Scentre Group Business Model Canvas

Inside Scentre Group: A compact Business Model Canvas to monetize prime retail footfall

Unlock the full strategic blueprint behind Scentre Group’s business model—this in-depth Business Model Canvas reveals how the company creates value, optimises its retail ecosystem, and monetises footfall across prime Australian and New Zealand assets; ideal for investors, strategists, and consultants seeking actionable, company-specific insight. Download the complete Word & Excel canvas to benchmark, plan, or present with confidence.

Partnerships

Retail and Luxury Brands

Scentre Group secures long-term leases with global and local retail giants—about 92% occupancy across 2024 Westfield assets—ensuring premium brand mix that drives footfall and retail sales (group retail sales NZ$12.3bn in FY2024).

By 2025 partnerships shifted toward experiential and flagship stores, with ~18% of new lettable area allocated to experience-led formats and multi-year co-investment on storefront fit-outs.

Joint Venture Capital Partners

Scentre Group routinely forms co-ownership joint ventures with institutional investors and pension funds—having 2024 joint-venture assets under management of about A$23.6 billion—spreading development risk and securing capital for large projects like Westfield Plenty Valley. These partnerships let Scentre manage high-value retail assets while keeping net debt lower (net debt A$4.2bn at 30 Jun 2024), a vital tactic for funding capital-intensive premium real estate.

Government and Urban Planners

Collaboration with local councils and state governments secures zoning, planning permits and integration of Westfield centres into transport hubs; in 2024 Scentre Group reported A$1.2bn of capex commitments partly earmarked for transport-linked redevelopments. As of late 2025 these partnerships prioritise sustainable urban development and community infrastructure—aligning with targets to cut Scope 1–2 emissions 50% by 2030—keeping centres central to Australian and NZ metropolitan planning.

Technology and Digital Service Providers

Strategic alliances with tech firms enable Scentre Group to integrate smart building systems and the Westfield Direct marketplace, cutting energy use up to 20% in pilots and boosting click‑to‑collect sales 35% in 2024.

These partners link physical retail and e‑commerce via advanced logistics and analytics, reducing store stockouts by 18% and improving dwell‑time personalization; the tech layer raises NPS and lowers ops costs.

- Energy cut: ~20% in smart building pilots (2023–24)

- Click‑to‑collect growth: +35% (2024)

- Stockouts reduced: ~18%

- Higher NPS and lower operating costs

Entertainment and Hospitality Operators

Partnerships with major cinema chains (e.g., Event Cinemas), high-end restaurateurs, and leisure providers have turned Scentre Group malls into mixed-use destinations, lifting non-retail visitation; in 2024 precincts with curated F&B and entertainment saw 12–18% higher evening foot traffic and 8–11% longer dwell times versus retail-only centers.

- Evening foot traffic +12–18% (2024 data)

- Dwell time +8–11%

- 2025 focus: destination dining + immersive entertainment

- Leads to higher F&B NOI and leasing premiums

Scentre Group: 92% occupancy, A$23.6bn JV AUM, experience-led growth & efficiency

Scentre Group’s key partnerships drive 92% occupancy (2024), A$23.6bn JV AUM (2024), net debt A$4.2bn (30 Jun 2024), A$1.2bn capex commitments (2024) and +35% click‑to‑collect growth (2024), enabling experience-led space (≈18% new area) and ~20% energy cuts in pilots.

| Metric | Value |

|---|---|

| Occupancy | 92% (2024) |

| JV AUM | A$23.6bn (2024) |

| Net debt | A$4.2bn (30 Jun 2024) |

| Capex commitments | A$1.2bn (2024) |

| Experience area | ≈18% new lettable area (2025) |

| Click‑to‑collect | +35% (2024) |

| Energy cut pilots | ~20% (2023–24) |

What is included in the product

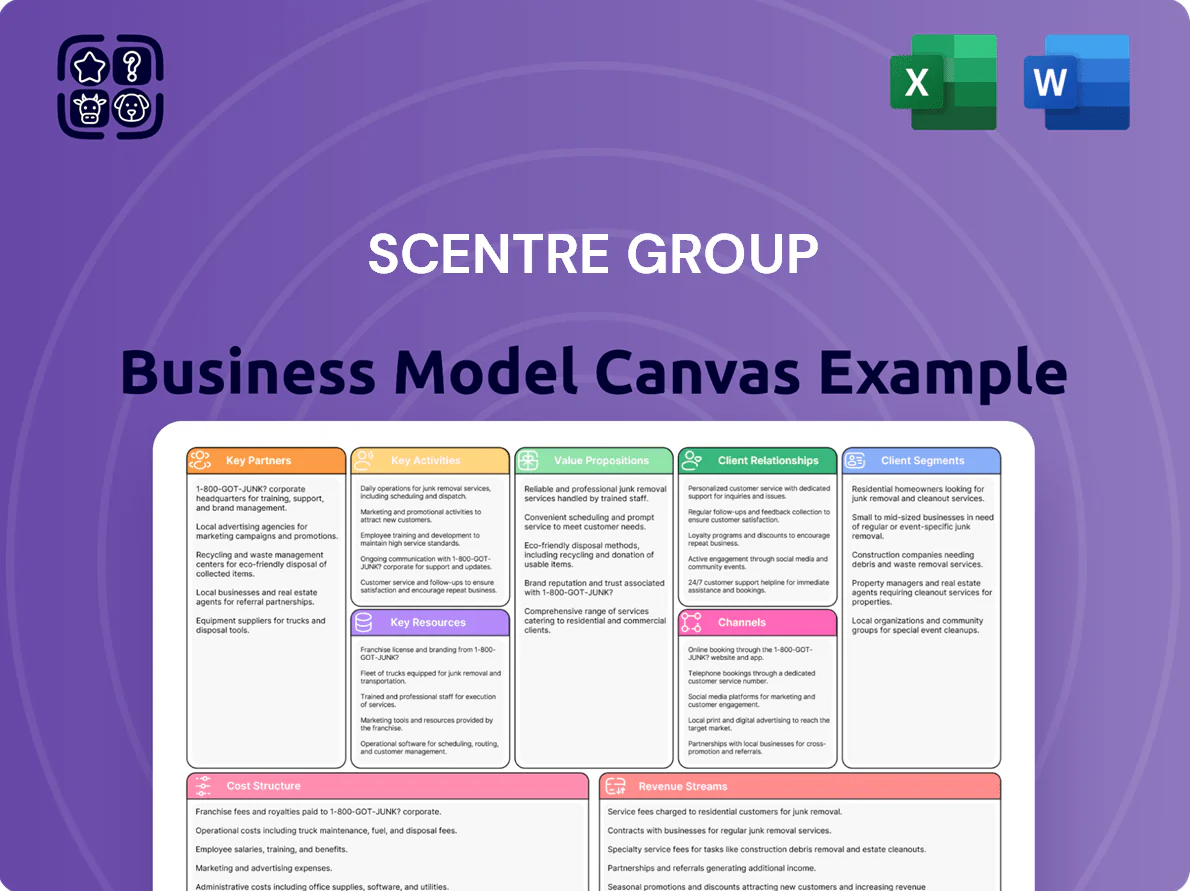

A concise, investor-ready Business Model Canvas for Scentre Group detailing nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with real-world retail property management and development operations, competitive advantages, SWOT-linked insights, and polished for presentations or strategic decision-making.

High-level view of Scentre Group’s retail property model with editable cells, enabling quick identification of value drivers and tenant mix strategies.

Activities

Property Management and Operations

The team runs daily maintenance, cleaning and security across 42 Westfield centres in Australia and New Zealand, servicing ~6,000 retail tenancies and 500m+ annual visits (2024), while managing HVAC, lighting and utilities that cost ~A$420m/year; efficient ops keep net operating income and the Westfield premium experience stable.

Strategic Asset Development

Scentre Group continuously redevelops and expands its Westfield malls—spending A$1.2bn on capital projects in FY2024—to boost land value and modern utility through architectural design, construction management and repurposing underutilised space into residential or office assets. These strategic developments lifted portfolio NOI (net operating income) growth to 3.5% in 2024, helping malls compete with digital retail by increasing mixed-use footfall and rental yield.

Leasing and Tenant Curation

Actively curating tenant mix ensures each Scentre Group shopping centre matches local demographics, using continuous market research, lease negotiations, and onboarding of emerging brands; in FY2024 Scentre reported portfolio occupancy of ~99.5% and 1.2% like-for-like rent growth, showing high-performing tenancy drives steady income.

Marketing and Community Engagement

The group runs large-scale marketing campaigns and community events—seasonal festivals, celebrity appearances, and Westfield Plus loyalty pushes—to boost footfall and dwell time; Westfield reported 8% YoY app engagement growth and c. A$120m loyalty-driven retail sales in FY2024.

- Seasonal festivals driving weekend footfall spikes (+12% per event)

- Celebrity appearances for PR reach and rent uplift

- Westfield Plus: 8% YoY engagement, A$120m sales FY2024

Digital Integration and Data Analytics

By 2025 Scentre Group has refined Westfield Direct, driving a 28% increase in online-to-store conversions and using anonymized consumer-behaviour data to deliver personalized marketing that lifts tenant sales per sqm by ~12% year-over-year.

Data-driven forecasting—now a core competency—reduced vacancy-risk forecasting error to ±3% and informs leasing and merchandising, improving centre NOI (net operating income) resilience during demand shifts.

- Westfield Direct: +28% online-to-store conversion

- Tenant sales per sqm: +12% YoY from personalization

- Vacancy forecasting error: ±3%

- Outcome: stronger NOI resilience

Westfield: 42 centres, 500M+ visits, A$1.2bn CapEx, 99.5% occupancy, NOI +3.5%

Scentre runs ops across 42 Westfield centres (AU/NZ), servicing ~6,000 tenancies and 500m+ visits (2024), managing A$420m utilities; spends A$1.2bn CapEx in FY2024, yielding 3.5% NOI growth and 99.5% occupancy; Westfield Direct +28% online-to-store, personalization +12% sales/sqm; vacancy forecast error ±3%.

| Metric | 2024/25 |

|---|---|

| Centres | 42 |

| Tenancies | ~6,000 |

| Visits | 500m+ |

| Utilities cost | A$420m/yr |

| CapEx | A$1.2bn FY2024 |

| NOI growth | 3.5% |

| Occupancy | 99.5% |

| Online→Store | +28% |

| Sales/sqm | +12% YoY |

| Vacancy error | ±3% |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the exact Scentre Group Business Model Canvas you’ll receive after purchase—no mockups or samples. Upon completing your order, you’ll instantly get the full, editable file formatted precisely as shown, ready for presentation or analysis. This preview reflects the real deliverable with all core sections included, ensuring transparency and no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Inside Scentre Group: A compact Business Model Canvas to monetize prime retail footfall

Unlock the full strategic blueprint behind Scentre Group’s business model—this in-depth Business Model Canvas reveals how the company creates value, optimises its retail ecosystem, and monetises footfall across prime Australian and New Zealand assets; ideal for investors, strategists, and consultants seeking actionable, company-specific insight. Download the complete Word & Excel canvas to benchmark, plan, or present with confidence.

Partnerships

Retail and Luxury Brands

Scentre Group secures long-term leases with global and local retail giants—about 92% occupancy across 2024 Westfield assets—ensuring premium brand mix that drives footfall and retail sales (group retail sales NZ$12.3bn in FY2024).

By 2025 partnerships shifted toward experiential and flagship stores, with ~18% of new lettable area allocated to experience-led formats and multi-year co-investment on storefront fit-outs.

Joint Venture Capital Partners

Scentre Group routinely forms co-ownership joint ventures with institutional investors and pension funds—having 2024 joint-venture assets under management of about A$23.6 billion—spreading development risk and securing capital for large projects like Westfield Plenty Valley. These partnerships let Scentre manage high-value retail assets while keeping net debt lower (net debt A$4.2bn at 30 Jun 2024), a vital tactic for funding capital-intensive premium real estate.

Government and Urban Planners

Collaboration with local councils and state governments secures zoning, planning permits and integration of Westfield centres into transport hubs; in 2024 Scentre Group reported A$1.2bn of capex commitments partly earmarked for transport-linked redevelopments. As of late 2025 these partnerships prioritise sustainable urban development and community infrastructure—aligning with targets to cut Scope 1–2 emissions 50% by 2030—keeping centres central to Australian and NZ metropolitan planning.

Technology and Digital Service Providers

Strategic alliances with tech firms enable Scentre Group to integrate smart building systems and the Westfield Direct marketplace, cutting energy use up to 20% in pilots and boosting click‑to‑collect sales 35% in 2024.

These partners link physical retail and e‑commerce via advanced logistics and analytics, reducing store stockouts by 18% and improving dwell‑time personalization; the tech layer raises NPS and lowers ops costs.

- Energy cut: ~20% in smart building pilots (2023–24)

- Click‑to‑collect growth: +35% (2024)

- Stockouts reduced: ~18%

- Higher NPS and lower operating costs

Entertainment and Hospitality Operators

Partnerships with major cinema chains (e.g., Event Cinemas), high-end restaurateurs, and leisure providers have turned Scentre Group malls into mixed-use destinations, lifting non-retail visitation; in 2024 precincts with curated F&B and entertainment saw 12–18% higher evening foot traffic and 8–11% longer dwell times versus retail-only centers.

- Evening foot traffic +12–18% (2024 data)

- Dwell time +8–11%

- 2025 focus: destination dining + immersive entertainment

- Leads to higher F&B NOI and leasing premiums

Scentre Group: 92% occupancy, A$23.6bn JV AUM, experience-led growth & efficiency

Scentre Group’s key partnerships drive 92% occupancy (2024), A$23.6bn JV AUM (2024), net debt A$4.2bn (30 Jun 2024), A$1.2bn capex commitments (2024) and +35% click‑to‑collect growth (2024), enabling experience-led space (≈18% new area) and ~20% energy cuts in pilots.

| Metric | Value |

|---|---|

| Occupancy | 92% (2024) |

| JV AUM | A$23.6bn (2024) |

| Net debt | A$4.2bn (30 Jun 2024) |

| Capex commitments | A$1.2bn (2024) |

| Experience area | ≈18% new lettable area (2025) |

| Click‑to‑collect | +35% (2024) |

| Energy cut pilots | ~20% (2023–24) |

What is included in the product

A concise, investor-ready Business Model Canvas for Scentre Group detailing nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with real-world retail property management and development operations, competitive advantages, SWOT-linked insights, and polished for presentations or strategic decision-making.

High-level view of Scentre Group’s retail property model with editable cells, enabling quick identification of value drivers and tenant mix strategies.

Activities

Property Management and Operations

The team runs daily maintenance, cleaning and security across 42 Westfield centres in Australia and New Zealand, servicing ~6,000 retail tenancies and 500m+ annual visits (2024), while managing HVAC, lighting and utilities that cost ~A$420m/year; efficient ops keep net operating income and the Westfield premium experience stable.

Strategic Asset Development

Scentre Group continuously redevelops and expands its Westfield malls—spending A$1.2bn on capital projects in FY2024—to boost land value and modern utility through architectural design, construction management and repurposing underutilised space into residential or office assets. These strategic developments lifted portfolio NOI (net operating income) growth to 3.5% in 2024, helping malls compete with digital retail by increasing mixed-use footfall and rental yield.

Leasing and Tenant Curation

Actively curating tenant mix ensures each Scentre Group shopping centre matches local demographics, using continuous market research, lease negotiations, and onboarding of emerging brands; in FY2024 Scentre reported portfolio occupancy of ~99.5% and 1.2% like-for-like rent growth, showing high-performing tenancy drives steady income.

Marketing and Community Engagement

The group runs large-scale marketing campaigns and community events—seasonal festivals, celebrity appearances, and Westfield Plus loyalty pushes—to boost footfall and dwell time; Westfield reported 8% YoY app engagement growth and c. A$120m loyalty-driven retail sales in FY2024.

- Seasonal festivals driving weekend footfall spikes (+12% per event)

- Celebrity appearances for PR reach and rent uplift

- Westfield Plus: 8% YoY engagement, A$120m sales FY2024

Digital Integration and Data Analytics

By 2025 Scentre Group has refined Westfield Direct, driving a 28% increase in online-to-store conversions and using anonymized consumer-behaviour data to deliver personalized marketing that lifts tenant sales per sqm by ~12% year-over-year.

Data-driven forecasting—now a core competency—reduced vacancy-risk forecasting error to ±3% and informs leasing and merchandising, improving centre NOI (net operating income) resilience during demand shifts.

- Westfield Direct: +28% online-to-store conversion

- Tenant sales per sqm: +12% YoY from personalization

- Vacancy forecasting error: ±3%

- Outcome: stronger NOI resilience

Westfield: 42 centres, 500M+ visits, A$1.2bn CapEx, 99.5% occupancy, NOI +3.5%

Scentre runs ops across 42 Westfield centres (AU/NZ), servicing ~6,000 tenancies and 500m+ visits (2024), managing A$420m utilities; spends A$1.2bn CapEx in FY2024, yielding 3.5% NOI growth and 99.5% occupancy; Westfield Direct +28% online-to-store, personalization +12% sales/sqm; vacancy forecast error ±3%.

| Metric | 2024/25 |

|---|---|

| Centres | 42 |

| Tenancies | ~6,000 |

| Visits | 500m+ |

| Utilities cost | A$420m/yr |

| CapEx | A$1.2bn FY2024 |

| NOI growth | 3.5% |

| Occupancy | 99.5% |

| Online→Store | +28% |

| Sales/sqm | +12% YoY |

| Vacancy error | ±3% |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the exact Scentre Group Business Model Canvas you’ll receive after purchase—no mockups or samples. Upon completing your order, you’ll instantly get the full, editable file formatted precisely as shown, ready for presentation or analysis. This preview reflects the real deliverable with all core sections included, ensuring transparency and no surprises.