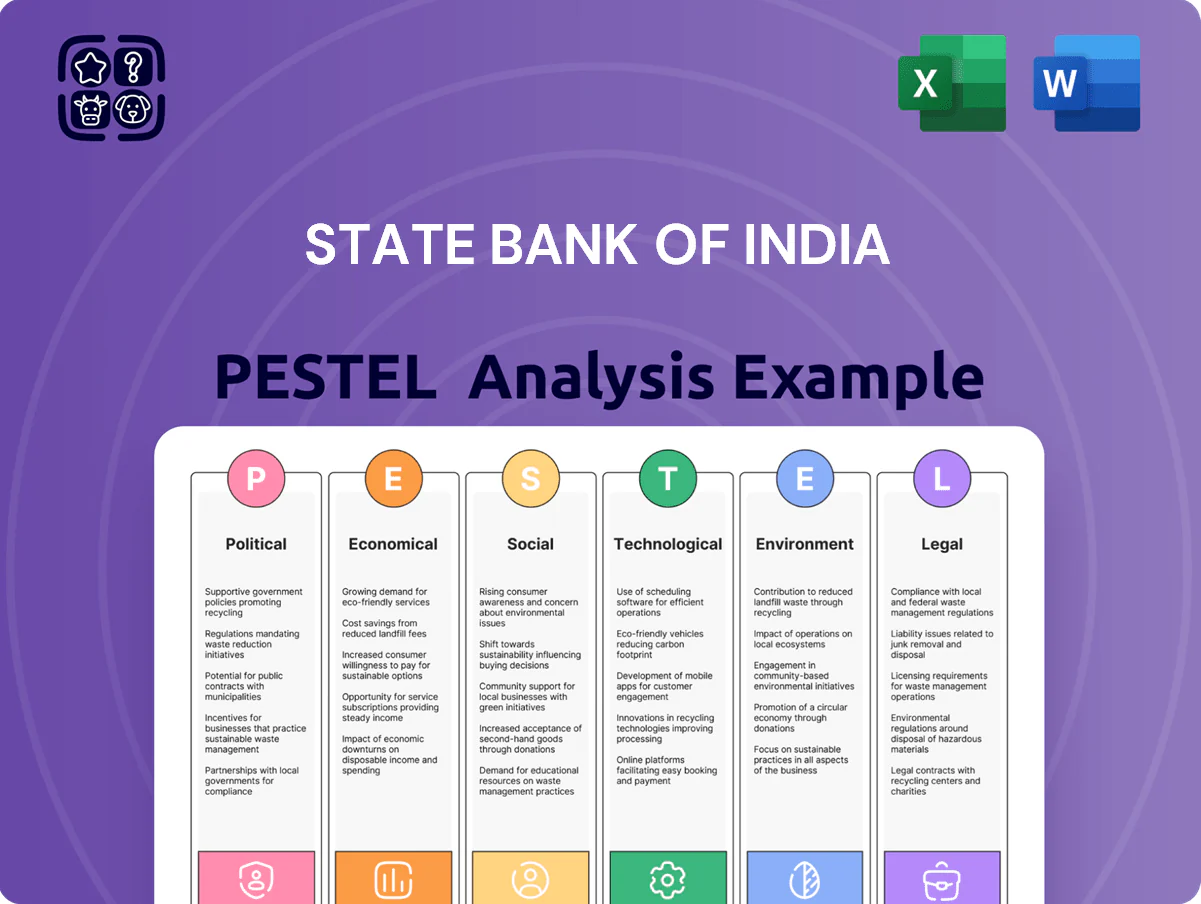

State Bank of India PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how regulatory shifts, macroeconomic trends, and fintech disruption are reshaping State Bank of India's strategy and risk profile; our concise PESTLE highlights immediate implications for growth, compliance, and digital transformation—buy the full analysis for a complete, actionable roadmap you can use in investment models and strategic plans.

Political factors

Government Ownership and Strategic Direction

As majority state-owned, SBI executes government social and economic agendas; in FY2024–25 SBI sanctioned ~INR 4.8 lakh crore to priority sectors supporting Atmanirbhar Bharat and MSME growth.

By late 2025, SBI aligns credit growth with national infrastructure plans, having allocated ~INR 1.2 lakh crore for road, rail and urban projects in 2024.

India’s political stability through 2024–25 has limited abrupt policy reversals, enabling SBI to pursue multi-year governance and capital plans with a CRAR of ~13.8% in FY2025.

Financial Inclusion Mandates

Geopolitical Influence on International Operations

SBI’s network across 30+ countries ties its international operations to India’s diplomatic stance and rising geopolitical tensions; in FY2024 SBI’s overseas business contributed about 6% of total net profit, exposing it to cross-border risk. Trade agreements and sanctions driven by alliances affect forex flows and trade finance—SBI’s overseas trade finance portfolio was ~INR 450 billion in 2024, vulnerable to policy shifts. In 2025 the bank must manage fragmented trade corridors while financing Indian exporters expanding abroad.

Public Sector Bank Privatization Discourse

The political debate on PSB privatization positions SBI as the national champion; privatization proposals surged in 2024-25 but SBI remains state-held, facing private banks that grew system loan share to ~46% in FY2024 while SBI's market share was 23.5%.

Government choices on capital infusion (₹30,000 crore deployed to PSBs in 2024) and dividend policy (SBI paid ₹10,000 crore in FY2024) materially impact SBI's CET1 and liquidity.

- SBI state-owned, market share 23.5% FY2024

- Private banks loan share ~46% FY2024

- ₹30,000 crore capital infusion to PSBs (2024)

- SBI dividend ~₹10,000 crore (FY2024)

Regulatory Influence of the Ministry of Finance

The Ministry of Finance, via the Financial Services Institutions Bureau, controls SBI's top appointments and strategic targets, directing board composition that can shift the bank's risk appetite and priority sectors for fiscal 2025-26.

Political appointees may steer allocations toward government priorities—credit to infrastructure, MSMEs, or social schemes—affecting SBI's loan mix and provisioning decisions as government borrowings hit 15.2 trillion INR in FY2024-25.

This alignment ensures SBI's objectives mirror the federal budget and fiscal policy, reinforcing coordinated credit flow for policy goals while constraining autonomous market-driven strategy shifts.

- Ministry controls appointments via FSIB

- Board makeup can change risk appetite for 2025-26

- Influences loan focus amid 15.2 trillion INR government borrowings (FY2024-25)

- Ensures sync with federal budget and fiscal policy

SBI dominates with 23.5% market share as state support, dividends and PSB infusion bolster growth

State control drives SBI’s policy lending and low-cost CASA deposits; FY2024 SBI market share 23.5%, private banks loan share ~46%, SBI CRAR ~13.8% (FY2025). Govt infused ₹30,000 crore to PSBs (2024); SBI dividend ₹10,000 crore (FY2024); government borrowings ₹15.2 trillion (FY2024‑25); overseas profit ~6% (FY2024); priority sector sanctions ~₹4.8 lakh crore (FY2024‑25).

| Metric | Value |

|---|---|

| SBI market share | 23.5% (FY2024) |

| Private banks loan share | 46% (FY2024) |

| CRAR | 13.8% (FY2025) |

| Govt PSB infusion | ₹30,000 crore (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the State Bank of India across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific examples, forward-looking insights for scenario planning, and clean formatting ready for reports, pitch decks, or strategic use by executives, consultants, and investors.

A concise PESTLE snapshot of State Bank of India that clearly segments political, economic, social, technological, legal, and environmental factors for quick reference in meetings and strategy sessions.

Economic factors

Interest Rate Volatility and Net Interest Margins

By end-2025, RBI policy remains a key profitability driver for State Bank of India; cumulative repo rate moves of +75 bps since 2022 lifted system repo to 6.50% by Dec‑2025, directly raising SBI’s cost of funds.

Repo volatility alters yields across SBI’s loan book—outstanding advances of ₹22.4 trillion (FY2024) see repricing risk that can compress NIMs if asset yields lag funding costs.

SBI must rebalance duration and CASA mix—CASA ratio at ~42% in FY2024 provides some buffer, but active liability management and loan repricing cadence are essential to protect NIMs amid inflation volatility.

India's GDP Growth Trajectory

As India remained one of the fastest-growing major economies in 2025 with IMF projecting 6.8% GDP growth and RBI estimating 7.0% for FY26, SBI's loan demand rose—corporate credit growth at 14.5% y/y and retail advances at 11.8% y/y in FY25 boosted net interest income and fee pools. Robust capex in infrastructure and private consumption supported SME and mortgage lending, improving CASA and loan origination. A slowdown would compress credit growth targets and raise GNPA risk, where SBI's GNPA stood at 3.6% in FY25, underlining sensitivity to GDP swings.

Asset Quality and Non-Performing Assets

The economic health of corporate India and retail demand drives SBI slippages and provisions; FY2024 saw SBI GNPA ratio at 2.02% and PCR at 74.7%, shaping provisioning needs.

By late 2025 SBI leverages upgraded AI-based credit monitoring and early-warning systems, helping keep NPAs near historical lows—GNPA targeted around 2% range.

Sectoral risks persist: MSME and agriculture stress could trigger localized spikes, with MSME exposure comprising around 14–16% of advances, posing contingent downside.

Inflationary Pressures on Operational Costs

Persistent inflation raises SBI’s operational costs, with employee wages and tech maintenance rising; India’s CPI was 6.5% in 2024 and wage revisions for banks typically add 5–8% annual staff cost pressure.

As India’s largest employer, SBI faces periodic wage revision liabilities (over 240,000 employees) and rising IT spend (SBI’s FY2023 IT expense ~INR 5,160 crore), impacting cost-to-income ratios.

- India CPI 2024: 6.5% — increases wage/IT costs

- Employees: ~240,000 — wage revision risk

- FY2023 IT spend: ~INR 5,160 crore — maintenance/upgrades

- Cost-to-income sensitivity: higher overheads compress margins

Capital Market Performance and Subsidiary Valuation

SBI's economic value is materially supported by subsidiaries: SBI Life (market cap ~INR 1.2 lakh crore in Jan 2025), SBI Mutual Fund (AUM ~INR 8.5 lakh crore FY2024-25) and SBI Cards (market cap ~INR 65,000 crore), which strengthen the bank's capital base through listed valuations.

Robust 2025 capital markets enable SBI to unlock value via stake sales or IPOs, improving Tier-1 ratios and providing liquidity buffers.

- Subsidiary market caps/AUM bolster CET1 and capital adequacy

SBI margins squeezed as repo rises to 6.5%—credit growth lifts NII, GNPA & opex risks

RBI rate path (system repo ~6.50% by Dec‑2025) raised SBI funding costs, pressuring NIMs despite CASA ~42% (FY2024); advances ₹22.4t expose repricing risk.

Strong GDP (IMF 6.8% 2025) lifted credit growth—corporate +14.5% and retail +11.8% y/y—boosting NII but GNPA sensitivity remains (GNPA ~3.6% FY25; PCR ~74.7%).

Wage/IT inflation (CPI 6.5% 2024; FY2023 IT spend ~INR 5,160cr; ~240,000 employees) raises opex, compressing cost-to-income; subsidiaries (SBI Life mcap ~INR 1.2L cr; AUM ~INR 8.5L cr) support capital.

| Metric | Value |

|---|---|

| System repo (Dec‑2025) | 6.50% |

| Advances (FY2024) | ₹22.4 trillion |

| CASA (FY2024) | ~42% |

| GNPA (FY25) | 3.6% |

| PCR | 74.7% |

| CPI (2024) | 6.5% |

| Employees | ~240,000 |

| SBI Life mcap (Jan‑2025) | ~INR 1.2 lakh crore |

Full Version Awaits

State Bank of India PESTLE Analysis

The preview shown here is the exact State Bank of India PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no placeholders or surprises. The content, layout, and structure visible here match the downloadable file you’ll get immediately after checkout. What you see is the finished document you’ll own upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how regulatory shifts, macroeconomic trends, and fintech disruption are reshaping State Bank of India's strategy and risk profile; our concise PESTLE highlights immediate implications for growth, compliance, and digital transformation—buy the full analysis for a complete, actionable roadmap you can use in investment models and strategic plans.

Political factors

Government Ownership and Strategic Direction

As majority state-owned, SBI executes government social and economic agendas; in FY2024–25 SBI sanctioned ~INR 4.8 lakh crore to priority sectors supporting Atmanirbhar Bharat and MSME growth.

By late 2025, SBI aligns credit growth with national infrastructure plans, having allocated ~INR 1.2 lakh crore for road, rail and urban projects in 2024.

India’s political stability through 2024–25 has limited abrupt policy reversals, enabling SBI to pursue multi-year governance and capital plans with a CRAR of ~13.8% in FY2025.

Financial Inclusion Mandates

Geopolitical Influence on International Operations

SBI’s network across 30+ countries ties its international operations to India’s diplomatic stance and rising geopolitical tensions; in FY2024 SBI’s overseas business contributed about 6% of total net profit, exposing it to cross-border risk. Trade agreements and sanctions driven by alliances affect forex flows and trade finance—SBI’s overseas trade finance portfolio was ~INR 450 billion in 2024, vulnerable to policy shifts. In 2025 the bank must manage fragmented trade corridors while financing Indian exporters expanding abroad.

Public Sector Bank Privatization Discourse

The political debate on PSB privatization positions SBI as the national champion; privatization proposals surged in 2024-25 but SBI remains state-held, facing private banks that grew system loan share to ~46% in FY2024 while SBI's market share was 23.5%.

Government choices on capital infusion (₹30,000 crore deployed to PSBs in 2024) and dividend policy (SBI paid ₹10,000 crore in FY2024) materially impact SBI's CET1 and liquidity.

- SBI state-owned, market share 23.5% FY2024

- Private banks loan share ~46% FY2024

- ₹30,000 crore capital infusion to PSBs (2024)

- SBI dividend ~₹10,000 crore (FY2024)

Regulatory Influence of the Ministry of Finance

The Ministry of Finance, via the Financial Services Institutions Bureau, controls SBI's top appointments and strategic targets, directing board composition that can shift the bank's risk appetite and priority sectors for fiscal 2025-26.

Political appointees may steer allocations toward government priorities—credit to infrastructure, MSMEs, or social schemes—affecting SBI's loan mix and provisioning decisions as government borrowings hit 15.2 trillion INR in FY2024-25.

This alignment ensures SBI's objectives mirror the federal budget and fiscal policy, reinforcing coordinated credit flow for policy goals while constraining autonomous market-driven strategy shifts.

- Ministry controls appointments via FSIB

- Board makeup can change risk appetite for 2025-26

- Influences loan focus amid 15.2 trillion INR government borrowings (FY2024-25)

- Ensures sync with federal budget and fiscal policy

SBI dominates with 23.5% market share as state support, dividends and PSB infusion bolster growth

State control drives SBI’s policy lending and low-cost CASA deposits; FY2024 SBI market share 23.5%, private banks loan share ~46%, SBI CRAR ~13.8% (FY2025). Govt infused ₹30,000 crore to PSBs (2024); SBI dividend ₹10,000 crore (FY2024); government borrowings ₹15.2 trillion (FY2024‑25); overseas profit ~6% (FY2024); priority sector sanctions ~₹4.8 lakh crore (FY2024‑25).

| Metric | Value |

|---|---|

| SBI market share | 23.5% (FY2024) |

| Private banks loan share | 46% (FY2024) |

| CRAR | 13.8% (FY2025) |

| Govt PSB infusion | ₹30,000 crore (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the State Bank of India across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific examples, forward-looking insights for scenario planning, and clean formatting ready for reports, pitch decks, or strategic use by executives, consultants, and investors.

A concise PESTLE snapshot of State Bank of India that clearly segments political, economic, social, technological, legal, and environmental factors for quick reference in meetings and strategy sessions.

Economic factors

Interest Rate Volatility and Net Interest Margins

By end-2025, RBI policy remains a key profitability driver for State Bank of India; cumulative repo rate moves of +75 bps since 2022 lifted system repo to 6.50% by Dec‑2025, directly raising SBI’s cost of funds.

Repo volatility alters yields across SBI’s loan book—outstanding advances of ₹22.4 trillion (FY2024) see repricing risk that can compress NIMs if asset yields lag funding costs.

SBI must rebalance duration and CASA mix—CASA ratio at ~42% in FY2024 provides some buffer, but active liability management and loan repricing cadence are essential to protect NIMs amid inflation volatility.

India's GDP Growth Trajectory

As India remained one of the fastest-growing major economies in 2025 with IMF projecting 6.8% GDP growth and RBI estimating 7.0% for FY26, SBI's loan demand rose—corporate credit growth at 14.5% y/y and retail advances at 11.8% y/y in FY25 boosted net interest income and fee pools. Robust capex in infrastructure and private consumption supported SME and mortgage lending, improving CASA and loan origination. A slowdown would compress credit growth targets and raise GNPA risk, where SBI's GNPA stood at 3.6% in FY25, underlining sensitivity to GDP swings.

Asset Quality and Non-Performing Assets

The economic health of corporate India and retail demand drives SBI slippages and provisions; FY2024 saw SBI GNPA ratio at 2.02% and PCR at 74.7%, shaping provisioning needs.

By late 2025 SBI leverages upgraded AI-based credit monitoring and early-warning systems, helping keep NPAs near historical lows—GNPA targeted around 2% range.

Sectoral risks persist: MSME and agriculture stress could trigger localized spikes, with MSME exposure comprising around 14–16% of advances, posing contingent downside.

Inflationary Pressures on Operational Costs

Persistent inflation raises SBI’s operational costs, with employee wages and tech maintenance rising; India’s CPI was 6.5% in 2024 and wage revisions for banks typically add 5–8% annual staff cost pressure.

As India’s largest employer, SBI faces periodic wage revision liabilities (over 240,000 employees) and rising IT spend (SBI’s FY2023 IT expense ~INR 5,160 crore), impacting cost-to-income ratios.

- India CPI 2024: 6.5% — increases wage/IT costs

- Employees: ~240,000 — wage revision risk

- FY2023 IT spend: ~INR 5,160 crore — maintenance/upgrades

- Cost-to-income sensitivity: higher overheads compress margins

Capital Market Performance and Subsidiary Valuation

SBI's economic value is materially supported by subsidiaries: SBI Life (market cap ~INR 1.2 lakh crore in Jan 2025), SBI Mutual Fund (AUM ~INR 8.5 lakh crore FY2024-25) and SBI Cards (market cap ~INR 65,000 crore), which strengthen the bank's capital base through listed valuations.

Robust 2025 capital markets enable SBI to unlock value via stake sales or IPOs, improving Tier-1 ratios and providing liquidity buffers.

- Subsidiary market caps/AUM bolster CET1 and capital adequacy

SBI margins squeezed as repo rises to 6.5%—credit growth lifts NII, GNPA & opex risks

RBI rate path (system repo ~6.50% by Dec‑2025) raised SBI funding costs, pressuring NIMs despite CASA ~42% (FY2024); advances ₹22.4t expose repricing risk.

Strong GDP (IMF 6.8% 2025) lifted credit growth—corporate +14.5% and retail +11.8% y/y—boosting NII but GNPA sensitivity remains (GNPA ~3.6% FY25; PCR ~74.7%).

Wage/IT inflation (CPI 6.5% 2024; FY2023 IT spend ~INR 5,160cr; ~240,000 employees) raises opex, compressing cost-to-income; subsidiaries (SBI Life mcap ~INR 1.2L cr; AUM ~INR 8.5L cr) support capital.

| Metric | Value |

|---|---|

| System repo (Dec‑2025) | 6.50% |

| Advances (FY2024) | ₹22.4 trillion |

| CASA (FY2024) | ~42% |

| GNPA (FY25) | 3.6% |

| PCR | 74.7% |

| CPI (2024) | 6.5% |

| Employees | ~240,000 |

| SBI Life mcap (Jan‑2025) | ~INR 1.2 lakh crore |

Full Version Awaits

State Bank of India PESTLE Analysis

The preview shown here is the exact State Bank of India PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no placeholders or surprises. The content, layout, and structure visible here match the downloadable file you’ll get immediately after checkout. What you see is the finished document you’ll own upon payment.