Scentre Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

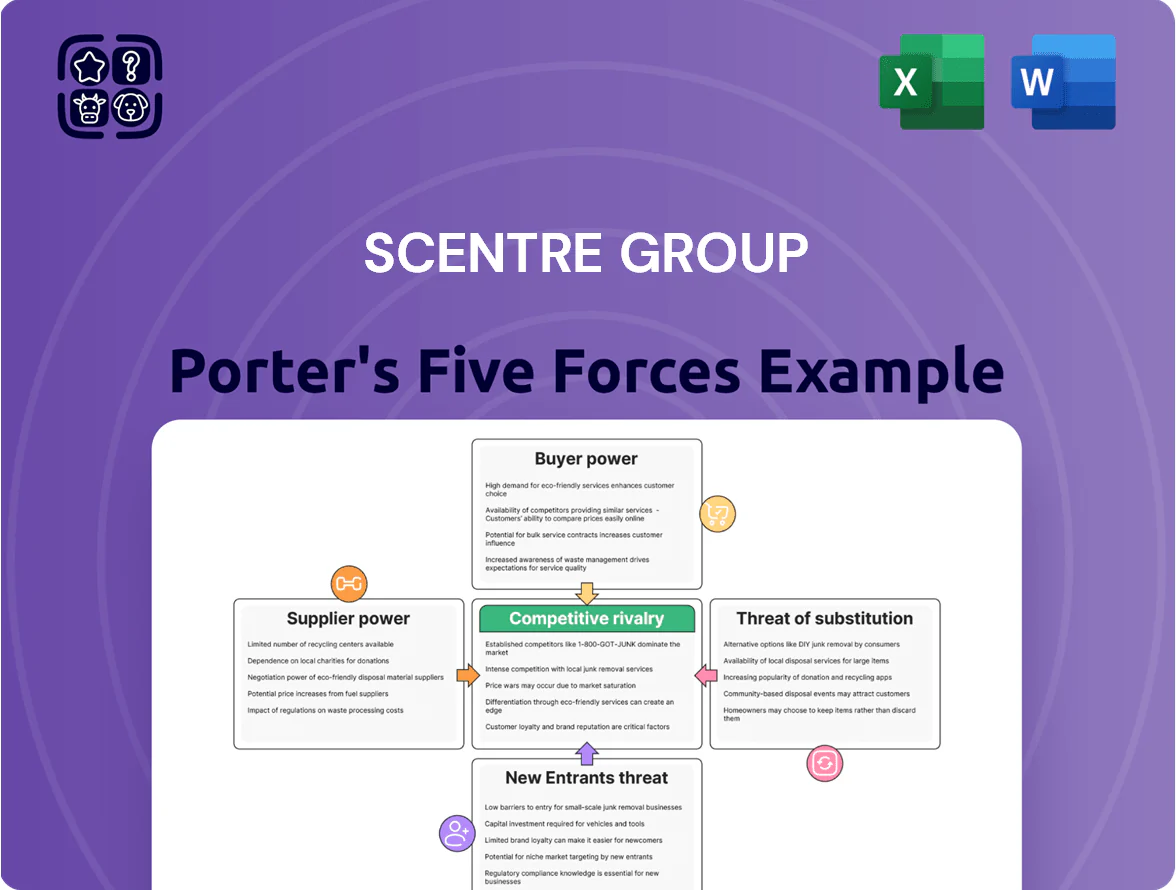

Scentre Group operates in a mature retail property sector where bargaining power of large tenants and evolving e-commerce trends intensify competitive pressures, while high entry barriers and substantial capital requirements limit new entrants.

Supplier influence is moderate given specialized construction and services, and substitutes like online retail pose a growing threat to footfall and leasing dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scentre Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Tier-One Construction Firms

Scentre Group depends on a small set of Tier‑One contractors for multi‑billion dollar Westfield redevelopments, giving suppliers leverage despite Scentre’s high volume spend; large projects often exceed AUD 500–800m each. Specialized retail infrastructure and Australia’s chronic skilled‑trade deficit—ABS reported a 2024 construction vacancy rate near 6%—keeps supplier power moderate as firms compete for priority on timelines into late 2025.

Energy and Utility Provider Influence

Scentre Group, operating 42 Westfield shopping centres in Australia and New Zealand, is highly sensitive to energy pricing; electricity made up about 2.8% of FY2024 operating expenses, so supplier rates materially affect margins.

Australian renewable mandates and grid upgrades force reliance on specific green suppliers and network capacity, increasing bargaining power for those providers.

Scentre mitigates supplier power via long-term power purchase agreements covering ~40% of consumption and $120m+ invested in onsite solar to cap future price exposure.

Financial Capital and Debt Markets

The supply of capital from institutional investors and banks is a critical input for Scentre Group; in 2025 Australian office and retail real estate spreads widened as the RBA cash rate sat at 4.35% (Jan 2025), lifting average A-REIT borrowing costs by ~120 bps year-on-year. Debt providers thus control expansion capacity: tighter credit availability since 2024 raised secured loan pricing and reduced leverage headroom. Maintaining an investment-grade credit rating (Scentre held BBB+ by S&P in 2024) is vital to secure lower coupons and longer maturities. Any global liquidity tightening directly raises Scentre’s cost of capital, increasing funding costs for development and acquisitions.

Technology and Digital Service Providers

Scentre Group increasingly depends on specialized tech vendors for Westfield Direct and smart building systems, which deliver analytics and engagement tools that drove a 12% YoY lift in digital sales channels in FY2024.

These providers control proprietary platforms and APIs that are costly to replace; industry swap costs can exceed 6–9 months of lost operations and CAPEX of A$20–50m for enterprise integrations, giving vendors rising fee leverage.

- 12% YoY digital sales lift (FY2024)

- Switch costs: 6–9 months downtime

- Integration CAPEX estimate: A$20–50m

- Suppliers set fees, API standards

Government and Regulatory Bodies as Land Suppliers

Government bodies act as de facto land suppliers for Scentre Group by controlling zoning and development approvals; in 2024 Scentre sought 12 major planning permits across NSW and Victoria, with average approval timelines of 9–15 months that delay redevelopment cash flows.

This regulatory bottleneck limits available floor-space growth, making Scentre reliant on local and state policy—giving authorities leverage over project timing, costs, and feasibility and raising capex risk for the group.

- 12 major permits sought in 2024

- 9–15 months average approval time

- Regulatory delays raise capex timing risk

- Authorities control redevelopment feasibility

Suppliers wield leverage: AUD500–800m redevelopments, 40% PPA, BBB+ impacts finance

Suppliers hold moderate-to-high power: few Tier‑One contractors for AUD 500–800m redevelopments, 6% construction vacancy (ABS 2024), electricity ~2.8% of FY2024 opex, ~40% PPA coverage, $120m+ onsite solar, BBB+ rating (S&P 2024) affects borrowing costs; tech vendors drove 12% digital sales lift (FY2024) and entail A$20–50m swap CAPEX.

| Metric | Value |

|---|---|

| Redev. size | AUD 500–800m |

| Construction vacancy | 6% (2024) |

| Electricity opex | 2.8% (FY2024) |

| PPA cover | ~40% |

| Onsite solar | $120m+ |

| Credit rating | BBB+ (S&P 2024) |

| Digital sales lift | 12% YoY (FY2024) |

| Swap CAPEX | A$20–50m |

What is included in the product

Tailored exclusively for Scentre Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers protecting incumbents, and substitutes or disruptive threats shaping mall portfolio profitability.

A concise, one-sheet Porter's Five Forces summary for Scentre Group—quickly spot competitive pressures and real estate risks to inform leasing, development and portfolio decisions.

Customers Bargaining Power

Leverage of Major Anchor Tenants

Large anchors like Myer, David Jones and Woolworths/Coles drive 60–70% of weekly mall footfall in Scentre Group centres (Scentre FY2024), giving them strong leverage.

Because anchors are traffic-critical, they secure lower rent-to-sales ratios (often 5–8% vs 12–15% for specialty retailers), longer lease terms, and significant fit-out and turnover rent concessions.

Specialty Retailer Fragmentation

Specialty retailers in Westfield centres hold low individual bargaining power versus anchor tenants; Scentre Group’s curated footfall—Westfield attracted ~330 million visits in 2024—keeps demand for premium space high, letting Scentre push smaller-boutique rents upward.

Low Switching Costs for Global Brands

International luxury and fast-fashion brands have low switching costs and can relocate flagship stores; LVMH, Inditex, and H&M Group routinely rebalance store footprints across markets. If Scentre Group (Westfield) loses prestige or footfall, high-value tenants can move to rivals like Vicinity Centres or GPT, threatening rental income—top-tier tenants often pay 30–50% above mall averages. This mobility forces Scentre to reinvest: Westfield upgrades cost ~A$50–150 million per major mall refurbishment to protect rental yields and shopper traffic.

Consumer Influence on Tenant Health

Shoppers drive tenants’ sales and thus Scentre Group’s rent collectability; Australian retail sales rose 2.1% year-on-year to Nov 2025, but spending shifted 15% toward experiences per Roy Morgan’s 2025 leisure report, weakening landlords that keep product-heavy mixes.

Scentre must reweight leases toward dining, leisure and services—these categories saw 8–12% higher footfall in 2024–25—otherwise declining shopper interest cuts landlord bargaining power at renewals and forces rent incentives.

- Shoppers = ultimate payers; sales up 2.1% (Nov 2025)

- Experience spend +15% (Roy Morgan 2025)

- Dining/leisure footfall +8–12% (2024–25)

- Tenant mix shift needed to keep lease leverage

Impact of Short-Term Lease Flexibility

The shift to short-term leases and pop-ups lets retailers exit poor sites quickly; industry data shows pop-up tenancy rose ~18% in Australian malls in 2024, raising tenant bargaining power and churn risk for Scentre Group (ASX: SCG).

Retailers now demand flexible terms to hedge economic swings, forcing Scentre to adopt collaborative, performance-linked leases to sustain occupancy.

- Pop-up growth ~18% (2024)

- Higher churn risk

- More performance-linked leases

Anchors Drive 60–70% Footfall as Experience Spend Jumps 15%—Westfield 330M Visits

Large anchors (Myer, David Jones, Woolworths/Coles) drive 60–70% of mall footfall (Scentre FY2024), giving them strong rent leverage; specialty retailers face higher rents and lower bargaining power as Westfield attracted ~330m visits in 2024. Experience spend rose 15% (Roy Morgan 2025) and dining/leisure footfall +8–12% (2024–25), forcing Scentre to shift mixes and offer flexible, performance-linked leases; pop-ups grew ~18% (2024), raising churn risk.

| Metric | Value |

|---|---|

| Anchor share of footfall | 60–70% |

| Westfield visits (2024) | ~330m |

| Experience spend change (2025) | +15% |

| Dining/leisure footfall (2024–25) | +8–12% |

| Pop-up growth (2024) | ~18% |

Same Document Delivered

Scentre Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Scentre Group you’ll receive after purchase—no placeholders, no mockups, just the final, professionally formatted document ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Scentre Group operates in a mature retail property sector where bargaining power of large tenants and evolving e-commerce trends intensify competitive pressures, while high entry barriers and substantial capital requirements limit new entrants.

Supplier influence is moderate given specialized construction and services, and substitutes like online retail pose a growing threat to footfall and leasing dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scentre Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Tier-One Construction Firms

Scentre Group depends on a small set of Tier‑One contractors for multi‑billion dollar Westfield redevelopments, giving suppliers leverage despite Scentre’s high volume spend; large projects often exceed AUD 500–800m each. Specialized retail infrastructure and Australia’s chronic skilled‑trade deficit—ABS reported a 2024 construction vacancy rate near 6%—keeps supplier power moderate as firms compete for priority on timelines into late 2025.

Energy and Utility Provider Influence

Scentre Group, operating 42 Westfield shopping centres in Australia and New Zealand, is highly sensitive to energy pricing; electricity made up about 2.8% of FY2024 operating expenses, so supplier rates materially affect margins.

Australian renewable mandates and grid upgrades force reliance on specific green suppliers and network capacity, increasing bargaining power for those providers.

Scentre mitigates supplier power via long-term power purchase agreements covering ~40% of consumption and $120m+ invested in onsite solar to cap future price exposure.

Financial Capital and Debt Markets

The supply of capital from institutional investors and banks is a critical input for Scentre Group; in 2025 Australian office and retail real estate spreads widened as the RBA cash rate sat at 4.35% (Jan 2025), lifting average A-REIT borrowing costs by ~120 bps year-on-year. Debt providers thus control expansion capacity: tighter credit availability since 2024 raised secured loan pricing and reduced leverage headroom. Maintaining an investment-grade credit rating (Scentre held BBB+ by S&P in 2024) is vital to secure lower coupons and longer maturities. Any global liquidity tightening directly raises Scentre’s cost of capital, increasing funding costs for development and acquisitions.

Technology and Digital Service Providers

Scentre Group increasingly depends on specialized tech vendors for Westfield Direct and smart building systems, which deliver analytics and engagement tools that drove a 12% YoY lift in digital sales channels in FY2024.

These providers control proprietary platforms and APIs that are costly to replace; industry swap costs can exceed 6–9 months of lost operations and CAPEX of A$20–50m for enterprise integrations, giving vendors rising fee leverage.

- 12% YoY digital sales lift (FY2024)

- Switch costs: 6–9 months downtime

- Integration CAPEX estimate: A$20–50m

- Suppliers set fees, API standards

Government and Regulatory Bodies as Land Suppliers

Government bodies act as de facto land suppliers for Scentre Group by controlling zoning and development approvals; in 2024 Scentre sought 12 major planning permits across NSW and Victoria, with average approval timelines of 9–15 months that delay redevelopment cash flows.

This regulatory bottleneck limits available floor-space growth, making Scentre reliant on local and state policy—giving authorities leverage over project timing, costs, and feasibility and raising capex risk for the group.

- 12 major permits sought in 2024

- 9–15 months average approval time

- Regulatory delays raise capex timing risk

- Authorities control redevelopment feasibility

Suppliers wield leverage: AUD500–800m redevelopments, 40% PPA, BBB+ impacts finance

Suppliers hold moderate-to-high power: few Tier‑One contractors for AUD 500–800m redevelopments, 6% construction vacancy (ABS 2024), electricity ~2.8% of FY2024 opex, ~40% PPA coverage, $120m+ onsite solar, BBB+ rating (S&P 2024) affects borrowing costs; tech vendors drove 12% digital sales lift (FY2024) and entail A$20–50m swap CAPEX.

| Metric | Value |

|---|---|

| Redev. size | AUD 500–800m |

| Construction vacancy | 6% (2024) |

| Electricity opex | 2.8% (FY2024) |

| PPA cover | ~40% |

| Onsite solar | $120m+ |

| Credit rating | BBB+ (S&P 2024) |

| Digital sales lift | 12% YoY (FY2024) |

| Swap CAPEX | A$20–50m |

What is included in the product

Tailored exclusively for Scentre Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers protecting incumbents, and substitutes or disruptive threats shaping mall portfolio profitability.

A concise, one-sheet Porter's Five Forces summary for Scentre Group—quickly spot competitive pressures and real estate risks to inform leasing, development and portfolio decisions.

Customers Bargaining Power

Leverage of Major Anchor Tenants

Large anchors like Myer, David Jones and Woolworths/Coles drive 60–70% of weekly mall footfall in Scentre Group centres (Scentre FY2024), giving them strong leverage.

Because anchors are traffic-critical, they secure lower rent-to-sales ratios (often 5–8% vs 12–15% for specialty retailers), longer lease terms, and significant fit-out and turnover rent concessions.

Specialty Retailer Fragmentation

Specialty retailers in Westfield centres hold low individual bargaining power versus anchor tenants; Scentre Group’s curated footfall—Westfield attracted ~330 million visits in 2024—keeps demand for premium space high, letting Scentre push smaller-boutique rents upward.

Low Switching Costs for Global Brands

International luxury and fast-fashion brands have low switching costs and can relocate flagship stores; LVMH, Inditex, and H&M Group routinely rebalance store footprints across markets. If Scentre Group (Westfield) loses prestige or footfall, high-value tenants can move to rivals like Vicinity Centres or GPT, threatening rental income—top-tier tenants often pay 30–50% above mall averages. This mobility forces Scentre to reinvest: Westfield upgrades cost ~A$50–150 million per major mall refurbishment to protect rental yields and shopper traffic.

Consumer Influence on Tenant Health

Shoppers drive tenants’ sales and thus Scentre Group’s rent collectability; Australian retail sales rose 2.1% year-on-year to Nov 2025, but spending shifted 15% toward experiences per Roy Morgan’s 2025 leisure report, weakening landlords that keep product-heavy mixes.

Scentre must reweight leases toward dining, leisure and services—these categories saw 8–12% higher footfall in 2024–25—otherwise declining shopper interest cuts landlord bargaining power at renewals and forces rent incentives.

- Shoppers = ultimate payers; sales up 2.1% (Nov 2025)

- Experience spend +15% (Roy Morgan 2025)

- Dining/leisure footfall +8–12% (2024–25)

- Tenant mix shift needed to keep lease leverage

Impact of Short-Term Lease Flexibility

The shift to short-term leases and pop-ups lets retailers exit poor sites quickly; industry data shows pop-up tenancy rose ~18% in Australian malls in 2024, raising tenant bargaining power and churn risk for Scentre Group (ASX: SCG).

Retailers now demand flexible terms to hedge economic swings, forcing Scentre to adopt collaborative, performance-linked leases to sustain occupancy.

- Pop-up growth ~18% (2024)

- Higher churn risk

- More performance-linked leases

Anchors Drive 60–70% Footfall as Experience Spend Jumps 15%—Westfield 330M Visits

Large anchors (Myer, David Jones, Woolworths/Coles) drive 60–70% of mall footfall (Scentre FY2024), giving them strong rent leverage; specialty retailers face higher rents and lower bargaining power as Westfield attracted ~330m visits in 2024. Experience spend rose 15% (Roy Morgan 2025) and dining/leisure footfall +8–12% (2024–25), forcing Scentre to shift mixes and offer flexible, performance-linked leases; pop-ups grew ~18% (2024), raising churn risk.

| Metric | Value |

|---|---|

| Anchor share of footfall | 60–70% |

| Westfield visits (2024) | ~330m |

| Experience spend change (2025) | +15% |

| Dining/leisure footfall (2024–25) | +8–12% |

| Pop-up growth (2024) | ~18% |

Same Document Delivered

Scentre Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Scentre Group you’ll receive after purchase—no placeholders, no mockups, just the final, professionally formatted document ready for immediate download and use.