Sapiens Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Sapiens faces moderate supplier power, intense buyer scrutiny, and significant rivalry from nimble insurtech and legacy vendors, while regulatory shifts and substitutes (platforms/cloud solutions) create material strategic pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sapiens’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Cloud Infrastructure Providers

Sapiens increasingly depends on major cloud providers such as Microsoft Azure and Amazon Web Services to host its cloud-native insurance platforms, giving suppliers strong leverage because migrating petabyte-scale policy and claims databases is often cost-prohibitive and risky; industry estimates put large-scale migration costs at $5–20M per insurer and 9–18 months of downtime risk. By end-2025, as Sapiens targets >40% SaaS revenue mix, this infrastructure dependency remains a critical strategic risk.

Scarcity of Specialized Insurance Tech Talent

The pool of software engineers with deep insurance-domain and regulatory expertise is scarce; industry surveys show 38% of insurers report talent shortages in 2024, raising hiring costs by ~22% year-on-year for niche roles.

Sapiens competes with banks and insurtechs for this workforce, which pushes wages up and increases R&D personnel costs, a key input for product development.

Any sustained shortage can delay Sapiens’ roadmap: 2024 customer reports linked talent gaps to average delivery slippages of 3–6 months.

Integration with Third Party Data Analytics Providers

Sapiens integrates third-party data feeds for underwriting, risk assessment, and claims, with 35–45% of module accuracy improvements tied to external data in recent insurer studies (2024).

Many vendors exist, but regional providers of localized regulatory and telematics data command higher leverage—contract churn costs Sapiens an estimated $2–4M per major region switch.

Reliance on Specialized Cybersecurity Vendors

Sapiens must spend heavily on specialized cybersecurity vendors to protect sensitive insurance data; in 2024 global cybersecurity spending hit about 207 billion USD and enterprise-grade threat intelligence services command premium pricing, giving suppliers moderate bargaining power.

These vendors’ proprietary tools and skilled teams are hard to replicate in-house, so Sapiens depends on them to maintain client trust; as attacks rose ~15% YoY through 2024–2025, reliance—and supplier leverage—increased.

- 2024 global cybersecurity spend ≈ 207B USD

- Cyber incidents +15% YoY to 2025

- In-house replication cost > third-party contracting

Consolidation of Enterprise Software Tooling

Sapiens relies on ERP and development tools from a few large vendors (Oracle, Atlassian), whose products are deeply embedded in its dev lifecycle and carry high switching costs; Gartner estimates enterprise tooling spend concentration top-three vendors ≈45% of market in 2024. This supplier consolidation gives vendors pricing power, producing a stable but non-negotiable cost base for Sapiens and limited room for big discounts.

- Top vendor concentration ~45% (Gartner 2024)

- High switching costs: migration projects often 6–12 months

- Embedded workflows reduce bargaining leverage

- Stable pricing, limited room for major cost cuts

Suppliers wield rising power: costly cloud migrations, scarce talent, $207B cyber spend

Suppliers hold moderate–high power: cloud giants (Azure/AWS) create high switching costs (migration $5–20M, 9–18 months); niche insurance engineers are scarce (38% talent gap 2024; wages +22% YoY); specialized data/telematics and cyber vendors command regional leverage (churn $2–4M per region; global cyber spend ≈207B USD 2024; incidents +15% YoY).

| Item | Metric |

|---|---|

| Cloud migration | $5–20M; 9–18m |

| Talent gap | 38%; wages +22% |

| Data vendor churn | $2–4M/region |

| Cyber spend | $207B; incidents +15% |

What is included in the product

Tailored Porter's Five Forces for Sapiens that uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats—supported by industry context and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces summary that turns complex competitive analysis into instant decision-ready insights—editable pressures, clean radar visualization, and copy-ready layout for decks or dashboards.

Customers Bargaining Power

High Switching Costs for Core Insurance Systems

Once an insurer deploys a Sapiens core system, estimated switching costs—implementation, data migration, regulatory validation and training—often exceed $5–20M and 12–36 months of downtime risk, creating strong client lock-in that lowers customers’ bargaining power at renewals. This advantage becomes durable only after the multi-year go-live period completes; until then buyers retain leverage during implementation delays or unmet milestones.

Concentration of Tier One Insurance Carriers

Demand for Modular and Flexible SaaS Pricing

By late 2025, 46% of enterprise insurers prefer consumption-based or modular SaaS pricing over upfront licenses, pushing Sapiens to offer pay-as-you-go and module-by-module contracts to win deals.

Smaller initial deployments—often 20–40% of full-suite spend—let buyers scale and trial rivals, reducing switching costs and increasing customer bargaining power versus Sapiens.

Insurers leverage this to demand continuous value: Sapiens must deliver measurable incremental updates each quarter or face churn; in 2024 Sapiens reported 7% churn in cloud clients who didn’t receive fast feature releases.

Insurers Internal IT Capabilities

Larger insurers often keep sizable internal IT teams able to maintain legacy systems, creating a credible alternative to Sapiens during procurement; 2024 Aon data shows 42% of global insurers increased in-house digital spending vs vendors.

Sapiens must prove platform ROI—lower TCO and faster go-live—versus bespoke builds that insurers may prefer to delay transformation.

- 42% grew in-house spend (2024, Aon)

- In-house delays raise switch costs

- Focus on TCO, speed, measurable ROI

Influence of Third Party Industry Consultants

Insurance buyers often hire consultants such as Deloitte or Accenture to run software selection; these firms influenced ~30–40% of large insurer vendor choices in 2024, tilting deals toward partners they favor.

Consultant recommendations and comparison reports raise customer bargaining power by offering expert alternatives, price benchmarks, and contract-negotiation support, reducing Sapiens’ leverage.

- Consultant influence: ~30–40% large deals (2024)

- Shifts vendor preference via partnerships

- Provides price benchmarks, boosting buyer leverage

Buyers’ power vs Sapiens: high switching costs yet rising discounts, SaaS & in‑house trends

Buyers’ bargaining power vs Sapiens is mixed: high switching costs ($5–20M, 12–36 months) and 7% cloud churn lower leverage, but Tier‑one insurers (60–70% spend) win 10–30% discounts, modular SaaS demand (46% prefer by late 2025), consultant influence (30–40% of large deals) and growing in‑house IT (42% increased spend in 2024) raise buyer leverage.

| Metric | Value |

|---|---|

| Switching cost | $5–20M; 12–36 months |

| Tier‑one spend share | 60–70% |

| Typical discounts | 10–30% |

| SaaS preference (late 2025) | 46% |

| Consultant influence (2024) | 30–40% |

| In‑house spend growth (2024) | 42% |

| Cloud churn without fast releases (2024) | 7% |

Preview Before You Purchase

Sapiens Porter's Five Forces Analysis

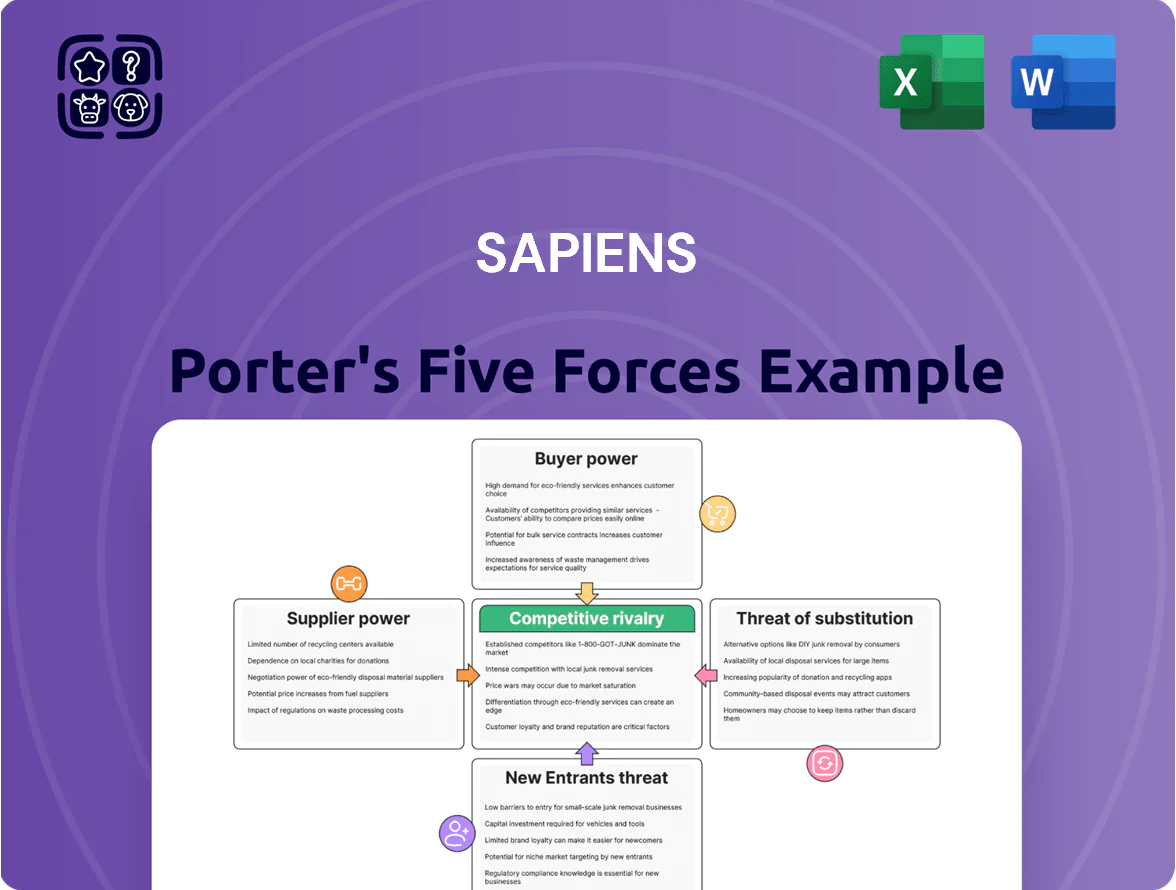

This preview shows the exact Sapiens Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document you see is the final, professionally formatted file, ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes. You’ll get instant access to this same deliverable upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Sapiens faces moderate supplier power, intense buyer scrutiny, and significant rivalry from nimble insurtech and legacy vendors, while regulatory shifts and substitutes (platforms/cloud solutions) create material strategic pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sapiens’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Cloud Infrastructure Providers

Sapiens increasingly depends on major cloud providers such as Microsoft Azure and Amazon Web Services to host its cloud-native insurance platforms, giving suppliers strong leverage because migrating petabyte-scale policy and claims databases is often cost-prohibitive and risky; industry estimates put large-scale migration costs at $5–20M per insurer and 9–18 months of downtime risk. By end-2025, as Sapiens targets >40% SaaS revenue mix, this infrastructure dependency remains a critical strategic risk.

Scarcity of Specialized Insurance Tech Talent

The pool of software engineers with deep insurance-domain and regulatory expertise is scarce; industry surveys show 38% of insurers report talent shortages in 2024, raising hiring costs by ~22% year-on-year for niche roles.

Sapiens competes with banks and insurtechs for this workforce, which pushes wages up and increases R&D personnel costs, a key input for product development.

Any sustained shortage can delay Sapiens’ roadmap: 2024 customer reports linked talent gaps to average delivery slippages of 3–6 months.

Integration with Third Party Data Analytics Providers

Sapiens integrates third-party data feeds for underwriting, risk assessment, and claims, with 35–45% of module accuracy improvements tied to external data in recent insurer studies (2024).

Many vendors exist, but regional providers of localized regulatory and telematics data command higher leverage—contract churn costs Sapiens an estimated $2–4M per major region switch.

Reliance on Specialized Cybersecurity Vendors

Sapiens must spend heavily on specialized cybersecurity vendors to protect sensitive insurance data; in 2024 global cybersecurity spending hit about 207 billion USD and enterprise-grade threat intelligence services command premium pricing, giving suppliers moderate bargaining power.

These vendors’ proprietary tools and skilled teams are hard to replicate in-house, so Sapiens depends on them to maintain client trust; as attacks rose ~15% YoY through 2024–2025, reliance—and supplier leverage—increased.

- 2024 global cybersecurity spend ≈ 207B USD

- Cyber incidents +15% YoY to 2025

- In-house replication cost > third-party contracting

Consolidation of Enterprise Software Tooling

Sapiens relies on ERP and development tools from a few large vendors (Oracle, Atlassian), whose products are deeply embedded in its dev lifecycle and carry high switching costs; Gartner estimates enterprise tooling spend concentration top-three vendors ≈45% of market in 2024. This supplier consolidation gives vendors pricing power, producing a stable but non-negotiable cost base for Sapiens and limited room for big discounts.

- Top vendor concentration ~45% (Gartner 2024)

- High switching costs: migration projects often 6–12 months

- Embedded workflows reduce bargaining leverage

- Stable pricing, limited room for major cost cuts

Suppliers wield rising power: costly cloud migrations, scarce talent, $207B cyber spend

Suppliers hold moderate–high power: cloud giants (Azure/AWS) create high switching costs (migration $5–20M, 9–18 months); niche insurance engineers are scarce (38% talent gap 2024; wages +22% YoY); specialized data/telematics and cyber vendors command regional leverage (churn $2–4M per region; global cyber spend ≈207B USD 2024; incidents +15% YoY).

| Item | Metric |

|---|---|

| Cloud migration | $5–20M; 9–18m |

| Talent gap | 38%; wages +22% |

| Data vendor churn | $2–4M/region |

| Cyber spend | $207B; incidents +15% |

What is included in the product

Tailored Porter's Five Forces for Sapiens that uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats—supported by industry context and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces summary that turns complex competitive analysis into instant decision-ready insights—editable pressures, clean radar visualization, and copy-ready layout for decks or dashboards.

Customers Bargaining Power

High Switching Costs for Core Insurance Systems

Once an insurer deploys a Sapiens core system, estimated switching costs—implementation, data migration, regulatory validation and training—often exceed $5–20M and 12–36 months of downtime risk, creating strong client lock-in that lowers customers’ bargaining power at renewals. This advantage becomes durable only after the multi-year go-live period completes; until then buyers retain leverage during implementation delays or unmet milestones.

Concentration of Tier One Insurance Carriers

Demand for Modular and Flexible SaaS Pricing

By late 2025, 46% of enterprise insurers prefer consumption-based or modular SaaS pricing over upfront licenses, pushing Sapiens to offer pay-as-you-go and module-by-module contracts to win deals.

Smaller initial deployments—often 20–40% of full-suite spend—let buyers scale and trial rivals, reducing switching costs and increasing customer bargaining power versus Sapiens.

Insurers leverage this to demand continuous value: Sapiens must deliver measurable incremental updates each quarter or face churn; in 2024 Sapiens reported 7% churn in cloud clients who didn’t receive fast feature releases.

Insurers Internal IT Capabilities

Larger insurers often keep sizable internal IT teams able to maintain legacy systems, creating a credible alternative to Sapiens during procurement; 2024 Aon data shows 42% of global insurers increased in-house digital spending vs vendors.

Sapiens must prove platform ROI—lower TCO and faster go-live—versus bespoke builds that insurers may prefer to delay transformation.

- 42% grew in-house spend (2024, Aon)

- In-house delays raise switch costs

- Focus on TCO, speed, measurable ROI

Influence of Third Party Industry Consultants

Insurance buyers often hire consultants such as Deloitte or Accenture to run software selection; these firms influenced ~30–40% of large insurer vendor choices in 2024, tilting deals toward partners they favor.

Consultant recommendations and comparison reports raise customer bargaining power by offering expert alternatives, price benchmarks, and contract-negotiation support, reducing Sapiens’ leverage.

- Consultant influence: ~30–40% large deals (2024)

- Shifts vendor preference via partnerships

- Provides price benchmarks, boosting buyer leverage

Buyers’ power vs Sapiens: high switching costs yet rising discounts, SaaS & in‑house trends

Buyers’ bargaining power vs Sapiens is mixed: high switching costs ($5–20M, 12–36 months) and 7% cloud churn lower leverage, but Tier‑one insurers (60–70% spend) win 10–30% discounts, modular SaaS demand (46% prefer by late 2025), consultant influence (30–40% of large deals) and growing in‑house IT (42% increased spend in 2024) raise buyer leverage.

| Metric | Value |

|---|---|

| Switching cost | $5–20M; 12–36 months |

| Tier‑one spend share | 60–70% |

| Typical discounts | 10–30% |

| SaaS preference (late 2025) | 46% |

| Consultant influence (2024) | 30–40% |

| In‑house spend growth (2024) | 42% |

| Cloud churn without fast releases (2024) | 7% |

Preview Before You Purchase

Sapiens Porter's Five Forces Analysis

This preview shows the exact Sapiens Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document you see is the final, professionally formatted file, ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes. You’ll get instant access to this same deliverable upon payment.