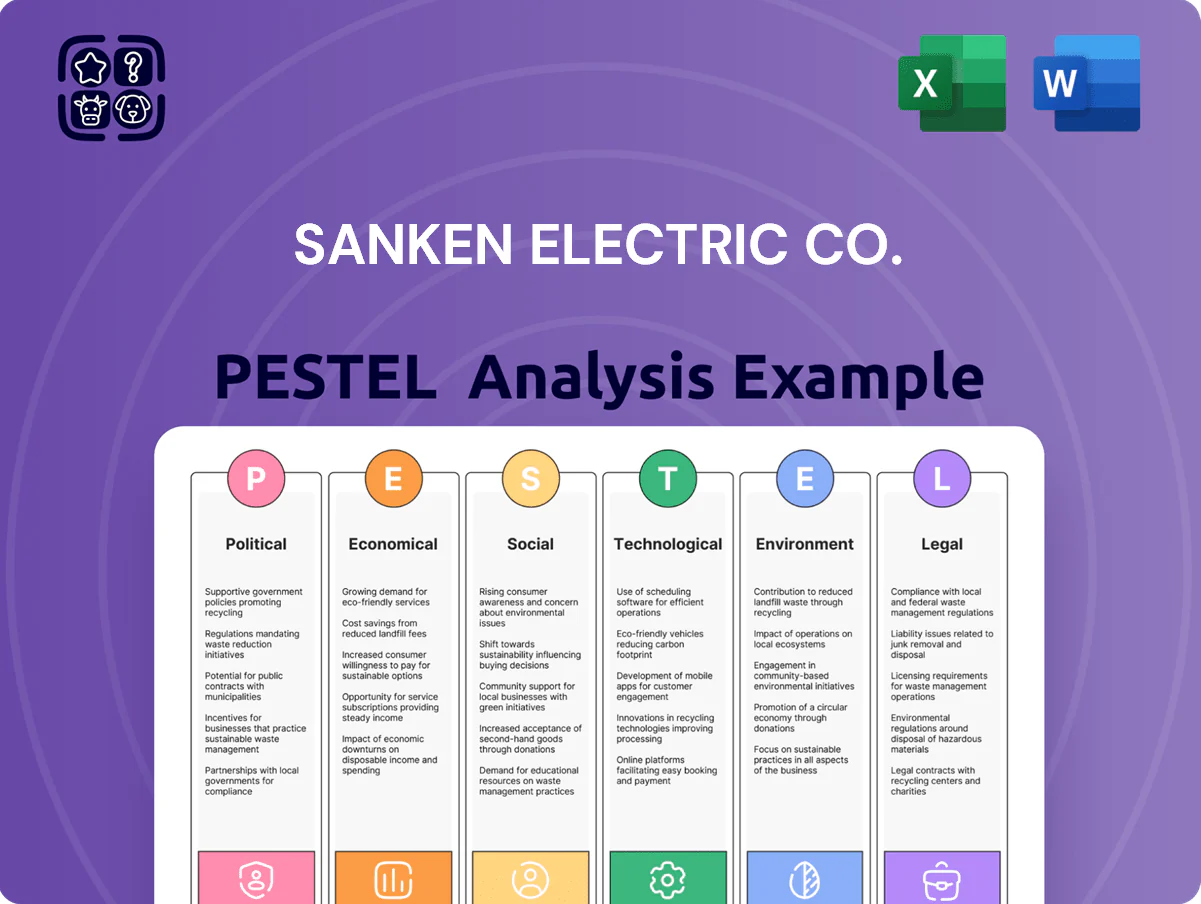

Sanken Electric Co. PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Sanken Electric Co.’s external landscape is shifting—regulatory changes, supply-chain pressures, and rapid electrification trends are reshaping its competitive edge and risk profile; our PESTLE highlights where opportunity and vulnerability meet. Purchase the full PESTLE for a sector-specific, actionable breakdown that investors and strategists can use immediately to inform decisions and de-risk plans.

Political factors

Global Trade Policy and Export Controls

The ongoing trade friction between the US, China and allies forces Sanken to navigate export controls on sensitive semiconductor tech, with Japan issuing 2024 tight controls affecting shipments to certain Chinese fabs and semiconductor-related exports rising 12% in value for Japan in 2024, increasing compliance cost and logistical risk.

Government Subsidies for Semiconductor Manufacturing

Governments in Japan, the US and EU have announced over USD 200 billion combined (Japan’s ~JPY 2.0 trillion 2023 package, US CHIPS Act ~$52.7 billion, EU’s IPCEI & recovery funds) to onshore semiconductor production and supply chains.

Sanken can access these subsidies to expand capacity—reducing capital outlay as fabs for power electronics and SiC/GaN devices scale to meet projected global power-semiconductor demand CAGR ~7–9% through 2028.

Political aims to cut foreign dependence and grow domestic high-tech industries improve Sanken’s incentive eligibility for grant, tax-credit and low-interest loan programs that accelerate next-generation facility investments.

Geopolitical Tensions in the Asia-Pacific Region

As Sanken Electric, with over 60% of manufacturing capacity in Asia, geopolitical tensions in the Asia-Pacific risk disruptions to maritime routes—notably the South China Sea, which handled about $3.4 trillion in trade in 2023—potentially interrupting shipment of substrates and gases used in semiconductor fabrication.

The company flags supply-chain exposure after 2022–24 regional incidents that raised freight insurance by up to 18% in 2024 and maintains contingency plans, dual-sourcing and inventory buffers to protect production in primary hubs.

National Security and Supply Chain Resilience

Semiconductors are now treated as national security assets; in 2024 Japan tightened FDI rules and added chip-related tech to export controls, raising scrutiny on M&A and partnerships affecting Sanken Electric’s power IC lines.

Sanken must align strategy with Japan’s 2024 National Security Policy to avoid regulatory blocks during international expansion, particularly in the US, EU, and ASEAN markets.

This political climate increases demand for secure, transparent supply chains; Sanken should document supplier provenance and compliance as buyers and regulators prioritize resilience—global chip export controls rose ~18% in 2023–24.

- Stricter FDI/export controls in 2024

- Alignment with Japan’s National Security Policy required

- Supply-chain transparency and provenance essential

- ~18% rise in chip-related export controls 2023–24

Decarbonization Policies and EV Mandates

- IEA: 26M EVs in 2023; ~40–50M by 2025

- Higher semiconductor content per EV increases TAM for power devices

- Policy-driven subsidies and mandates lower adoption barriers

- Sanken positioned to capture growth in EV and green energy supply chains

Geopolitics, subsidies and EV surge reshape $3.4T trade routes and chip demand

Political risks: export/FDI controls up ~18% (2023–24) constrain China exports; Japan’s 2024 security/controls and ~JPY2.0T package plus US CHIPS ~$52.7B/EU funds >$150B create subsidy access; Asia-Pacific maritime tensions threaten $3.4T trade routes; EV/renewable mandates (IEA: 26M EVs 2023; ~40–50M by 2025) expand power-semiconductor demand.

| Metric | Value |

|---|---|

| Export controls rise | ~18% (2023–24) |

| Japan package | ~JPY2.0T (2023) |

| US CHIPS | $52.7B |

| Trade via S. China Sea | $3.4T (2023) |

| EV stock | 26M (2023); 40–50M by 2025 |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces specifically shape Sanken Electric Co.’s operating landscape, with data-driven subpoints and regional industry context to reveal risks and opportunities.

A concise PESTLE snapshot of Sanken Electric that distills political, economic, social, technological, legal, and environmental factors into a single-slide friendly summary, helping teams quickly assess external risks and strategic levers during meetings or client briefings.

Economic factors

Fluctuations in Foreign Exchange Rates

As a Japan-based global exporter, Sanken's FY2024 revenue exposure rises as the Yen strengthened ~6% vs the US dollar in 2024, squeezing dollar-priced sales competitiveness and lifting JPY-based costs; a 5% yen appreciation historically cuts operating income by several percentage points for peers. Significant FX swings also raise imported semiconductor and copper input costs; Sanken uses forward contracts and currency options—hedging over 60% of forecasted FX exposure in 2024—to stabilize margins.

Capital Expenditure Trends in Industrial Automation

Global factory automation and Industry 4.0 investments lifted demand for power modules and motor control ICs, with global industrial automation spending projected at $270 billion in 2025 (IFR/Statista) supporting Sanken’s product lines.

Corporate capex cycles directly affect industrial-semiconductor sales; global manufacturing capex grew 6.8% in 2024, driving higher order volumes for industrial-grade components.

By end-2025, increased plant automation spend—forecasted to rise another 4–6%—is expected to remain a primary growth driver for Sanken, bolstering revenue exposure to motor-drive and power module markets.

Inflationary Pressure on Raw Material Costs

Rising prices for silicon (+22% YoY in 2024), copper (+18% in 2024) and specialty chemicals have compressed semiconductor gross margins industry-wide; Sanken reported a materials cost increase of ~16% in FY2024, pressuring margins.

To offset this, Sanken is focused on yield improvements and automation investments targeting a 7–10% production-cost reduction by 2026 while renegotiating long-term contract pricing to include inflation pass-through clauses.

Persistent energy inflation—power costs up ~12% in 2024—raises fab overhead, prompting Sanken to invest in energy-efficiency and on-site generation to stabilize unit costs.

Interest Rate Impacts on Consumer Spending

Global interest rates rose in 2024–2025, with the Fed funds rate averaging ~4.5% in 2024 and remaining elevated into 2025, reducing consumer credit affordability and dampening demand for high-ticket appliances and electronics that drive Sanken Electric’s power management chip sales.

Higher borrowing costs have correlated with slower appliance unit growth—global household appliance sales grew only ~1–2% in 2024—prompting Sanken to adjust forecasts and inventory across consumer segments.

Sanken tracks rate curve shifts and consumer financing trends to align production, inventory turnover, and chip allocation with anticipated lower-end-product demand.

- Fed funds ~4.5% in 2024; rates elevated into 2025

- Global appliance unit growth ~1–2% in 2024

- Sanken uses rate and financing data to adjust forecasts and inventory

Growth of the Electric Vehicle Market

The global EV stock surpassed 26 million in 2023 and is projected to reach ~145 million by 2030, driving semiconductor content per vehicle from ~$400 (ICE-era) toward $800–$1,200 for EVs; this shift creates a multi-decade addressable market for Sanken’s power semiconductors as automakers increase inverter, onboard charger and DC-DC demand.

Sanken has expanded automotive-qualified product lines and reported automotive revenue growth (mid-teens CAGR 2021–2024), positioning it to capture higher ASPs per vehicle despite near-term OEM cycle volatility and supply-chain normalization risks.

- EV stock: 26M (2023) → est. 145M (2030)

- Semiconductor content per EV: ~$800–$1,200

- Sanken automotive revenue: mid-teens CAGR 2021–2024

- Long-term structural tailwind vs short-term cyclical risk

Sanken weathers yen, higher materials; automation and EVs drive long‑term growth

Yen strength (≈+6% vs USD in 2024) cut competitiveness; Sanken hedged >60% FX exposure. Industrial automation spend ≈$270B (2025) and manufacturing capex +6.8% (2024) support demand. Materials: silicon +22%, copper +18% (2024); Sanken materials cost +16% (FY2024). Fed funds ≈4.5% (2024) damped appliance growth ~1–2%. EVs: 26M (2023) → est. 145M (2030); auto revenue mid‑teens CAGR (2021–24).

| Metric | Value |

|---|---|

| Yen vs USD (2024) | +6% |

| FX hedge | >60% |

| Materials cost rise | +16% |

| Fed funds (2024) | ≈4.5% |

| EV stock (2023) | 26M → 145M (2030) |

Preview Before You Purchase

Sanken Electric Co. PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Sanken Electric Co. you’ll receive after purchase—fully formatted and ready to use, with political, economic, social, technological, legal, and environmental factors analyzed.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Sanken Electric Co.’s external landscape is shifting—regulatory changes, supply-chain pressures, and rapid electrification trends are reshaping its competitive edge and risk profile; our PESTLE highlights where opportunity and vulnerability meet. Purchase the full PESTLE for a sector-specific, actionable breakdown that investors and strategists can use immediately to inform decisions and de-risk plans.

Political factors

Global Trade Policy and Export Controls

The ongoing trade friction between the US, China and allies forces Sanken to navigate export controls on sensitive semiconductor tech, with Japan issuing 2024 tight controls affecting shipments to certain Chinese fabs and semiconductor-related exports rising 12% in value for Japan in 2024, increasing compliance cost and logistical risk.

Government Subsidies for Semiconductor Manufacturing

Governments in Japan, the US and EU have announced over USD 200 billion combined (Japan’s ~JPY 2.0 trillion 2023 package, US CHIPS Act ~$52.7 billion, EU’s IPCEI & recovery funds) to onshore semiconductor production and supply chains.

Sanken can access these subsidies to expand capacity—reducing capital outlay as fabs for power electronics and SiC/GaN devices scale to meet projected global power-semiconductor demand CAGR ~7–9% through 2028.

Political aims to cut foreign dependence and grow domestic high-tech industries improve Sanken’s incentive eligibility for grant, tax-credit and low-interest loan programs that accelerate next-generation facility investments.

Geopolitical Tensions in the Asia-Pacific Region

As Sanken Electric, with over 60% of manufacturing capacity in Asia, geopolitical tensions in the Asia-Pacific risk disruptions to maritime routes—notably the South China Sea, which handled about $3.4 trillion in trade in 2023—potentially interrupting shipment of substrates and gases used in semiconductor fabrication.

The company flags supply-chain exposure after 2022–24 regional incidents that raised freight insurance by up to 18% in 2024 and maintains contingency plans, dual-sourcing and inventory buffers to protect production in primary hubs.

National Security and Supply Chain Resilience

Semiconductors are now treated as national security assets; in 2024 Japan tightened FDI rules and added chip-related tech to export controls, raising scrutiny on M&A and partnerships affecting Sanken Electric’s power IC lines.

Sanken must align strategy with Japan’s 2024 National Security Policy to avoid regulatory blocks during international expansion, particularly in the US, EU, and ASEAN markets.

This political climate increases demand for secure, transparent supply chains; Sanken should document supplier provenance and compliance as buyers and regulators prioritize resilience—global chip export controls rose ~18% in 2023–24.

- Stricter FDI/export controls in 2024

- Alignment with Japan’s National Security Policy required

- Supply-chain transparency and provenance essential

- ~18% rise in chip-related export controls 2023–24

Decarbonization Policies and EV Mandates

- IEA: 26M EVs in 2023; ~40–50M by 2025

- Higher semiconductor content per EV increases TAM for power devices

- Policy-driven subsidies and mandates lower adoption barriers

- Sanken positioned to capture growth in EV and green energy supply chains

Geopolitics, subsidies and EV surge reshape $3.4T trade routes and chip demand

Political risks: export/FDI controls up ~18% (2023–24) constrain China exports; Japan’s 2024 security/controls and ~JPY2.0T package plus US CHIPS ~$52.7B/EU funds >$150B create subsidy access; Asia-Pacific maritime tensions threaten $3.4T trade routes; EV/renewable mandates (IEA: 26M EVs 2023; ~40–50M by 2025) expand power-semiconductor demand.

| Metric | Value |

|---|---|

| Export controls rise | ~18% (2023–24) |

| Japan package | ~JPY2.0T (2023) |

| US CHIPS | $52.7B |

| Trade via S. China Sea | $3.4T (2023) |

| EV stock | 26M (2023); 40–50M by 2025 |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces specifically shape Sanken Electric Co.’s operating landscape, with data-driven subpoints and regional industry context to reveal risks and opportunities.

A concise PESTLE snapshot of Sanken Electric that distills political, economic, social, technological, legal, and environmental factors into a single-slide friendly summary, helping teams quickly assess external risks and strategic levers during meetings or client briefings.

Economic factors

Fluctuations in Foreign Exchange Rates

As a Japan-based global exporter, Sanken's FY2024 revenue exposure rises as the Yen strengthened ~6% vs the US dollar in 2024, squeezing dollar-priced sales competitiveness and lifting JPY-based costs; a 5% yen appreciation historically cuts operating income by several percentage points for peers. Significant FX swings also raise imported semiconductor and copper input costs; Sanken uses forward contracts and currency options—hedging over 60% of forecasted FX exposure in 2024—to stabilize margins.

Capital Expenditure Trends in Industrial Automation

Global factory automation and Industry 4.0 investments lifted demand for power modules and motor control ICs, with global industrial automation spending projected at $270 billion in 2025 (IFR/Statista) supporting Sanken’s product lines.

Corporate capex cycles directly affect industrial-semiconductor sales; global manufacturing capex grew 6.8% in 2024, driving higher order volumes for industrial-grade components.

By end-2025, increased plant automation spend—forecasted to rise another 4–6%—is expected to remain a primary growth driver for Sanken, bolstering revenue exposure to motor-drive and power module markets.

Inflationary Pressure on Raw Material Costs

Rising prices for silicon (+22% YoY in 2024), copper (+18% in 2024) and specialty chemicals have compressed semiconductor gross margins industry-wide; Sanken reported a materials cost increase of ~16% in FY2024, pressuring margins.

To offset this, Sanken is focused on yield improvements and automation investments targeting a 7–10% production-cost reduction by 2026 while renegotiating long-term contract pricing to include inflation pass-through clauses.

Persistent energy inflation—power costs up ~12% in 2024—raises fab overhead, prompting Sanken to invest in energy-efficiency and on-site generation to stabilize unit costs.

Interest Rate Impacts on Consumer Spending

Global interest rates rose in 2024–2025, with the Fed funds rate averaging ~4.5% in 2024 and remaining elevated into 2025, reducing consumer credit affordability and dampening demand for high-ticket appliances and electronics that drive Sanken Electric’s power management chip sales.

Higher borrowing costs have correlated with slower appliance unit growth—global household appliance sales grew only ~1–2% in 2024—prompting Sanken to adjust forecasts and inventory across consumer segments.

Sanken tracks rate curve shifts and consumer financing trends to align production, inventory turnover, and chip allocation with anticipated lower-end-product demand.

- Fed funds ~4.5% in 2024; rates elevated into 2025

- Global appliance unit growth ~1–2% in 2024

- Sanken uses rate and financing data to adjust forecasts and inventory

Growth of the Electric Vehicle Market

The global EV stock surpassed 26 million in 2023 and is projected to reach ~145 million by 2030, driving semiconductor content per vehicle from ~$400 (ICE-era) toward $800–$1,200 for EVs; this shift creates a multi-decade addressable market for Sanken’s power semiconductors as automakers increase inverter, onboard charger and DC-DC demand.

Sanken has expanded automotive-qualified product lines and reported automotive revenue growth (mid-teens CAGR 2021–2024), positioning it to capture higher ASPs per vehicle despite near-term OEM cycle volatility and supply-chain normalization risks.

- EV stock: 26M (2023) → est. 145M (2030)

- Semiconductor content per EV: ~$800–$1,200

- Sanken automotive revenue: mid-teens CAGR 2021–2024

- Long-term structural tailwind vs short-term cyclical risk

Sanken weathers yen, higher materials; automation and EVs drive long‑term growth

Yen strength (≈+6% vs USD in 2024) cut competitiveness; Sanken hedged >60% FX exposure. Industrial automation spend ≈$270B (2025) and manufacturing capex +6.8% (2024) support demand. Materials: silicon +22%, copper +18% (2024); Sanken materials cost +16% (FY2024). Fed funds ≈4.5% (2024) damped appliance growth ~1–2%. EVs: 26M (2023) → est. 145M (2030); auto revenue mid‑teens CAGR (2021–24).

| Metric | Value |

|---|---|

| Yen vs USD (2024) | +6% |

| FX hedge | >60% |

| Materials cost rise | +16% |

| Fed funds (2024) | ≈4.5% |

| EV stock (2023) | 26M → 145M (2030) |

Preview Before You Purchase

Sanken Electric Co. PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Sanken Electric Co. you’ll receive after purchase—fully formatted and ready to use, with political, economic, social, technological, legal, and environmental factors analyzed.