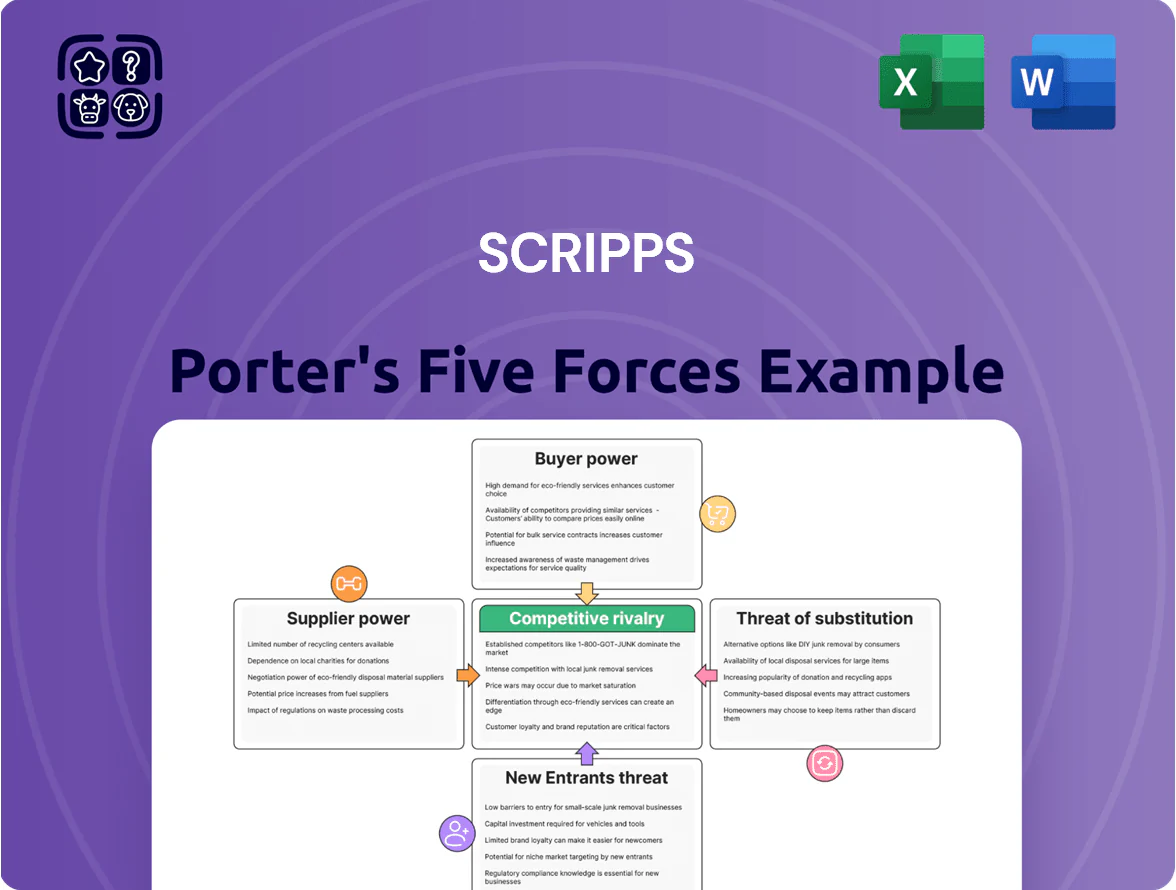

Scripps Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Scripps operates in a rapidly shifting media landscape where supplier bargaining, buyer fragmentation, digital substitutes, entry threats, and competitive rivalry collectively shape margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scripps’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content and Syndication Costs

The cost of acquiring high-quality national programming and syndicated shows remains a major expense for E.W. Scripps Company, which reported $1.64 billion in operating revenues and saw content and programming costs squeeze margins in 2024; top syndicated packages can cost tens of millions per show annually. Producers and syndicators hold leverage because Scripps needs popular content to sustain viewership and 2024 ad RPM pressure; rising production costs in 2023–2025 further raise bid prices and reduce bargaining power.

Sports Broadcasting Rights

As Scripps scales sports, supplier power — pro leagues and teams — is high: top US leagues renewed rights at record sums (eg NFL TV deals exceed $110B through 2033; MLB local packages rose ~15% in 2023), forcing Scripps to pay steep fees for exclusives. Competition from Disney/ESPN, Fox, Amazon and regional nets has driven bid prices and raised CPIs for rights; these deals are vital to reach 25–54 demos and pull premium ad rates.

Cloud and Digital Infrastructure

Scripps depends on third-party cloud and digital-infrastructure providers for streaming and data management; in 2024 Scripps reported digital ad revenue growth of 18% but outsources CDN, cloud compute, and ad-tech to major firms that control national distribution nodes.

Large tech firms like AWS, Google Cloud, and Akamai (common industry providers) underpin national networks, giving suppliers scale advantages and pricing power as Scripps’ 2024 capex shift favored OPEX for cloud services.

Switching these complex systems would likely cost tens of millions and risk service disruption, so supplier leverage is moderate-high and materially affects operating margins and gross margin volatility.

On-Air Talent and Personnel

Key anchors and local personalities drive Scripps Porter station identity; Nielsen 2023 local TV ratings show top anchors can command 20–40% higher ad CPMs, giving them leverage in pay talks.

In metros like Phoenix and Tampa, high-profile talent wins pay premiums—contracts may include raises of 15–35% and noncompete clauses—raising supplier (talent) bargaining power.

Losing a marquee anchor can cut viewership 5–12% within a quarter, increasing churn to rival stations and hurting local ad revenue.

- Anchors lift CPMs 20–40%

- Pay premiums 15–35% in major markets

- Audience loss 5–12% after departures

Network Equipment Manufacturers

The shift to ATSC 3.0 (NextGen TV) needs specialized transmitters, encoders, and RF gear from a small set of vendors, giving network equipment manufacturers strong leverage over Scripps’ costs and delivery timelines.

Regulatory specs and technical complexity mean switching suppliers is costly; as of 2025, ATSC 3.0-capable transmitter upgrades average $200k–$1.2M per station, so Scripps must keep supplier ties to avoid downtime and meet spectrum rules.

- Limited vendor pool concentrates supplier power

- ATSC 3.0 upgrade cost: $200k–$1.2M per station (2025)

- Technical/regulatory switching costs raise dependency

- Maintaining supplier relations ensures continuity and upgrades

Rising rights, cloud costs & ATSC 3.0 drive supplier power—Scripps faces $1.64B squeeze

Supplier power is moderate-high: content/sports rights and cloud/CDN vendors drive costs—Scripps faced $1.64B revenue in 2024 with rising programming costs; NFL/MLB deals pushed rights prices (NFL ~$110B total through 2033); cloud/OPEX shift raises dependence on AWS/Google/Akamai; ATSC 3.0 upgrades cost $200k–$1.2M per station (2025); top anchors lift CPMs 20–40% and demand 15–35% pay premiums.

| Item | Key number |

|---|---|

| 2024 revenue | $1.64B |

| NFL rights | $110B (through 2033) |

| ATSC 3.0 cost | $200k–$1.2M |

What is included in the product

Tailored exclusively for Scripps, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, barriers to entry, substitutes, and disruptive threats shaping its market position.

Scripps Porter’s Five Forces one-sheet distills competitive pressure into a clear, customizable radar chart—perfect for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

National Advertiser Leverage

Large agencies and national brands account for roughly 40%–50% of Scripps' advertising revenue, giving these buyers strong leverage to shift budgets to Google, Meta, or streaming rivals if Scripps cannot demonstrate superior reach or ROI.

The proliferation of programmatic, connected-TV, and social ad options—which captured over 60% of U.S. ad spend in 2024—limits Scripps' ability to command premium CPMs, forcing competitive pricing and performance guarantees.

MVPD Retransmission Negotiations

MVPDs (cable/satellite) haggle retransmission consent fees with Scripps; as US MVPD subscribers fell ~28% from 2015–2024 to ~60 million, distributors resist fee hikes to protect margins.

Stronger buyer bargaining means Scripps faces real risk of carriage loss—Scripps reported $1.6B in 2024 distribution revenue, so dropped carriage could materially cut cash flow.

Local Business Ad Spending

In local markets, small businesses choose social media and local search—Google Ads and Meta drove an estimated 63% of US SMB digital ad spend in 2024, so Scripps faces cheaper, highly targeted alternatives. That competition forces Scripps to match ROI or lower CPMs; local ad budgets average under $10k annually per SMB, raising price sensitivity. As a result, local buyers wield high bargaining power over Scripps’ local ad rates and package terms.

Direct-to-Consumer Expectations

Viewers now expect high-quality content free or cheap across phones, tablets, and smart TVs, and Scripps must meet that: in 2024 US streaming minutes rose 18% YoY, and ad-supported models grew 22%.

As Scripps expands digital apps and FAST channels, loyalty to TV schedules falls—linear TV ad revenue declined 6% in 2024—so churn risk rises unless personalization improves.

Switching apps is trivial, raising customers' indirect power over programming and ad strategy; average US household subscribes to 4.5 streaming services in 2025, upping competitive pressure.

- High-quality, low-cost demand: streaming minutes +18% (2024)

- Ad-supported growth: +22% (2024)

- Linear TV ad revenue: -6% (2024)

- Household streaming subs: 4.5 (2025)

Programmatic Ad Platforms

Programmatic ad platforms let buyers bypass sales teams and bid across networks, commoditizing inventory and pressuring Scripps' CPMs if its audiences aren't clearly differentiated.

In 2024 programmatic accounted for ~85% of US digital display spend and lowered average video CPMs ~15% YoY, so buyers can chase the lowest cost per reach instead of premium placements.

That means Scripps must prove unique audience value or face reduced yield and higher reliance on direct-sold premium deals.

- Scripps risk: falling CPMs vs programmatic market

- 2024: ~85% US display programmatic penetration

- Buyers prioritize cost-per-reach, pressuring premium rates

- Defense: prove niche audience metrics, sell direct premium

Scripps faces ad pressure: national buyers, programmatic & CTV shift threaten revenue

Large national buyers supply ~45% of Scripps’ ad revenue (2024), giving them leverage to shift spend to Google/Meta/streaming if CPMs or ROI lag; programmatic (≈85% of US display spend, 2024) and CTV/social (60%+ of ad spend, 2024) compress rates. MVPD carriage risk threatens $1.6B distribution revenue (2024) as MVPD subs fell ~28% since 2015. Local SMBs (avg <$10k/yr) favor Google/Meta (63% SMB digital spend, 2024), raising price sensitivity.

| Metric | Value (Year) |

|---|---|

| Share from national buyers | ~45% (2024) |

| Programmatic display penetration | ~85% (2024) |

| CTV/social share of ad spend | >60% (2024) |

| Distribution revenue | $1.6B (2024) |

| MVPD subs change | -28% (2015–2024) |

| SMB share to Google/Meta | 63% (2024) |

Preview the Actual Deliverable

Scripps Porter's Five Forces Analysis

This preview shows the exact Scripps Porter Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Scripps operates in a rapidly shifting media landscape where supplier bargaining, buyer fragmentation, digital substitutes, entry threats, and competitive rivalry collectively shape margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scripps’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content and Syndication Costs

The cost of acquiring high-quality national programming and syndicated shows remains a major expense for E.W. Scripps Company, which reported $1.64 billion in operating revenues and saw content and programming costs squeeze margins in 2024; top syndicated packages can cost tens of millions per show annually. Producers and syndicators hold leverage because Scripps needs popular content to sustain viewership and 2024 ad RPM pressure; rising production costs in 2023–2025 further raise bid prices and reduce bargaining power.

Sports Broadcasting Rights

As Scripps scales sports, supplier power — pro leagues and teams — is high: top US leagues renewed rights at record sums (eg NFL TV deals exceed $110B through 2033; MLB local packages rose ~15% in 2023), forcing Scripps to pay steep fees for exclusives. Competition from Disney/ESPN, Fox, Amazon and regional nets has driven bid prices and raised CPIs for rights; these deals are vital to reach 25–54 demos and pull premium ad rates.

Cloud and Digital Infrastructure

Scripps depends on third-party cloud and digital-infrastructure providers for streaming and data management; in 2024 Scripps reported digital ad revenue growth of 18% but outsources CDN, cloud compute, and ad-tech to major firms that control national distribution nodes.

Large tech firms like AWS, Google Cloud, and Akamai (common industry providers) underpin national networks, giving suppliers scale advantages and pricing power as Scripps’ 2024 capex shift favored OPEX for cloud services.

Switching these complex systems would likely cost tens of millions and risk service disruption, so supplier leverage is moderate-high and materially affects operating margins and gross margin volatility.

On-Air Talent and Personnel

Key anchors and local personalities drive Scripps Porter station identity; Nielsen 2023 local TV ratings show top anchors can command 20–40% higher ad CPMs, giving them leverage in pay talks.

In metros like Phoenix and Tampa, high-profile talent wins pay premiums—contracts may include raises of 15–35% and noncompete clauses—raising supplier (talent) bargaining power.

Losing a marquee anchor can cut viewership 5–12% within a quarter, increasing churn to rival stations and hurting local ad revenue.

- Anchors lift CPMs 20–40%

- Pay premiums 15–35% in major markets

- Audience loss 5–12% after departures

Network Equipment Manufacturers

The shift to ATSC 3.0 (NextGen TV) needs specialized transmitters, encoders, and RF gear from a small set of vendors, giving network equipment manufacturers strong leverage over Scripps’ costs and delivery timelines.

Regulatory specs and technical complexity mean switching suppliers is costly; as of 2025, ATSC 3.0-capable transmitter upgrades average $200k–$1.2M per station, so Scripps must keep supplier ties to avoid downtime and meet spectrum rules.

- Limited vendor pool concentrates supplier power

- ATSC 3.0 upgrade cost: $200k–$1.2M per station (2025)

- Technical/regulatory switching costs raise dependency

- Maintaining supplier relations ensures continuity and upgrades

Rising rights, cloud costs & ATSC 3.0 drive supplier power—Scripps faces $1.64B squeeze

Supplier power is moderate-high: content/sports rights and cloud/CDN vendors drive costs—Scripps faced $1.64B revenue in 2024 with rising programming costs; NFL/MLB deals pushed rights prices (NFL ~$110B total through 2033); cloud/OPEX shift raises dependence on AWS/Google/Akamai; ATSC 3.0 upgrades cost $200k–$1.2M per station (2025); top anchors lift CPMs 20–40% and demand 15–35% pay premiums.

| Item | Key number |

|---|---|

| 2024 revenue | $1.64B |

| NFL rights | $110B (through 2033) |

| ATSC 3.0 cost | $200k–$1.2M |

What is included in the product

Tailored exclusively for Scripps, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, barriers to entry, substitutes, and disruptive threats shaping its market position.

Scripps Porter’s Five Forces one-sheet distills competitive pressure into a clear, customizable radar chart—perfect for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

National Advertiser Leverage

Large agencies and national brands account for roughly 40%–50% of Scripps' advertising revenue, giving these buyers strong leverage to shift budgets to Google, Meta, or streaming rivals if Scripps cannot demonstrate superior reach or ROI.

The proliferation of programmatic, connected-TV, and social ad options—which captured over 60% of U.S. ad spend in 2024—limits Scripps' ability to command premium CPMs, forcing competitive pricing and performance guarantees.

MVPD Retransmission Negotiations

MVPDs (cable/satellite) haggle retransmission consent fees with Scripps; as US MVPD subscribers fell ~28% from 2015–2024 to ~60 million, distributors resist fee hikes to protect margins.

Stronger buyer bargaining means Scripps faces real risk of carriage loss—Scripps reported $1.6B in 2024 distribution revenue, so dropped carriage could materially cut cash flow.

Local Business Ad Spending

In local markets, small businesses choose social media and local search—Google Ads and Meta drove an estimated 63% of US SMB digital ad spend in 2024, so Scripps faces cheaper, highly targeted alternatives. That competition forces Scripps to match ROI or lower CPMs; local ad budgets average under $10k annually per SMB, raising price sensitivity. As a result, local buyers wield high bargaining power over Scripps’ local ad rates and package terms.

Direct-to-Consumer Expectations

Viewers now expect high-quality content free or cheap across phones, tablets, and smart TVs, and Scripps must meet that: in 2024 US streaming minutes rose 18% YoY, and ad-supported models grew 22%.

As Scripps expands digital apps and FAST channels, loyalty to TV schedules falls—linear TV ad revenue declined 6% in 2024—so churn risk rises unless personalization improves.

Switching apps is trivial, raising customers' indirect power over programming and ad strategy; average US household subscribes to 4.5 streaming services in 2025, upping competitive pressure.

- High-quality, low-cost demand: streaming minutes +18% (2024)

- Ad-supported growth: +22% (2024)

- Linear TV ad revenue: -6% (2024)

- Household streaming subs: 4.5 (2025)

Programmatic Ad Platforms

Programmatic ad platforms let buyers bypass sales teams and bid across networks, commoditizing inventory and pressuring Scripps' CPMs if its audiences aren't clearly differentiated.

In 2024 programmatic accounted for ~85% of US digital display spend and lowered average video CPMs ~15% YoY, so buyers can chase the lowest cost per reach instead of premium placements.

That means Scripps must prove unique audience value or face reduced yield and higher reliance on direct-sold premium deals.

- Scripps risk: falling CPMs vs programmatic market

- 2024: ~85% US display programmatic penetration

- Buyers prioritize cost-per-reach, pressuring premium rates

- Defense: prove niche audience metrics, sell direct premium

Scripps faces ad pressure: national buyers, programmatic & CTV shift threaten revenue

Large national buyers supply ~45% of Scripps’ ad revenue (2024), giving them leverage to shift spend to Google/Meta/streaming if CPMs or ROI lag; programmatic (≈85% of US display spend, 2024) and CTV/social (60%+ of ad spend, 2024) compress rates. MVPD carriage risk threatens $1.6B distribution revenue (2024) as MVPD subs fell ~28% since 2015. Local SMBs (avg <$10k/yr) favor Google/Meta (63% SMB digital spend, 2024), raising price sensitivity.

| Metric | Value (Year) |

|---|---|

| Share from national buyers | ~45% (2024) |

| Programmatic display penetration | ~85% (2024) |

| CTV/social share of ad spend | >60% (2024) |

| Distribution revenue | $1.6B (2024) |

| MVPD subs change | -28% (2015–2024) |

| SMB share to Google/Meta | 63% (2024) |

Preview the Actual Deliverable

Scripps Porter's Five Forces Analysis

This preview shows the exact Scripps Porter Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.