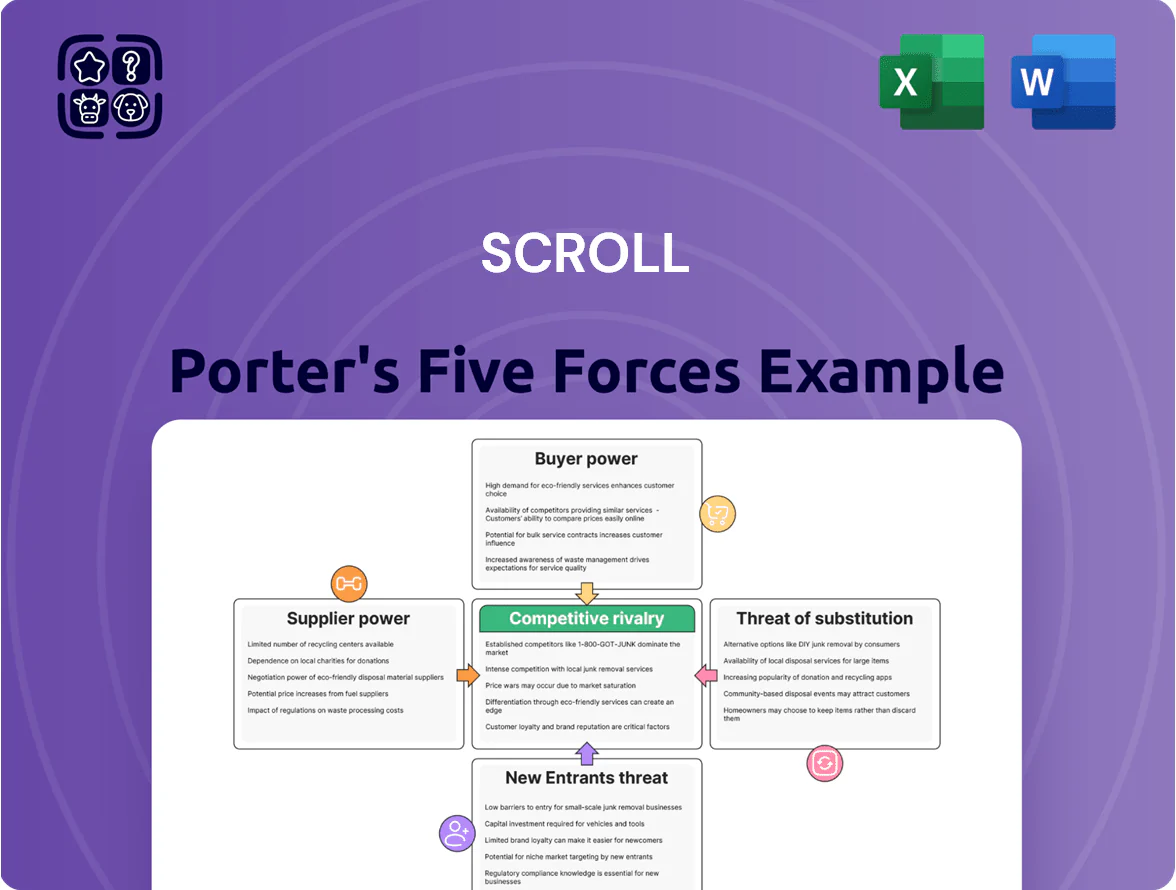

Scroll Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Scroll faces moderate supplier leverage and tech-driven rivalry, while buyer bargaining and substitutes hinge on adoption and interoperability; regulatory shifts add a wildcard to competitive intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scroll’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of apparel and miscellaneous goods manufacturers

Scroll sources from 120+ small–medium apparel and misc. manufacturers across Asia and Japan, so no single supplier holds pricing power; top five suppliers account for under 18% of purchases (FY2024). Fragmentation lets Scroll switch factories within 4–8 weeks when costs or quality slip, keeping supplier negotiation leverage high and input-cost pass-through low.

Dependency on major logistics and delivery providers

Scroll depends on national carriers such as Yamato Transport and Sagawa Express for most mail-order fulfillment; in Japan these two handle roughly 60–70% of B2C parcel volume (MLIT 2024), giving them strong leverage over rates and service terms.

Because carrier concentration is high, a 5–10% logistics price rise — similar to the 2023–24 fuel-related tariff increases — would cut Scroll’s e-commerce gross margin by an estimated 1.2–2.5 percentage points on FY2024 sales of ¥45 billion.

Volatility in raw material and energy costs

Suppliers of textiles and health products face commodity and energy swings; cotton prices rose 22% in 2024 and global oil averaged $84/barrel in 2024, so vendors have passed higher input costs to buyers.

Scroll saw supplier-led procurement cost increases of roughly 6–9% in FY2024, squeezing gross margin if retail prices stay fixed.

The company must absorb, hedge, or pass on costs; a 3–5% retail price rise would offset most FY2024 supplier inflation but risks lower volume.

Concentration of specialized beauty and health ingredients

In beauty and health, a handful of specialty chemical firms hold patents on high‑demand actives; 2024 data show top 5 suppliers control ~62% of global bioactive peptide supply, giving them price and delivery leverage over buyers like Scroll.

Scroll reduces this risk by broadening formulations across 18 product lines and spending $9.2M on R&D in FY2024 to develop in‑house alternatives and backward integrate some ingredient synthesis.

- Top 5 suppliers ≈62% market share for peptides

- Scroll: 18 product lines

- R&D spend FY2024: $9.2M

- Mitigation: in‑house alternatives, supplier diversification

Influence of digital infrastructure and cloud service providers

As an e-commerce firm, Scroll relies on global cloud providers (AWS, Microsoft Azure, Google Cloud) for compute and data services, giving those suppliers strong bargaining power due to high technical switching costs and vendor lock-in.

These platforms control pricing and feature roadmaps; in 2024 hyperscaler capex totaled roughly $150–200 billion, keeping market leverage high and pushing Scroll to absorb rising cloud costs.

Maintaining uptime, security, and compliance forces ongoing spend—cloud can be 20–30% of tech opex for mid-size e-commerce firms—so Scroll must budget for recurring price and terms exposure.

- High supplier power: hyperscalers dominate market share

- Switching cost: migration complexity and data egress fees

- Cost impact: cloud ~20–30% of tech opex

- Risk: pricing changes, compliance and service dependence

Supplier squeeze: logistics, hyperscalers and peptide concentration threaten margins

Suppliers wield mixed power: fragmented apparel vendors (120+; top‑5 <18% FY2024) keep input leverage low, but concentrated carriers (Yamato/Sagawa 60–70% B2C) and hyperscalers (AWS/Azure/GCP) raise costs; FY2024 supplier inflation +6–9% cut margins, logistics +5–10% would trim gross margin ~1.2–2.5 pts on ¥45B sales; R&D ¥9.2M and 18 product lines partly mitigate peptide supplier (top‑5 ≈62%) risks.

| Metric | Value |

|---|---|

| Sales FY2024 | ¥45B |

| Top‑5 apparel share | <18% |

| Carrier share (Japan) | 60–70% |

| Supplier inflation | 6–9% |

| R&D FY2024 | ¥9.2M |

| Peptide top‑5 | ≈62% |

What is included in the product

Tailored Five Forces analysis for Scroll that uncovers competitive drivers, buyer and supplier power, threat of substitutes and entrants, and identifies disruptive risks and strategic levers to protect market share and profitability.

Interactive Five Forces summary that highlights where strategic relief is needed—pinpoint high-pressure areas and prioritize countermeasures fast.

Customers Bargaining Power

Low switching costs for individual retail consumers

High price transparency and comparison tools

Japanese shoppers use price-comparison apps like Kakaku.com and Google Shopping; 72% of online buyers check prices across sites in 2024, forcing Scroll to match market rates and compress gross margins on standardized and third-party goods.

Demand for seamless delivery and return experiences

Customers now treat fast, low-cost shipping as standard—68% of US online shoppers expected free two-day shipping in 2024, so buyers abandon carts quickly when fees appear.

That abandonment gives buyers real leverage: Scroll risks conversion drops if shipping isn't competitive, yet its logistics costs rose ~12% in 2023–24, forcing trade-offs between margin and service.

Influence of social proof and online reviews

Customer buys sway strongly to peer reviews and social sentiment; 89% of shoppers (2024 BrightLocal) trust online reviews as much as personal recommendations, so product quality and reliability chatter drives purchase flow.

Negative review trends cut conversion rates quickly—a 1-star drop can lower sales by ~5–9% per Harvard Business Review (2022), eroding market share and revenue.

Buyers wield power via collective voice, social shares, and review platforms that can instantly alter brand valuation and short-term cash flow.

- 89% trust reviews (BrightLocal 2024)

- 1-star drop → −5–9% sales (HBR 2022)

- Social reach amplifies reputation risk, affecting revenue fast

Negotiation leverage of B2B solution clients

In the B2B e-commerce segment, Scroll faces strong customer bargaining power as corporate clients use professional procurement teams to extract customized SLAs and volume discounts; top 10 clients made up about 48% of segment revenue in 2024, so losing one major contract would slash revenue and raise churn risk materially.

Their leverage pushes Scroll to accept longer payment terms (avg 75 days in 2024) and tiered pricing, compressing margins by an estimated 220–350 basis points versus SMB deals.

- Top-10 clients ≈48% of B2B revenue (2024)

- Average payment terms 75 days (2024)

- Margin hit 220–350 bps vs SMB

- High concentration → single-contract risk

Customer power crushes margins: high churn, costly retention, and B2B payment drag

Customers hold high bargaining power: one-tap switching, low loyalty, and review-driven demand suppress margins and spike churn; retention CAC hit $45 (US, 2024) and app churn ~6%/mo. Price checks (72% in 2024) compress margins; shipping expectations (68% expect free 2-day) force cost-service trade-offs. B2B concentration (top10≈48% revenue) and 75-day terms cut margins ~220–350 bps.

| Metric | Value |

|---|---|

| Retention CAC (US) | $45 (2024) |

| App churn | ~6%/mo (2024) |

| Price checks | 72% (2024) |

| Free 2-day expectation | 68% (2024) |

| B2B top-10 share | ≈48% (2024) |

| Avg payment terms (B2B) | 75 days (2024) |

| Margin hit (B2B) | 220–350 bps |

What You See Is What You Get

Scroll Porter's Five Forces Analysis

This preview shows the exact Scroll Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups; the file is fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Scroll faces moderate supplier leverage and tech-driven rivalry, while buyer bargaining and substitutes hinge on adoption and interoperability; regulatory shifts add a wildcard to competitive intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scroll’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of apparel and miscellaneous goods manufacturers

Scroll sources from 120+ small–medium apparel and misc. manufacturers across Asia and Japan, so no single supplier holds pricing power; top five suppliers account for under 18% of purchases (FY2024). Fragmentation lets Scroll switch factories within 4–8 weeks when costs or quality slip, keeping supplier negotiation leverage high and input-cost pass-through low.

Dependency on major logistics and delivery providers

Scroll depends on national carriers such as Yamato Transport and Sagawa Express for most mail-order fulfillment; in Japan these two handle roughly 60–70% of B2C parcel volume (MLIT 2024), giving them strong leverage over rates and service terms.

Because carrier concentration is high, a 5–10% logistics price rise — similar to the 2023–24 fuel-related tariff increases — would cut Scroll’s e-commerce gross margin by an estimated 1.2–2.5 percentage points on FY2024 sales of ¥45 billion.

Volatility in raw material and energy costs

Suppliers of textiles and health products face commodity and energy swings; cotton prices rose 22% in 2024 and global oil averaged $84/barrel in 2024, so vendors have passed higher input costs to buyers.

Scroll saw supplier-led procurement cost increases of roughly 6–9% in FY2024, squeezing gross margin if retail prices stay fixed.

The company must absorb, hedge, or pass on costs; a 3–5% retail price rise would offset most FY2024 supplier inflation but risks lower volume.

Concentration of specialized beauty and health ingredients

In beauty and health, a handful of specialty chemical firms hold patents on high‑demand actives; 2024 data show top 5 suppliers control ~62% of global bioactive peptide supply, giving them price and delivery leverage over buyers like Scroll.

Scroll reduces this risk by broadening formulations across 18 product lines and spending $9.2M on R&D in FY2024 to develop in‑house alternatives and backward integrate some ingredient synthesis.

- Top 5 suppliers ≈62% market share for peptides

- Scroll: 18 product lines

- R&D spend FY2024: $9.2M

- Mitigation: in‑house alternatives, supplier diversification

Influence of digital infrastructure and cloud service providers

As an e-commerce firm, Scroll relies on global cloud providers (AWS, Microsoft Azure, Google Cloud) for compute and data services, giving those suppliers strong bargaining power due to high technical switching costs and vendor lock-in.

These platforms control pricing and feature roadmaps; in 2024 hyperscaler capex totaled roughly $150–200 billion, keeping market leverage high and pushing Scroll to absorb rising cloud costs.

Maintaining uptime, security, and compliance forces ongoing spend—cloud can be 20–30% of tech opex for mid-size e-commerce firms—so Scroll must budget for recurring price and terms exposure.

- High supplier power: hyperscalers dominate market share

- Switching cost: migration complexity and data egress fees

- Cost impact: cloud ~20–30% of tech opex

- Risk: pricing changes, compliance and service dependence

Supplier squeeze: logistics, hyperscalers and peptide concentration threaten margins

Suppliers wield mixed power: fragmented apparel vendors (120+; top‑5 <18% FY2024) keep input leverage low, but concentrated carriers (Yamato/Sagawa 60–70% B2C) and hyperscalers (AWS/Azure/GCP) raise costs; FY2024 supplier inflation +6–9% cut margins, logistics +5–10% would trim gross margin ~1.2–2.5 pts on ¥45B sales; R&D ¥9.2M and 18 product lines partly mitigate peptide supplier (top‑5 ≈62%) risks.

| Metric | Value |

|---|---|

| Sales FY2024 | ¥45B |

| Top‑5 apparel share | <18% |

| Carrier share (Japan) | 60–70% |

| Supplier inflation | 6–9% |

| R&D FY2024 | ¥9.2M |

| Peptide top‑5 | ≈62% |

What is included in the product

Tailored Five Forces analysis for Scroll that uncovers competitive drivers, buyer and supplier power, threat of substitutes and entrants, and identifies disruptive risks and strategic levers to protect market share and profitability.

Interactive Five Forces summary that highlights where strategic relief is needed—pinpoint high-pressure areas and prioritize countermeasures fast.

Customers Bargaining Power

Low switching costs for individual retail consumers

High price transparency and comparison tools

Japanese shoppers use price-comparison apps like Kakaku.com and Google Shopping; 72% of online buyers check prices across sites in 2024, forcing Scroll to match market rates and compress gross margins on standardized and third-party goods.

Demand for seamless delivery and return experiences

Customers now treat fast, low-cost shipping as standard—68% of US online shoppers expected free two-day shipping in 2024, so buyers abandon carts quickly when fees appear.

That abandonment gives buyers real leverage: Scroll risks conversion drops if shipping isn't competitive, yet its logistics costs rose ~12% in 2023–24, forcing trade-offs between margin and service.

Influence of social proof and online reviews

Customer buys sway strongly to peer reviews and social sentiment; 89% of shoppers (2024 BrightLocal) trust online reviews as much as personal recommendations, so product quality and reliability chatter drives purchase flow.

Negative review trends cut conversion rates quickly—a 1-star drop can lower sales by ~5–9% per Harvard Business Review (2022), eroding market share and revenue.

Buyers wield power via collective voice, social shares, and review platforms that can instantly alter brand valuation and short-term cash flow.

- 89% trust reviews (BrightLocal 2024)

- 1-star drop → −5–9% sales (HBR 2022)

- Social reach amplifies reputation risk, affecting revenue fast

Negotiation leverage of B2B solution clients

In the B2B e-commerce segment, Scroll faces strong customer bargaining power as corporate clients use professional procurement teams to extract customized SLAs and volume discounts; top 10 clients made up about 48% of segment revenue in 2024, so losing one major contract would slash revenue and raise churn risk materially.

Their leverage pushes Scroll to accept longer payment terms (avg 75 days in 2024) and tiered pricing, compressing margins by an estimated 220–350 basis points versus SMB deals.

- Top-10 clients ≈48% of B2B revenue (2024)

- Average payment terms 75 days (2024)

- Margin hit 220–350 bps vs SMB

- High concentration → single-contract risk

Customer power crushes margins: high churn, costly retention, and B2B payment drag

Customers hold high bargaining power: one-tap switching, low loyalty, and review-driven demand suppress margins and spike churn; retention CAC hit $45 (US, 2024) and app churn ~6%/mo. Price checks (72% in 2024) compress margins; shipping expectations (68% expect free 2-day) force cost-service trade-offs. B2B concentration (top10≈48% revenue) and 75-day terms cut margins ~220–350 bps.

| Metric | Value |

|---|---|

| Retention CAC (US) | $45 (2024) |

| App churn | ~6%/mo (2024) |

| Price checks | 72% (2024) |

| Free 2-day expectation | 68% (2024) |

| B2B top-10 share | ≈48% (2024) |

| Avg payment terms (B2B) | 75 days (2024) |

| Margin hit (B2B) | 220–350 bps |

What You See Is What You Get

Scroll Porter's Five Forces Analysis

This preview shows the exact Scroll Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups; the file is fully formatted and ready for use.