Schuler AG SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Schuler AG combines deep engineering expertise and a global footprint in metal forming with innovation in automation, but faces cyclical demand and margin pressure from raw material costs and competition; its strong service network and patents hint at resilient aftermarket revenue potential. Purchase the full SWOT analysis for a research-backed, editable report and Excel matrix to drive strategic or investment decisions.

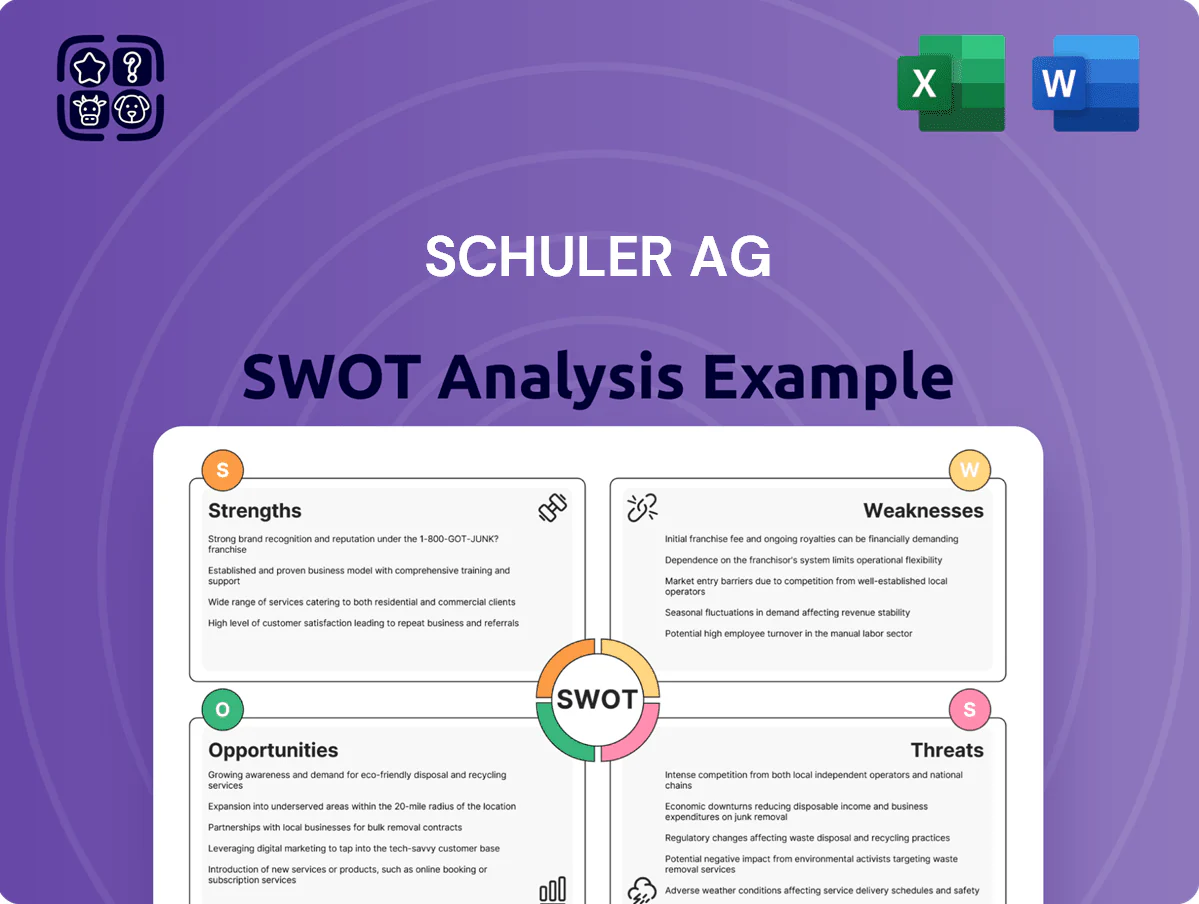

Strengths

Global Market Leadership in Metalforming

Schuler AG leads global metalforming, supplying ~40% of high-tonnage press lines worldwide and generating €710m revenue in FY2024, driven by automotive and e-mobility demand.

Advanced Technological Innovation and R&D

Schuler AG invests ~€60m annually in R&D (2024), funding ServoDirect and TwinServo systems that raise press output by up to 25% and cut energy use by ~18% versus mechanical presses; these gains helped Schuler secure €450m in 2024 order intake from automotive and e-mobility clients, keeping its presses the go-to for precision, high-throughput applications.

Strong Synergies with Andritz Group

As part of Andritz Group, Schuler gains financial backing—Andritz reported EUR 7.2bn revenue and EUR 386m EBIT in 2024—reducing liquidity risk and cushioning local downturns; shared procurement across ~30 production sites cuts input costs and shortens lead times. Cross-selling with Andritz plant-engineering teams increases large-project win rates, and centralized admin functions lower overheads, improving group EBITDA margins by several hundred basis points.

Comprehensive Lifecycle Service Network

- ~30% of 2024 revenue from services/spare parts

- Service margins ≈18% in 2024

- Retrofits increase installed-base lifetime and retention

- Rapid parts/support reduce production downtime

Strategic Focus on E-Mobility Solutions

Schuler AG pivoted its portfolio toward e-mobility, supplying presses and automation for battery housings, motor laminations, and lightweight structural parts; by FY2024 e-mobility orders made up about 28% of new bookings, underlining market fit.

This early alignment made Schuler a key partner for OEMs shifting from ICE to EVs, contributing to a 12% year-on-year revenue lift in Q4 2024 from e-mobility projects.

- 28% of 2024 bookings: e-mobility

- 12% revenue uplift Q4 2024 from e-mobility

- Key products: battery housings, motor laminations, lightweight structures

Market leader in high-tonnage presses: €710m revenue, 28% e-mobility bookings

Market leader in high-tonnage presses (~40% global share) with €710m revenue in FY2024; ~30% revenue from services (margins ≈18%).

R&D ~€60m (2024) funds ServoDirect/TwinServo: +25% output, −18% energy; 2024 order intake €450m; e-mobility = 28% bookings (12% Q4 2024 revenue lift).

| Metric | 2024 |

|---|---|

| Revenue | €710m |

| Service share | ~30% |

| Service margin | ≈18% |

| R&D spend | ~€60m |

| Order intake | €450m |

| E-mobility bookings | 28% |

What is included in the product

Provides a clear SWOT framework for analyzing Schuler AG’s business strategy, highlighting internal capabilities, operational gaps, market strengths, and external opportunities and threats shaping its competitive position.

Delivers a concise SWOT snapshot of Schuler AG for rapid strategic alignment and stakeholder updates.

Weaknesses

High Revenue Concentration in Automotive

Significant Exposure to European Energy Costs

Schuler AG’s large German/European footprint makes it highly exposed to regional energy volatility; German industrial electricity averaged about €0.39/kWh in 2023 vs EU industry €0.20/kWh, raising manufacturing overheads and eroding margins.

Higher gas and power costs can force price increases, weakening competitiveness vs lower-cost producers in Asia; in 2024 energy-related COGS spikes reportedly lifted some EU metalworking firms’ unit costs by 5–12%.

Maintaining margins requires continuous efficiency gains, capital investments in electrification and onsite generation, and hedging—else price pressure and margin compression vs global rivals will persist.

Complexity of Large-Scale Project Execution

The business model depends on delivering massive, bespoke engineering projects with multi-year lead times and complex logistics, and Schuler AG reported project backlog of about EUR 540m at FY 2024, so schedule slips can quickly scale. Delays in supply chains or installation raise risk of cost overruns and penalties; a single large contract can swing margins — FY 2024 gross margin was 10.2%. Meticulous project management is required, or financial exposure grows fast.

High Fixed Cost Structure

Schuler AG’s high-end engineering model requires a large specialist workforce and costly plants; fixed costs represented about 58% of total operating expenses in FY2024, amplifying margin pressure when orders fell 12% year-on-year.

Low capacity utilization during downturns raises per-unit costs and can swing operating leverage sharply; retaining skilled staff preserves product quality but restricts quick cost cuts.

- High fixed costs ≈58% of OPEX (FY2024)

- Orders down 12% YoY → lower utilization

- Skilled labor retention limits rapid cost reduction

Slower Digital Transformation of Legacy Hardware

Organizationally, Schuler must bridge heavy-equipment engineering culture and agile software practices, which raises time-to-market and integration costs, keeping digital margins below group averages.

- Installed base ~35,000 presses (2024)

- ~60% of shops delay digital retrofits >5 years

- SaaS growth constrained vs. hardware revenue

- Cultural gap slows product rollout and margin lift

Schuler risks: heavy auto reliance, high German energy costs & slow SaaS uptake

| Metric | Value |

|---|---|

| Auto revenue share | ~45% (2024) |

| OEM capex change | −12% YoY (Europe 2023–24) |

| German industrial power | €0.39/kWh (2023) |

| Fixed costs | ~58% OPEX (FY2024) |

| Orders | −12% YoY (2024) |

| Installed base | ~35,000 presses (2024) |

| Retrofit delay | ~60% defer >5 years |

What You See Is What You Get

Schuler AG SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Schuler AG combines deep engineering expertise and a global footprint in metal forming with innovation in automation, but faces cyclical demand and margin pressure from raw material costs and competition; its strong service network and patents hint at resilient aftermarket revenue potential. Purchase the full SWOT analysis for a research-backed, editable report and Excel matrix to drive strategic or investment decisions.

Strengths

Global Market Leadership in Metalforming

Schuler AG leads global metalforming, supplying ~40% of high-tonnage press lines worldwide and generating €710m revenue in FY2024, driven by automotive and e-mobility demand.

Advanced Technological Innovation and R&D

Schuler AG invests ~€60m annually in R&D (2024), funding ServoDirect and TwinServo systems that raise press output by up to 25% and cut energy use by ~18% versus mechanical presses; these gains helped Schuler secure €450m in 2024 order intake from automotive and e-mobility clients, keeping its presses the go-to for precision, high-throughput applications.

Strong Synergies with Andritz Group

As part of Andritz Group, Schuler gains financial backing—Andritz reported EUR 7.2bn revenue and EUR 386m EBIT in 2024—reducing liquidity risk and cushioning local downturns; shared procurement across ~30 production sites cuts input costs and shortens lead times. Cross-selling with Andritz plant-engineering teams increases large-project win rates, and centralized admin functions lower overheads, improving group EBITDA margins by several hundred basis points.

Comprehensive Lifecycle Service Network

- ~30% of 2024 revenue from services/spare parts

- Service margins ≈18% in 2024

- Retrofits increase installed-base lifetime and retention

- Rapid parts/support reduce production downtime

Strategic Focus on E-Mobility Solutions

Schuler AG pivoted its portfolio toward e-mobility, supplying presses and automation for battery housings, motor laminations, and lightweight structural parts; by FY2024 e-mobility orders made up about 28% of new bookings, underlining market fit.

This early alignment made Schuler a key partner for OEMs shifting from ICE to EVs, contributing to a 12% year-on-year revenue lift in Q4 2024 from e-mobility projects.

- 28% of 2024 bookings: e-mobility

- 12% revenue uplift Q4 2024 from e-mobility

- Key products: battery housings, motor laminations, lightweight structures

Market leader in high-tonnage presses: €710m revenue, 28% e-mobility bookings

Market leader in high-tonnage presses (~40% global share) with €710m revenue in FY2024; ~30% revenue from services (margins ≈18%).

R&D ~€60m (2024) funds ServoDirect/TwinServo: +25% output, −18% energy; 2024 order intake €450m; e-mobility = 28% bookings (12% Q4 2024 revenue lift).

| Metric | 2024 |

|---|---|

| Revenue | €710m |

| Service share | ~30% |

| Service margin | ≈18% |

| R&D spend | ~€60m |

| Order intake | €450m |

| E-mobility bookings | 28% |

What is included in the product

Provides a clear SWOT framework for analyzing Schuler AG’s business strategy, highlighting internal capabilities, operational gaps, market strengths, and external opportunities and threats shaping its competitive position.

Delivers a concise SWOT snapshot of Schuler AG for rapid strategic alignment and stakeholder updates.

Weaknesses

High Revenue Concentration in Automotive

Significant Exposure to European Energy Costs

Schuler AG’s large German/European footprint makes it highly exposed to regional energy volatility; German industrial electricity averaged about €0.39/kWh in 2023 vs EU industry €0.20/kWh, raising manufacturing overheads and eroding margins.

Higher gas and power costs can force price increases, weakening competitiveness vs lower-cost producers in Asia; in 2024 energy-related COGS spikes reportedly lifted some EU metalworking firms’ unit costs by 5–12%.

Maintaining margins requires continuous efficiency gains, capital investments in electrification and onsite generation, and hedging—else price pressure and margin compression vs global rivals will persist.

Complexity of Large-Scale Project Execution

The business model depends on delivering massive, bespoke engineering projects with multi-year lead times and complex logistics, and Schuler AG reported project backlog of about EUR 540m at FY 2024, so schedule slips can quickly scale. Delays in supply chains or installation raise risk of cost overruns and penalties; a single large contract can swing margins — FY 2024 gross margin was 10.2%. Meticulous project management is required, or financial exposure grows fast.

High Fixed Cost Structure

Schuler AG’s high-end engineering model requires a large specialist workforce and costly plants; fixed costs represented about 58% of total operating expenses in FY2024, amplifying margin pressure when orders fell 12% year-on-year.

Low capacity utilization during downturns raises per-unit costs and can swing operating leverage sharply; retaining skilled staff preserves product quality but restricts quick cost cuts.

- High fixed costs ≈58% of OPEX (FY2024)

- Orders down 12% YoY → lower utilization

- Skilled labor retention limits rapid cost reduction

Slower Digital Transformation of Legacy Hardware

Organizationally, Schuler must bridge heavy-equipment engineering culture and agile software practices, which raises time-to-market and integration costs, keeping digital margins below group averages.

- Installed base ~35,000 presses (2024)

- ~60% of shops delay digital retrofits >5 years

- SaaS growth constrained vs. hardware revenue

- Cultural gap slows product rollout and margin lift

Schuler risks: heavy auto reliance, high German energy costs & slow SaaS uptake

| Metric | Value |

|---|---|

| Auto revenue share | ~45% (2024) |

| OEM capex change | −12% YoY (Europe 2023–24) |

| German industrial power | €0.39/kWh (2023) |

| Fixed costs | ~58% OPEX (FY2024) |

| Orders | −12% YoY (2024) |

| Installed base | ~35,000 presses (2024) |

| Retrofit delay | ~60% defer >5 years |

What You See Is What You Get

Schuler AG SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.