Sanlam PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Sanlam PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the insurer’s future; buy the full report to get actionable insights, risk forecasts, and ready-to-use slides for investment or strategy decisions.

Political factors

South African Governance Stability

The formation and continued operation of the Government of National Unity through 2025 has improved predictability for long-term capital allocation, supporting Sanlam as the Johannesburg Stock Exchange saw foreign net inflows of ZAR 18.6bn in 2024. Improved investor sentiment and government commitment to structural reforms have helped lower country risk premiums, aiding Sanlam’s asset management and life insurance investment strategies. The stable political backdrop reduces the likelihood of abrupt policy shifts that could harm the financial services sector or South Africa’s sovereign credit metrics, where Moody’s maintained a B2 rating with stable outlook in 2025.

Pan-African Integration and AfCFTA

The deepening AfCFTA lowers tariffs and non-tariff barriers across 54 signatory countries, easing cross-border operations for SanlamAllianz across Africa’s markets of ~1.4 billion people and a combined GDP of about $3.4 trillion (2023-24).

Political commitment to integration accelerates regulatory harmonization, enabling smoother capital movement between subsidiaries and reducing compliance costs by an estimated 5–10% in cross-border transactions.

Sanlam leverages these tailwinds to scale life and general insurance, targeting multi-jurisdiction launches that can tap growing insurance penetration (sub-Saharan Africa penetration ~2.5% vs global ~6%) to boost premium growth across the region.

Geopolitical Volatility in Emerging Markets

Political instability in parts of West and East Africa—where Sanlam holds subsidiaries representing roughly 8-12% of group revenue—continues to threaten localized operations and growth projections.

Ongoing conflicts and sudden regime changes risk economic disruption, asset expropriation and currency controls, with IMF reporting 2024 FX interventions in several African states rising 15% year-on-year.

Sanlam must therefore maintain robust political risk insurance and diversify portfolios across countries and asset classes to mitigate impacts from civil unrest or administrative shifts.

Regulatory Diplomacy in India

Sanlam’s strategic stake in Shriram Finance compels continuous engagement with Indian regulators as FDI rules evolved in 2023–2025, with India recording FDI inflows of USD 84.6bn in FY2023–24, affecting cross‑border capital movements.

India’s focus on financial inclusion—over 500m Jan Dhan accounts by 2024 and rising credit penetration—supports Sanlam’s credit and insurance expansion in the subcontinent.

Maintaining ties with local political stakeholders is critical to safeguard profit repatriation and scale further amid potential regulatory shifts.

- Sanlam–Shriram exposure requires active regulatory diplomacy

- FDI context: USD 84.6bn inflows FY2023–24

- Financial inclusion: 500m+ Jan Dhan accounts by 2024

- Local political relationships protect repatriation and expansion

Public-Private Partnership Initiatives

Governments in Sanlam’s key markets are shifting to private funding for infrastructure and social projects through 2025; Sanlam, as a major institutional investor, channels about ZAR 45–60bn annually into PPPs to align with national development agendas and secure political goodwill.

These PPPs offer Sanlam access to stable, long-term yields—often 6–9% real returns—while reinforcing its license to operate in developing economies and reducing sovereign risk exposure.

- Annual PPP investment: ZAR 45–60bn

- Typical real yields: 6–9%

- Strategic benefit: political alignment and enhanced operating license

South Africa: Stable politics, AfCFTA growth, PPPs yield 6–9% amid rising regional risk

Stable South African politics through 2025 improved investor inflows (ZAR 18.6bn in 2024) and lower country risk; AfCFTA boosts cross‑border scale across ~1.4bn people and $3.4tn GDP; regional instability (8–12% revenue exposure) and rising FX interventions (+15% YoY 2024) heighten political risk; PPPs (ZAR 45–60bn pa) offer 6–9% real yields supporting long‑term asset allocation.

| Metric | Value |

|---|---|

| JSE foreign inflows 2024 | ZAR 18.6bn |

| AfCFTA coverage | ~1.4bn people, $3.4tn GDP |

| Revenue exposure (unstable regions) | 8–12% |

| FX interventions change (2024) | +15% YoY |

| Annual PPP investment | ZAR 45–60bn |

| Typical PPP real yields | 6–9% |

What is included in the product

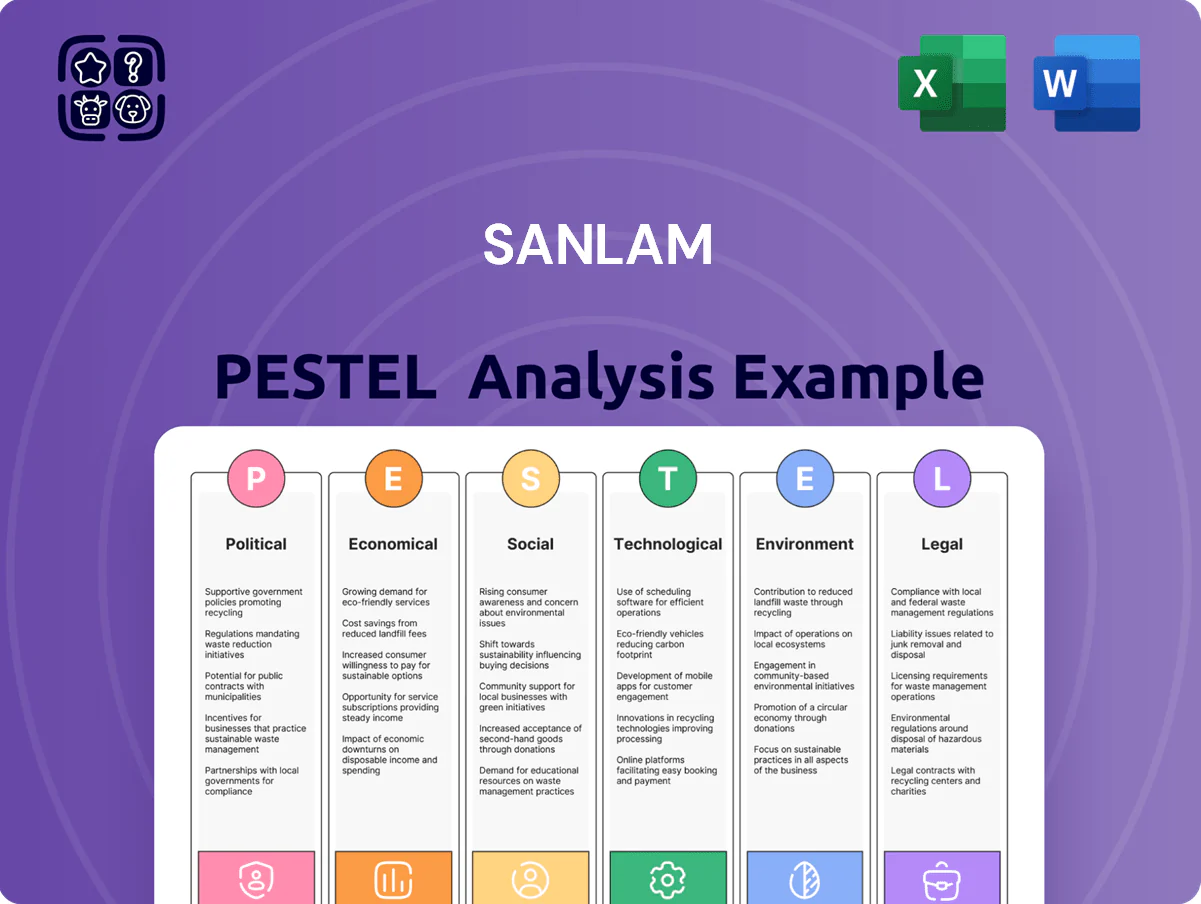

Explores how external macro-environmental factors uniquely affect Sanlam across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable Sanlam PESTLE summary that’s visually segmented by category for quick reference in meetings, easily dropped into presentations, and editable with notes for regional or business-line context.

Economic factors

Monetary Policy and Interest Rate Cycles

As global and South African policy rates began normalizing in late 2024 into 2025, Sanlam saw investment income recalibrated: South Africa's repo rate moved from 8.25% in Dec 2023 to 7.75% by Dec 2024, supporting equity gains and lifting AUM by 6% YoY to ~R1.2trn and wealth management fees accordingly.

Lower rates helped equity valuations, but margin compression on fixed-income products forced Sanlam to adopt advanced actuarial assumptions; lower bond yields pushed the yield on South African government bonds (10-yr) from ~9.6% in 2023 to ~8.2% in 2024, pressuring long-term life contract profitability.

Currency Volatility and Translation Risk

The South African Rand (ZAR) weakened ~8% vs USD in 2024, heightening translation risk across Sanlam’s African operations; volatility versus the Nigerian naira and Egyptian pound has driven marked earnings swings in recent quarters.

Sanlam uses layered currency hedges and non-deliverable forwards to shield reported earnings — management reported hedging reduced translation volatility by an estimated 60% in FY2024.

Significant devaluations in key markets can produce material translation losses or gains, affecting group equity ROE and dividend capacity; a 10% ZAR move can swing reported EPS by several percentage points given current African asset exposure.

Inflationary Pressure on Claims Costs

Persistent headline inflation in key African markets averaged 7.8% in 2024, pushing motor and property repair costs higher and increasing general insurance claim severity for Sanlam.

Sanlam must balance competitive premiums with rising replacement and operational costs to protect FY2024 underwriting margins, which faced pressure from higher loss ratios in short-term insurance.

Inflation-linked pricing—implemented across portfolios in 2024—remains critical to preserve sustainability of short-term insurance through 2025, as replacement-cost inflation outpaced wage inflation.

Emerging Market GDP Growth Trends

Emerging market GDP growth, notably India at ~7% real GDP in FY2024 and ASEAN-5 averaging ~4.5% in 2024–25, outpaces developed markets and fuels demand for retirement annuities and discretionary investments, supporting Sanlam’s expansion in these corridors.

Higher growth raises disposable incomes—India’s middle class rising toward 550m and Southeast Asia’s middle class at ~220m—boosting uptake of sophisticated financial products and offsetting sluggish developed-market momentum.

- India GDP ~7% (FY2024)

- ASEAN-5 ~4.5% (2024–25)

- India middle class ~550m

- SE Asia middle class ~220m

Capital Market Performance and Fee Income

Sanlam’s wealth and investment management revenue rose as global and South African equity markets climbed, with fee income up around 8–10% in 2024–25 as AUM exceeded ZAR 1.2 trillion, while market volatility continued to pressure net flows and retention.

Diversification into alternatives and private equity—now ~12% of institutional AUM—aims to deliver uncorrelated returns and stabilize fees, though liquidity and valuation risks remain during downturns.

- Fee income +8–10% (2024–25)

- AUM > ZAR 1.2 trillion

- Alternatives ~12% of institutional AUM

- Volatility risks pressure client retention

Normalization lifts AUM to ZAR1.25trn; margins squeezed as ZAR falls and inflation rises

Economic normalization in 2024–25 supported AUM growth to ~ZAR1.25trn and fee income +9% while lower bond yields (10y SA Govie ~8.2% in 2024) compressed long-term life margins; ZAR weakened ~8% vs USD in 2024 increasing translation risk, hedging cut volatility ~60%; emerging-market GDP (India ~7%, ASEAN-5 ~4.5%) boosted retail demand; inflation across key African markets averaged ~7.8% in 2024, raising claim severity.

| Metric | 2024/25 |

|---|---|

| AUM | ZAR1.25trn |

| Fee growth | +9% |

| SA 10y yield | ~8.2% |

| ZAR vs USD | -8% |

| Emerging GDP | India7% / ASEAN-5 4.5% |

| Avg inflation (Africa) | 7.8% |

Preview Before You Purchase

Sanlam PESTLE Analysis

The preview shown here is the exact Sanlam PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor briefings.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Sanlam PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the insurer’s future; buy the full report to get actionable insights, risk forecasts, and ready-to-use slides for investment or strategy decisions.

Political factors

South African Governance Stability

The formation and continued operation of the Government of National Unity through 2025 has improved predictability for long-term capital allocation, supporting Sanlam as the Johannesburg Stock Exchange saw foreign net inflows of ZAR 18.6bn in 2024. Improved investor sentiment and government commitment to structural reforms have helped lower country risk premiums, aiding Sanlam’s asset management and life insurance investment strategies. The stable political backdrop reduces the likelihood of abrupt policy shifts that could harm the financial services sector or South Africa’s sovereign credit metrics, where Moody’s maintained a B2 rating with stable outlook in 2025.

Pan-African Integration and AfCFTA

The deepening AfCFTA lowers tariffs and non-tariff barriers across 54 signatory countries, easing cross-border operations for SanlamAllianz across Africa’s markets of ~1.4 billion people and a combined GDP of about $3.4 trillion (2023-24).

Political commitment to integration accelerates regulatory harmonization, enabling smoother capital movement between subsidiaries and reducing compliance costs by an estimated 5–10% in cross-border transactions.

Sanlam leverages these tailwinds to scale life and general insurance, targeting multi-jurisdiction launches that can tap growing insurance penetration (sub-Saharan Africa penetration ~2.5% vs global ~6%) to boost premium growth across the region.

Geopolitical Volatility in Emerging Markets

Political instability in parts of West and East Africa—where Sanlam holds subsidiaries representing roughly 8-12% of group revenue—continues to threaten localized operations and growth projections.

Ongoing conflicts and sudden regime changes risk economic disruption, asset expropriation and currency controls, with IMF reporting 2024 FX interventions in several African states rising 15% year-on-year.

Sanlam must therefore maintain robust political risk insurance and diversify portfolios across countries and asset classes to mitigate impacts from civil unrest or administrative shifts.

Regulatory Diplomacy in India

Sanlam’s strategic stake in Shriram Finance compels continuous engagement with Indian regulators as FDI rules evolved in 2023–2025, with India recording FDI inflows of USD 84.6bn in FY2023–24, affecting cross‑border capital movements.

India’s focus on financial inclusion—over 500m Jan Dhan accounts by 2024 and rising credit penetration—supports Sanlam’s credit and insurance expansion in the subcontinent.

Maintaining ties with local political stakeholders is critical to safeguard profit repatriation and scale further amid potential regulatory shifts.

- Sanlam–Shriram exposure requires active regulatory diplomacy

- FDI context: USD 84.6bn inflows FY2023–24

- Financial inclusion: 500m+ Jan Dhan accounts by 2024

- Local political relationships protect repatriation and expansion

Public-Private Partnership Initiatives

Governments in Sanlam’s key markets are shifting to private funding for infrastructure and social projects through 2025; Sanlam, as a major institutional investor, channels about ZAR 45–60bn annually into PPPs to align with national development agendas and secure political goodwill.

These PPPs offer Sanlam access to stable, long-term yields—often 6–9% real returns—while reinforcing its license to operate in developing economies and reducing sovereign risk exposure.

- Annual PPP investment: ZAR 45–60bn

- Typical real yields: 6–9%

- Strategic benefit: political alignment and enhanced operating license

South Africa: Stable politics, AfCFTA growth, PPPs yield 6–9% amid rising regional risk

Stable South African politics through 2025 improved investor inflows (ZAR 18.6bn in 2024) and lower country risk; AfCFTA boosts cross‑border scale across ~1.4bn people and $3.4tn GDP; regional instability (8–12% revenue exposure) and rising FX interventions (+15% YoY 2024) heighten political risk; PPPs (ZAR 45–60bn pa) offer 6–9% real yields supporting long‑term asset allocation.

| Metric | Value |

|---|---|

| JSE foreign inflows 2024 | ZAR 18.6bn |

| AfCFTA coverage | ~1.4bn people, $3.4tn GDP |

| Revenue exposure (unstable regions) | 8–12% |

| FX interventions change (2024) | +15% YoY |

| Annual PPP investment | ZAR 45–60bn |

| Typical PPP real yields | 6–9% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sanlam across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable Sanlam PESTLE summary that’s visually segmented by category for quick reference in meetings, easily dropped into presentations, and editable with notes for regional or business-line context.

Economic factors

Monetary Policy and Interest Rate Cycles

As global and South African policy rates began normalizing in late 2024 into 2025, Sanlam saw investment income recalibrated: South Africa's repo rate moved from 8.25% in Dec 2023 to 7.75% by Dec 2024, supporting equity gains and lifting AUM by 6% YoY to ~R1.2trn and wealth management fees accordingly.

Lower rates helped equity valuations, but margin compression on fixed-income products forced Sanlam to adopt advanced actuarial assumptions; lower bond yields pushed the yield on South African government bonds (10-yr) from ~9.6% in 2023 to ~8.2% in 2024, pressuring long-term life contract profitability.

Currency Volatility and Translation Risk

The South African Rand (ZAR) weakened ~8% vs USD in 2024, heightening translation risk across Sanlam’s African operations; volatility versus the Nigerian naira and Egyptian pound has driven marked earnings swings in recent quarters.

Sanlam uses layered currency hedges and non-deliverable forwards to shield reported earnings — management reported hedging reduced translation volatility by an estimated 60% in FY2024.

Significant devaluations in key markets can produce material translation losses or gains, affecting group equity ROE and dividend capacity; a 10% ZAR move can swing reported EPS by several percentage points given current African asset exposure.

Inflationary Pressure on Claims Costs

Persistent headline inflation in key African markets averaged 7.8% in 2024, pushing motor and property repair costs higher and increasing general insurance claim severity for Sanlam.

Sanlam must balance competitive premiums with rising replacement and operational costs to protect FY2024 underwriting margins, which faced pressure from higher loss ratios in short-term insurance.

Inflation-linked pricing—implemented across portfolios in 2024—remains critical to preserve sustainability of short-term insurance through 2025, as replacement-cost inflation outpaced wage inflation.

Emerging Market GDP Growth Trends

Emerging market GDP growth, notably India at ~7% real GDP in FY2024 and ASEAN-5 averaging ~4.5% in 2024–25, outpaces developed markets and fuels demand for retirement annuities and discretionary investments, supporting Sanlam’s expansion in these corridors.

Higher growth raises disposable incomes—India’s middle class rising toward 550m and Southeast Asia’s middle class at ~220m—boosting uptake of sophisticated financial products and offsetting sluggish developed-market momentum.

- India GDP ~7% (FY2024)

- ASEAN-5 ~4.5% (2024–25)

- India middle class ~550m

- SE Asia middle class ~220m

Capital Market Performance and Fee Income

Sanlam’s wealth and investment management revenue rose as global and South African equity markets climbed, with fee income up around 8–10% in 2024–25 as AUM exceeded ZAR 1.2 trillion, while market volatility continued to pressure net flows and retention.

Diversification into alternatives and private equity—now ~12% of institutional AUM—aims to deliver uncorrelated returns and stabilize fees, though liquidity and valuation risks remain during downturns.

- Fee income +8–10% (2024–25)

- AUM > ZAR 1.2 trillion

- Alternatives ~12% of institutional AUM

- Volatility risks pressure client retention

Normalization lifts AUM to ZAR1.25trn; margins squeezed as ZAR falls and inflation rises

Economic normalization in 2024–25 supported AUM growth to ~ZAR1.25trn and fee income +9% while lower bond yields (10y SA Govie ~8.2% in 2024) compressed long-term life margins; ZAR weakened ~8% vs USD in 2024 increasing translation risk, hedging cut volatility ~60%; emerging-market GDP (India ~7%, ASEAN-5 ~4.5%) boosted retail demand; inflation across key African markets averaged ~7.8% in 2024, raising claim severity.

| Metric | 2024/25 |

|---|---|

| AUM | ZAR1.25trn |

| Fee growth | +9% |

| SA 10y yield | ~8.2% |

| ZAR vs USD | -8% |

| Emerging GDP | India7% / ASEAN-5 4.5% |

| Avg inflation (Africa) | 7.8% |

Preview Before You Purchase

Sanlam PESTLE Analysis

The preview shown here is the exact Sanlam PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor briefings.