Shandong Gold Mining Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

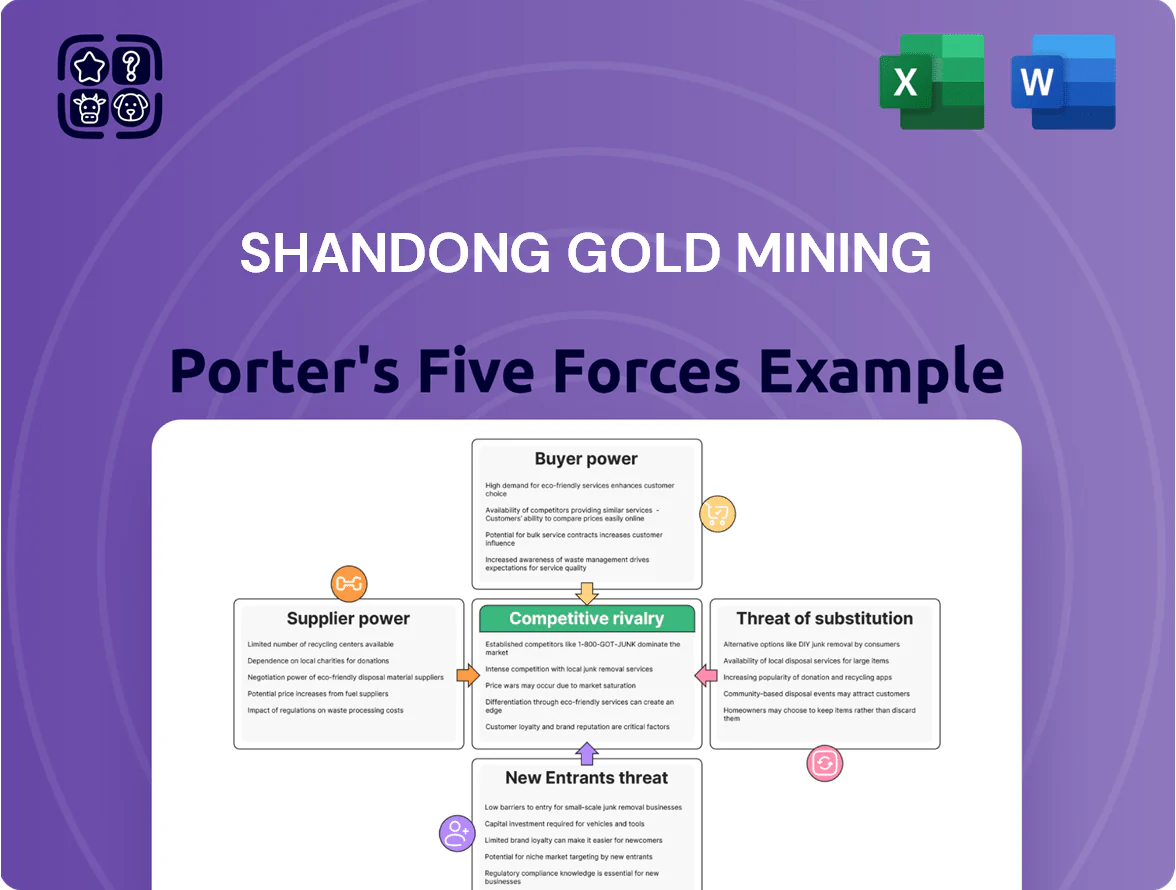

Shandong Gold Mining faces moderate supplier power and high rivalry due to concentrated competitors and cyclical gold prices, while barriers to entry remain significant but technological shifts and ESG demands heighten substitute and buyer scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shandong Gold Mining’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control of Mineral Rights

The Chinese state controls mineral rights and issues exploration and mining licenses, making it the de facto supplier of land access for Shandong Gold; losing or failing permit conditions can halt production. The company must meet strict state environmental and safety standards—noncompliance risks fines or revocation—so regulatory approval is a gating input. In Q4 2025 Beijing tightened green mining rules, raising regulator leverage; 2024–25 permit rejections rose ~22% in major mining provinces, increasing compliance costs.

Specialized Mining Equipment Providers

Shandong Gold relies on a handful of high-tech engineering firms for deep-shaft rigs and AI-driven ore-processing—vendors concentrated among 5–7 global suppliers; in 2024 capex for automation in China’s mining sector rose 18%, boosting demand for these niche systems.

Because smart-mining platforms tie into plant control and IoT analytics, switching costs run high—estimated at 10–25% of project value—so suppliers retain moderate pricing power and can push 5–12% higher margins on upgrades.

Energy and Utility Requirements

Mining and smelting at Shandong Gold consume large electricity and fuel volumes; in 2024 China’s mining sector used ~2,400 TWh and industrial electricity prices averaged ¥0.62/kWh, tying the firm to state grids and oil suppliers.

Energy-price swings and rising carbon costs (China’s national ETS allowance prices rose toward ¥60/ton CO2 in 2024) directly lift per-unit smelting costs, squeezing margins.

State-owned utilities and fuel monopolies dominate regional supply, leaving Shandong Gold with almost no leverage to negotiate lower tariffs or contract terms.

Technical Labor and Expertise

The scarcity of highly skilled mining engineers and geologists for deep-earth extraction gives technical staff strong leverage, pushing Shandong Gold to offer higher pay and benefits.

Domestic supply lags demand as operations shift to complex underground mines; industry surveys in 2024 showed a 22% shortfall in qualified specialists nationally.

Higher compensation raised technical labor costs by an estimated 6–9% of operating expenses in 2024, boosting supplier (labor) bargaining power.

- 22% domestic talent shortfall (2024)

- Technical labor adds ~6–9% to OPEX (2024)

- Specialists demand premium pay, increasing retention costs

Chemical and Processing Inputs

The procurement of cyanide and activated carbon for gold leaching relies on a small set of certified global suppliers; by 2024 roughly 60-70% of industrial sodium cyanide supply was concentrated among five firms, limiting options for Shandong Gold Mining.

Strict transport and hazardous-material rules in China and internationally raise compliance costs and bar smaller vendors, giving suppliers moderate bargaining power since a supply interruption could stop refining.

- 5 firms supply ~60–70% cyanide (2024)

- High compliance costs raise vendor barriers

- Moderate supplier power—disruption halts refining

China mining: rising permit rejections, concentrated suppliers, costly energy & ETS

State controls land/permits—permit rejections up ~22% in 2024–25; tighter green rules since Q4 2025 raise compliance costs. Key tech vendors (5–7 firms) and cyanide suppliers (5 firms hold 60–70% market) create switching costs ~10–25% of project value; suppliers can push 5–12% premium. Energy tied to state grids (2024 price ¥0.62/kWh); China mining used ~2,400 TWh (2024), and ETS ~¥60/ton CO2 (2024).

| Metric | 2024–25 |

|---|---|

| Permit rejections | +22% |

| Tech vendors | 5–7 |

| Cyanide concentration | 60–70% (5 firms) |

| Switching cost | 10–25% project value |

| Energy price | ¥0.62/kWh |

| China mining electricity | ~2,400 TWh |

| ETS price | ~¥60/ton CO2 |

What is included in the product

Tailored Porter's Five Forces for Shandong Gold Mining uncovering competitive intensity, buyer/supplier power, threat of substitutes and entrants, and industry rivalry—highlighting key drivers, emerging threats, and strategic implications for pricing and profitability.

Clear Porter's Five Forces snapshot for Shandong Gold—one-sheet view to quickly assess competitive pressures and strategic levers.

Customers Bargaining Power

Commodity Price Takership

As a producer of a standardized commodity, Shandong Gold cannot set prices; gold trades at global rates set by exchanges like the London Bullion Market and Shanghai Gold Exchange, which determined the 2025 average LBMA gold price near $1,980/oz and SGE premiums that year.

Concentration of the Shanghai Gold Exchange

Central Bank Procurement

The People's Bank of China and other central banks are major institutional buyers whose 2024 gold reserves grew: China added about 80 tonnes in 2024, bringing reserves to ~2,010 tonnes, while global central-bank net purchases hit ~1,100 tonnes in 2024—boosting demand and market liquidity.

These buyers do not negotiate price but their accumulation patterns shape market sentiment and volatility; central-bank buying accounted for roughly 30% of net physical demand in 2024, tightening supply.

Shandong Gold must align production and delivery schedules to multi-month reserve procurement timelines and offer verified provenance and LBMA-compliant bars to secure predictable off-take from these institutional clients.

Industrial and Jewelry Demand

Industrial and jewelry demand—about 45% of global fabricated gold use in 2024—fluctuates with GDP and consumer sentiment, so downturns cut volumes quickly and push buyers to lower-purity alloys.

When spot gold climbed above $2,300/oz in 2024 buyers trimmed orders or shifted alloys, pressuring margins indirectly, but fungibility means they cannot force Shandong Gold to sell below the global spot price.

- ~45% of fabricated gold demand: jewelry + electronics (2024)

- Peak spot: ~$2,300/oz (2024) reduced purchases

- Buyers can reduce volume, not set below-spot prices

Investment Fund Influence

Exchange-traded funds (ETFs) and institutional investors treat gold as a financial asset, trading on rates and FX; ETFs held 3,534 tonnes of gold at end-2024, up 4% year-on-year, amplifying price moves that affect Shandong Gold Mining revenue volatility.

They influence cash flows via market prices rather than direct contracts with the firm, so customer bargaining power is indirect but significant when rate shifts or RMB moves spike volatility.

- ETFs 3,534 t (2024)

- ETFs drive price-led revenue swings

- Impact indirect—market, not contracts

Gold Prices Driven by Central Banks & ETFs; Shandong Gold Faces Compressed Spreads

Customers have low direct bargaining power—gold is a global commodity priced by LBMA/SGE (2025 avg ~$1,980/oz); ~55% of Shandong Gold’s domestic sales flowed via SGE in 2024, compressing spreads. Central banks (China +80t in 2024 to ~2,010t) and ETFs (3,534t end-2024) drive prices and liquidity; buyers can cut volumes but not force below-spot sales.

| Metric | 2024/25 |

|---|---|

| LBMA avg price (2025) | $1,980/oz |

| SGE share of domestic sales | ~55% |

| China reserves | ~2,010t (+80t) |

| ETF holdings | 3,534t |

Same Document Delivered

Shandong Gold Mining Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shandong Gold Mining you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the same fully formatted, professionally written file you'll be able to download and use the moment you buy.

You're viewing the actual deliverable: complete, ready-to-use, and available for instant access upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Shandong Gold Mining faces moderate supplier power and high rivalry due to concentrated competitors and cyclical gold prices, while barriers to entry remain significant but technological shifts and ESG demands heighten substitute and buyer scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shandong Gold Mining’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control of Mineral Rights

The Chinese state controls mineral rights and issues exploration and mining licenses, making it the de facto supplier of land access for Shandong Gold; losing or failing permit conditions can halt production. The company must meet strict state environmental and safety standards—noncompliance risks fines or revocation—so regulatory approval is a gating input. In Q4 2025 Beijing tightened green mining rules, raising regulator leverage; 2024–25 permit rejections rose ~22% in major mining provinces, increasing compliance costs.

Specialized Mining Equipment Providers

Shandong Gold relies on a handful of high-tech engineering firms for deep-shaft rigs and AI-driven ore-processing—vendors concentrated among 5–7 global suppliers; in 2024 capex for automation in China’s mining sector rose 18%, boosting demand for these niche systems.

Because smart-mining platforms tie into plant control and IoT analytics, switching costs run high—estimated at 10–25% of project value—so suppliers retain moderate pricing power and can push 5–12% higher margins on upgrades.

Energy and Utility Requirements

Mining and smelting at Shandong Gold consume large electricity and fuel volumes; in 2024 China’s mining sector used ~2,400 TWh and industrial electricity prices averaged ¥0.62/kWh, tying the firm to state grids and oil suppliers.

Energy-price swings and rising carbon costs (China’s national ETS allowance prices rose toward ¥60/ton CO2 in 2024) directly lift per-unit smelting costs, squeezing margins.

State-owned utilities and fuel monopolies dominate regional supply, leaving Shandong Gold with almost no leverage to negotiate lower tariffs or contract terms.

Technical Labor and Expertise

The scarcity of highly skilled mining engineers and geologists for deep-earth extraction gives technical staff strong leverage, pushing Shandong Gold to offer higher pay and benefits.

Domestic supply lags demand as operations shift to complex underground mines; industry surveys in 2024 showed a 22% shortfall in qualified specialists nationally.

Higher compensation raised technical labor costs by an estimated 6–9% of operating expenses in 2024, boosting supplier (labor) bargaining power.

- 22% domestic talent shortfall (2024)

- Technical labor adds ~6–9% to OPEX (2024)

- Specialists demand premium pay, increasing retention costs

Chemical and Processing Inputs

The procurement of cyanide and activated carbon for gold leaching relies on a small set of certified global suppliers; by 2024 roughly 60-70% of industrial sodium cyanide supply was concentrated among five firms, limiting options for Shandong Gold Mining.

Strict transport and hazardous-material rules in China and internationally raise compliance costs and bar smaller vendors, giving suppliers moderate bargaining power since a supply interruption could stop refining.

- 5 firms supply ~60–70% cyanide (2024)

- High compliance costs raise vendor barriers

- Moderate supplier power—disruption halts refining

China mining: rising permit rejections, concentrated suppliers, costly energy & ETS

State controls land/permits—permit rejections up ~22% in 2024–25; tighter green rules since Q4 2025 raise compliance costs. Key tech vendors (5–7 firms) and cyanide suppliers (5 firms hold 60–70% market) create switching costs ~10–25% of project value; suppliers can push 5–12% premium. Energy tied to state grids (2024 price ¥0.62/kWh); China mining used ~2,400 TWh (2024), and ETS ~¥60/ton CO2 (2024).

| Metric | 2024–25 |

|---|---|

| Permit rejections | +22% |

| Tech vendors | 5–7 |

| Cyanide concentration | 60–70% (5 firms) |

| Switching cost | 10–25% project value |

| Energy price | ¥0.62/kWh |

| China mining electricity | ~2,400 TWh |

| ETS price | ~¥60/ton CO2 |

What is included in the product

Tailored Porter's Five Forces for Shandong Gold Mining uncovering competitive intensity, buyer/supplier power, threat of substitutes and entrants, and industry rivalry—highlighting key drivers, emerging threats, and strategic implications for pricing and profitability.

Clear Porter's Five Forces snapshot for Shandong Gold—one-sheet view to quickly assess competitive pressures and strategic levers.

Customers Bargaining Power

Commodity Price Takership

As a producer of a standardized commodity, Shandong Gold cannot set prices; gold trades at global rates set by exchanges like the London Bullion Market and Shanghai Gold Exchange, which determined the 2025 average LBMA gold price near $1,980/oz and SGE premiums that year.

Concentration of the Shanghai Gold Exchange

Central Bank Procurement

The People's Bank of China and other central banks are major institutional buyers whose 2024 gold reserves grew: China added about 80 tonnes in 2024, bringing reserves to ~2,010 tonnes, while global central-bank net purchases hit ~1,100 tonnes in 2024—boosting demand and market liquidity.

These buyers do not negotiate price but their accumulation patterns shape market sentiment and volatility; central-bank buying accounted for roughly 30% of net physical demand in 2024, tightening supply.

Shandong Gold must align production and delivery schedules to multi-month reserve procurement timelines and offer verified provenance and LBMA-compliant bars to secure predictable off-take from these institutional clients.

Industrial and Jewelry Demand

Industrial and jewelry demand—about 45% of global fabricated gold use in 2024—fluctuates with GDP and consumer sentiment, so downturns cut volumes quickly and push buyers to lower-purity alloys.

When spot gold climbed above $2,300/oz in 2024 buyers trimmed orders or shifted alloys, pressuring margins indirectly, but fungibility means they cannot force Shandong Gold to sell below the global spot price.

- ~45% of fabricated gold demand: jewelry + electronics (2024)

- Peak spot: ~$2,300/oz (2024) reduced purchases

- Buyers can reduce volume, not set below-spot prices

Investment Fund Influence

Exchange-traded funds (ETFs) and institutional investors treat gold as a financial asset, trading on rates and FX; ETFs held 3,534 tonnes of gold at end-2024, up 4% year-on-year, amplifying price moves that affect Shandong Gold Mining revenue volatility.

They influence cash flows via market prices rather than direct contracts with the firm, so customer bargaining power is indirect but significant when rate shifts or RMB moves spike volatility.

- ETFs 3,534 t (2024)

- ETFs drive price-led revenue swings

- Impact indirect—market, not contracts

Gold Prices Driven by Central Banks & ETFs; Shandong Gold Faces Compressed Spreads

Customers have low direct bargaining power—gold is a global commodity priced by LBMA/SGE (2025 avg ~$1,980/oz); ~55% of Shandong Gold’s domestic sales flowed via SGE in 2024, compressing spreads. Central banks (China +80t in 2024 to ~2,010t) and ETFs (3,534t end-2024) drive prices and liquidity; buyers can cut volumes but not force below-spot sales.

| Metric | 2024/25 |

|---|---|

| LBMA avg price (2025) | $1,980/oz |

| SGE share of domestic sales | ~55% |

| China reserves | ~2,010t (+80t) |

| ETF holdings | 3,534t |

Same Document Delivered

Shandong Gold Mining Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shandong Gold Mining you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the same fully formatted, professionally written file you'll be able to download and use the moment you buy.

You're viewing the actual deliverable: complete, ready-to-use, and available for instant access upon payment.