Savills PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological change are reshaping Savills' strategic outlook in our concise PESTLE snapshot—perfect for investors and advisors who need fast, actionable context; purchase the full PESTLE for the complete, editable breakdown and immediate insights to guide decisions.

Political factors

Geopolitical instability and global capital flows

Ongoing geopolitical tensions in Eastern Europe and the Middle East have reduced investor risk appetite, with cross-border real estate deal volumes down 12% globally in 2024 versus 2023, according to RCA data, pushing capital toward perceived safe-havens.

Savills must navigate shifting patterns as UK and Singapore investment inflows rose 18% and 22% respectively in 2024, capturing increased allocations from Europe and Asia-Pacific investors.

Political stability remains a primary driver for institutional allocation into 2026, with the top 50 global pension funds reporting a 35% weighting preference for markets with stable governance and predictable regulatory regimes.

Government housing and planning reforms

In the UK and key markets, government planning reforms to hit housing targets—England's 300,000 annual homes pledge and Scotland's 110,000 target by 2032—boost Savills' advisory work by increasing demand for site assembly and consenting services.

Legislative moves to streamline approvals, such as England's 2024 planning reforms reducing decision times by up to 30%, can lift residential and land transaction volumes, benefiting Savills' brokerage revenues.

Savills leverages planning consultancy expertise across permitting, viability and masterplanning, capturing higher-fee advisory mandates as public-sector and private clients seek faster delivery and financing certainty.

Trade policies and international relations

Changes in trade agreements and diplomatic relations alter corporate relocation strategies and industrial real estate demand; Savills tracks that 2024 saw a 12% rise in enquiries for cross-border relocations amid renewed US-EU and UK-EU talks.

Savills monitors shifts like near-shoring and friend-shoring—responsible for a 9% increase in demand for logistics hubs in 2023–24—reshaping requirements for warehousing and manufacturing facilities.

Political decisions on tariffs and trade barriers raised operational costs for multinational clients by an estimated 3–5% in 2024, influencing lease terms and site selection.

Taxation policy for foreign investors

Changes in stamp duty, capital gains and corporate tax for foreign owners—such as the UK’s 2% non-resident stamp duty surcharge and recent proposals to align non-resident CGT—can cool investment flows or spur market entry; Savills must advise on tax-efficient structuring to preserve returns.

Political motives—housing affordability, revenue targets (UK property tax receipts ~16.6bn GBP in 2023/24)—drive shifts; anticipating these preserves Savills’ edge in investment management and client structuring.

- Non-resident stamp duty surcharge (UK 2%) impacts pricing and yield

- Rising CGT/corporate rates reduce after-tax IRR for investors

- Tax receipts and affordability goals signal more policy tweaks

- Savills needs proactive tax-structuring advisory to protect flows

Public sector infrastructure investment

Large-scale government spending—UK committed 2024–25 to £600bn National Infrastructure Plan and EU recovery funds €200bn—boosts demand for commercial and residential development in newly connected zones, lifting valuations and leasing activity that Savills captures through transactional services.

Savills advisory teams time recommendations to multi-year budget cycles and projects like HS2 and urban regeneration, using projected uplift rates (often 10–25% near major schemes) to forecast long-term growth hotspots for clients.

- £600bn UK infrastructure pipeline 2024–25

- HS2/major projects can raise local values 10–25%

- Advisory forecasting tied to government budget cycles

Geopolitics dent cross‑border deals -12%; UK & Singapore inflows surge, infra lifts local values

Geopolitical tensions cut cross-border deals 12% in 2024; UK and Singapore inflows rose 18% and 22%. Planning reforms (England target 300,000/yr) and faster approvals (decision times -30%) boost advisory fees. Non-resident stamp duty +2% and proposed CGT changes alter yields; large infrastructure pipelines (£600bn UK, €200bn EU) lift local values 10–25% near projects.

| Indicator | 2024/25 |

|---|---|

| Cross-border deals | -12% |

| UK inflows | +18% |

| Singapore inflows | +22% |

| UK infra pipeline | £600bn |

What is included in the product

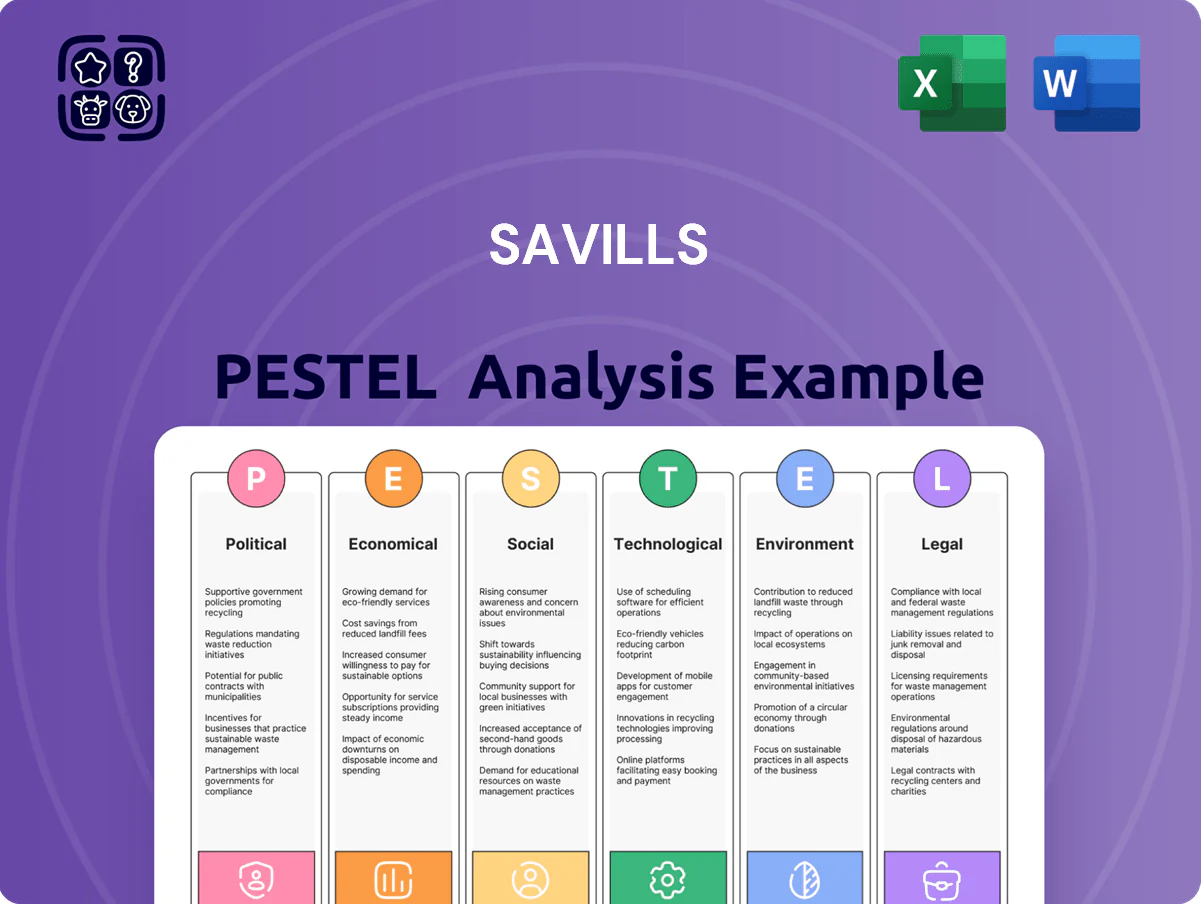

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Savills, with each section backed by current data and market trends to identify risks and opportunities for executives, investors, and strategists.

Condenses Savills' full PESTLE into a concise, easily shareable summary that supports quick alignment across teams and can be dropped into presentations or planning sessions for fast, practical decision-making.

Economic factors

Interest rate cycles and debt availability

As central banks stabilized rates after 2023–24 inflation peaks, global policy rates averaged about 4.5% by end-2025, lowering debt costs and boosting real estate transaction activity.

Savills investment and capital markets are sensitive to the spread between property yields and borrowing costs; UK prime yields tightened to c.4.0% in 2025, narrowing gaps and improving deal IRRs.

A more predictable monetary backdrop lifted market liquidity, with global commercial real estate transaction volumes rising ~18% in 2025 versus 2024, prompting renewed large-scale acquisitions.

Global economic growth and office demand

Global GDP growth slowed to 3.1% in 2024 (IMF) which tempers corporate hiring and reduces office footprint expansion, though US growth near 2.4% and India at 6.3% sustain demand in key markets.

Savills uses real-time indicators—PMI, vacancy rates (prime office vacancy averaged 12% in EMEA H2 2024) and rent growth—to recommend leasing and portfolio optimization focused on cost-efficiency.

Sector divergence is clear: retail and some finance subsectors retrench, while tech and life sciences drove 7–10% premium leasing activity for lab-ready and flexible office space in 2024.

Currency volatility and cross-border investment

Fluctuations in the Pound, Euro and Dollar alter international buyers’ purchasing power—GBP fell ~7% vs USD in 2023, making UK assets relatively cheaper to dollar investors while EUR/USD volatility of ±5% in 2024 shifted eurozone cross-border flows.

Savills’ global network captured currency-driven deals as UK and continental markets saw foreign demand rise; cross-border transactions accounted for ~30% of prime London activity in 2024.

Managing currency risk is integral to Savills’ advisory: hedging strategies, FX sensitivity models and scenario DCFs are routinely provided to institutional and UHNW clients to protect returns.

Inflationary pressures on construction costs

Despite headline UK CPI easing to 3.9% in 2025, UK construction input costs rose 4.6% year-on-year in Q4 2025 driven by labor shortages and material prices, keeping project viability under pressure.

Savills development consultancy must model these inputs precisely—labor accounts for ~30% of build costs and timber/steel cement spikes can add 5–10% to budgets—affecting bankability and developer margins.

Elevated build costs constrain new supply, supporting rental growth: prime London office rents rose 6% in 2025 as limited new completions tightened markets.

- Headline CPI 3.9% (2025)

- Construction input costs +4.6% YoY Q4 2025

- Labor ~30% of build costs

- Material shocks can add 5–10% to budgets

- Prime London office rents +6% in 2025

Consumer spending and retail sector evolution

Economic health and disposable income drive retail and leisure real estate: UK household real consumption rose 1.2% in 2024, supporting prime high-street rents while secondary centres see pressure.

Savills' footfall and consumer-behaviour data (2024: city centre footfall -8% YoY; leisure visits +4%) helps landlords and tenants navigate omnichannel shifts.

Luxury retail showed resilience in 2024 with global personal luxury goods sales up ~5%, while Savills teams advise repurposing secondary centres into mixed-use and logistics.

- Household consumption +1.2% (UK, 2024)

- City centre footfall -8% YoY (2024); leisure +4%

- Luxury goods sales +5% (2024)

- Focus: mixed-use conversion and last-mile logistics

Higher rates, tighter supply drive 18% surge in global CRE and 6% London rent rise

Central-bank rates averaged ~4.5% by end‑2025, supporting an ~18% rise in global CRE transactions (2025 vs 2024); UK CPI 3.9% (2025) and construction input costs +4.6% YoY Q4 2025 raised build costs, constraining supply and lifting prime rents (London offices +6% 2025); cross‑border deals ~30% of prime London 2024; FX moves (GBP -7% vs USD in 2023) altered buyer demand.

| Metric | Value |

|---|---|

| Policy rate (avg) | 4.5% (end‑2025) |

| CRE volumes | +18% (2025 vs 2024) |

| UK CPI | 3.9% (2025) |

| Construction costs | +4.6% YoY Q4 2025 |

| Prime London rent | +6% (2025) |

What You See Is What You Get

Savills PESTLE Analysis

The preview shown here is the exact Savills PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological change are reshaping Savills' strategic outlook in our concise PESTLE snapshot—perfect for investors and advisors who need fast, actionable context; purchase the full PESTLE for the complete, editable breakdown and immediate insights to guide decisions.

Political factors

Geopolitical instability and global capital flows

Ongoing geopolitical tensions in Eastern Europe and the Middle East have reduced investor risk appetite, with cross-border real estate deal volumes down 12% globally in 2024 versus 2023, according to RCA data, pushing capital toward perceived safe-havens.

Savills must navigate shifting patterns as UK and Singapore investment inflows rose 18% and 22% respectively in 2024, capturing increased allocations from Europe and Asia-Pacific investors.

Political stability remains a primary driver for institutional allocation into 2026, with the top 50 global pension funds reporting a 35% weighting preference for markets with stable governance and predictable regulatory regimes.

Government housing and planning reforms

In the UK and key markets, government planning reforms to hit housing targets—England's 300,000 annual homes pledge and Scotland's 110,000 target by 2032—boost Savills' advisory work by increasing demand for site assembly and consenting services.

Legislative moves to streamline approvals, such as England's 2024 planning reforms reducing decision times by up to 30%, can lift residential and land transaction volumes, benefiting Savills' brokerage revenues.

Savills leverages planning consultancy expertise across permitting, viability and masterplanning, capturing higher-fee advisory mandates as public-sector and private clients seek faster delivery and financing certainty.

Trade policies and international relations

Changes in trade agreements and diplomatic relations alter corporate relocation strategies and industrial real estate demand; Savills tracks that 2024 saw a 12% rise in enquiries for cross-border relocations amid renewed US-EU and UK-EU talks.

Savills monitors shifts like near-shoring and friend-shoring—responsible for a 9% increase in demand for logistics hubs in 2023–24—reshaping requirements for warehousing and manufacturing facilities.

Political decisions on tariffs and trade barriers raised operational costs for multinational clients by an estimated 3–5% in 2024, influencing lease terms and site selection.

Taxation policy for foreign investors

Changes in stamp duty, capital gains and corporate tax for foreign owners—such as the UK’s 2% non-resident stamp duty surcharge and recent proposals to align non-resident CGT—can cool investment flows or spur market entry; Savills must advise on tax-efficient structuring to preserve returns.

Political motives—housing affordability, revenue targets (UK property tax receipts ~16.6bn GBP in 2023/24)—drive shifts; anticipating these preserves Savills’ edge in investment management and client structuring.

- Non-resident stamp duty surcharge (UK 2%) impacts pricing and yield

- Rising CGT/corporate rates reduce after-tax IRR for investors

- Tax receipts and affordability goals signal more policy tweaks

- Savills needs proactive tax-structuring advisory to protect flows

Public sector infrastructure investment

Large-scale government spending—UK committed 2024–25 to £600bn National Infrastructure Plan and EU recovery funds €200bn—boosts demand for commercial and residential development in newly connected zones, lifting valuations and leasing activity that Savills captures through transactional services.

Savills advisory teams time recommendations to multi-year budget cycles and projects like HS2 and urban regeneration, using projected uplift rates (often 10–25% near major schemes) to forecast long-term growth hotspots for clients.

- £600bn UK infrastructure pipeline 2024–25

- HS2/major projects can raise local values 10–25%

- Advisory forecasting tied to government budget cycles

Geopolitics dent cross‑border deals -12%; UK & Singapore inflows surge, infra lifts local values

Geopolitical tensions cut cross-border deals 12% in 2024; UK and Singapore inflows rose 18% and 22%. Planning reforms (England target 300,000/yr) and faster approvals (decision times -30%) boost advisory fees. Non-resident stamp duty +2% and proposed CGT changes alter yields; large infrastructure pipelines (£600bn UK, €200bn EU) lift local values 10–25% near projects.

| Indicator | 2024/25 |

|---|---|

| Cross-border deals | -12% |

| UK inflows | +18% |

| Singapore inflows | +22% |

| UK infra pipeline | £600bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Savills, with each section backed by current data and market trends to identify risks and opportunities for executives, investors, and strategists.

Condenses Savills' full PESTLE into a concise, easily shareable summary that supports quick alignment across teams and can be dropped into presentations or planning sessions for fast, practical decision-making.

Economic factors

Interest rate cycles and debt availability

As central banks stabilized rates after 2023–24 inflation peaks, global policy rates averaged about 4.5% by end-2025, lowering debt costs and boosting real estate transaction activity.

Savills investment and capital markets are sensitive to the spread between property yields and borrowing costs; UK prime yields tightened to c.4.0% in 2025, narrowing gaps and improving deal IRRs.

A more predictable monetary backdrop lifted market liquidity, with global commercial real estate transaction volumes rising ~18% in 2025 versus 2024, prompting renewed large-scale acquisitions.

Global economic growth and office demand

Global GDP growth slowed to 3.1% in 2024 (IMF) which tempers corporate hiring and reduces office footprint expansion, though US growth near 2.4% and India at 6.3% sustain demand in key markets.

Savills uses real-time indicators—PMI, vacancy rates (prime office vacancy averaged 12% in EMEA H2 2024) and rent growth—to recommend leasing and portfolio optimization focused on cost-efficiency.

Sector divergence is clear: retail and some finance subsectors retrench, while tech and life sciences drove 7–10% premium leasing activity for lab-ready and flexible office space in 2024.

Currency volatility and cross-border investment

Fluctuations in the Pound, Euro and Dollar alter international buyers’ purchasing power—GBP fell ~7% vs USD in 2023, making UK assets relatively cheaper to dollar investors while EUR/USD volatility of ±5% in 2024 shifted eurozone cross-border flows.

Savills’ global network captured currency-driven deals as UK and continental markets saw foreign demand rise; cross-border transactions accounted for ~30% of prime London activity in 2024.

Managing currency risk is integral to Savills’ advisory: hedging strategies, FX sensitivity models and scenario DCFs are routinely provided to institutional and UHNW clients to protect returns.

Inflationary pressures on construction costs

Despite headline UK CPI easing to 3.9% in 2025, UK construction input costs rose 4.6% year-on-year in Q4 2025 driven by labor shortages and material prices, keeping project viability under pressure.

Savills development consultancy must model these inputs precisely—labor accounts for ~30% of build costs and timber/steel cement spikes can add 5–10% to budgets—affecting bankability and developer margins.

Elevated build costs constrain new supply, supporting rental growth: prime London office rents rose 6% in 2025 as limited new completions tightened markets.

- Headline CPI 3.9% (2025)

- Construction input costs +4.6% YoY Q4 2025

- Labor ~30% of build costs

- Material shocks can add 5–10% to budgets

- Prime London office rents +6% in 2025

Consumer spending and retail sector evolution

Economic health and disposable income drive retail and leisure real estate: UK household real consumption rose 1.2% in 2024, supporting prime high-street rents while secondary centres see pressure.

Savills' footfall and consumer-behaviour data (2024: city centre footfall -8% YoY; leisure visits +4%) helps landlords and tenants navigate omnichannel shifts.

Luxury retail showed resilience in 2024 with global personal luxury goods sales up ~5%, while Savills teams advise repurposing secondary centres into mixed-use and logistics.

- Household consumption +1.2% (UK, 2024)

- City centre footfall -8% YoY (2024); leisure +4%

- Luxury goods sales +5% (2024)

- Focus: mixed-use conversion and last-mile logistics

Higher rates, tighter supply drive 18% surge in global CRE and 6% London rent rise

Central-bank rates averaged ~4.5% by end‑2025, supporting an ~18% rise in global CRE transactions (2025 vs 2024); UK CPI 3.9% (2025) and construction input costs +4.6% YoY Q4 2025 raised build costs, constraining supply and lifting prime rents (London offices +6% 2025); cross‑border deals ~30% of prime London 2024; FX moves (GBP -7% vs USD in 2023) altered buyer demand.

| Metric | Value |

|---|---|

| Policy rate (avg) | 4.5% (end‑2025) |

| CRE volumes | +18% (2025 vs 2024) |

| UK CPI | 3.9% (2025) |

| Construction costs | +4.6% YoY Q4 2025 |

| Prime London rent | +6% (2025) |

What You See Is What You Get

Savills PESTLE Analysis

The preview shown here is the exact Savills PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.