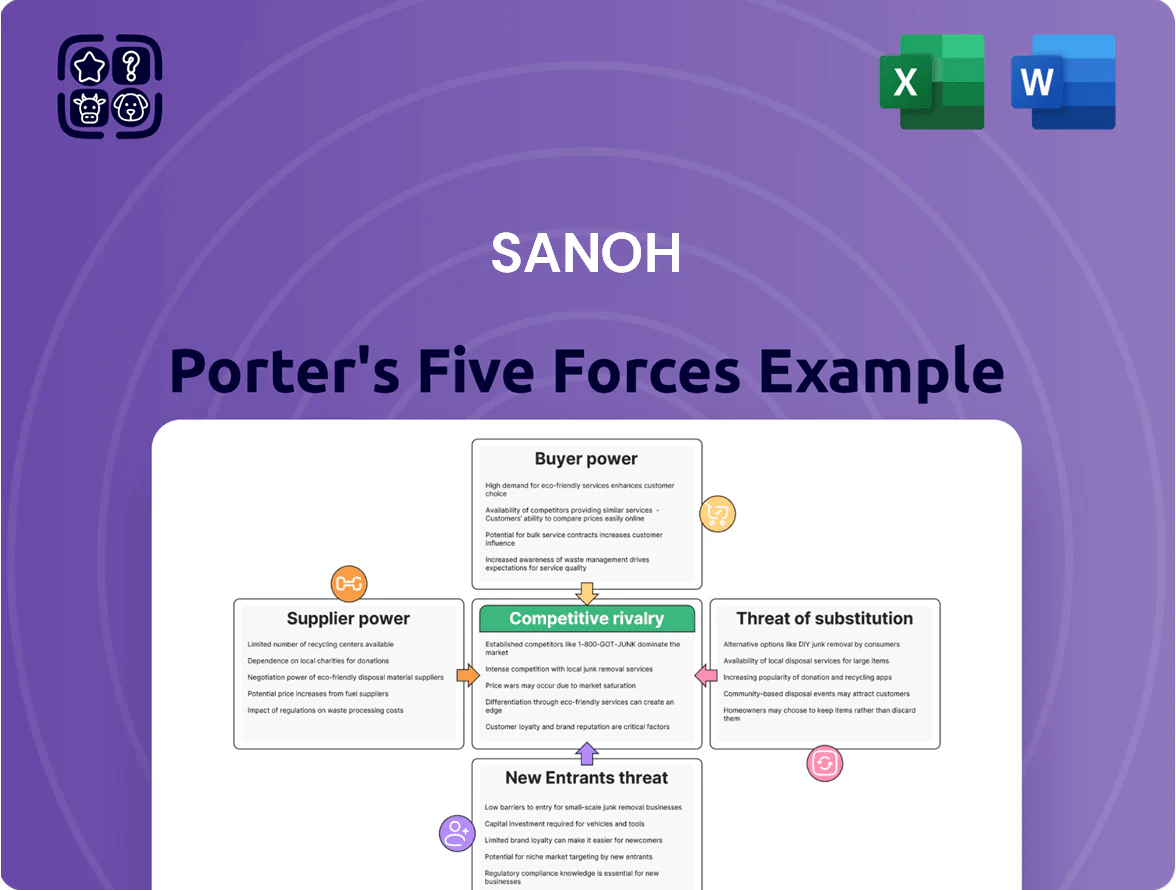

Sanoh Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Sanoh faces moderate supplier power and margin pressure from OEM consolidation, while buyer leverage and price sensitivity keep competition intense in core markets.

Emerging substitutes and tightening regulations raise strategic risks, but Sanoh’s scale and technical capabilities create defensible advantages in specialized segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sanoh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Sanoh depends heavily on steel, aluminum and specialized resins for tubing; raw-materials made up about 42% of COGS in FY2024, so price swings hit margins directly.

Through late 2025, steel futures rose ~18% year-over-year and resin prices climbed 12%, pushing input cost volatility and compressing operating margins by an estimated 120–180 basis points.

High-grade metal suppliers hold leverage because strict automotive safety specs limit qualified vendors to roughly 3–6 per region, raising switching costs and supplier bargaining power.

Specialized Material Requirements for EVs

The EV shift raised demand for advanced polymers and lightweight alloys for cooling lines, up 24% CAGR in EV components 2019–2024 and adding ~$1.3B global market value for polymeric coolant hoses by 2024 (source: industry reports).

These inputs come from a small set of high-tech chemical and metallurgical firms—top 5 suppliers control ~60% of capacity—giving suppliers stronger pricing power versus Tier-1s like Sanoh.

Energy Costs and Utility Providers

Manufacturing tubular components uses extrusion, bending, and heat treatment, making energy a major input; Sanoh reported energy costs rose ~18% in 2022–2024, squeezing margins.

Global energy price volatility through 2025 left Sanoh exposed to regional utility tariffs and policy-driven surcharges, boosting supplier leverage.

Because energy is non-substitutable for heavy industrial production, local utilities keep strong pricing power in negotiations, driving cost pass-through risk.

Geopolitical Supply Chain Disruptions

Sanoh’s global production network is sensitive to geopolitical shifts and trade rules; 2024 trade disruptions raised lead times by ~18% for automotive metal parts, hitting margins. Suppliers in restricted or unstable regions caused a 12% production shortfall in Q3 2024 for some OEM lines. Suppliers in politically stable countries captured ~8–15% pricing premia during 2023–2024 supply shocks.

- Global lead times +18% (2024)

- Q3 2024 production shortfall 12%

- Pricing premia 8–15% (2023–2024)

Tier-2 Supplier Consolidation

Tier-2 consolidation has concentrated suppliers: by 2025, the top 10 Tier-2/3 auto suppliers held ~52% of segment revenue vs 41% in 2018, giving larger firms greater pricing and delivery leverage over Sanoh during contract renewals.

Fewer alternatives raise switching costs and shorten Sanoh’s negotiation room; lead times can be extended 10–20% when large Tier-2s prioritize OEMs, pressuring Sanoh’s margins.

- Top-10 share ~52% (2025)

- Switching cost ↑, fewer sources

- Lead times +10–20%

- Stronger supplier pricing power

Supplier squeeze: raw materials 42% of COGS, prices cut margins 120–180bps

Suppliers hold strong leverage: raw materials were ~42% of COGS in FY2024, steel/resin price spikes (steel +18% YoY, resins +12% through 2025) cut margins ~120–180 bps; top-5 input suppliers control ~60% capacity and top-10 Tier-2/3 share rose to ~52% by 2025, raising switching costs and lead times (+10–20%, global +18% in 2024).

| Metric | Value |

|---|---|

| Raw materials (% of COGS FY2024) | ~42% |

| Steel price change (2024–2025) | +18% YoY |

| Resin price change (through 2025) | +12% |

| Margin impact | −120–180 bps |

| Top-5 suppliers capacity share | ~60% |

| Top-10 Tier-2/3 market share (2025) | ~52% |

| Lead time change (2024) | +18% global; +10–20% when prioritized |

What is included in the product

Tailored analysis of Sanoh's competitive landscape using Porter's Five Forces, uncovering supplier and buyer power, substitute threats, entry barriers, and rivalry to assess pricing pressure and profitability.

Sanoh Porter's Five Forces distilled into a one-sheet, letting you spot supplier, buyer, and entrant pressures instantly and copy-ready for decks—no macros, fully customizable to reflect changing market data.

Customers Bargaining Power

High Concentration of Global OEMs

Sanoh sells mainly to a few giant OEMs—Toyota, Nissan, Ford—who bought roughly 60–70% of global light-vehicle parts in 2024, giving them strong price leverage over suppliers.

These OEMs place large, recurring orders; losing one major contract could cut Sanoh’s revenue by an estimated 15–30% based on 2024 sales mixes, so bargaining power is high.

Strict Annual Cost Reduction Mandates

OEMs demand annual price cuts, commonly 1–3% per year in 2024–25 auto contracts, forcing Sanoh to boost productivity and shave costs to retain business.

Buyers’ scale—top five customers often represent >50% of sales—lets them extract concessions, limiting Sanoh’s pricing power even if input inflation rose 8–12% in 2024.

Low Switching Costs for Standardized Parts

Many fuel and brake lines are standardized and can be made by several global Tier-1s; industry data shows ~60–70% of tubing volumes are non-differentiated, so buyers can shift suppliers with low effort.

If Sanoh raises prices, OEMs often switch to rivals like Sumitomo or Mubea with global footprints, keeping Sanoh largely a price-taker on legacy lines.

Customer Vertical Integration

Major OEMs such as Toyota and Tesla have announced moves toward in‑house EV thermal systems; Tesla’s 2024 report noted internalizing coolant lines cut supplier spend by an estimated 5–8% of battery system costs.

This backward integration risk caps Sanoh’s pricing power and forces tighter margins and innovation to retain contracts.

- OEMs internalizing critical tubing

- Example: Tesla 2024, 5–8% cost shift

- Limits Sanoh pricing, raises margin pressure

Demand for Co-Development and R&D Investment

Sanoh at Risk: Top OEMs Hold Pricing Power, Losing One Client Could Cut 15–30%

Sanoh faces high customer bargaining power: top OEMs (Toyota, Nissan, Ford) bought ~60–70% of light-vehicle parts in 2024, with Sanoh’s top five customers >50% of sales, so losing one client could cut revenue 15–30%.

OEMs demand 1–3% annual price cuts and shift non-differentiated tubing (~60–70% of volumes) easily; supplier-funded R&D (2–4% of sales) and OEM back-integration (Tesla cut supplier spend ~5–8% in 2024) squeeze margins.

| Metric | 2024 value |

|---|---|

| OEM share of parts | 60–70% |

| Top 5 customers share | >50% |

| Revenue risk per lost client | 15–30% |

| Annual price cuts | 1–3% |

| Non-diff tubing | 60–70% |

| Supplier R&D burden | 2–4% of sales |

| Tesla internalization impact | 5–8% supplier spend |

Full Version Awaits

Sanoh Porter's Five Forces Analysis

This preview shows the exact Sanoh Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Sanoh faces moderate supplier power and margin pressure from OEM consolidation, while buyer leverage and price sensitivity keep competition intense in core markets.

Emerging substitutes and tightening regulations raise strategic risks, but Sanoh’s scale and technical capabilities create defensible advantages in specialized segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sanoh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Sanoh depends heavily on steel, aluminum and specialized resins for tubing; raw-materials made up about 42% of COGS in FY2024, so price swings hit margins directly.

Through late 2025, steel futures rose ~18% year-over-year and resin prices climbed 12%, pushing input cost volatility and compressing operating margins by an estimated 120–180 basis points.

High-grade metal suppliers hold leverage because strict automotive safety specs limit qualified vendors to roughly 3–6 per region, raising switching costs and supplier bargaining power.

Specialized Material Requirements for EVs

The EV shift raised demand for advanced polymers and lightweight alloys for cooling lines, up 24% CAGR in EV components 2019–2024 and adding ~$1.3B global market value for polymeric coolant hoses by 2024 (source: industry reports).

These inputs come from a small set of high-tech chemical and metallurgical firms—top 5 suppliers control ~60% of capacity—giving suppliers stronger pricing power versus Tier-1s like Sanoh.

Energy Costs and Utility Providers

Manufacturing tubular components uses extrusion, bending, and heat treatment, making energy a major input; Sanoh reported energy costs rose ~18% in 2022–2024, squeezing margins.

Global energy price volatility through 2025 left Sanoh exposed to regional utility tariffs and policy-driven surcharges, boosting supplier leverage.

Because energy is non-substitutable for heavy industrial production, local utilities keep strong pricing power in negotiations, driving cost pass-through risk.

Geopolitical Supply Chain Disruptions

Sanoh’s global production network is sensitive to geopolitical shifts and trade rules; 2024 trade disruptions raised lead times by ~18% for automotive metal parts, hitting margins. Suppliers in restricted or unstable regions caused a 12% production shortfall in Q3 2024 for some OEM lines. Suppliers in politically stable countries captured ~8–15% pricing premia during 2023–2024 supply shocks.

- Global lead times +18% (2024)

- Q3 2024 production shortfall 12%

- Pricing premia 8–15% (2023–2024)

Tier-2 Supplier Consolidation

Tier-2 consolidation has concentrated suppliers: by 2025, the top 10 Tier-2/3 auto suppliers held ~52% of segment revenue vs 41% in 2018, giving larger firms greater pricing and delivery leverage over Sanoh during contract renewals.

Fewer alternatives raise switching costs and shorten Sanoh’s negotiation room; lead times can be extended 10–20% when large Tier-2s prioritize OEMs, pressuring Sanoh’s margins.

- Top-10 share ~52% (2025)

- Switching cost ↑, fewer sources

- Lead times +10–20%

- Stronger supplier pricing power

Supplier squeeze: raw materials 42% of COGS, prices cut margins 120–180bps

Suppliers hold strong leverage: raw materials were ~42% of COGS in FY2024, steel/resin price spikes (steel +18% YoY, resins +12% through 2025) cut margins ~120–180 bps; top-5 input suppliers control ~60% capacity and top-10 Tier-2/3 share rose to ~52% by 2025, raising switching costs and lead times (+10–20%, global +18% in 2024).

| Metric | Value |

|---|---|

| Raw materials (% of COGS FY2024) | ~42% |

| Steel price change (2024–2025) | +18% YoY |

| Resin price change (through 2025) | +12% |

| Margin impact | −120–180 bps |

| Top-5 suppliers capacity share | ~60% |

| Top-10 Tier-2/3 market share (2025) | ~52% |

| Lead time change (2024) | +18% global; +10–20% when prioritized |

What is included in the product

Tailored analysis of Sanoh's competitive landscape using Porter's Five Forces, uncovering supplier and buyer power, substitute threats, entry barriers, and rivalry to assess pricing pressure and profitability.

Sanoh Porter's Five Forces distilled into a one-sheet, letting you spot supplier, buyer, and entrant pressures instantly and copy-ready for decks—no macros, fully customizable to reflect changing market data.

Customers Bargaining Power

High Concentration of Global OEMs

Sanoh sells mainly to a few giant OEMs—Toyota, Nissan, Ford—who bought roughly 60–70% of global light-vehicle parts in 2024, giving them strong price leverage over suppliers.

These OEMs place large, recurring orders; losing one major contract could cut Sanoh’s revenue by an estimated 15–30% based on 2024 sales mixes, so bargaining power is high.

Strict Annual Cost Reduction Mandates

OEMs demand annual price cuts, commonly 1–3% per year in 2024–25 auto contracts, forcing Sanoh to boost productivity and shave costs to retain business.

Buyers’ scale—top five customers often represent >50% of sales—lets them extract concessions, limiting Sanoh’s pricing power even if input inflation rose 8–12% in 2024.

Low Switching Costs for Standardized Parts

Many fuel and brake lines are standardized and can be made by several global Tier-1s; industry data shows ~60–70% of tubing volumes are non-differentiated, so buyers can shift suppliers with low effort.

If Sanoh raises prices, OEMs often switch to rivals like Sumitomo or Mubea with global footprints, keeping Sanoh largely a price-taker on legacy lines.

Customer Vertical Integration

Major OEMs such as Toyota and Tesla have announced moves toward in‑house EV thermal systems; Tesla’s 2024 report noted internalizing coolant lines cut supplier spend by an estimated 5–8% of battery system costs.

This backward integration risk caps Sanoh’s pricing power and forces tighter margins and innovation to retain contracts.

- OEMs internalizing critical tubing

- Example: Tesla 2024, 5–8% cost shift

- Limits Sanoh pricing, raises margin pressure

Demand for Co-Development and R&D Investment

Sanoh at Risk: Top OEMs Hold Pricing Power, Losing One Client Could Cut 15–30%

Sanoh faces high customer bargaining power: top OEMs (Toyota, Nissan, Ford) bought ~60–70% of light-vehicle parts in 2024, with Sanoh’s top five customers >50% of sales, so losing one client could cut revenue 15–30%.

OEMs demand 1–3% annual price cuts and shift non-differentiated tubing (~60–70% of volumes) easily; supplier-funded R&D (2–4% of sales) and OEM back-integration (Tesla cut supplier spend ~5–8% in 2024) squeeze margins.

| Metric | 2024 value |

|---|---|

| OEM share of parts | 60–70% |

| Top 5 customers share | >50% |

| Revenue risk per lost client | 15–30% |

| Annual price cuts | 1–3% |

| Non-diff tubing | 60–70% |

| Supplier R&D burden | 2–4% of sales |

| Tesla internalization impact | 5–8% supplier spend |

Full Version Awaits

Sanoh Porter's Five Forces Analysis

This preview shows the exact Sanoh Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.