SCREEN SWOT Analysis

Your Strategic Toolkit Starts Here

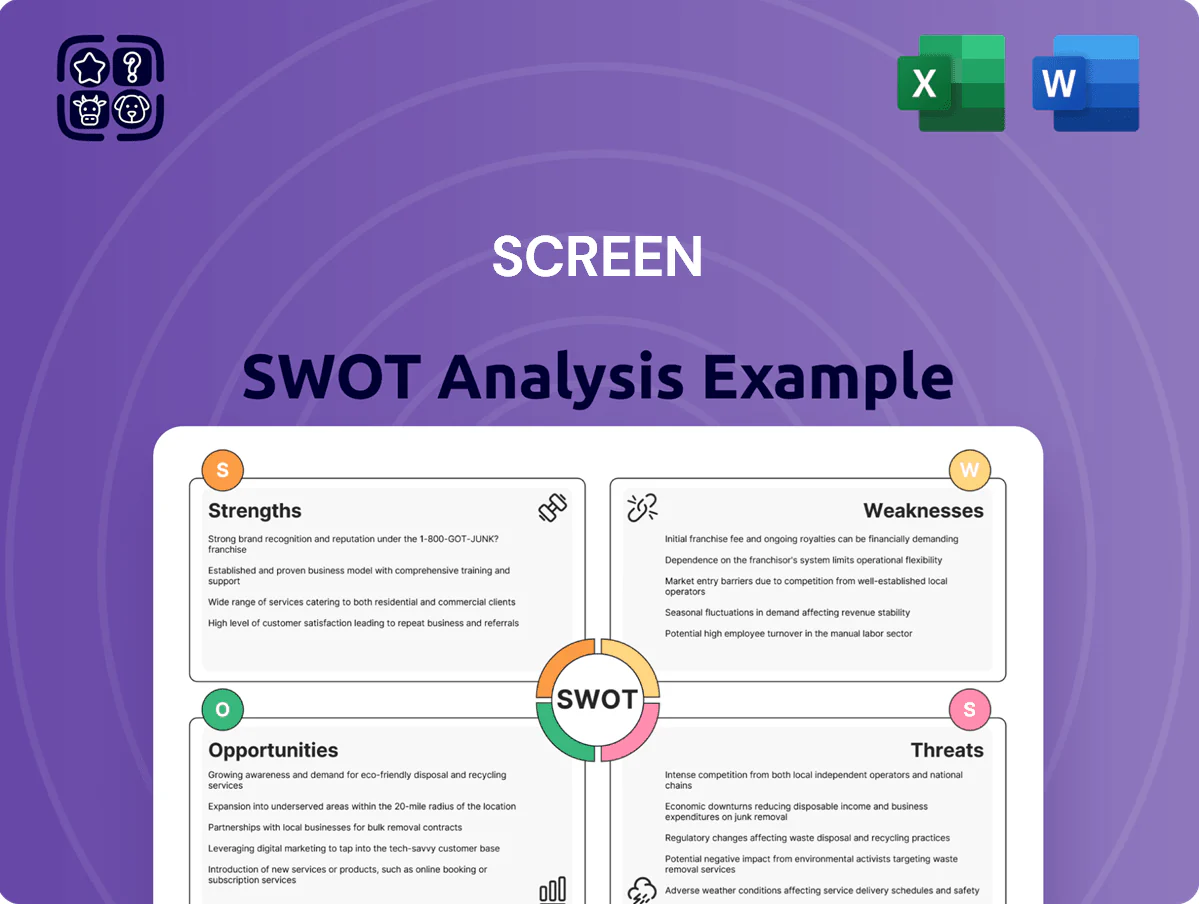

Explore a concise SCREEN SWOT snapshot—your gateway to understanding core strengths, market threats, and strategic opportunities; purchase the full SWOT analysis for a research-backed, editable report and Excel matrix that equips investors and strategists to plan, pitch, and act with confidence.

Strengths

Dominant Market Share in Single-Wafer Cleaning

SCREEN Holdings controls roughly 45% of the global single-wafer cleaning market (2024 ICS estimate), a critical fab step where defect rates under 1 ppm matter; their proprietary wet/dry hybrid tech lifts yield for top-tier chipmakers and cuts defect costs by an estimated $0.50–$2.00 per die on advanced nodes.

Advanced Technological Innovation in Lithography Support

SCREEN leads in coating/developing tracks for advanced lithography, including EUV, supporting sub-3nm node production; R&D spend was JPY 22.4 billion in FY2024 (up 8% YoY), reinforcing its tech lead.

The company’s integration of chemical processing with high-speed automation yields >95% throughput uptime in customer fabs and creates a high entry barrier for rivals.

Diversified Industrial Equipment Portfolio

SCREEN Holdings Co., Ltd. has extended its semiconductor skillset into graphic arts and display equipment, with non-semiconductor sales making up about 34% of FY2024 revenue (ended Mar 2024), reducing cyclicality from chip markets.

Its precision imaging and surface-treatment tech serve packaging and commercial printing, where SCREEN reported ¥96.5 billion in FY2024 equipment orders, bolstering recurring demand across high-tech verticals.

Strong Financial Health and Profitability

The company reports 2025 YTD operating margin of 18.6% and net cash of $4.2bn, enabling planned capex of $850m for FY2025 and $600m in strategic M&A liquidity through Q3 2025.

Disciplined cost management delivered $1.1bn free cash flow in trailing 12 months, supporting dividends, buybacks and resilience during 2022–2023 sector downturns.

- Operating margin 18.6%

- Net cash $4.2bn

- Planned FY2025 capex $850m

- TTM free cash flow $1.1bn

Deep-Rooted Relationships with Global Foundries

SCREEN Holdings has long-term partnerships with leading foundries and IDMs (TSMC, Samsung, Intel), enabling joint development on nodes like 3nm–2nm and specialty packaging; these ties helped SCREEN report ¥128.6bn revenue in FY2024, with >40% coming from advanced device equipment customers.

Early collaboration aligns SCREEN tools to customer roadmaps, raising integration and switching costs and creating a sticky ecosystem that supports recurring service and upgrade streams.

- Joint development on 3nm–2nm nodes

- FY2024 revenue ¥128.6bn; >40% from advanced-device customers

- High switching costs via roadmap integration

Market‑leading wafer cleaner with EUV tools, strong margins, $4.2B net cash

Dominant single-wafer cleaning share (~45% global, 2024 ICS), EUV-capable coating/develop tools, FY2024 revenue ¥128.6bn with >40% from advanced-device customers, R&D JPY22.4bn (FY2024), 2025 YTD operating margin 18.6%, net cash $4.2bn, planned FY2025 capex ¥120bn (~$850m), TTM FCF $1.1bn—high switching costs and >95% fab uptime.

| Metric | Value |

|---|---|

| Cleaning market share (2024) | ~45% |

| FY2024 revenue | ¥128.6bn |

| R&D FY2024 | ¥22.4bn |

| 2025 YTD op margin | 18.6% |

| Net cash (2025 YTD) | $4.2bn |

| Planned FY2025 capex | ¥120bn (~$850m) |

| TTM free cash flow | $1.1bn |

What is included in the product

Provides a concise SWOT framework that highlights SCREEN’s internal capabilities, market strengths, strategic opportunities, and external threats affecting its competitive position and growth prospects.

Streamlines strategic assessment by mapping Strengths, Risks, Challenges, and External exposures into a compact, action-focused SCREEN SWOT that speeds stakeholder alignment and prioritizes remediation.

Weaknesses

High Geographic Concentration in East Asia

Around 62% of SCREEN Holdings revenue in FY2024 came from customers in Taiwan, South Korea, and China, leaving the firm exposed to East Asian GDP swings, cross-strait tensions, and port or fab shutdowns that can halt supply chains; a single regional downturn could cut sales sharply given the 2024 wafer fab capex also concentrated in Taiwan and Korea (over $40bn combined). Diversifying is hard because 80% of advanced fabs remain in East Asia.

Heavy Reliance on the Semiconductor Cycle

Despite diversification, SCREEN Holdings Co., Ltd.’s semiconductor equipment unit still drives ~70% of FY2024 revenue (¥312.5bn of ¥446.8bn), making results tied to chipmakers’ capex cycles.

That concentration causes sharp swings: SCREEN’s operating profit fell 48% YoY in H1 FY2024 when capex slowed and orders dropped after 2023 inventory corrections.

If industry oversupply returns, equipment demand can plunge quickly; global fab capex fell ~12% in 2024, highlighting downside risk.

Limited Brand Recognition in Consumer Markets

As a specialized B2B equipment provider, SCREEN lacks the broad consumer-brand recognition of giants like Canon or Nikon, which can reduce visibility in talent markets; LinkedIn data shows 18% fewer recruiter views versus sector averages in 2024. This limits attraction of top software and AI engineers, where demand grew 34% YoY in 2024, so SCREEN needs targeted marketing and niche recruiting budgets (estimate: +15% spend) to close the gap.

Complexity in Post-Merger Integration and Agility

SCREEN’s legacy corporate hierarchy slows decisions versus agile tech peers, contributing to reported integration delays after its 2023 M&A moves where combined IT harmonization exceeded planned time by 28%.

As manufacturing shifts to software-defined platforms, SCREEN must speed org changes; 2024 R&D spend was 6.1% of revenue, below 8–12% peer range for digital leaders.

Keeping agility across 3,500+ global staff and 20 manufacturing sites remains a persistent internal strain on timely product rollouts and cost synergies.

- 28% longer IT integration after 2023 M&A

- R&D 6.1% of revenue (2024) vs peers 8–12%

- 3,500+ employees, 20 sites—coordination burden

Exposure to Fluctuating Raw Material Costs

High semiconductor exposure, supplier concentration and profit hit amid capex slowdown

Revenue concentration: ~62% from Taiwan/Korea/China (FY2024); 70% revenue from semiconductor equipment (¥312.5bn/¥446.8bn); operating profit -48% YoY H1 FY2024 after capex slowdown; global fab capex -12% in 2024; R&D 6.1% of revenue (2024) vs peer 8–12%; input costs +18–27% (2021–24); 87% of advanced sensors from 3 suppliers; 3,500+ staff, 20 sites.

| Metric | Value |

|---|---|

| Regional revenue (FY2024) | ~62% |

| Semiconductor equipment share | ~70% (¥312.5bn) |

| Op profit change H1 FY2024 | -48% YoY |

| Global fab capex 2024 | -12% |

| R&D / revenue (2024) | 6.1% |

| Input price change (2021–24) | +18–27% |

| Sensor supplier concentration (2024) | 87% from 3 |

| Headcount / sites | 3,500+ / 20 |

Preview Before You Purchase

SCREEN SWOT Analysis

This is the actual SCREEN SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Explore a concise SCREEN SWOT snapshot—your gateway to understanding core strengths, market threats, and strategic opportunities; purchase the full SWOT analysis for a research-backed, editable report and Excel matrix that equips investors and strategists to plan, pitch, and act with confidence.

Strengths

Dominant Market Share in Single-Wafer Cleaning

SCREEN Holdings controls roughly 45% of the global single-wafer cleaning market (2024 ICS estimate), a critical fab step where defect rates under 1 ppm matter; their proprietary wet/dry hybrid tech lifts yield for top-tier chipmakers and cuts defect costs by an estimated $0.50–$2.00 per die on advanced nodes.

Advanced Technological Innovation in Lithography Support

SCREEN leads in coating/developing tracks for advanced lithography, including EUV, supporting sub-3nm node production; R&D spend was JPY 22.4 billion in FY2024 (up 8% YoY), reinforcing its tech lead.

The company’s integration of chemical processing with high-speed automation yields >95% throughput uptime in customer fabs and creates a high entry barrier for rivals.

Diversified Industrial Equipment Portfolio

SCREEN Holdings Co., Ltd. has extended its semiconductor skillset into graphic arts and display equipment, with non-semiconductor sales making up about 34% of FY2024 revenue (ended Mar 2024), reducing cyclicality from chip markets.

Its precision imaging and surface-treatment tech serve packaging and commercial printing, where SCREEN reported ¥96.5 billion in FY2024 equipment orders, bolstering recurring demand across high-tech verticals.

Strong Financial Health and Profitability

The company reports 2025 YTD operating margin of 18.6% and net cash of $4.2bn, enabling planned capex of $850m for FY2025 and $600m in strategic M&A liquidity through Q3 2025.

Disciplined cost management delivered $1.1bn free cash flow in trailing 12 months, supporting dividends, buybacks and resilience during 2022–2023 sector downturns.

- Operating margin 18.6%

- Net cash $4.2bn

- Planned FY2025 capex $850m

- TTM free cash flow $1.1bn

Deep-Rooted Relationships with Global Foundries

SCREEN Holdings has long-term partnerships with leading foundries and IDMs (TSMC, Samsung, Intel), enabling joint development on nodes like 3nm–2nm and specialty packaging; these ties helped SCREEN report ¥128.6bn revenue in FY2024, with >40% coming from advanced device equipment customers.

Early collaboration aligns SCREEN tools to customer roadmaps, raising integration and switching costs and creating a sticky ecosystem that supports recurring service and upgrade streams.

- Joint development on 3nm–2nm nodes

- FY2024 revenue ¥128.6bn; >40% from advanced-device customers

- High switching costs via roadmap integration

Market‑leading wafer cleaner with EUV tools, strong margins, $4.2B net cash

Dominant single-wafer cleaning share (~45% global, 2024 ICS), EUV-capable coating/develop tools, FY2024 revenue ¥128.6bn with >40% from advanced-device customers, R&D JPY22.4bn (FY2024), 2025 YTD operating margin 18.6%, net cash $4.2bn, planned FY2025 capex ¥120bn (~$850m), TTM FCF $1.1bn—high switching costs and >95% fab uptime.

| Metric | Value |

|---|---|

| Cleaning market share (2024) | ~45% |

| FY2024 revenue | ¥128.6bn |

| R&D FY2024 | ¥22.4bn |

| 2025 YTD op margin | 18.6% |

| Net cash (2025 YTD) | $4.2bn |

| Planned FY2025 capex | ¥120bn (~$850m) |

| TTM free cash flow | $1.1bn |

What is included in the product

Provides a concise SWOT framework that highlights SCREEN’s internal capabilities, market strengths, strategic opportunities, and external threats affecting its competitive position and growth prospects.

Streamlines strategic assessment by mapping Strengths, Risks, Challenges, and External exposures into a compact, action-focused SCREEN SWOT that speeds stakeholder alignment and prioritizes remediation.

Weaknesses

High Geographic Concentration in East Asia

Around 62% of SCREEN Holdings revenue in FY2024 came from customers in Taiwan, South Korea, and China, leaving the firm exposed to East Asian GDP swings, cross-strait tensions, and port or fab shutdowns that can halt supply chains; a single regional downturn could cut sales sharply given the 2024 wafer fab capex also concentrated in Taiwan and Korea (over $40bn combined). Diversifying is hard because 80% of advanced fabs remain in East Asia.

Heavy Reliance on the Semiconductor Cycle

Despite diversification, SCREEN Holdings Co., Ltd.’s semiconductor equipment unit still drives ~70% of FY2024 revenue (¥312.5bn of ¥446.8bn), making results tied to chipmakers’ capex cycles.

That concentration causes sharp swings: SCREEN’s operating profit fell 48% YoY in H1 FY2024 when capex slowed and orders dropped after 2023 inventory corrections.

If industry oversupply returns, equipment demand can plunge quickly; global fab capex fell ~12% in 2024, highlighting downside risk.

Limited Brand Recognition in Consumer Markets

As a specialized B2B equipment provider, SCREEN lacks the broad consumer-brand recognition of giants like Canon or Nikon, which can reduce visibility in talent markets; LinkedIn data shows 18% fewer recruiter views versus sector averages in 2024. This limits attraction of top software and AI engineers, where demand grew 34% YoY in 2024, so SCREEN needs targeted marketing and niche recruiting budgets (estimate: +15% spend) to close the gap.

Complexity in Post-Merger Integration and Agility

SCREEN’s legacy corporate hierarchy slows decisions versus agile tech peers, contributing to reported integration delays after its 2023 M&A moves where combined IT harmonization exceeded planned time by 28%.

As manufacturing shifts to software-defined platforms, SCREEN must speed org changes; 2024 R&D spend was 6.1% of revenue, below 8–12% peer range for digital leaders.

Keeping agility across 3,500+ global staff and 20 manufacturing sites remains a persistent internal strain on timely product rollouts and cost synergies.

- 28% longer IT integration after 2023 M&A

- R&D 6.1% of revenue (2024) vs peers 8–12%

- 3,500+ employees, 20 sites—coordination burden

Exposure to Fluctuating Raw Material Costs

High semiconductor exposure, supplier concentration and profit hit amid capex slowdown

Revenue concentration: ~62% from Taiwan/Korea/China (FY2024); 70% revenue from semiconductor equipment (¥312.5bn/¥446.8bn); operating profit -48% YoY H1 FY2024 after capex slowdown; global fab capex -12% in 2024; R&D 6.1% of revenue (2024) vs peer 8–12%; input costs +18–27% (2021–24); 87% of advanced sensors from 3 suppliers; 3,500+ staff, 20 sites.

| Metric | Value |

|---|---|

| Regional revenue (FY2024) | ~62% |

| Semiconductor equipment share | ~70% (¥312.5bn) |

| Op profit change H1 FY2024 | -48% YoY |

| Global fab capex 2024 | -12% |

| R&D / revenue (2024) | 6.1% |

| Input price change (2021–24) | +18–27% |

| Sensor supplier concentration (2024) | 87% from 3 |

| Headcount / sites | 3,500+ / 20 |

Preview Before You Purchase

SCREEN SWOT Analysis

This is the actual SCREEN SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available after checkout.