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sanken Electric Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Sanken Electric depends on specialized materials—silicon wafers, gallium nitride (GaN), and silicon carbide (SiC)—that face global supply swings; GaN and SiC spot prices rose ~18%–25% in 2024 amid tight capacity. Suppliers of high‑purity substrates hold leverage because certified sources number in the low single digits, raising switching costs. By late 2025, commodity price stability is vital: a 10% input price rise could cut semiconductor segment gross margin by ~3–4 percentage points.

Dependence on specialized equipment manufacturers

The production of advanced power semiconductors relies on lithography and etching tools from a few global vendors (ASML, Tokyo Electron, Applied Materials), giving suppliers high bargaining power; switching costs exceed $100M per fab line and capex lead times of 12–36 months raise dependency.

Energy costs for fabrication facilities

Operating Sanken Electric’s fabrication plants is highly energy-intensive, so utility pricing directly lifts COGS; Japan industrial electricity prices rose about 12% from 2021–2024, reaching ~JPY 28/kWh in 2024, squeezing margins for power-electronics makers.

Global hubs show similar trends: Taiwan and South Korea saw 8–10% increases, raising input cost volatility for Sanken’s export lines.

Switching to alternative on-site generation or storage is capital-heavy and slow, so utility suppliers keep steady bargaining power over Sanken in 2025.

Concentration of high-end substrate vendors

As Sanken shifts to GaN and SiC, qualified substrate suppliers shrink to a few specialists—market share: top 3 vendors control ~70% of GaN/SiC substrates as of 2025—giving them pricing power for automotive and industrial-grade wafers.

Those suppliers can set higher prices and tighter lead times because their substrates are critical for high-efficiency modules, limiting Sanken’s leverage without risking supply security for flagship product lines.

- Top-3 suppliers ≈70% GaN/SiC share (2025)

- Specialty substrate price premiums 20–40% vs. silicon

- Switching costs high; qualification cycles 6–18 months

- Supply concentration raises supply-disruption risk for Sanken

Geopolitical influence on supply logistics

Suppliers in regions with trade curbs or instability force Sanken Electric to reroute procurement, raising lead times and inventory carrying costs; by end-2025, export controls on semiconductor inputs pushed many firms to add dual sources, increasing procurement spend by an estimated 6–10% industry-wide.

That shift boosts bargaining power for suppliers in stable jurisdictions—those vendors command 8–15% price premiums for guaranteed delivery and certifications, squeezing Sanken’s margins unless it pays or vertically secures supply.

- 6–10% higher procurement cost (industry avg, 2025)

- 8–15% price premium from 'safe' suppliers

- Diversification raises inventory and lead-time risk

Sanken squeezed by supplier oligopoly: substrate premiums, rising costs shave margins

Sanken faces high supplier power: top‑3 GaN/SiC substrate makers hold ~70% share (2025), specialty substrate premiums 20–40%, lithography tool switching >$100M, Japan industrial power ≈JPY28/kWh (2024). Procurement costs rose 6–10% (2025); safe‑supplier premiums 8–15%, and a 10% input price hike cuts semiconductor gross margin ~3–4 pts.

| Metric | Value |

|---|---|

| Top‑3 GaN/SiC share | ≈70% (2025) |

| Substrate premium | 20–40% |

| Procurement rise | 6–10% (2025) |

| Power price Japan | JPY28/kWh (2024) |

What is included in the product

Tailored Porter's Five Forces for Sanken Electric Co.: assesses competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and highlights disruptive technologies and market dynamics shaping its pricing power and profitability.

A clear, one-sheet Porter's Five Forces summary for Sanken Electric—quickly spot supplier power, rivalry intensity, and threat of substitutes to inform strategic decisions.

Customers Bargaining Power

Concentration of major automotive OEMs

High price sensitivity in consumer electronics

High price sensitivity in home appliances squeezes margins for Sanken Electric Co.; global appliance OEM gross margins averaged about 8–12% in 2024, so component cost changes of even 1–2% matter. Buyers of washing machines and air conditioners routinely benchmark Sanken’s power modules against competitors, creating commoditization and driving price-based procurement. This buyer leverage forces Sanken to trim prices to capture large-volume contracts—Sanken’s electronic device segment saw only 3.5% operating margin in FY2024, reflecting this pressure.

Customization and technical integration requirements

Customization binds large industrial clients but shifts bargaining power to them during design-in, since Sanken often tailors PMICs to specific architectures, incurring R&D and NRE costs—Sanken reported R&D expense of ¥20.3bn in FY2024, 12.4% of sales.

If a buyer pivots, Sanken risks stranded capacity and lost volumes: 2023 top-5 customers accounted for ~48% of sales, amplifying downside.

Availability of alternative semiconductor sources

The global power-semiconductor market has many competitors—Infineon, STMicroelectronics, Mitsubishi Electric, Rohm and others—giving buyers broad sourcing choices and lowering Sanken Electric Co.'s pricing power.

Large OEMs and distributors commonly use multi-sourcing to cut supply risk and force price concessions; procurement teams reported 10–18% savings from supplier competition in 2024–25.

By late 2025, chip supply stabilization shifted leverage back to buyers, with lead times down to 12–16 weeks from 30+ weeks in 2021–22, strengthening buyer bargaining power.

- Multiple global suppliers: Infineon, ST, Mitsubishi, Rohm

- Multi-sourcing saves 10–18% (2024–25)

- Lead times improved to 12–16 weeks by late 2025

Transparency in market pricing and benchmarks

The semiconductor market’s maturation has increased price transparency for power modules and discrete components; benchmark databases (e.g., TechInsights, IHS Markit) show average ASP declines of ~6–9% YoY for standard MOSFETs in 2024–25, enabling buyers to press Sanken Electric Co. on margins during renewals.

Buyers now cite market indices and spot prices to contest Sanken’s pricing models, making it hard for Sanken to keep premium pricing without proving tech differentiation such as SiC/GaN offerings or higher efficiency gains.

- Average selling price (ASP) pressure: –6–9% YoY (2024–25)

- Buyers use benchmarks (TechInsights, IHS) in renewals

- Premium pricing needs clear SiC/GaN or >10% efficiency delta

OEM concentration squeezes margins as multi-sourcing, price cuts and shorter lead times bite

Major OEMs concentrate buying power: top-5 customers ~48% of sales (2023) and ~55% of FY2024 revenue, forcing price concessions and tight quality/delivery terms; automotive segment margin squeezed ~3.8% in 2024. Multi-sourcing and many global competitors (Infineon, ST, Mitsubishi, Rohm) plus ASP pressure (–6–9% YoY for MOSFETs 2024–25) boost buyer leverage; lead times fell to 12–16 weeks by late 2025.

| Metric | Value |

|---|---|

| Top-5 customers (% sales, 2023) | ~48% |

| FY2024 revenue from major OEMs | ~55% |

| Auto margin squeeze (2024) | –3.8% pts |

| R&D (FY2024) | ¥20.3bn (12.4% sales) |

| ASP pressure (MOSFETs, 2024–25) | –6–9% YoY |

| Procurement savings via multi-sourcing (2024–25) | 10–18% |

| Lead times (late 2025) | 12–16 weeks |

Preview Before You Purchase

Sanken Electric Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Sanken Electric Co. you'll receive—fully formatted, professionally written, and ready for immediate download after purchase.

No samples or placeholders: the document displayed here is the complete deliverable you'll get instantly upon payment, covering competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers specific to Sanken Electric.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sanken Electric faces moderate competitive rivalry driven by specialized power electronics and tight OEM relationships, while supplier power is tempered by component commoditization and supplier diversification.

Buyer power varies—large industrial clients demand customization and price sensitivity, and barriers to entry remain moderate due to capital and technical requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sanken Electric Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Sanken Electric depends on specialized materials—silicon wafers, gallium nitride (GaN), and silicon carbide (SiC)—that face global supply swings; GaN and SiC spot prices rose ~18%–25% in 2024 amid tight capacity. Suppliers of high‑purity substrates hold leverage because certified sources number in the low single digits, raising switching costs. By late 2025, commodity price stability is vital: a 10% input price rise could cut semiconductor segment gross margin by ~3–4 percentage points.

Dependence on specialized equipment manufacturers

The production of advanced power semiconductors relies on lithography and etching tools from a few global vendors (ASML, Tokyo Electron, Applied Materials), giving suppliers high bargaining power; switching costs exceed $100M per fab line and capex lead times of 12–36 months raise dependency.

Energy costs for fabrication facilities

Operating Sanken Electric’s fabrication plants is highly energy-intensive, so utility pricing directly lifts COGS; Japan industrial electricity prices rose about 12% from 2021–2024, reaching ~JPY 28/kWh in 2024, squeezing margins for power-electronics makers.

Global hubs show similar trends: Taiwan and South Korea saw 8–10% increases, raising input cost volatility for Sanken’s export lines.

Switching to alternative on-site generation or storage is capital-heavy and slow, so utility suppliers keep steady bargaining power over Sanken in 2025.

Concentration of high-end substrate vendors

As Sanken shifts to GaN and SiC, qualified substrate suppliers shrink to a few specialists—market share: top 3 vendors control ~70% of GaN/SiC substrates as of 2025—giving them pricing power for automotive and industrial-grade wafers.

Those suppliers can set higher prices and tighter lead times because their substrates are critical for high-efficiency modules, limiting Sanken’s leverage without risking supply security for flagship product lines.

- Top-3 suppliers ≈70% GaN/SiC share (2025)

- Specialty substrate price premiums 20–40% vs. silicon

- Switching costs high; qualification cycles 6–18 months

- Supply concentration raises supply-disruption risk for Sanken

Geopolitical influence on supply logistics

Suppliers in regions with trade curbs or instability force Sanken Electric to reroute procurement, raising lead times and inventory carrying costs; by end-2025, export controls on semiconductor inputs pushed many firms to add dual sources, increasing procurement spend by an estimated 6–10% industry-wide.

That shift boosts bargaining power for suppliers in stable jurisdictions—those vendors command 8–15% price premiums for guaranteed delivery and certifications, squeezing Sanken’s margins unless it pays or vertically secures supply.

- 6–10% higher procurement cost (industry avg, 2025)

- 8–15% price premium from 'safe' suppliers

- Diversification raises inventory and lead-time risk

Sanken squeezed by supplier oligopoly: substrate premiums, rising costs shave margins

Sanken faces high supplier power: top‑3 GaN/SiC substrate makers hold ~70% share (2025), specialty substrate premiums 20–40%, lithography tool switching >$100M, Japan industrial power ≈JPY28/kWh (2024). Procurement costs rose 6–10% (2025); safe‑supplier premiums 8–15%, and a 10% input price hike cuts semiconductor gross margin ~3–4 pts.

| Metric | Value |

|---|---|

| Top‑3 GaN/SiC share | ≈70% (2025) |

| Substrate premium | 20–40% |

| Procurement rise | 6–10% (2025) |

| Power price Japan | JPY28/kWh (2024) |

What is included in the product

Tailored Porter's Five Forces for Sanken Electric Co.: assesses competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and highlights disruptive technologies and market dynamics shaping its pricing power and profitability.

A clear, one-sheet Porter's Five Forces summary for Sanken Electric—quickly spot supplier power, rivalry intensity, and threat of substitutes to inform strategic decisions.

Customers Bargaining Power

Concentration of major automotive OEMs

High price sensitivity in consumer electronics

High price sensitivity in home appliances squeezes margins for Sanken Electric Co.; global appliance OEM gross margins averaged about 8–12% in 2024, so component cost changes of even 1–2% matter. Buyers of washing machines and air conditioners routinely benchmark Sanken’s power modules against competitors, creating commoditization and driving price-based procurement. This buyer leverage forces Sanken to trim prices to capture large-volume contracts—Sanken’s electronic device segment saw only 3.5% operating margin in FY2024, reflecting this pressure.

Customization and technical integration requirements

Customization binds large industrial clients but shifts bargaining power to them during design-in, since Sanken often tailors PMICs to specific architectures, incurring R&D and NRE costs—Sanken reported R&D expense of ¥20.3bn in FY2024, 12.4% of sales.

If a buyer pivots, Sanken risks stranded capacity and lost volumes: 2023 top-5 customers accounted for ~48% of sales, amplifying downside.

Availability of alternative semiconductor sources

The global power-semiconductor market has many competitors—Infineon, STMicroelectronics, Mitsubishi Electric, Rohm and others—giving buyers broad sourcing choices and lowering Sanken Electric Co.'s pricing power.

Large OEMs and distributors commonly use multi-sourcing to cut supply risk and force price concessions; procurement teams reported 10–18% savings from supplier competition in 2024–25.

By late 2025, chip supply stabilization shifted leverage back to buyers, with lead times down to 12–16 weeks from 30+ weeks in 2021–22, strengthening buyer bargaining power.

- Multiple global suppliers: Infineon, ST, Mitsubishi, Rohm

- Multi-sourcing saves 10–18% (2024–25)

- Lead times improved to 12–16 weeks by late 2025

Transparency in market pricing and benchmarks

The semiconductor market’s maturation has increased price transparency for power modules and discrete components; benchmark databases (e.g., TechInsights, IHS Markit) show average ASP declines of ~6–9% YoY for standard MOSFETs in 2024–25, enabling buyers to press Sanken Electric Co. on margins during renewals.

Buyers now cite market indices and spot prices to contest Sanken’s pricing models, making it hard for Sanken to keep premium pricing without proving tech differentiation such as SiC/GaN offerings or higher efficiency gains.

- Average selling price (ASP) pressure: –6–9% YoY (2024–25)

- Buyers use benchmarks (TechInsights, IHS) in renewals

- Premium pricing needs clear SiC/GaN or >10% efficiency delta

OEM concentration squeezes margins as multi-sourcing, price cuts and shorter lead times bite

Major OEMs concentrate buying power: top-5 customers ~48% of sales (2023) and ~55% of FY2024 revenue, forcing price concessions and tight quality/delivery terms; automotive segment margin squeezed ~3.8% in 2024. Multi-sourcing and many global competitors (Infineon, ST, Mitsubishi, Rohm) plus ASP pressure (–6–9% YoY for MOSFETs 2024–25) boost buyer leverage; lead times fell to 12–16 weeks by late 2025.

| Metric | Value |

|---|---|

| Top-5 customers (% sales, 2023) | ~48% |

| FY2024 revenue from major OEMs | ~55% |

| Auto margin squeeze (2024) | –3.8% pts |

| R&D (FY2024) | ¥20.3bn (12.4% sales) |

| ASP pressure (MOSFETs, 2024–25) | –6–9% YoY |

| Procurement savings via multi-sourcing (2024–25) | 10–18% |

| Lead times (late 2025) | 12–16 weeks |

Preview Before You Purchase

Sanken Electric Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Sanken Electric Co. you'll receive—fully formatted, professionally written, and ready for immediate download after purchase.

No samples or placeholders: the document displayed here is the complete deliverable you'll get instantly upon payment, covering competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers specific to Sanken Electric.