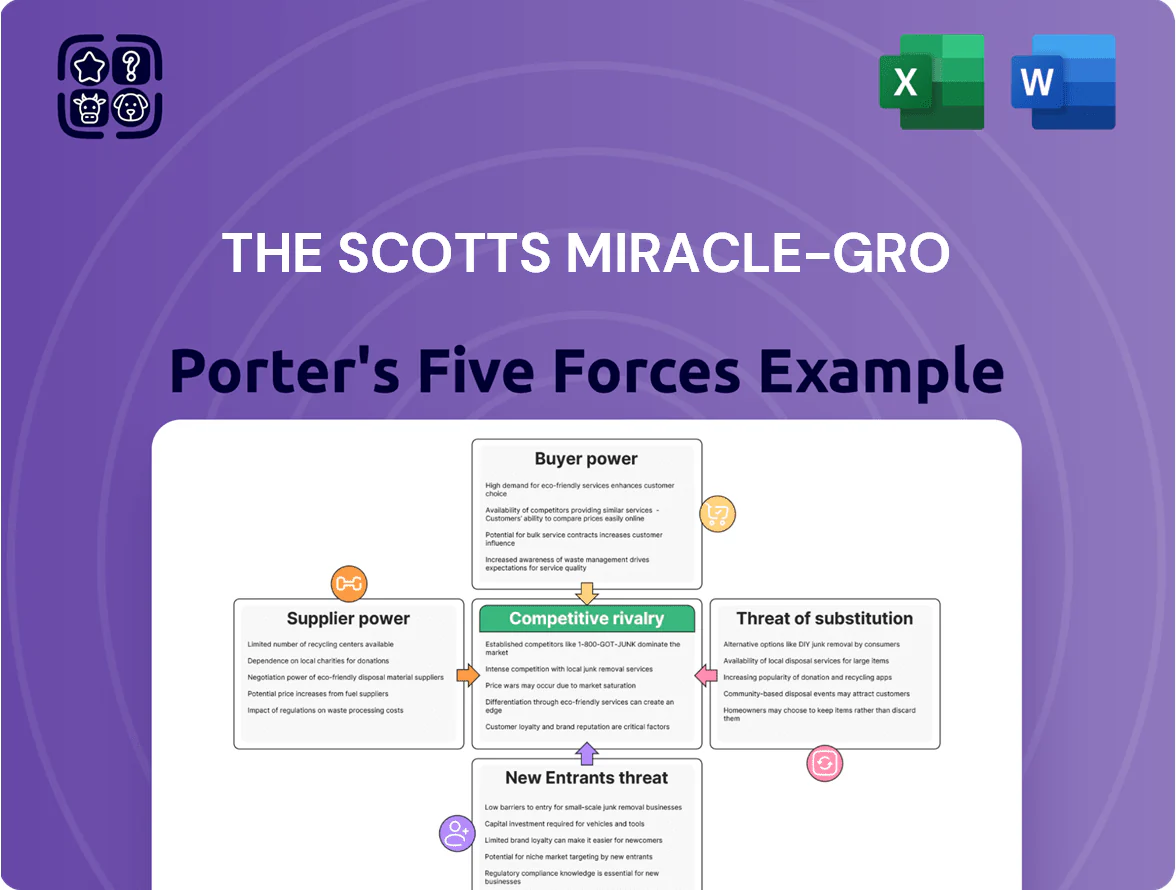

The Scotts Miracle-Gro Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Scotts Miracle‑Gro faces intense rivalry from diversified lawn and garden players, shifting buyer preferences toward organic alternatives, and moderate supplier leverage—while scale and brand provide defensive moats against new entrants and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore The Scotts Miracle-Gro’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Scotts Miracle-Gro depends on global commodities—urea, potash, phosphate—for ~40% of COGS in its lawn & garden segment (FY2024). Price volatility from geopolitics and supply disruptions sharply reduces pricing control, so Scotts used hedges covering roughly 60% of expected inputs in 2024 and passed about $120m of higher input costs to customers in FY2024 to protect margins.

Energy and Logistics Costs

Manufacturing and distributing heavy potting soil and fertilizers demands large energy and fuel inputs; in 2024 ScottsMiracle-Gro reported freight and energy-driven COGS pressure, with diesel averaging $4.10/gal in the US H1 2024, raising logistics spend by ~6–8% year-over-year.

Specialized Hydroponic Components

The Hawthorne Gardening segment relies on specialized suppliers for LED lighting, HVAC, and automated nutrient systems; although the hydroponics component market grew ~12% CAGR 2019–2024 to ~$3.8bn, top-tier manufacturers number in the low dozens, not hundreds, so suppliers kept pricing power—Hawthorne faced supplier-driven price uplifts of ~6–9% in 2023 during peak demand, squeezing margins on premium indoor-gardening SKUs.

Chemical Active Ingredient Sourcing

Labor Market Dynamics

Skilled labor availability for Scotts Miracle-Gro’s manufacturing plants and logistics hubs constrains production capacity, with U.S. manufacturing job openings at 723,000 in Dec 2024 signaling tight supply.

Regional competition for warehouse and factory workers—especially in Ohio and Indiana where key plants sit—pushed average hourly wages for production workers up ~6% year-over-year in 2024, raising operating costs.

Reliance on staffing agencies and the broader labor pool gives workers and agencies bargaining leverage during peak spring seasons, limiting rapid scaling and increasing temporary labor spend.

- 723,000 U.S. manufacturing openings, Dec 2024

- ~6% wage growth for production workers, 2024

- Higher seasonal temp labor costs, peak spring

Suppliers Hold the Levers: Top‑3 Supply 60% of Actives, Scotts Hedges Costs

Suppliers hold meaningful power: top-3 chemical suppliers supply ~60% of herbicide actives (2024), Scotts spent >$150m on chemicals and hedged ~60% of key fertilizer inputs in 2024; diesel averaged $4.10/gal H1 2024 raising logistics ~6–8%; Hawthorne saw supplier price uplifts 6–9% in 2023. Scotts uses multi-year contracts and joint R&D to limit supplier leverage.

| Metric | Value (2024) |

|---|---|

| Top‑3 supplier share | ≈60% |

| Chemical spend | >$150m |

| Input hedged | ~60% |

| Diesel (US H1) | $4.10/gal |

What is included in the product

Tailored exclusively for The Scotts Miracle‑Gro, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position.

A concise Porter's Five Forces snapshot for Scotts Miracle-Gro—highlighting supplier, buyer, rivalry, entry, and substitute pressures to speed strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Big-Box Retailers

A vast share of Scotts Miracle-Gro revenue — about 60% in FY2024 according to the company — comes from a few big-box partners like Home Depot, Lowe’s, and Walmart, concentrating customer power.

These retailers dictate pricing, shelf placement, and inventory terms, squeezing margins and forcing promotional funding; Scotts reported $150–200 million annual merchandising support in recent years.

If a major account cut orders, Scotts would face severe impact: a 10% decline in combined big-box sales would roughly equal a 6% revenue hit (~$240M on 2024 net sales of $4.0B), pressuring profit and cash flow.

Consumer Price Sensitivity

Scotts Miracle-Gro’s Scotts and Miracle-Gro brands command premium pricing, but 2024 US CPI-linked retail data show 62% of gardeners report higher price sensitivity; if branded SKUs exceed generic premiums by more than ~25% customers tend to downtrade to private labels, per 2023 NielsenIQ lawn/garden spending trends. This caps Scotts’ ability to raise prices without risking double-digit volume declines in key retail channels.

Rise of Private Label Brands

Many of Scotts Miracle-Gro Co's major retailers, including Home Depot and Lowe's, expanded private-label lawn and garden lines, capturing higher margins and pressuring branded sales; private-label share in US lawn/garden aisles rose to about 18% by 2024, up from ~12% in 2019.

These store brands sit beside Scotts on shelf at lower price points, offering consumers a convenient substitute; Scotts reported a 3–5% pricing premium erosion in core retail channels in 2023–24.

Internal retail competition forces Scotts to defend premium pricing through product innovation and marketing spend—Scotts increased R&D and SG&A investments to roughly $110 million in FY2024 to sustain differentiation.

Seasonal Demand Leverage

The gardening market’s spring surge concentrates roughly 60–70% of retail seasonal sales into a 8–12 week window, giving big-box retailers leverage to extract better credit terms and promotional allowances from Scotts Miracle-Gro in exchange for prime floor space for mulch, soil and bulky goods.

This seasonal squeeze forces Scotts to accept lower margins or higher marketing spend during spring; in 2024 Scotts reported 56% of net sales occurring in Q2, illustrating the buyer’s timing power.

- 60–70% sales in peak season

- 56% of Scotts 2024 net sales in Q2

- Retailers demand promo allowances, favorable credit

- Concentrated window increases buyer negotiating power

Information Transparency and E-commerce

The rise of e-commerce and price-comparison tools lets consumers quickly find lowest prices, eroding Scotts Miracle-Gro’s localized pricing power and forcing tighter price parity across online and retail channels.

Scotts reports rising digital marketing spend; industry data shows online garden retail grew ~12% in 2023–24, and acquisition costs for consumer goods rose roughly 18% year-over-year, increasing retention spend in a crowded digital market.

- Online garden retail growth ~12% (2023–24)

- Acquisition costs +18% YoY for consumer goods

- Price parity pressure across channels

- Higher digital marketing and retention spend

Big-box buyers wield power: 60% sales concentration, rising private-label & online pressure

Buyers are highly concentrated: ~60% of FY2024 sales tied to Home Depot, Lowe’s, Walmart, giving retailers strong pricing, placement, and promo leverage; Scotts paid ~$150–200M in merchandising support and saw Q2 = 56% of $4.0B sales, so a 10% big-box cut ≈ $240M loss. Private-label share rose to ~18% (2024), online garden retail +12% (2023–24), forcing higher marketing/R&D spend (~$110M in FY2024).

| Metric | Value |

|---|---|

| Big-box share | ~60% (FY2024) |

| Q2 share | 56% of $4.0B |

| Merch support | $150–200M |

| Private-label | ~18% (2024) |

| Online growth | +12% (2023–24) |

| R&D & SG&A | ~$110M (FY2024) |

What You See Is What You Get

The Scotts Miracle-Gro Porter's Five Forces Analysis

This preview shows the exact Scotts Miracle-Gro Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Scotts Miracle‑Gro faces intense rivalry from diversified lawn and garden players, shifting buyer preferences toward organic alternatives, and moderate supplier leverage—while scale and brand provide defensive moats against new entrants and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore The Scotts Miracle-Gro’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Scotts Miracle-Gro depends on global commodities—urea, potash, phosphate—for ~40% of COGS in its lawn & garden segment (FY2024). Price volatility from geopolitics and supply disruptions sharply reduces pricing control, so Scotts used hedges covering roughly 60% of expected inputs in 2024 and passed about $120m of higher input costs to customers in FY2024 to protect margins.

Energy and Logistics Costs

Manufacturing and distributing heavy potting soil and fertilizers demands large energy and fuel inputs; in 2024 ScottsMiracle-Gro reported freight and energy-driven COGS pressure, with diesel averaging $4.10/gal in the US H1 2024, raising logistics spend by ~6–8% year-over-year.

Specialized Hydroponic Components

The Hawthorne Gardening segment relies on specialized suppliers for LED lighting, HVAC, and automated nutrient systems; although the hydroponics component market grew ~12% CAGR 2019–2024 to ~$3.8bn, top-tier manufacturers number in the low dozens, not hundreds, so suppliers kept pricing power—Hawthorne faced supplier-driven price uplifts of ~6–9% in 2023 during peak demand, squeezing margins on premium indoor-gardening SKUs.

Chemical Active Ingredient Sourcing

Labor Market Dynamics

Skilled labor availability for Scotts Miracle-Gro’s manufacturing plants and logistics hubs constrains production capacity, with U.S. manufacturing job openings at 723,000 in Dec 2024 signaling tight supply.

Regional competition for warehouse and factory workers—especially in Ohio and Indiana where key plants sit—pushed average hourly wages for production workers up ~6% year-over-year in 2024, raising operating costs.

Reliance on staffing agencies and the broader labor pool gives workers and agencies bargaining leverage during peak spring seasons, limiting rapid scaling and increasing temporary labor spend.

- 723,000 U.S. manufacturing openings, Dec 2024

- ~6% wage growth for production workers, 2024

- Higher seasonal temp labor costs, peak spring

Suppliers Hold the Levers: Top‑3 Supply 60% of Actives, Scotts Hedges Costs

Suppliers hold meaningful power: top-3 chemical suppliers supply ~60% of herbicide actives (2024), Scotts spent >$150m on chemicals and hedged ~60% of key fertilizer inputs in 2024; diesel averaged $4.10/gal H1 2024 raising logistics ~6–8%; Hawthorne saw supplier price uplifts 6–9% in 2023. Scotts uses multi-year contracts and joint R&D to limit supplier leverage.

| Metric | Value (2024) |

|---|---|

| Top‑3 supplier share | ≈60% |

| Chemical spend | >$150m |

| Input hedged | ~60% |

| Diesel (US H1) | $4.10/gal |

What is included in the product

Tailored exclusively for The Scotts Miracle‑Gro, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position.

A concise Porter's Five Forces snapshot for Scotts Miracle-Gro—highlighting supplier, buyer, rivalry, entry, and substitute pressures to speed strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Big-Box Retailers

A vast share of Scotts Miracle-Gro revenue — about 60% in FY2024 according to the company — comes from a few big-box partners like Home Depot, Lowe’s, and Walmart, concentrating customer power.

These retailers dictate pricing, shelf placement, and inventory terms, squeezing margins and forcing promotional funding; Scotts reported $150–200 million annual merchandising support in recent years.

If a major account cut orders, Scotts would face severe impact: a 10% decline in combined big-box sales would roughly equal a 6% revenue hit (~$240M on 2024 net sales of $4.0B), pressuring profit and cash flow.

Consumer Price Sensitivity

Scotts Miracle-Gro’s Scotts and Miracle-Gro brands command premium pricing, but 2024 US CPI-linked retail data show 62% of gardeners report higher price sensitivity; if branded SKUs exceed generic premiums by more than ~25% customers tend to downtrade to private labels, per 2023 NielsenIQ lawn/garden spending trends. This caps Scotts’ ability to raise prices without risking double-digit volume declines in key retail channels.

Rise of Private Label Brands

Many of Scotts Miracle-Gro Co's major retailers, including Home Depot and Lowe's, expanded private-label lawn and garden lines, capturing higher margins and pressuring branded sales; private-label share in US lawn/garden aisles rose to about 18% by 2024, up from ~12% in 2019.

These store brands sit beside Scotts on shelf at lower price points, offering consumers a convenient substitute; Scotts reported a 3–5% pricing premium erosion in core retail channels in 2023–24.

Internal retail competition forces Scotts to defend premium pricing through product innovation and marketing spend—Scotts increased R&D and SG&A investments to roughly $110 million in FY2024 to sustain differentiation.

Seasonal Demand Leverage

The gardening market’s spring surge concentrates roughly 60–70% of retail seasonal sales into a 8–12 week window, giving big-box retailers leverage to extract better credit terms and promotional allowances from Scotts Miracle-Gro in exchange for prime floor space for mulch, soil and bulky goods.

This seasonal squeeze forces Scotts to accept lower margins or higher marketing spend during spring; in 2024 Scotts reported 56% of net sales occurring in Q2, illustrating the buyer’s timing power.

- 60–70% sales in peak season

- 56% of Scotts 2024 net sales in Q2

- Retailers demand promo allowances, favorable credit

- Concentrated window increases buyer negotiating power

Information Transparency and E-commerce

The rise of e-commerce and price-comparison tools lets consumers quickly find lowest prices, eroding Scotts Miracle-Gro’s localized pricing power and forcing tighter price parity across online and retail channels.

Scotts reports rising digital marketing spend; industry data shows online garden retail grew ~12% in 2023–24, and acquisition costs for consumer goods rose roughly 18% year-over-year, increasing retention spend in a crowded digital market.

- Online garden retail growth ~12% (2023–24)

- Acquisition costs +18% YoY for consumer goods

- Price parity pressure across channels

- Higher digital marketing and retention spend

Big-box buyers wield power: 60% sales concentration, rising private-label & online pressure

Buyers are highly concentrated: ~60% of FY2024 sales tied to Home Depot, Lowe’s, Walmart, giving retailers strong pricing, placement, and promo leverage; Scotts paid ~$150–200M in merchandising support and saw Q2 = 56% of $4.0B sales, so a 10% big-box cut ≈ $240M loss. Private-label share rose to ~18% (2024), online garden retail +12% (2023–24), forcing higher marketing/R&D spend (~$110M in FY2024).

| Metric | Value |

|---|---|

| Big-box share | ~60% (FY2024) |

| Q2 share | 56% of $4.0B |

| Merch support | $150–200M |

| Private-label | ~18% (2024) |

| Online growth | +12% (2023–24) |

| R&D & SG&A | ~$110M (FY2024) |

What You See Is What You Get

The Scotts Miracle-Gro Porter's Five Forces Analysis

This preview shows the exact Scotts Miracle-Gro Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.