Savills Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

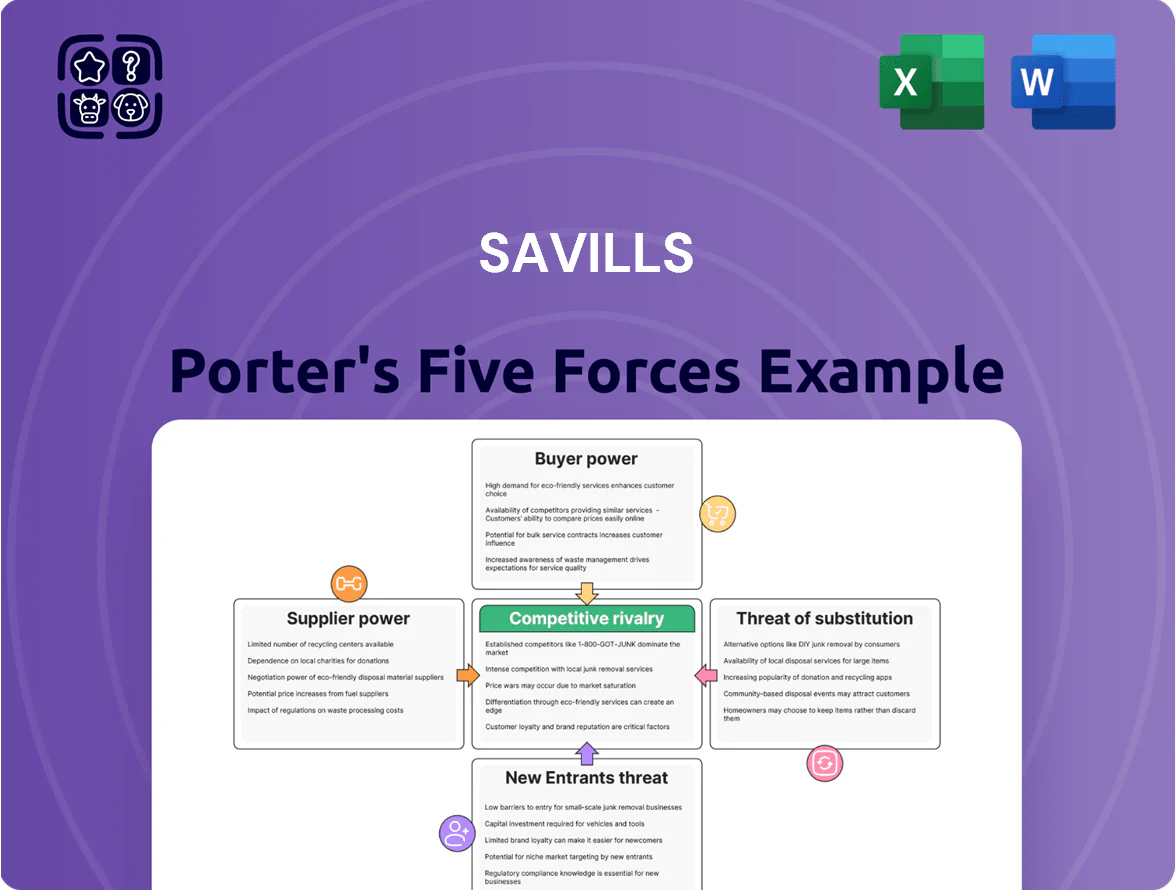

Savills faces moderate buyer power and significant rivalry from global and local real estate firms, while supplier and substitute threats vary across commercial and residential segments; regulatory shifts also shape margins and expansion. This snapshot highlights key competitive tensions but scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Savills’s market pressures, force-by-force ratings, visuals, and strategic implications in depth.

Suppliers Bargaining Power

Specialized Human Capital and Professional Talent

Primary suppliers for Savills are its brokers, advisors, and technical consultants who enable complex deals; in 2025, global demand for ESG and sustainable-development specialists rose ~22% year-over-year, pushing top talent salaries up 10–18% in major markets.

That wage pressure and a 12% annual attrition rate for senior agents mean these professionals hold strong bargaining power, so Savills must match compensation benchmarks and strengthen culture to avoid losses to rivals and boutiques.

Technology and Data Analytics Providers

Savills depends on third-party market data, CRM and analytics vendors; in 2024 about 34% of global real estate firms reported using AI platforms for valuation, raising supplier leverage. Vendors control proprietary algorithms and premium data feeds, giving them pricing power—enterprise AI subscriptions rose ~18% in 2023. High switching costs stem from deep integrations and the need to preserve historical data continuity, often exceeding $1m for national rollouts.

Regulatory and Compliance Bodies

Regulatory and compliance bodies—governments and professional associations—set the legal framework Savills must follow, affecting operations across 70+ markets; non‑compliance fines averaged up to 2% of revenue in real estate sectors in 2024. Compliance with evolving international property standards and local zoning laws forces ongoing investment in legal teams and admin overheads; Savills reported governance and compliance costs rising ~6% year‑on‑year in 2024. These mandatory standards raise entry and operating costs, constraining pricing flexibility and margins across jurisdictions.

PropTech and Digital Infrastructure Vendors

Cloud and cybersecurity vendors are now critical to Savills, supporting global platforms that handled an estimated £1.2bn in digital transactions for commercial real estate in 2024; outages or breaches would disrupt revenue and reputation.

Their bargaining power is high because specialized PropTech integrations and data residency needs make switching costly—typical migration projects exceed $2–5m and take 6–12 months.

- Cloud/cyber vendors = backbone of operations

- 2024 CRE digital transactions ~£1.2bn

- Migration cost $2–5m, 6–12 months

- High switching risk raises supplier leverage

Office Space and Physical Infrastructure

Savills needs premium offices in hubs like London, New York and Singapore to host clients and protect brand value; Class A rents there averaged £89/sq ft in West End London Q4 2024, $95/sq ft in Manhattan 2024, and SGD 13.5/sq ft in Singapore CBD 2024, so landlords hold pricing power.

Even as a real estate adviser, Savills faces the same lease risks and vacancy cycles; tight vacancy (West End 3.6% Q4 2024) increases landlord leverage during renewals and relocations.

- High rent levels in top hubs

- Low vacancy boosts landlord leverage

- Savills’ expertise reduces but doesn’t remove tenant risk

Suppliers Gain Leverage: Talent, AI Lock‑In, Compliance and Skyrocketing Office Rents

Suppliers wield high bargaining power: talent shortages (ESG specialist demand +22% in 2025; salaries +10–18%), vendor lock‑in (34% firms using AI in 2024; enterprise AI subscriptions +18% in 2023; migration $2–5m, 6–12 months), compliance costs (+6% y/y 2024; fines up to 2% revenue), and premium office rents (West End £89/sq ft Q4 2024; Manhattan $95/sq ft 2024).

| Metric | 2024–25 |

|---|---|

| ESG demand | +22% (2025) |

| AI adoption | 34% (2024) |

| Migration cost | $2–5m |

| West End rent | £89/sq ft Q4 2024 |

What is included in the product

Uncovers key competitive drivers for Savills—buyers, suppliers, entrants, substitutes, and rivalry—highlighting pricing power, market entry barriers, emerging disruptors, and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet for Savills—perfect for swift strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Institutional Investor Concentration

Large institutional clients—pension funds and sovereign wealth funds—account for an estimated 30–40% of Savills' advisory revenue in 2024, giving them strong bargaining power; they demand bespoke service packages and fee discounts because they manage trillions in assets (example: Norway’s GPFG held NOK 14.5 trillion in 2024). Their ability to shift multi-billion-dollar portfolios between global advisors forces Savills to trade short-term margins for long-term relationship retention.

Corporate Occupier Demands

Multinational corporate occupiers push Savills for borderless leasing and global facilities management, with 62% of Fortune 500 firms using multi-market RFPs in 2024, forcing price competition on standardized property services.

Competitive bidding drove average management fees down ~8% in EMEA offices 2023–24, so Savills must boost margins by selling specialized advisory—portfolio strategy, ESG certification, and workplace analytics—that command 15–30% premium.

High Net Worth Individual Influence

High-net-worth individuals (HNWIs) in residential markets demand personalized, discreet service and often require senior-partner involvement; globally there were 6.6 million HNWIs in 2024, controlling about $96 trillion in wealth, so their choices shift revenue materially.

Their financial flexibility lets them pick luxury firms or boutiques—Savills faces competition as top 1% buyers can switch providers quickly, raising client retention costs.

HNWIs also sway market sentiment and referrals within elite networks; a single referral can influence multiple high-value transactions, amplifying their bargaining power.

Information Transparency and Digital Access

Information transparency from online portals and public data has slashed information asymmetry that once favored brokers; as of 2024, 78% of UK buyers used portals (Rightmove, Zoopla) before contacting agents, and comparable-transaction access rose 42% since 2018.

Customers now enter talks armed with market prices, historical trends, and comps, enabling tougher price and term negotiations and reducing brokers’ role as sole gatekeepers.

- 78% of UK buyers use portals pre-contact

- 42% rise in comps access since 2018

- Average agent fee pressure: down ~0.3–0.5ppt

Low Switching Costs for Standardized Services

Institutional buyers, HNWIs and portals squeeze UK agents—fees fall as volumes drop

Large institutional clients (30–40% of Savills advisory revenue in 2024) and 6.6M HNWIs (controlling $96T) exert strong bargaining power, forcing fee discounts and bespoke offers; portals(78% UK buyers) and 42% rise in comps since 2018 cut brokers’ informational edge, lowering agent fees ~0.3–0.5ppt and driving price-based switching amid UK residential volumes down 8% in 2024.

| Metric | 2024 value |

|---|---|

| Institutional share of advisory | 30–40% |

| HNWIs (global) | 6.6M; $96T |

| UK buyers using portals | 78% |

| Rise in comps access since 2018 | 42% |

| Agent fee pressure | -0.3–0.5ppt |

| UK residential volumes YoY | -8% |

What You See Is What You Get

Savills Porter's Five Forces Analysis

This preview shows the exact Savills Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Savills faces moderate buyer power and significant rivalry from global and local real estate firms, while supplier and substitute threats vary across commercial and residential segments; regulatory shifts also shape margins and expansion. This snapshot highlights key competitive tensions but scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Savills’s market pressures, force-by-force ratings, visuals, and strategic implications in depth.

Suppliers Bargaining Power

Specialized Human Capital and Professional Talent

Primary suppliers for Savills are its brokers, advisors, and technical consultants who enable complex deals; in 2025, global demand for ESG and sustainable-development specialists rose ~22% year-over-year, pushing top talent salaries up 10–18% in major markets.

That wage pressure and a 12% annual attrition rate for senior agents mean these professionals hold strong bargaining power, so Savills must match compensation benchmarks and strengthen culture to avoid losses to rivals and boutiques.

Technology and Data Analytics Providers

Savills depends on third-party market data, CRM and analytics vendors; in 2024 about 34% of global real estate firms reported using AI platforms for valuation, raising supplier leverage. Vendors control proprietary algorithms and premium data feeds, giving them pricing power—enterprise AI subscriptions rose ~18% in 2023. High switching costs stem from deep integrations and the need to preserve historical data continuity, often exceeding $1m for national rollouts.

Regulatory and Compliance Bodies

Regulatory and compliance bodies—governments and professional associations—set the legal framework Savills must follow, affecting operations across 70+ markets; non‑compliance fines averaged up to 2% of revenue in real estate sectors in 2024. Compliance with evolving international property standards and local zoning laws forces ongoing investment in legal teams and admin overheads; Savills reported governance and compliance costs rising ~6% year‑on‑year in 2024. These mandatory standards raise entry and operating costs, constraining pricing flexibility and margins across jurisdictions.

PropTech and Digital Infrastructure Vendors

Cloud and cybersecurity vendors are now critical to Savills, supporting global platforms that handled an estimated £1.2bn in digital transactions for commercial real estate in 2024; outages or breaches would disrupt revenue and reputation.

Their bargaining power is high because specialized PropTech integrations and data residency needs make switching costly—typical migration projects exceed $2–5m and take 6–12 months.

- Cloud/cyber vendors = backbone of operations

- 2024 CRE digital transactions ~£1.2bn

- Migration cost $2–5m, 6–12 months

- High switching risk raises supplier leverage

Office Space and Physical Infrastructure

Savills needs premium offices in hubs like London, New York and Singapore to host clients and protect brand value; Class A rents there averaged £89/sq ft in West End London Q4 2024, $95/sq ft in Manhattan 2024, and SGD 13.5/sq ft in Singapore CBD 2024, so landlords hold pricing power.

Even as a real estate adviser, Savills faces the same lease risks and vacancy cycles; tight vacancy (West End 3.6% Q4 2024) increases landlord leverage during renewals and relocations.

- High rent levels in top hubs

- Low vacancy boosts landlord leverage

- Savills’ expertise reduces but doesn’t remove tenant risk

Suppliers Gain Leverage: Talent, AI Lock‑In, Compliance and Skyrocketing Office Rents

Suppliers wield high bargaining power: talent shortages (ESG specialist demand +22% in 2025; salaries +10–18%), vendor lock‑in (34% firms using AI in 2024; enterprise AI subscriptions +18% in 2023; migration $2–5m, 6–12 months), compliance costs (+6% y/y 2024; fines up to 2% revenue), and premium office rents (West End £89/sq ft Q4 2024; Manhattan $95/sq ft 2024).

| Metric | 2024–25 |

|---|---|

| ESG demand | +22% (2025) |

| AI adoption | 34% (2024) |

| Migration cost | $2–5m |

| West End rent | £89/sq ft Q4 2024 |

What is included in the product

Uncovers key competitive drivers for Savills—buyers, suppliers, entrants, substitutes, and rivalry—highlighting pricing power, market entry barriers, emerging disruptors, and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet for Savills—perfect for swift strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Institutional Investor Concentration

Large institutional clients—pension funds and sovereign wealth funds—account for an estimated 30–40% of Savills' advisory revenue in 2024, giving them strong bargaining power; they demand bespoke service packages and fee discounts because they manage trillions in assets (example: Norway’s GPFG held NOK 14.5 trillion in 2024). Their ability to shift multi-billion-dollar portfolios between global advisors forces Savills to trade short-term margins for long-term relationship retention.

Corporate Occupier Demands

Multinational corporate occupiers push Savills for borderless leasing and global facilities management, with 62% of Fortune 500 firms using multi-market RFPs in 2024, forcing price competition on standardized property services.

Competitive bidding drove average management fees down ~8% in EMEA offices 2023–24, so Savills must boost margins by selling specialized advisory—portfolio strategy, ESG certification, and workplace analytics—that command 15–30% premium.

High Net Worth Individual Influence

High-net-worth individuals (HNWIs) in residential markets demand personalized, discreet service and often require senior-partner involvement; globally there were 6.6 million HNWIs in 2024, controlling about $96 trillion in wealth, so their choices shift revenue materially.

Their financial flexibility lets them pick luxury firms or boutiques—Savills faces competition as top 1% buyers can switch providers quickly, raising client retention costs.

HNWIs also sway market sentiment and referrals within elite networks; a single referral can influence multiple high-value transactions, amplifying their bargaining power.

Information Transparency and Digital Access

Information transparency from online portals and public data has slashed information asymmetry that once favored brokers; as of 2024, 78% of UK buyers used portals (Rightmove, Zoopla) before contacting agents, and comparable-transaction access rose 42% since 2018.

Customers now enter talks armed with market prices, historical trends, and comps, enabling tougher price and term negotiations and reducing brokers’ role as sole gatekeepers.

- 78% of UK buyers use portals pre-contact

- 42% rise in comps access since 2018

- Average agent fee pressure: down ~0.3–0.5ppt

Low Switching Costs for Standardized Services

Institutional buyers, HNWIs and portals squeeze UK agents—fees fall as volumes drop

Large institutional clients (30–40% of Savills advisory revenue in 2024) and 6.6M HNWIs (controlling $96T) exert strong bargaining power, forcing fee discounts and bespoke offers; portals(78% UK buyers) and 42% rise in comps since 2018 cut brokers’ informational edge, lowering agent fees ~0.3–0.5ppt and driving price-based switching amid UK residential volumes down 8% in 2024.

| Metric | 2024 value |

|---|---|

| Institutional share of advisory | 30–40% |

| HNWIs (global) | 6.6M; $96T |

| UK buyers using portals | 78% |

| Rise in comps access since 2018 | 42% |

| Agent fee pressure | -0.3–0.5ppt |

| UK residential volumes YoY | -8% |

What You See Is What You Get

Savills Porter's Five Forces Analysis

This preview shows the exact Savills Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.