Sapura Energy Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

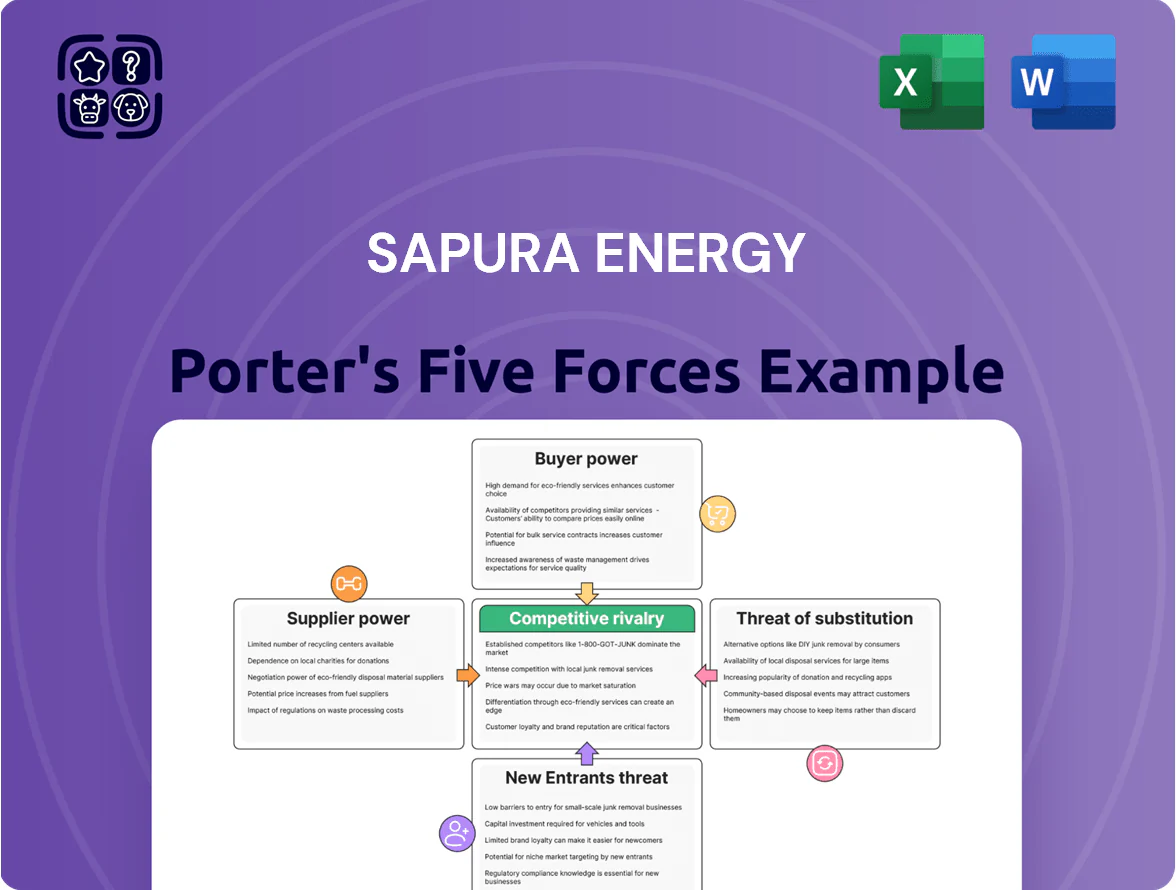

Sapura Energy navigates a complex industry landscape, where the bargaining power of buyers and the intensity of rivalry significantly shape its strategic options. Understanding these forces is crucial for any stakeholder looking to grasp the company's competitive positioning.

The complete report reveals the real forces shaping Sapura Energy’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Equipment and Technology Suppliers

Sapura Energy's dependence on highly specialized equipment and advanced technology for its complex offshore operations, such as drilling rigs and subsea vessels, significantly impacts supplier bargaining power. These sophisticated machinery providers often operate in a niche market.

The limited number of suppliers capable of producing such specialized equipment grants them considerable leverage. This is particularly true when their offerings are proprietary or possess unique, hard-to-replicate capabilities. For instance, a supplier of a unique deep-water drilling system for Sapura Energy could command higher prices.

Switching costs further bolster this supplier power. High costs associated with retraining personnel, integrating new systems, or ensuring compatibility with existing infrastructure mean Sapura Energy faces substantial hurdles if it seeks to change suppliers for critical equipment, reinforcing the suppliers' strong position.

Skilled Labor and Expertise Providers

The upstream oil and gas sector, where Sapura Energy operates, is heavily reliant on a highly specialized workforce. This includes critical roles like petroleum engineers, geoscientists, project managers, and skilled technicians for offshore operations. The demand for these professionals often outstrips the available supply, giving them significant bargaining power.

Suppliers of this expertise, whether they are individual contractors or specialized engineering and technical service firms, can therefore command higher rates and favorable contract terms. For instance, in 2024, the global shortage of experienced offshore drilling personnel continued to drive up day rates for specialized crews. Sapura Energy's capacity to either develop its internal talent pool or its dependence on these external expert providers directly influences the leverage these suppliers hold.

Raw Material and Component Suppliers

The bargaining power of suppliers for raw materials and components, while less potent than for specialized equipment, remains a notable factor for Sapura Energy. For instance, in 2024, global steel prices, a key component in offshore structures, experienced volatility, impacting project budgets. A concentrated supplier base for critical components can also lead to increased costs and potential delays.

Financial Creditors and Lenders

Financial creditors and lenders hold significant sway over Sapura Energy, particularly given its ongoing financial restructuring. Their decisions on providing capital, extending credit, or approving debt modifications are crucial for the company's day-to-day operations and its ability to pursue future projects. For instance, as of early 2024, Sapura Energy's successful completion of its debt restructuring program, which involved significant negotiations with its lenders, underscores this power. The terms agreed upon in these arrangements directly influence the company's financial flexibility and cost of capital.

- Lender Influence: The ability of creditors to dictate terms for new financing or debt relief gives them considerable bargaining power.

- Restructuring Impact: Sapura Energy's recent financial restructuring, completed in early 2024, highlights the crucial role and leverage of its lenders in shaping the company's financial future.

- Capital Dependency: The company's reliance on external funding for its capital-intensive projects amplifies the bargaining power of financial institutions.

Logistics and Support Service Providers

Sapura Energy’s global operations necessitate a robust network of logistics and support service providers, including transportation and field services. The bargaining power of these suppliers can be significant if they are highly concentrated or possess specialized capabilities in regions where Sapura Energy operates. For instance, in 2024, the cost of specialized offshore vessel chartering, a key logistical support, saw fluctuations based on global demand and availability, directly impacting Sapura Energy's project costs.

The efficiency and cost-effectiveness of these logistics and support services are paramount to Sapura Energy’s project execution timelines and ultimately its profitability. Any disruption or significant price increase from these providers can directly affect Sapura Energy’s competitive edge and financial performance.

- Concentration of Providers: A limited number of specialized logistics and support firms in key operating regions can lead to higher bargaining power for those suppliers.

- Specialized Capabilities: Providers offering unique or highly technical services, such as advanced subsea construction support, often command greater leverage.

- Cost Sensitivity: Sapura Energy's profitability is directly tied to the efficiency and cost of these outsourced services, making supplier pricing a critical factor.

- Global Reach Requirements: The need for services across multiple continents means Sapura Energy must navigate varying supplier landscapes and potential regional dependencies.

Supplier Power Shapes Offshore Energy Operations

Sapura Energy faces significant supplier bargaining power due to its reliance on specialized offshore equipment and skilled labor. The limited number of providers for critical machinery and the high switching costs associated with integrating new systems empower these suppliers. Furthermore, the scarcity of experienced offshore personnel in 2024 directly translated into higher rates for specialized crews, impacting Sapura Energy's operational expenses.

Financial creditors also wield considerable influence, as demonstrated by Sapura Energy's early 2024 debt restructuring. The terms negotiated with lenders critically shape the company's financial flexibility and access to capital for its capital-intensive projects.

Suppliers of raw materials like steel, a key component in offshore structures, also exert influence, with price volatility in 2024 affecting project budgets. Similarly, concentrated logistics and support service providers, particularly those offering specialized offshore vessel chartering, can dictate terms due to demand and availability fluctuations.

| Supplier Category | Key Factors Influencing Bargaining Power | Impact on Sapura Energy | 2024 Data/Trend Example |

|---|---|---|---|

| Specialized Equipment Manufacturers | Niche market, proprietary technology, high switching costs | Higher equipment costs, potential project delays if supply is constrained | Continued demand for advanced deep-water drilling systems |

| Skilled Labor Providers (e.g., specialized crews) | Shortage of experienced personnel, high demand | Increased labor costs, potential difficulty in securing adequate staffing | Rising day rates for experienced offshore drilling personnel |

| Financial Creditors | Capital dependency, debt restructuring terms | Influence on financing costs, operational flexibility, and strategic decisions | Successful completion of debt restructuring in early 2024 |

| Raw Material Suppliers (e.g., Steel) | Concentrated supplier base, global commodity price fluctuations | Impact on project budgets and material costs | Volatility in global steel prices affecting offshore structure costs |

| Logistics & Support Services | Concentration of providers, specialized capabilities, regional dependencies | Affects project execution timelines and operational efficiency | Fluctuations in specialized offshore vessel chartering costs |

What is included in the product

This analysis dissects the competitive landscape for Sapura Energy by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the oil and gas services sector.

Instantly visualize Sapura Energy's competitive landscape, highlighting key pressures from rivals and new entrants to inform strategic responses.

Customers Bargaining Power

Large Oil and Gas Companies

Sapura Energy's key clients are typically substantial, integrated oil and gas corporations such as Petronas, Chevron, PTTEP, and ExxonMobil. These industry giants possess considerable financial strength and a consistent stream of large-scale projects, enabling them to negotiate advantageous contract conditions.

The sheer size of these projects grants these major oil and gas companies significant leverage. This concentrated purchasing power can lead to downward pressure on the prices Sapura Energy can charge and, consequently, impact its profit margins.

For instance, in fiscal year 2024, Sapura Energy's revenue from its major clients, particularly Petronas, remained a critical component of its financial performance, highlighting the ongoing influence these large customers wield over the company's commercial agreements and profitability.

Project-Based Procurement

Customers in the energy services sector frequently utilize project-based procurement, a strategy that involves issuing large, long-term contracts for services like Engineering, Procurement, Construction, Installation, and Commissioning (EPCIC), as well as drilling and Operations & Maintenance (O&M).

This approach empowers customers by enabling them to solicit competitive bids from a wide array of service providers, thereby significantly amplifying their bargaining leverage. For Sapura Energy, navigating this environment means its capacity to secure new contracts and sustain a robust order book is directly tied to its performance within these competitive bidding processes.

Price Sensitivity and Cost Control

Customers in the oil and gas sector, including Sapura Energy's clients, exhibit significant price sensitivity. This is driven by the inherent volatility of oil prices, compelling companies to rigorously control costs and boost operational efficiency. For instance, in 2023, global oil prices fluctuated, impacting the budgets of exploration and production companies, which in turn pressures service providers like Sapura Energy to offer more competitive pricing.

This heightened price sensitivity means that Sapura Energy must not only provide cost-effective solutions but also clearly articulate the value proposition of its services. Demonstrating tangible benefits and a strong return on investment is crucial for securing contracts in a market where every dollar counts. The company's focus on operational discipline and margin preservation is a direct response to this customer demand.

Technical Specifications and Performance Demands

Customers in the upstream oil and gas sector, including major energy companies, often impose highly specific technical requirements and expect exceptional performance from their service providers. This necessity for advanced technology and proven project execution capabilities significantly bolsters their bargaining power. For instance, a major oil discovery might necessitate specialized subsea engineering capabilities that only a few companies can provide, allowing the customer to negotiate favorable terms.

The stringent performance demands translate directly into higher costs for service providers, who must invest heavily in research, development, and cutting-edge equipment. This capital intensity means that customers, by virtue of their purchasing power and project scale, can effectively dictate pricing and quality standards. In 2024, the global upstream oil and gas market saw continued emphasis on efficiency and technological advancement, further empowering sophisticated buyers.

- High Technical Specifications: Buyers demand specialized solutions, limiting the pool of qualified suppliers.

- Performance Standards: Stringent operational requirements necessitate significant investment by service providers.

- Customer Leverage: The need for specialized capabilities allows customers to negotiate pricing and contract terms.

- Market Influence: Major clients can influence industry-wide standards through their procurement practices.

Diversification of Customer Base

Sapura Energy's strategy to diversify its customer base across various regions and project types is crucial in lessening the influence of any single client. This approach helps to spread risk and reduce dependency on a few large contracts.

Maintaining long-term relationships with key clients, like those with PTTEP and Chevron in Thailand, provides a degree of stability. These established partnerships, often built on trust and a track record of successful project delivery, can act as a buffer against the bargaining power of individual customers.

- Geographic Diversification: Expanding into new markets reduces reliance on any one region's economic conditions or client base.

- Project Type Variety: Engaging in different types of projects, such as offshore construction, drilling, and maintenance, broadens Sapura Energy's appeal and client pool.

- Client Relationship Management: Nurturing strong, long-term partnerships can foster loyalty and create more stable revenue streams, thereby mitigating customer power.

Client Power Shapes Sapura Energy's Market Dynamics

Sapura Energy faces significant bargaining power from its major clients, primarily large integrated oil and gas corporations. These clients, such as Petronas and Chevron, leverage their substantial financial clout and the sheer scale of projects to negotiate favorable terms, often driving down prices and impacting Sapura Energy's profit margins. For instance, in fiscal year 2024, revenue from these key clients remained a critical factor, underscoring their continued influence on contract conditions.

The project-based procurement model prevalent in the energy sector, where clients solicit bids for large, long-term contracts, amplifies customer leverage. This competitive bidding process, coupled with the inherent price sensitivity of the oil and gas industry, as seen with oil price fluctuations in 2023, forces service providers like Sapura Energy to offer cost-effective solutions and clearly demonstrate value to secure business.

Customers' demand for highly specific technical requirements and exceptional performance standards further strengthens their bargaining position. Sapura Energy must invest heavily in advanced technology and expertise to meet these stringent demands, allowing clients to dictate pricing and quality. The upstream oil and gas market in 2024 continued to emphasize efficiency and technological advancement, empowering these sophisticated buyers.

Sapura Energy aims to mitigate this customer power through geographic and project diversification, reducing reliance on any single client or region. Furthermore, nurturing strong, long-term relationships with key clients provides a degree of stability, as demonstrated by ongoing partnerships with companies like PTTEP and Chevron.

| Client Type | Leverage Factors | Impact on Sapura Energy | Example Clients | Fiscal Year 2024 Relevance |

|---|---|---|---|---|

| Major Integrated Oil & Gas Companies | Financial Strength, Project Scale, Price Sensitivity | Downward pressure on pricing, reduced profit margins | Petronas, Chevron, PTTEP, ExxonMobil | Critical revenue component, ongoing influence on agreements |

| Project-Based Procurement Users | Competitive Bidding, Contract Volume | Need for competitive pricing and strong bid performance | Various E&P companies | Directly impacts new contract acquisition and order book sustainability |

| Technically Demanding Clients | High Technical Specifications, Stringent Performance Standards | Increased costs for service providers, ability to dictate terms | Companies undertaking complex offshore projects | Continued emphasis on efficiency and technological advancement |

Full Version Awaits

Sapura Energy Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details Sapura Energy's competitive landscape through a comprehensive Porter's Five Forces analysis, examining threats from new entrants, the bargaining power of buyers and suppliers, the intensity of rivalry, and the threat of substitute products or services. This in-depth analysis provides crucial insights for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sapura Energy navigates a complex industry landscape, where the bargaining power of buyers and the intensity of rivalry significantly shape its strategic options. Understanding these forces is crucial for any stakeholder looking to grasp the company's competitive positioning.

The complete report reveals the real forces shaping Sapura Energy’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Equipment and Technology Suppliers

Sapura Energy's dependence on highly specialized equipment and advanced technology for its complex offshore operations, such as drilling rigs and subsea vessels, significantly impacts supplier bargaining power. These sophisticated machinery providers often operate in a niche market.

The limited number of suppliers capable of producing such specialized equipment grants them considerable leverage. This is particularly true when their offerings are proprietary or possess unique, hard-to-replicate capabilities. For instance, a supplier of a unique deep-water drilling system for Sapura Energy could command higher prices.

Switching costs further bolster this supplier power. High costs associated with retraining personnel, integrating new systems, or ensuring compatibility with existing infrastructure mean Sapura Energy faces substantial hurdles if it seeks to change suppliers for critical equipment, reinforcing the suppliers' strong position.

Skilled Labor and Expertise Providers

The upstream oil and gas sector, where Sapura Energy operates, is heavily reliant on a highly specialized workforce. This includes critical roles like petroleum engineers, geoscientists, project managers, and skilled technicians for offshore operations. The demand for these professionals often outstrips the available supply, giving them significant bargaining power.

Suppliers of this expertise, whether they are individual contractors or specialized engineering and technical service firms, can therefore command higher rates and favorable contract terms. For instance, in 2024, the global shortage of experienced offshore drilling personnel continued to drive up day rates for specialized crews. Sapura Energy's capacity to either develop its internal talent pool or its dependence on these external expert providers directly influences the leverage these suppliers hold.

Raw Material and Component Suppliers

The bargaining power of suppliers for raw materials and components, while less potent than for specialized equipment, remains a notable factor for Sapura Energy. For instance, in 2024, global steel prices, a key component in offshore structures, experienced volatility, impacting project budgets. A concentrated supplier base for critical components can also lead to increased costs and potential delays.

Financial Creditors and Lenders

Financial creditors and lenders hold significant sway over Sapura Energy, particularly given its ongoing financial restructuring. Their decisions on providing capital, extending credit, or approving debt modifications are crucial for the company's day-to-day operations and its ability to pursue future projects. For instance, as of early 2024, Sapura Energy's successful completion of its debt restructuring program, which involved significant negotiations with its lenders, underscores this power. The terms agreed upon in these arrangements directly influence the company's financial flexibility and cost of capital.

- Lender Influence: The ability of creditors to dictate terms for new financing or debt relief gives them considerable bargaining power.

- Restructuring Impact: Sapura Energy's recent financial restructuring, completed in early 2024, highlights the crucial role and leverage of its lenders in shaping the company's financial future.

- Capital Dependency: The company's reliance on external funding for its capital-intensive projects amplifies the bargaining power of financial institutions.

Logistics and Support Service Providers

Sapura Energy’s global operations necessitate a robust network of logistics and support service providers, including transportation and field services. The bargaining power of these suppliers can be significant if they are highly concentrated or possess specialized capabilities in regions where Sapura Energy operates. For instance, in 2024, the cost of specialized offshore vessel chartering, a key logistical support, saw fluctuations based on global demand and availability, directly impacting Sapura Energy's project costs.

The efficiency and cost-effectiveness of these logistics and support services are paramount to Sapura Energy’s project execution timelines and ultimately its profitability. Any disruption or significant price increase from these providers can directly affect Sapura Energy’s competitive edge and financial performance.

- Concentration of Providers: A limited number of specialized logistics and support firms in key operating regions can lead to higher bargaining power for those suppliers.

- Specialized Capabilities: Providers offering unique or highly technical services, such as advanced subsea construction support, often command greater leverage.

- Cost Sensitivity: Sapura Energy's profitability is directly tied to the efficiency and cost of these outsourced services, making supplier pricing a critical factor.

- Global Reach Requirements: The need for services across multiple continents means Sapura Energy must navigate varying supplier landscapes and potential regional dependencies.

Supplier Power Shapes Offshore Energy Operations

Sapura Energy faces significant supplier bargaining power due to its reliance on specialized offshore equipment and skilled labor. The limited number of providers for critical machinery and the high switching costs associated with integrating new systems empower these suppliers. Furthermore, the scarcity of experienced offshore personnel in 2024 directly translated into higher rates for specialized crews, impacting Sapura Energy's operational expenses.

Financial creditors also wield considerable influence, as demonstrated by Sapura Energy's early 2024 debt restructuring. The terms negotiated with lenders critically shape the company's financial flexibility and access to capital for its capital-intensive projects.

Suppliers of raw materials like steel, a key component in offshore structures, also exert influence, with price volatility in 2024 affecting project budgets. Similarly, concentrated logistics and support service providers, particularly those offering specialized offshore vessel chartering, can dictate terms due to demand and availability fluctuations.

| Supplier Category | Key Factors Influencing Bargaining Power | Impact on Sapura Energy | 2024 Data/Trend Example |

|---|---|---|---|

| Specialized Equipment Manufacturers | Niche market, proprietary technology, high switching costs | Higher equipment costs, potential project delays if supply is constrained | Continued demand for advanced deep-water drilling systems |

| Skilled Labor Providers (e.g., specialized crews) | Shortage of experienced personnel, high demand | Increased labor costs, potential difficulty in securing adequate staffing | Rising day rates for experienced offshore drilling personnel |

| Financial Creditors | Capital dependency, debt restructuring terms | Influence on financing costs, operational flexibility, and strategic decisions | Successful completion of debt restructuring in early 2024 |

| Raw Material Suppliers (e.g., Steel) | Concentrated supplier base, global commodity price fluctuations | Impact on project budgets and material costs | Volatility in global steel prices affecting offshore structure costs |

| Logistics & Support Services | Concentration of providers, specialized capabilities, regional dependencies | Affects project execution timelines and operational efficiency | Fluctuations in specialized offshore vessel chartering costs |

What is included in the product

This analysis dissects the competitive landscape for Sapura Energy by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the oil and gas services sector.

Instantly visualize Sapura Energy's competitive landscape, highlighting key pressures from rivals and new entrants to inform strategic responses.

Customers Bargaining Power

Large Oil and Gas Companies

Sapura Energy's key clients are typically substantial, integrated oil and gas corporations such as Petronas, Chevron, PTTEP, and ExxonMobil. These industry giants possess considerable financial strength and a consistent stream of large-scale projects, enabling them to negotiate advantageous contract conditions.

The sheer size of these projects grants these major oil and gas companies significant leverage. This concentrated purchasing power can lead to downward pressure on the prices Sapura Energy can charge and, consequently, impact its profit margins.

For instance, in fiscal year 2024, Sapura Energy's revenue from its major clients, particularly Petronas, remained a critical component of its financial performance, highlighting the ongoing influence these large customers wield over the company's commercial agreements and profitability.

Project-Based Procurement

Customers in the energy services sector frequently utilize project-based procurement, a strategy that involves issuing large, long-term contracts for services like Engineering, Procurement, Construction, Installation, and Commissioning (EPCIC), as well as drilling and Operations & Maintenance (O&M).

This approach empowers customers by enabling them to solicit competitive bids from a wide array of service providers, thereby significantly amplifying their bargaining leverage. For Sapura Energy, navigating this environment means its capacity to secure new contracts and sustain a robust order book is directly tied to its performance within these competitive bidding processes.

Price Sensitivity and Cost Control

Customers in the oil and gas sector, including Sapura Energy's clients, exhibit significant price sensitivity. This is driven by the inherent volatility of oil prices, compelling companies to rigorously control costs and boost operational efficiency. For instance, in 2023, global oil prices fluctuated, impacting the budgets of exploration and production companies, which in turn pressures service providers like Sapura Energy to offer more competitive pricing.

This heightened price sensitivity means that Sapura Energy must not only provide cost-effective solutions but also clearly articulate the value proposition of its services. Demonstrating tangible benefits and a strong return on investment is crucial for securing contracts in a market where every dollar counts. The company's focus on operational discipline and margin preservation is a direct response to this customer demand.

Technical Specifications and Performance Demands

Customers in the upstream oil and gas sector, including major energy companies, often impose highly specific technical requirements and expect exceptional performance from their service providers. This necessity for advanced technology and proven project execution capabilities significantly bolsters their bargaining power. For instance, a major oil discovery might necessitate specialized subsea engineering capabilities that only a few companies can provide, allowing the customer to negotiate favorable terms.

The stringent performance demands translate directly into higher costs for service providers, who must invest heavily in research, development, and cutting-edge equipment. This capital intensity means that customers, by virtue of their purchasing power and project scale, can effectively dictate pricing and quality standards. In 2024, the global upstream oil and gas market saw continued emphasis on efficiency and technological advancement, further empowering sophisticated buyers.

- High Technical Specifications: Buyers demand specialized solutions, limiting the pool of qualified suppliers.

- Performance Standards: Stringent operational requirements necessitate significant investment by service providers.

- Customer Leverage: The need for specialized capabilities allows customers to negotiate pricing and contract terms.

- Market Influence: Major clients can influence industry-wide standards through their procurement practices.

Diversification of Customer Base

Sapura Energy's strategy to diversify its customer base across various regions and project types is crucial in lessening the influence of any single client. This approach helps to spread risk and reduce dependency on a few large contracts.

Maintaining long-term relationships with key clients, like those with PTTEP and Chevron in Thailand, provides a degree of stability. These established partnerships, often built on trust and a track record of successful project delivery, can act as a buffer against the bargaining power of individual customers.

- Geographic Diversification: Expanding into new markets reduces reliance on any one region's economic conditions or client base.

- Project Type Variety: Engaging in different types of projects, such as offshore construction, drilling, and maintenance, broadens Sapura Energy's appeal and client pool.

- Client Relationship Management: Nurturing strong, long-term partnerships can foster loyalty and create more stable revenue streams, thereby mitigating customer power.

Client Power Shapes Sapura Energy's Market Dynamics

Sapura Energy faces significant bargaining power from its major clients, primarily large integrated oil and gas corporations. These clients, such as Petronas and Chevron, leverage their substantial financial clout and the sheer scale of projects to negotiate favorable terms, often driving down prices and impacting Sapura Energy's profit margins. For instance, in fiscal year 2024, revenue from these key clients remained a critical factor, underscoring their continued influence on contract conditions.

The project-based procurement model prevalent in the energy sector, where clients solicit bids for large, long-term contracts, amplifies customer leverage. This competitive bidding process, coupled with the inherent price sensitivity of the oil and gas industry, as seen with oil price fluctuations in 2023, forces service providers like Sapura Energy to offer cost-effective solutions and clearly demonstrate value to secure business.

Customers' demand for highly specific technical requirements and exceptional performance standards further strengthens their bargaining position. Sapura Energy must invest heavily in advanced technology and expertise to meet these stringent demands, allowing clients to dictate pricing and quality. The upstream oil and gas market in 2024 continued to emphasize efficiency and technological advancement, empowering these sophisticated buyers.

Sapura Energy aims to mitigate this customer power through geographic and project diversification, reducing reliance on any single client or region. Furthermore, nurturing strong, long-term relationships with key clients provides a degree of stability, as demonstrated by ongoing partnerships with companies like PTTEP and Chevron.

| Client Type | Leverage Factors | Impact on Sapura Energy | Example Clients | Fiscal Year 2024 Relevance |

|---|---|---|---|---|

| Major Integrated Oil & Gas Companies | Financial Strength, Project Scale, Price Sensitivity | Downward pressure on pricing, reduced profit margins | Petronas, Chevron, PTTEP, ExxonMobil | Critical revenue component, ongoing influence on agreements |

| Project-Based Procurement Users | Competitive Bidding, Contract Volume | Need for competitive pricing and strong bid performance | Various E&P companies | Directly impacts new contract acquisition and order book sustainability |

| Technically Demanding Clients | High Technical Specifications, Stringent Performance Standards | Increased costs for service providers, ability to dictate terms | Companies undertaking complex offshore projects | Continued emphasis on efficiency and technological advancement |

Full Version Awaits

Sapura Energy Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details Sapura Energy's competitive landscape through a comprehensive Porter's Five Forces analysis, examining threats from new entrants, the bargaining power of buyers and suppliers, the intensity of rivalry, and the threat of substitute products or services. This in-depth analysis provides crucial insights for strategic decision-making.