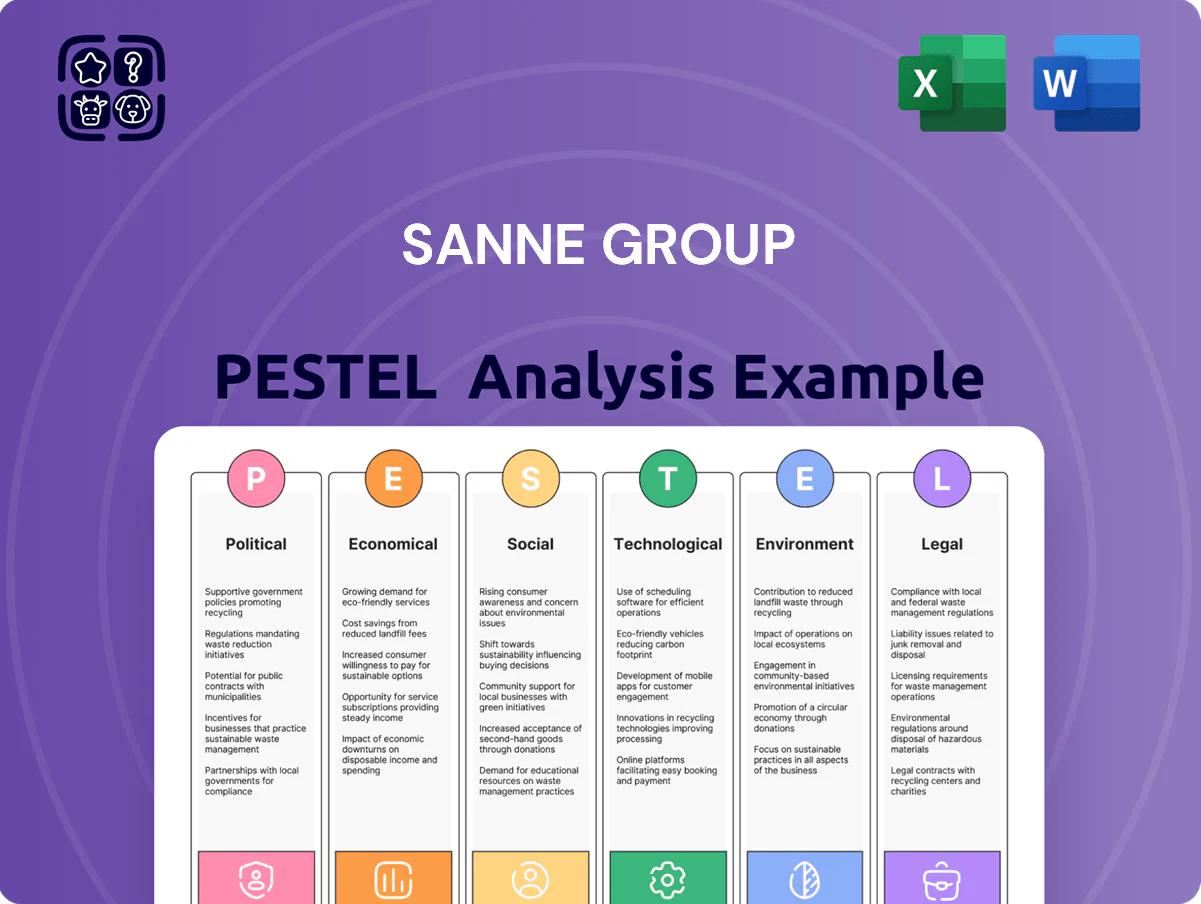

Sanne Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock the strategic landscape surrounding Sanne Group with our comprehensive PESTLE analysis. Understand how political shifts, economic volatility, and technological advancements are redefining the financial services sector, directly impacting Sanne's operations and future growth. Download the full PESTLE analysis now to gain actionable intelligence and refine your own strategic approach.

Political factors

Geopolitical Instability and Trade Policies

Geopolitical instability and evolving trade policies, exemplified by ongoing trade disputes and the potential for further tariffs, create significant headwinds for global investment flows. For alternative asset managers like Apex Group, which now includes Sanne Group, this translates into a need to rigorously re-evaluate regional investment allocations and strengthen risk management through sophisticated hedging strategies. The dynamic nature of these political factors necessitates continuous adaptation to safeguard investor capital.

Government Support for Investment Sectors

Government policies significantly shape investment landscapes. For instance, the US Inflation Reduction Act of 2022, with its substantial tax credits for clean energy, has driven billions in new private investment into sectors like solar and battery manufacturing. This demonstrates how shifts in government priorities, such as supporting critical minerals or infrastructure development, can directly channel capital and create lucrative opportunities for alternative investment firms.

Changes in Financial Services Administration

Shifts in political leadership, particularly within financial regulatory bodies, directly influence the oversight and enforcement priorities for the financial services sector. For instance, a new administration coming into power in 2024 or 2025 might champion a deregulatory approach, potentially easing compliance burdens or re-prioritizing areas like data privacy and cybersecurity enforcement.

International Cooperation on Financial Regulation

International cooperation significantly shapes the landscape of financial regulation, influencing how global firms operate. The degree to which countries align their rules, particularly in areas like sustainable finance and data privacy, directly affects the complexity of compliance for international service providers. For instance, the Financial Stability Board (FSB) actively promotes international cooperation to foster consistent regulatory approaches, aiming to reduce fragmentation. However, divergence remains a challenge; by the end of 2024, differing national implementations of Basel III reforms continued to present varied capital requirements for banks globally, impacting cross-border financial activities.

Navigating these varied frameworks is crucial for companies like Sanne Group, which provides alternative asset administration. Discrepancies in regulations, such as the varying timelines for implementing ESG disclosure requirements across the EU, UK, and US, can necessitate tailored compliance strategies for each market. This can increase operational costs and introduce risks if not managed effectively.

- Harmonization Efforts: The G20 and international standard-setting bodies like the International Organization of Securities Commissions (IOSCO) are continuously working towards greater harmonization of financial regulations.

- Divergence Challenges: Differing national approaches to areas like digital asset regulation or cross-border data transfer can create compliance burdens for global financial service providers.

- Sustainable Finance Standards: The evolving global standards for sustainable finance, such as the ISSB standards, require adaptation from asset managers and administrators to meet diverse investor and regulatory expectations by 2025.

- Data Privacy Regulations: Variations in data privacy laws, like GDPR in Europe and similar frameworks emerging in other regions, necessitate robust data governance to ensure compliance across all operating jurisdictions.

Political Focus on Economic Competitiveness

Governments globally are sharpening their focus on economic growth and competitiveness. This heightened priority directly shapes the legislative landscape, particularly for sectors like green finance. For instance, the UK's Autumn Statement 2023 outlined measures to boost investment and economic growth, potentially influencing the speed of new environmental regulations.

This political emphasis can lead to a more measured approach to introducing new legislation, or conversely, a drive to optimize existing regulatory frameworks for greater efficiency. Financial institutions like Sanne Group may see this translate into a period of regulatory stability or a push to enhance the practical application of current rules, impacting operational strategies and service offerings.

Key political considerations for economic competitiveness influencing financial services include:

- Government initiatives promoting investment: Many nations are implementing tax incentives and funding programs to attract capital, which can benefit financial service providers. For example, the EU's NextGenerationEU recovery plan aims to stimulate economic activity and digital transformation.

- Regulatory streamlining efforts: To foster competitiveness, governments may review and simplify existing regulations, making it easier for businesses to operate and innovate.

- Focus on specific growth sectors: Policies often target areas like renewable energy or digital infrastructure, creating opportunities and demands for specialized financial services.

- International trade agreements: These can impact cross-border financial flows and regulatory alignment, affecting firms with international operations.

Policy & Geopolitics: Shaping Financial Services

Political stability and government policies are paramount for financial services firms like Sanne Group. For example, the UK's commitment to net-zero targets by 2050, reinforced by policies announced in 2024, creates demand for green finance administration services. Conversely, geopolitical tensions, such as those impacting supply chains in 2024, can lead to increased market volatility, necessitating robust risk management for alternative assets.

Governments are increasingly focused on regulatory alignment to foster international trade and investment. The ongoing efforts by bodies like the Financial Stability Board (FSB) to harmonize prudential standards, particularly in light of the 2023 banking sector stresses, directly impact how firms like Sanne Group manage capital and cross-border operations. By 2025, continued progress in this harmonization is expected to simplify compliance for globally operating entities.

| Policy Area | Impact on Sanne Group | Example/Data Point (2024/2025 Focus) |

|---|---|---|

| Sustainable Finance Regulation | Increased demand for ESG reporting and administration services. | The EU Taxonomy Regulation, with phased implementation continuing through 2025, requires detailed environmental impact reporting for eligible assets. |

| Digital Asset Regulation | Need for specialized administration and compliance for crypto and tokenized assets. | MiCA (Markets in Crypto-Assets) regulation in the EU, fully applicable by late 2024, sets a precedent for digital asset oversight globally. |

| Tax Policy Changes | Potential shifts in investment attractiveness and operational costs. | Anticipated adjustments to capital gains tax or corporate tax rates in major economies by 2025 could influence fund structures and investor decisions. |

| Geopolitical Risk Mitigation | Requirement for enhanced due diligence and diversified investment strategies. | Ongoing global trade disputes and regional conflicts in 2024 necessitate careful monitoring of asset locations and counterparty risk. |

What is included in the product

This PESTLE analysis provides a comprehensive examination of the external macro-environmental factors influencing the Sanne Group, covering Political, Economic, Social, Technological, Environmental, and Legal dimensions.

It offers a strategic framework for understanding how these global forces create both challenges and opportunities for Sanne's business operations and future growth.

The Sanne Group PESTLE Analysis offers a streamlined, easily digestible summary, alleviating the pain point of sifting through dense reports for critical strategic insights.

Economic factors

Private Equity Dealmaking Resurgence

The private equity market is showing strong signs of recovery in 2024, with expectations for continued momentum into 2025. This resurgence is largely attributed to easing inflationary pressures and a more stable interest rate environment, which are reducing previous dealmaking uncertainties.

This uptick in activity, particularly with larger transactions and a greater number of successful exits, directly benefits fund administrators like Sanne Group. The increased volume of deals, including a notable rise in megadeals, translates into higher demand for specialized services in areas such as transaction support, fund accounting, and regulatory compliance.

Global private equity deal volume saw a substantial increase in 2024, with reports indicating a significant rebound from the slower pace of previous years. For instance, some analyses suggest that global PE deal value in the first half of 2024 could surpass the entirety of 2023, underscoring the renewed confidence and capital deployment within the sector.

Interest Rate Environment and Credit Markets

The current interest rate environment, with many central banks signaling potential easing in 2025, is a significant tailwind for credit markets. This shift is expected to lower borrowing costs, making it easier for private equity firms to finance acquisitions. For instance, the European Central Bank has indicated a pivot towards rate cuts, which will likely translate into more accessible and affordable debt for leveraged buyouts throughout 2025.

A more robust credit market, characterized by increased liquidity and a willingness from lenders to provide capital, directly fuels deal execution. Private equity sponsors are benefiting from this open credit access, a trend that is projected to drive a notable increase in dealmaking activity in 2025. The competitive landscape within direct lending markets is also a key factor, creating avenues for value creation through more favorable financing terms.

Inflationary Pressures and Economic Growth

Stabilizing economic growth and a noticeable decline in inflation are painting a more optimistic picture for financial markets. For instance, the US Consumer Price Index (CPI) saw a moderation in its year-over-year increase, falling to 3.1% in January 2024, a significant drop from its peak. This macroeconomic stability helps to lower uncertainty for investors, encouraging continued investment, particularly in alternative assets.

While the overall economic environment is improving, financial services firms must remain vigilant about their operational costs. The lingering effects of past inflationary periods mean that expenses related to technology, talent, and compliance can still present challenges. For example, while wage growth may be moderating, the cost of specialized financial expertise remains high.

Increased Dry Powder in Alternative Investments

The alternative investment landscape is awash with capital, with record-high levels of dry powder in private equity. This signifies a substantial pool of unallocated funds ready for deployment, creating a fertile ground for deal-making. As of the first half of 2024, private equity dry powder reached an estimated $2.5 trillion globally, a figure that has steadily climbed over the past few years.

This abundance of capital exerts considerable pressure on financial sponsors to identify and execute transactions. The drive to deploy this capital efficiently fuels increased M&A activity within the private markets. Consequently, this heightened deal flow directly translates into a greater demand for specialized administration services that support these complex transactions.

The robust fundraising environment further amplifies this trend. For instance, 2023 saw private equity firms raise over $1.2 trillion globally, demonstrating continued investor confidence and capital availability. This sustained influx of funds ensures that the pressure to deploy dry powder will persist, benefiting service providers.

- Record Dry Powder: Global private equity dry powder estimated at $2.5 trillion in H1 2024.

- Increased Deal Pressure: Sponsors are incentivized to complete transactions to deploy capital.

- Robust Fundraising: Over $1.2 trillion raised by PE firms in 2023, indicating sustained capital inflow.

- Demand for Administration: Higher deal volumes drive demand for specialized financial administration services.

Liquidity Demands from Limited Partners

Limited partners (LPs) are increasingly prioritizing liquidity, putting pressure on general partners (GPs) to secure profitable exit opportunities and return invested capital. This trend is particularly evident in the private equity space, where LPs are looking for ways to monetize their holdings more efficiently.

The heightened demand for liquidity is spurring the adoption of alternative exit strategies. Continuation funds, which allow existing investors to sell their stakes to a new fund managed by the same sponsor, and sponsor-to-sponsor sales are becoming more common. These methods offer GPs a way to provide liquidity to their LPs while potentially retaining valuable assets.

This shift is expected to act as a catalyst for renewed fundraising across various alternative asset classes. As LPs seek greater liquidity, they may allocate more capital to funds that demonstrate a clear path to exits and capital repatriation. For instance, Preqin data from early 2024 indicated a growing interest in secondary market transactions, a key component of liquidity solutions for LPs.

- Increased LP focus on liquidity: LPs are actively seeking to monetize their private market investments.

- Rise of alternative exits: Continuation funds and sponsor-to-sponsor deals are gaining traction as liquidity solutions.

- Catalyst for fundraising: The demand for liquidity is anticipated to boost capital raising for alternative asset managers.

- Secondary market activity: Data suggests a significant uptick in secondary transactions as LPs aim to exit investments.

Private Equity Surges: Economic Tailwinds Boost Deal Flow

Economic factors are currently favorable for Sanne Group, with stabilizing growth and moderating inflation reducing deal uncertainty. The anticipated easing of interest rates in 2025 is expected to lower borrowing costs, directly benefiting private equity firms and increasing deal activity.

The robust fundraising environment, with over $1.2 trillion raised by PE firms in 2023 and record dry powder of $2.5 trillion in H1 2024, creates significant pressure to deploy capital. This heightened deal flow directly translates into increased demand for specialized administration services that Sanne Group provides.

The market is experiencing a strong recovery in private equity dealmaking, with expectations for continued momentum into 2025 due to easing inflation and more stable interest rates. This resurgence, marked by larger transactions and successful exits, directly benefits fund administrators like Sanne Group through increased demand for their specialized services.

The current economic climate, characterized by moderating inflation and potential interest rate cuts in 2025, is a significant tailwind for financial markets. For instance, the US CPI fell to 3.1% in January 2024, down from its peak, fostering greater investor confidence and encouraging investment in alternative assets.

Preview Before You Purchase

Sanne Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of the Sanne Group provides a comprehensive overview of the external factors influencing its operations and strategic decisions. You'll gain insights into the Political, Economic, Social, Technological, Legal, and Environmental landscape impacting the company.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock the strategic landscape surrounding Sanne Group with our comprehensive PESTLE analysis. Understand how political shifts, economic volatility, and technological advancements are redefining the financial services sector, directly impacting Sanne's operations and future growth. Download the full PESTLE analysis now to gain actionable intelligence and refine your own strategic approach.

Political factors

Geopolitical Instability and Trade Policies

Geopolitical instability and evolving trade policies, exemplified by ongoing trade disputes and the potential for further tariffs, create significant headwinds for global investment flows. For alternative asset managers like Apex Group, which now includes Sanne Group, this translates into a need to rigorously re-evaluate regional investment allocations and strengthen risk management through sophisticated hedging strategies. The dynamic nature of these political factors necessitates continuous adaptation to safeguard investor capital.

Government Support for Investment Sectors

Government policies significantly shape investment landscapes. For instance, the US Inflation Reduction Act of 2022, with its substantial tax credits for clean energy, has driven billions in new private investment into sectors like solar and battery manufacturing. This demonstrates how shifts in government priorities, such as supporting critical minerals or infrastructure development, can directly channel capital and create lucrative opportunities for alternative investment firms.

Changes in Financial Services Administration

Shifts in political leadership, particularly within financial regulatory bodies, directly influence the oversight and enforcement priorities for the financial services sector. For instance, a new administration coming into power in 2024 or 2025 might champion a deregulatory approach, potentially easing compliance burdens or re-prioritizing areas like data privacy and cybersecurity enforcement.

International Cooperation on Financial Regulation

International cooperation significantly shapes the landscape of financial regulation, influencing how global firms operate. The degree to which countries align their rules, particularly in areas like sustainable finance and data privacy, directly affects the complexity of compliance for international service providers. For instance, the Financial Stability Board (FSB) actively promotes international cooperation to foster consistent regulatory approaches, aiming to reduce fragmentation. However, divergence remains a challenge; by the end of 2024, differing national implementations of Basel III reforms continued to present varied capital requirements for banks globally, impacting cross-border financial activities.

Navigating these varied frameworks is crucial for companies like Sanne Group, which provides alternative asset administration. Discrepancies in regulations, such as the varying timelines for implementing ESG disclosure requirements across the EU, UK, and US, can necessitate tailored compliance strategies for each market. This can increase operational costs and introduce risks if not managed effectively.

- Harmonization Efforts: The G20 and international standard-setting bodies like the International Organization of Securities Commissions (IOSCO) are continuously working towards greater harmonization of financial regulations.

- Divergence Challenges: Differing national approaches to areas like digital asset regulation or cross-border data transfer can create compliance burdens for global financial service providers.

- Sustainable Finance Standards: The evolving global standards for sustainable finance, such as the ISSB standards, require adaptation from asset managers and administrators to meet diverse investor and regulatory expectations by 2025.

- Data Privacy Regulations: Variations in data privacy laws, like GDPR in Europe and similar frameworks emerging in other regions, necessitate robust data governance to ensure compliance across all operating jurisdictions.

Political Focus on Economic Competitiveness

Governments globally are sharpening their focus on economic growth and competitiveness. This heightened priority directly shapes the legislative landscape, particularly for sectors like green finance. For instance, the UK's Autumn Statement 2023 outlined measures to boost investment and economic growth, potentially influencing the speed of new environmental regulations.

This political emphasis can lead to a more measured approach to introducing new legislation, or conversely, a drive to optimize existing regulatory frameworks for greater efficiency. Financial institutions like Sanne Group may see this translate into a period of regulatory stability or a push to enhance the practical application of current rules, impacting operational strategies and service offerings.

Key political considerations for economic competitiveness influencing financial services include:

- Government initiatives promoting investment: Many nations are implementing tax incentives and funding programs to attract capital, which can benefit financial service providers. For example, the EU's NextGenerationEU recovery plan aims to stimulate economic activity and digital transformation.

- Regulatory streamlining efforts: To foster competitiveness, governments may review and simplify existing regulations, making it easier for businesses to operate and innovate.

- Focus on specific growth sectors: Policies often target areas like renewable energy or digital infrastructure, creating opportunities and demands for specialized financial services.

- International trade agreements: These can impact cross-border financial flows and regulatory alignment, affecting firms with international operations.

Policy & Geopolitics: Shaping Financial Services

Political stability and government policies are paramount for financial services firms like Sanne Group. For example, the UK's commitment to net-zero targets by 2050, reinforced by policies announced in 2024, creates demand for green finance administration services. Conversely, geopolitical tensions, such as those impacting supply chains in 2024, can lead to increased market volatility, necessitating robust risk management for alternative assets.

Governments are increasingly focused on regulatory alignment to foster international trade and investment. The ongoing efforts by bodies like the Financial Stability Board (FSB) to harmonize prudential standards, particularly in light of the 2023 banking sector stresses, directly impact how firms like Sanne Group manage capital and cross-border operations. By 2025, continued progress in this harmonization is expected to simplify compliance for globally operating entities.

| Policy Area | Impact on Sanne Group | Example/Data Point (2024/2025 Focus) |

|---|---|---|

| Sustainable Finance Regulation | Increased demand for ESG reporting and administration services. | The EU Taxonomy Regulation, with phased implementation continuing through 2025, requires detailed environmental impact reporting for eligible assets. |

| Digital Asset Regulation | Need for specialized administration and compliance for crypto and tokenized assets. | MiCA (Markets in Crypto-Assets) regulation in the EU, fully applicable by late 2024, sets a precedent for digital asset oversight globally. |

| Tax Policy Changes | Potential shifts in investment attractiveness and operational costs. | Anticipated adjustments to capital gains tax or corporate tax rates in major economies by 2025 could influence fund structures and investor decisions. |

| Geopolitical Risk Mitigation | Requirement for enhanced due diligence and diversified investment strategies. | Ongoing global trade disputes and regional conflicts in 2024 necessitate careful monitoring of asset locations and counterparty risk. |

What is included in the product

This PESTLE analysis provides a comprehensive examination of the external macro-environmental factors influencing the Sanne Group, covering Political, Economic, Social, Technological, Environmental, and Legal dimensions.

It offers a strategic framework for understanding how these global forces create both challenges and opportunities for Sanne's business operations and future growth.

The Sanne Group PESTLE Analysis offers a streamlined, easily digestible summary, alleviating the pain point of sifting through dense reports for critical strategic insights.

Economic factors

Private Equity Dealmaking Resurgence

The private equity market is showing strong signs of recovery in 2024, with expectations for continued momentum into 2025. This resurgence is largely attributed to easing inflationary pressures and a more stable interest rate environment, which are reducing previous dealmaking uncertainties.

This uptick in activity, particularly with larger transactions and a greater number of successful exits, directly benefits fund administrators like Sanne Group. The increased volume of deals, including a notable rise in megadeals, translates into higher demand for specialized services in areas such as transaction support, fund accounting, and regulatory compliance.

Global private equity deal volume saw a substantial increase in 2024, with reports indicating a significant rebound from the slower pace of previous years. For instance, some analyses suggest that global PE deal value in the first half of 2024 could surpass the entirety of 2023, underscoring the renewed confidence and capital deployment within the sector.

Interest Rate Environment and Credit Markets

The current interest rate environment, with many central banks signaling potential easing in 2025, is a significant tailwind for credit markets. This shift is expected to lower borrowing costs, making it easier for private equity firms to finance acquisitions. For instance, the European Central Bank has indicated a pivot towards rate cuts, which will likely translate into more accessible and affordable debt for leveraged buyouts throughout 2025.

A more robust credit market, characterized by increased liquidity and a willingness from lenders to provide capital, directly fuels deal execution. Private equity sponsors are benefiting from this open credit access, a trend that is projected to drive a notable increase in dealmaking activity in 2025. The competitive landscape within direct lending markets is also a key factor, creating avenues for value creation through more favorable financing terms.

Inflationary Pressures and Economic Growth

Stabilizing economic growth and a noticeable decline in inflation are painting a more optimistic picture for financial markets. For instance, the US Consumer Price Index (CPI) saw a moderation in its year-over-year increase, falling to 3.1% in January 2024, a significant drop from its peak. This macroeconomic stability helps to lower uncertainty for investors, encouraging continued investment, particularly in alternative assets.

While the overall economic environment is improving, financial services firms must remain vigilant about their operational costs. The lingering effects of past inflationary periods mean that expenses related to technology, talent, and compliance can still present challenges. For example, while wage growth may be moderating, the cost of specialized financial expertise remains high.

Increased Dry Powder in Alternative Investments

The alternative investment landscape is awash with capital, with record-high levels of dry powder in private equity. This signifies a substantial pool of unallocated funds ready for deployment, creating a fertile ground for deal-making. As of the first half of 2024, private equity dry powder reached an estimated $2.5 trillion globally, a figure that has steadily climbed over the past few years.

This abundance of capital exerts considerable pressure on financial sponsors to identify and execute transactions. The drive to deploy this capital efficiently fuels increased M&A activity within the private markets. Consequently, this heightened deal flow directly translates into a greater demand for specialized administration services that support these complex transactions.

The robust fundraising environment further amplifies this trend. For instance, 2023 saw private equity firms raise over $1.2 trillion globally, demonstrating continued investor confidence and capital availability. This sustained influx of funds ensures that the pressure to deploy dry powder will persist, benefiting service providers.

- Record Dry Powder: Global private equity dry powder estimated at $2.5 trillion in H1 2024.

- Increased Deal Pressure: Sponsors are incentivized to complete transactions to deploy capital.

- Robust Fundraising: Over $1.2 trillion raised by PE firms in 2023, indicating sustained capital inflow.

- Demand for Administration: Higher deal volumes drive demand for specialized financial administration services.

Liquidity Demands from Limited Partners

Limited partners (LPs) are increasingly prioritizing liquidity, putting pressure on general partners (GPs) to secure profitable exit opportunities and return invested capital. This trend is particularly evident in the private equity space, where LPs are looking for ways to monetize their holdings more efficiently.

The heightened demand for liquidity is spurring the adoption of alternative exit strategies. Continuation funds, which allow existing investors to sell their stakes to a new fund managed by the same sponsor, and sponsor-to-sponsor sales are becoming more common. These methods offer GPs a way to provide liquidity to their LPs while potentially retaining valuable assets.

This shift is expected to act as a catalyst for renewed fundraising across various alternative asset classes. As LPs seek greater liquidity, they may allocate more capital to funds that demonstrate a clear path to exits and capital repatriation. For instance, Preqin data from early 2024 indicated a growing interest in secondary market transactions, a key component of liquidity solutions for LPs.

- Increased LP focus on liquidity: LPs are actively seeking to monetize their private market investments.

- Rise of alternative exits: Continuation funds and sponsor-to-sponsor deals are gaining traction as liquidity solutions.

- Catalyst for fundraising: The demand for liquidity is anticipated to boost capital raising for alternative asset managers.

- Secondary market activity: Data suggests a significant uptick in secondary transactions as LPs aim to exit investments.

Private Equity Surges: Economic Tailwinds Boost Deal Flow

Economic factors are currently favorable for Sanne Group, with stabilizing growth and moderating inflation reducing deal uncertainty. The anticipated easing of interest rates in 2025 is expected to lower borrowing costs, directly benefiting private equity firms and increasing deal activity.

The robust fundraising environment, with over $1.2 trillion raised by PE firms in 2023 and record dry powder of $2.5 trillion in H1 2024, creates significant pressure to deploy capital. This heightened deal flow directly translates into increased demand for specialized administration services that Sanne Group provides.

The market is experiencing a strong recovery in private equity dealmaking, with expectations for continued momentum into 2025 due to easing inflation and more stable interest rates. This resurgence, marked by larger transactions and successful exits, directly benefits fund administrators like Sanne Group through increased demand for their specialized services.

The current economic climate, characterized by moderating inflation and potential interest rate cuts in 2025, is a significant tailwind for financial markets. For instance, the US CPI fell to 3.1% in January 2024, down from its peak, fostering greater investor confidence and encouraging investment in alternative assets.

Preview Before You Purchase

Sanne Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of the Sanne Group provides a comprehensive overview of the external factors influencing its operations and strategic decisions. You'll gain insights into the Political, Economic, Social, Technological, Legal, and Environmental landscape impacting the company.