SBA Communications Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

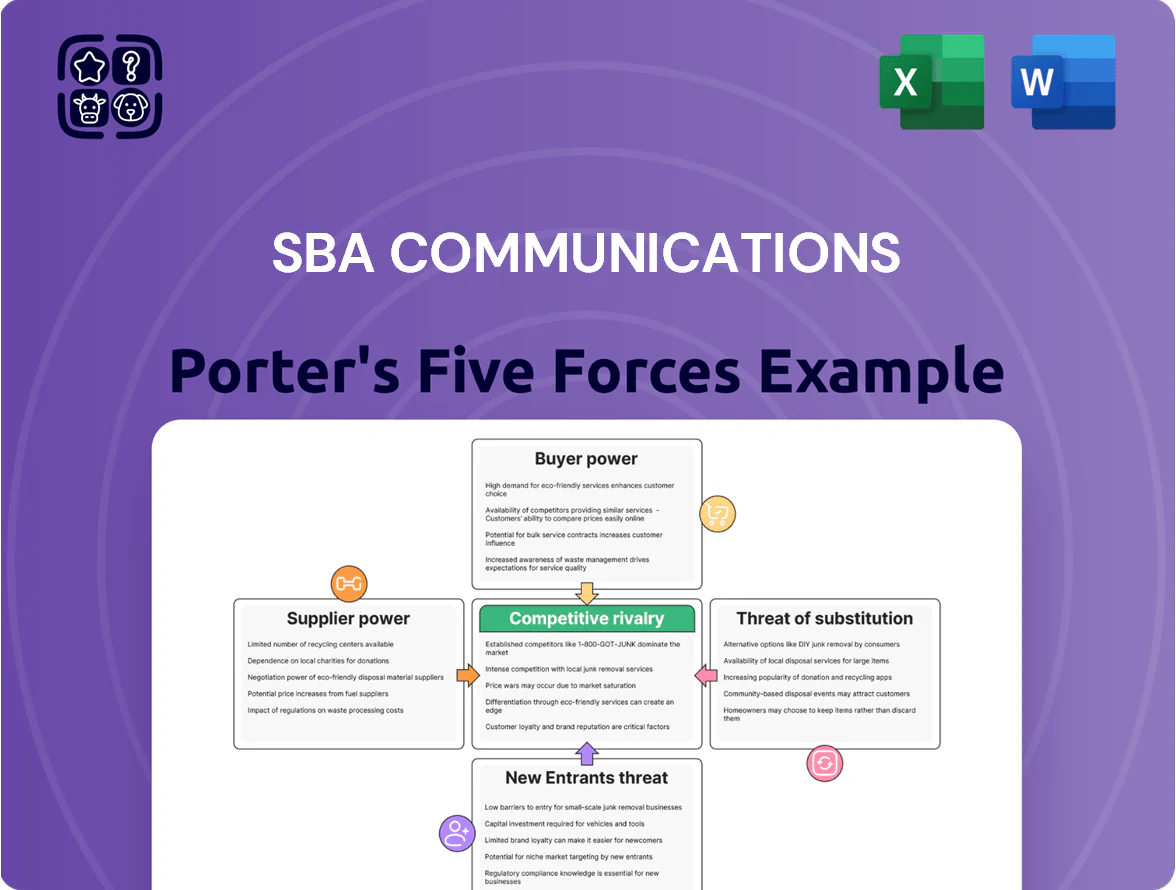

SBA Communications faces powerful buyer and supplier dynamics, evolving threat from new entrants via towerless tech, and substitution pressures from small-cell solutions; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to SBA Communications’s market position.

Suppliers Bargaining Power

Ground Lease Landowner Leverage

SBA commonly holds long-term ground leases from private and public landowners for tower sites, exposing it to renewal rent increases; however, over 70% of U.S. towers sit on leases with remaining terms exceeding 10 years, limiting immediate landowner leverage. The specialized site location and estimated relocation costs of $200k–$1M per tower sharply constrain landowner bargaining power. SBA mitigates lease risk by negotiating extensions—SBA reported buying 1,200 sites through 2024—and selectively purchasing land to remove supplier exposure.

Specialized Construction and Labor

Building and maintaining towers requires specialized engineering and technical labor that tightens during major upgrade cycles; in 2024 U.S. tower construction costs rose about 6% year-over-year, reflecting labor scarcity. These providers can push SBA Communications (SBA) pricing for site development and maintenance during high demand, squeezing margins. SBA reduces this risk by keeping a vetted subcontractor network and using scale—over 40,000 towers globally—to secure volume discounts and priority scheduling. This sourcing strategy helped SBA contain operating expense growth to about 3% in 2024.

Steel and Raw Material Costs

Steel and other raw materials drive tower build and reinforcement costs; steel accounted for ~15–20% of site development capex in 2024, so a 10% steel-price swing could change capex by ~1.5–2.0%.

Global commodity volatility—steel futures rose ~18% in 2024 vs 2023—raises expansion and capital-spend uncertainty for SBA Communications’ site development segment.

Multiple global suppliers dilute supplier power, but macro trends (China demand, tariffs, freight) set a baseline price SBA must absorb or hedge against.

Energy and Utility Providers

- Single-utility dependence raises electricity rate risk and bargaining power

- Backup generators and BESS deployed to improve uptime and control costs

- Renewable PPAs and on-site solar reduce long-term grid reliance

- Estimate: BESS can cut outage revenue losses 30–60% at high-risk sites

Regulatory and Zoning Authorities

Government entities act as suppliers by issuing mandatory permits and zoning approvals; denial or delay can halt tower builds and leases.

Their bargaining power is high due to strict local standards and environmental rules; in 2024 roughly 30% of U.S. tower projects faced permitting delays over 6 months, raising capex and timeline risk.

SBA spends heavily on government relations and compliance—legal and permitting costs can add 5–10% to project budgets—and must manage distinct rules across hundreds of jurisdictions.

- Permitting delays: ~30% projects >6 months (2024)

- Added cost: legal/permitting ~5–10% of project capex

- Risk: localized rules across hundreds of jurisdictions

Moderate supplier power: long leases cushion but steel, construction and permits hike costs

Suppliers (landowners, contractors, steel, utilities, regulators) exert moderate bargaining power: long-term leases (>70% >10 years) and SBA’s scale (40k+ towers) limit immediate landowner leverage, but 2024 steel +18% and 6% higher construction costs, single-utility risks, and ~30% projects facing >6-month permitting delays raise input cost and timing risk.

| Supplier | Key metric | 2024–25 impact |

|---|---|---|

| Land leases | >70% >10yr | Low short-term leverage |

| Construction | Costs +6% YoY | Higher capex |

| Steel | Futures +18% | Capex +1.5–2% |

| Permitting | 30% delays >6mo | Timelines +costs |

What is included in the product

Provides a concise Porter's Five Forces overview for SBA Communications, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, plus emerging disruptive risks to its tower infrastructure business.

Clear, one-sheet Porter's Five Forces for SBA Communications—instantly see competitive pressures and relieve decision fatigue with adjustable force levels tied to market data.

Customers Bargaining Power

High Tenant Concentration

The primary customers for SBA Communications are a few large U.S. carriers—T-Mobile, Verizon, and AT&T—which together accounted for roughly 70–80% of U.S. tower leasing revenue for tower companies in 2024, giving them strong leverage to negotiate nationwide master lease agreements on price and terms.

Those master leases set pricing across thousands of sites; for SBA, the top three tenants represented about 50–60% of rental revenue in 2024, concentrating bargaining power and compressing pricing flexibility.

The loss of one major carrier, or consolidation such as T-Mobile’s 2020 Sprint merger, can reduce site tenancy and long-term revenue visibility; a single large-tenant departure could cut several percentage points off annualized revenue and growth forecasts.

Fixed Long-Term Lease Structures

Wireless carriers sign typical SBA Communications leases of 5–10 years, giving SBA predictable cash flow—SBA reported 2024 consolidated net tower cash rent growth of 3.8%—but these terms limit quick price resets.

Leases often include fixed annual escalators (commonly 2–3%), shielding SBA from inflation but blocking capture of sudden demand-driven rate spikes seen in 2023 small-cell bidding.

Customers exploit long-term commitments to negotiate lower rates during tech shifts; in 2024 carrier renegotiations reportedly affected ~8% of site rents, increasing customer bargaining power.

Carrier Consolidation Risks

Carrier consolidation—like T‑Mobile/Sprint (2020) and Verizon’s smaller regional deals—lets merged providers cut redundant sites, terminate leases, or push lower rents; studies show post‑merger site reductions often reach 5–15% of overlapping towers. SBA must track M&A pipelines and tower tenancy metrics since losing even one anchor tenant can lower tower EBITDA by roughly 10–25% and raise net churn risk across its ~40,000 towers.

Network Architecture Shifts

- Small-cell growth ~18% (2024)

- SBA sites ~150,000 (2024)

- FFO/share growth ~4% (2024)

In-House Infrastructure Development

Large carriers could vertically integrate by building towers or neutral-host networks if leasing costs rise, capping SBA Communications' pricing power over top customers.

Still, tower build costs are high: a single macro site can cost $150k–$300k to deploy and carriers face multi-year payback, so leasing from SBA often remains the cheaper option.

- Vertical-integration threat limits pricing

- Macro site capex ~$150k–$300k (2025 estimates)

- Leasing often lower upfront cost, faster rollout

Carrier Concentration Spurs Pricing Pressure as Small‑Cell Growth and Capex Shape Risks

Customers (T‑Mobile, Verizon, AT&T) held concentrated leverage, accounting for ~50–60% of SBA rental revenue in 2024 and enabling nationwide master-lease pricing pressure; carrier consolidation and tech shifts (small-cell growth ~18% in 2024) increase churn and renegotiation risk (~8% of site rents renegotiated in 2024) while high macro-site build costs ($150k–$300k) limit but do not eliminate vertical-integration threats.

| Metric | 2024 / 2025 |

|---|---|

| Top-3 carrier share of revenue | 50–60% |

| Site count | ~150,000 |

| Small-cell growth | ~18% |

| Rents renegotiated | ~8% |

| Macro site capex | $150k–$300k |

Preview the Actual Deliverable

SBA Communications Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of SBA Communications you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is available for instant download and use upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SBA Communications faces powerful buyer and supplier dynamics, evolving threat from new entrants via towerless tech, and substitution pressures from small-cell solutions; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to SBA Communications’s market position.

Suppliers Bargaining Power

Ground Lease Landowner Leverage

SBA commonly holds long-term ground leases from private and public landowners for tower sites, exposing it to renewal rent increases; however, over 70% of U.S. towers sit on leases with remaining terms exceeding 10 years, limiting immediate landowner leverage. The specialized site location and estimated relocation costs of $200k–$1M per tower sharply constrain landowner bargaining power. SBA mitigates lease risk by negotiating extensions—SBA reported buying 1,200 sites through 2024—and selectively purchasing land to remove supplier exposure.

Specialized Construction and Labor

Building and maintaining towers requires specialized engineering and technical labor that tightens during major upgrade cycles; in 2024 U.S. tower construction costs rose about 6% year-over-year, reflecting labor scarcity. These providers can push SBA Communications (SBA) pricing for site development and maintenance during high demand, squeezing margins. SBA reduces this risk by keeping a vetted subcontractor network and using scale—over 40,000 towers globally—to secure volume discounts and priority scheduling. This sourcing strategy helped SBA contain operating expense growth to about 3% in 2024.

Steel and Raw Material Costs

Steel and other raw materials drive tower build and reinforcement costs; steel accounted for ~15–20% of site development capex in 2024, so a 10% steel-price swing could change capex by ~1.5–2.0%.

Global commodity volatility—steel futures rose ~18% in 2024 vs 2023—raises expansion and capital-spend uncertainty for SBA Communications’ site development segment.

Multiple global suppliers dilute supplier power, but macro trends (China demand, tariffs, freight) set a baseline price SBA must absorb or hedge against.

Energy and Utility Providers

- Single-utility dependence raises electricity rate risk and bargaining power

- Backup generators and BESS deployed to improve uptime and control costs

- Renewable PPAs and on-site solar reduce long-term grid reliance

- Estimate: BESS can cut outage revenue losses 30–60% at high-risk sites

Regulatory and Zoning Authorities

Government entities act as suppliers by issuing mandatory permits and zoning approvals; denial or delay can halt tower builds and leases.

Their bargaining power is high due to strict local standards and environmental rules; in 2024 roughly 30% of U.S. tower projects faced permitting delays over 6 months, raising capex and timeline risk.

SBA spends heavily on government relations and compliance—legal and permitting costs can add 5–10% to project budgets—and must manage distinct rules across hundreds of jurisdictions.

- Permitting delays: ~30% projects >6 months (2024)

- Added cost: legal/permitting ~5–10% of project capex

- Risk: localized rules across hundreds of jurisdictions

Moderate supplier power: long leases cushion but steel, construction and permits hike costs

Suppliers (landowners, contractors, steel, utilities, regulators) exert moderate bargaining power: long-term leases (>70% >10 years) and SBA’s scale (40k+ towers) limit immediate landowner leverage, but 2024 steel +18% and 6% higher construction costs, single-utility risks, and ~30% projects facing >6-month permitting delays raise input cost and timing risk.

| Supplier | Key metric | 2024–25 impact |

|---|---|---|

| Land leases | >70% >10yr | Low short-term leverage |

| Construction | Costs +6% YoY | Higher capex |

| Steel | Futures +18% | Capex +1.5–2% |

| Permitting | 30% delays >6mo | Timelines +costs |

What is included in the product

Provides a concise Porter's Five Forces overview for SBA Communications, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, plus emerging disruptive risks to its tower infrastructure business.

Clear, one-sheet Porter's Five Forces for SBA Communications—instantly see competitive pressures and relieve decision fatigue with adjustable force levels tied to market data.

Customers Bargaining Power

High Tenant Concentration

The primary customers for SBA Communications are a few large U.S. carriers—T-Mobile, Verizon, and AT&T—which together accounted for roughly 70–80% of U.S. tower leasing revenue for tower companies in 2024, giving them strong leverage to negotiate nationwide master lease agreements on price and terms.

Those master leases set pricing across thousands of sites; for SBA, the top three tenants represented about 50–60% of rental revenue in 2024, concentrating bargaining power and compressing pricing flexibility.

The loss of one major carrier, or consolidation such as T-Mobile’s 2020 Sprint merger, can reduce site tenancy and long-term revenue visibility; a single large-tenant departure could cut several percentage points off annualized revenue and growth forecasts.

Fixed Long-Term Lease Structures

Wireless carriers sign typical SBA Communications leases of 5–10 years, giving SBA predictable cash flow—SBA reported 2024 consolidated net tower cash rent growth of 3.8%—but these terms limit quick price resets.

Leases often include fixed annual escalators (commonly 2–3%), shielding SBA from inflation but blocking capture of sudden demand-driven rate spikes seen in 2023 small-cell bidding.

Customers exploit long-term commitments to negotiate lower rates during tech shifts; in 2024 carrier renegotiations reportedly affected ~8% of site rents, increasing customer bargaining power.

Carrier Consolidation Risks

Carrier consolidation—like T‑Mobile/Sprint (2020) and Verizon’s smaller regional deals—lets merged providers cut redundant sites, terminate leases, or push lower rents; studies show post‑merger site reductions often reach 5–15% of overlapping towers. SBA must track M&A pipelines and tower tenancy metrics since losing even one anchor tenant can lower tower EBITDA by roughly 10–25% and raise net churn risk across its ~40,000 towers.

Network Architecture Shifts

- Small-cell growth ~18% (2024)

- SBA sites ~150,000 (2024)

- FFO/share growth ~4% (2024)

In-House Infrastructure Development

Large carriers could vertically integrate by building towers or neutral-host networks if leasing costs rise, capping SBA Communications' pricing power over top customers.

Still, tower build costs are high: a single macro site can cost $150k–$300k to deploy and carriers face multi-year payback, so leasing from SBA often remains the cheaper option.

- Vertical-integration threat limits pricing

- Macro site capex ~$150k–$300k (2025 estimates)

- Leasing often lower upfront cost, faster rollout

Carrier Concentration Spurs Pricing Pressure as Small‑Cell Growth and Capex Shape Risks

Customers (T‑Mobile, Verizon, AT&T) held concentrated leverage, accounting for ~50–60% of SBA rental revenue in 2024 and enabling nationwide master-lease pricing pressure; carrier consolidation and tech shifts (small-cell growth ~18% in 2024) increase churn and renegotiation risk (~8% of site rents renegotiated in 2024) while high macro-site build costs ($150k–$300k) limit but do not eliminate vertical-integration threats.

| Metric | 2024 / 2025 |

|---|---|

| Top-3 carrier share of revenue | 50–60% |

| Site count | ~150,000 |

| Small-cell growth | ~18% |

| Rents renegotiated | ~8% |

| Macro site capex | $150k–$300k |

Preview the Actual Deliverable

SBA Communications Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of SBA Communications you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is available for instant download and use upon payment.