Showa Denko K.K. SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Showa Denko’s diversified materials portfolio and strong R&D position underpin resilient revenue streams, but exposure to cyclic petrochemical markets and raw-material volatility present notable risks; strategic shifts toward high-value electronic materials and battery components could unlock growth if capex and regulatory hurdles are managed.

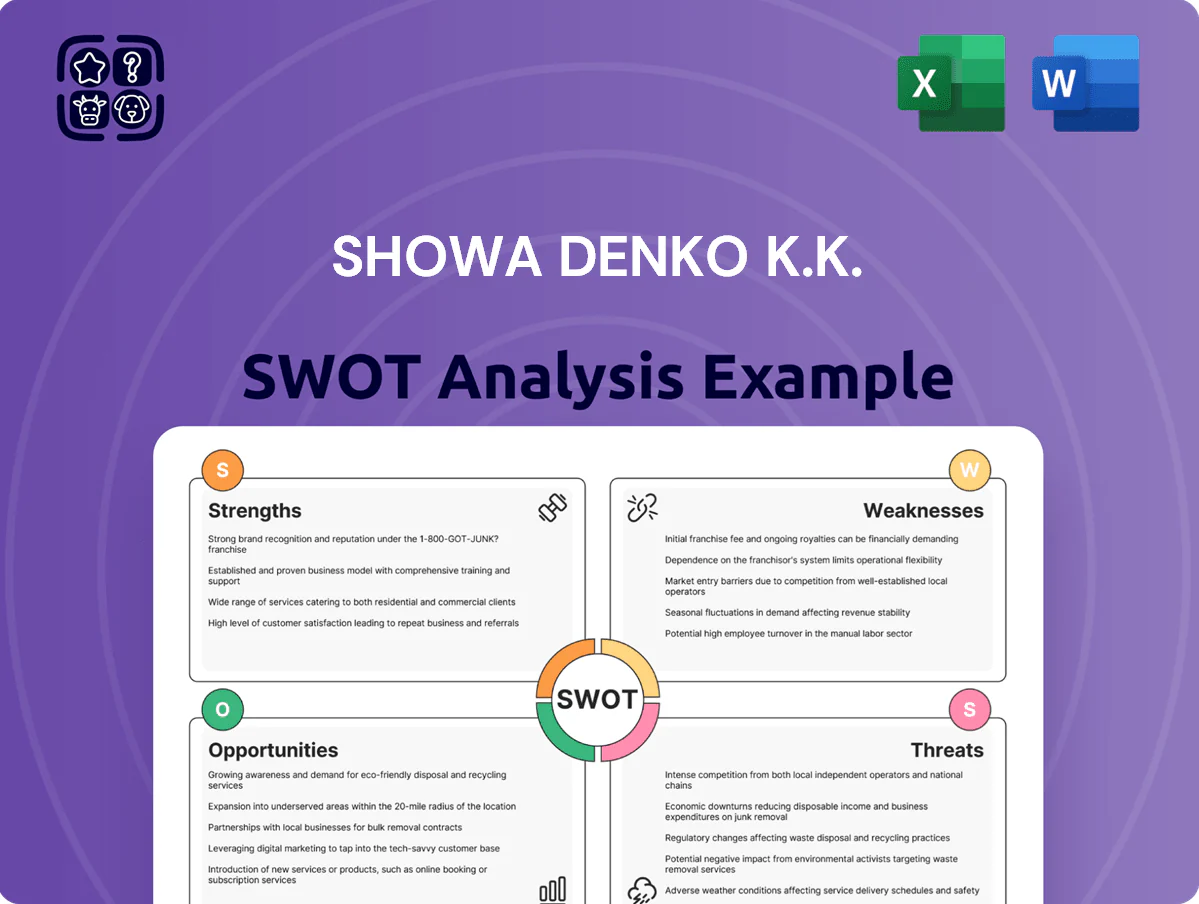

Strengths

Global Leadership in Semiconductor Materials

Resonac (Showa Denko Materials) commands ~30–35% share of the global photoresist and CMP slurry markets as of 2025, driving ¥250–270bn revenue from semiconductor materials in FY2024. The 2023 integration widened its product suite for logic and memory fabs, boosting cross‑sell and R&D scale. Its volume gives strong bargaining power and multi‑year supply contracts with TSMC, Samsung and GlobalFoundries, lowering sales volatility.

Dominant Market Share in Graphite Electrodes

Showa Denko remains a top global producer of graphite electrodes, supplying roughly 18% of global capacity in 2024 and driving ¥74.2bn revenue from carbon products in FY2024 (ended March 2024).

Demand for high-quality electrodes rises with electric-arc-furnace (EAF) steelmaking—EAF share of global crude steel hit ~34% in 2024—boosting Showa Denko’s pricing power and volume growth.

Resonac’s (Showa Denko group) specialized R&D and production scale create a strong moat, keeping gross margins in the carbon segment above 22% in FY2024 versus smaller peers under 15%.

Vertically Integrated SiC Supply Chain

Resonac (Showa Denko K.K.) operates a vertically integrated Silicon Carbide (SiC) epi wafer supply chain—from raw SiC grain to finished wafers—ensuring higher yield and tighter specs; this helped SiC wafer shipments grow ~38% YoY in 2024, supporting revenue resilience (Resonac reported ¥290.5bn consolidated sales FY2024). By owning upstream steps, the firm reduces supply disruptions and meets automaker quality demands as EV power modules shift to SiC, where adoption in new EV models rose to ~22% global penetration in 2024.

Synergistic R and D Capabilities

Showa Denko K.K.'s merger-created R and D platform merges chemical synthesis with advanced material evaluation, enabling rapid prototyping of multilayer materials for modern electronics; R and D spending rose to ¥28.3 billion in FY2024 (up 12% YoY).

This lets the company innovate across both front-end and back-end semiconductor processes — a strategic asset supporting 18% revenue growth in electronics materials in 2024.

- ¥28.3 billion R and D spend FY2024

- 12% R and D YoY increase

- 18% electronics materials revenue growth 2024

Diversified Industrial Portfolio

Showa Denko K.K. holds strong positions beyond electronics—petrochemicals (FY2024 sales ¥260.3bn), aluminum (FY2024 sales ¥142.8bn), and inorganic materials—giving revenue diversification that cut segment volatility: electronics fell 18% in 2024 while petrochemicals rose 6%, buffering group EBITDA (FY2024 ¥89.5bn).

The broad industrial footprint lets the firm apply chemical engineering know-how across sectors—examples include catalyst tech moved from petrochemicals to battery materials, supporting 2024 CAPEX ¥68.4bn and faster product rollout.

- FY2024 sales mix: petrochemicals 28%, aluminum 15%, electronics 40%

- Group EBITDA FY2024 ¥89.5bn; CAPEX ¥68.4bn

- Diversification reduced revenue volatility vs 2023 by ~9% (std dev)

Resonac: Dominant semiconductor materials, strong SiC growth and resilient diversified margins

Resonac's ~30–35% global share in photoresist/CMP and ¥250–270bn semiconductor materials revenue FY2024, 18% carbon gross margin and ¥74.2bn carbon revenue, vertically integrated SiC (38% shipment growth 2024) and ¥28.3bn R&D (12% YoY) drive durable margins and supply security; diversified FY2024 sales (petrochemicals ¥260.3bn, aluminum ¥142.8bn, electronics 40%) cut volatility.

| Metric | Value (FY2024/2024) |

|---|---|

| Photoresist/CMP share | 30–35% |

| Semiconductor materials rev | ¥250–270bn |

| Carbon revenue | ¥74.2bn |

| Carbon gross margin | ~22% |

| SiC shipment growth | +38% YoY |

| R&D spend | ¥28.3bn (+12% YoY) |

| Petrochemicals sales | ¥260.3bn |

| Aluminum sales | ¥142.8bn |

| Group EBITDA | ¥89.5bn |

What is included in the product

Provides a clear SWOT framework for analyzing Showa Denko K.K.’s business strategy, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping future performance.

Provides a concise SWOT matrix tailored to Showa Denko for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Elevated Debt-to-Equity Ratio

The 2019 acquisition of Hitachi Chemical left Showa Denko K.K. with long-term debt of about ¥420 billion (post-consolidation 2024), keeping its debt-to-equity around 1.1x as of FY2024; deleveraging is underway but interest expense near ¥25 billion in 2024 limits free cash flow for new projects.

Cyclical Petrochemical Earnings Volatility

The petrochemical segment faces sharp earnings swings tied to global commodity cycles and naphtha feedstock costs; in 2023 naphtha spot swings of ±25% drove a petrochemical EBITDA drop of about 18% year-on-year for peers, highlighting vulnerability.

Demand volatility for basic chemicals causes uneven margins and unpredictable quarterly profits—Showa Denko reported petrochemical sales volatility contributing to a 2024 operating profit variance of roughly JPY 12–15 billion versus forecasts.

That cyclicality often hides steady specialty-materials growth, where Showa Denko’s high-margin units grew revenue ~6% in 2024, masking petrochemical profit instability.

Integration Complexity Post-Merger

Managing the cultural and operational merger of Showa Denko K.K. and Hitachi Chemical into Resonac has been a complex, multi-year process, with integration-related costs of about ¥40 billion recorded in FY2022 and ongoing synergies targeted through 2025.

Internal restructuring has caused temporary inefficiencies and a reported 3–5% drop in segment EBITDA margins in 2023, and the company disclosed voluntary departures of several senior engineers during 2022–24, risking loss of key talent.

Ensuring a unified corporate strategy across diverse units—chemicals, electronics materials, and specialty products—remains a major management challenge as Resonac seeks to hit its ¥100 billion synergy target by 2025 while aligning R&D roadmaps and sales channels.

High Dependency on Japanese Manufacturing

A large portion of Showa Denko K.K.’s manufacturing and supply chain stays concentrated in Japan—about 60–70% of installed capacity for key chemicals and advanced materials as of FY2024—raising exposure to domestic economic stagnation and higher labor/energy costs versus Southeast Asia.

This concentration heightens operational risk: local logistics snags or earthquakes in the Japanese archipelago can halt critical lines, and FY2024 yen-linked cost pressures trimmed operating margin by ~1.2 percentage points.

- ~60–70% capacity in Japan (FY2024)

- Higher unit costs vs low-cost regions

- Increased earthquake/logistics disruption risk

- FY2024 operating margin down ~1.2 pp from yen cost pressures

Margin Pressure in Commodity Segments

- Specialty EBITDA >15%

- Commodity margins <5%

- Commodities ≈40% revenue

- Price cuts by rivals 10–20% YoY

- Asset optimization target ¥50–70bn (2025)

High debt, commodity exposure and integration costs cloud Hitachi Chemical merger upside

High post-Hitachi Chemical debt (~¥420bn post-consolidation, D/E ~1.1x FY2024) and ~¥25bn interest cost cut free cash flow; petrochemical/commodity margins (<5%) drive volatility (commodities ≈40% revenue) while specialty EBITDA >15% masks risk; ~60–70% capacity in Japan raises disruption and cost exposure; integration costs ~¥40bn and asset-sale target ¥50–70bn (2025).

| Metric | Value |

|---|---|

| Net debt | ¥420bn |

| D/E | 1.1x (FY2024) |

| Interest | ¥25bn (2024) |

| Japan capacity | 60–70% |

| Commodities rev | ≈40% |

| Asset target | ¥50–70bn (2025) |

Preview Before You Purchase

Showa Denko K.K. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version and the complete analysis file becomes available immediately after checkout. Buy now to access the full, detailed report.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Showa Denko’s diversified materials portfolio and strong R&D position underpin resilient revenue streams, but exposure to cyclic petrochemical markets and raw-material volatility present notable risks; strategic shifts toward high-value electronic materials and battery components could unlock growth if capex and regulatory hurdles are managed.

Strengths

Global Leadership in Semiconductor Materials

Resonac (Showa Denko Materials) commands ~30–35% share of the global photoresist and CMP slurry markets as of 2025, driving ¥250–270bn revenue from semiconductor materials in FY2024. The 2023 integration widened its product suite for logic and memory fabs, boosting cross‑sell and R&D scale. Its volume gives strong bargaining power and multi‑year supply contracts with TSMC, Samsung and GlobalFoundries, lowering sales volatility.

Dominant Market Share in Graphite Electrodes

Showa Denko remains a top global producer of graphite electrodes, supplying roughly 18% of global capacity in 2024 and driving ¥74.2bn revenue from carbon products in FY2024 (ended March 2024).

Demand for high-quality electrodes rises with electric-arc-furnace (EAF) steelmaking—EAF share of global crude steel hit ~34% in 2024—boosting Showa Denko’s pricing power and volume growth.

Resonac’s (Showa Denko group) specialized R&D and production scale create a strong moat, keeping gross margins in the carbon segment above 22% in FY2024 versus smaller peers under 15%.

Vertically Integrated SiC Supply Chain

Resonac (Showa Denko K.K.) operates a vertically integrated Silicon Carbide (SiC) epi wafer supply chain—from raw SiC grain to finished wafers—ensuring higher yield and tighter specs; this helped SiC wafer shipments grow ~38% YoY in 2024, supporting revenue resilience (Resonac reported ¥290.5bn consolidated sales FY2024). By owning upstream steps, the firm reduces supply disruptions and meets automaker quality demands as EV power modules shift to SiC, where adoption in new EV models rose to ~22% global penetration in 2024.

Synergistic R and D Capabilities

Showa Denko K.K.'s merger-created R and D platform merges chemical synthesis with advanced material evaluation, enabling rapid prototyping of multilayer materials for modern electronics; R and D spending rose to ¥28.3 billion in FY2024 (up 12% YoY).

This lets the company innovate across both front-end and back-end semiconductor processes — a strategic asset supporting 18% revenue growth in electronics materials in 2024.

- ¥28.3 billion R and D spend FY2024

- 12% R and D YoY increase

- 18% electronics materials revenue growth 2024

Diversified Industrial Portfolio

Showa Denko K.K. holds strong positions beyond electronics—petrochemicals (FY2024 sales ¥260.3bn), aluminum (FY2024 sales ¥142.8bn), and inorganic materials—giving revenue diversification that cut segment volatility: electronics fell 18% in 2024 while petrochemicals rose 6%, buffering group EBITDA (FY2024 ¥89.5bn).

The broad industrial footprint lets the firm apply chemical engineering know-how across sectors—examples include catalyst tech moved from petrochemicals to battery materials, supporting 2024 CAPEX ¥68.4bn and faster product rollout.

- FY2024 sales mix: petrochemicals 28%, aluminum 15%, electronics 40%

- Group EBITDA FY2024 ¥89.5bn; CAPEX ¥68.4bn

- Diversification reduced revenue volatility vs 2023 by ~9% (std dev)

Resonac: Dominant semiconductor materials, strong SiC growth and resilient diversified margins

Resonac's ~30–35% global share in photoresist/CMP and ¥250–270bn semiconductor materials revenue FY2024, 18% carbon gross margin and ¥74.2bn carbon revenue, vertically integrated SiC (38% shipment growth 2024) and ¥28.3bn R&D (12% YoY) drive durable margins and supply security; diversified FY2024 sales (petrochemicals ¥260.3bn, aluminum ¥142.8bn, electronics 40%) cut volatility.

| Metric | Value (FY2024/2024) |

|---|---|

| Photoresist/CMP share | 30–35% |

| Semiconductor materials rev | ¥250–270bn |

| Carbon revenue | ¥74.2bn |

| Carbon gross margin | ~22% |

| SiC shipment growth | +38% YoY |

| R&D spend | ¥28.3bn (+12% YoY) |

| Petrochemicals sales | ¥260.3bn |

| Aluminum sales | ¥142.8bn |

| Group EBITDA | ¥89.5bn |

What is included in the product

Provides a clear SWOT framework for analyzing Showa Denko K.K.’s business strategy, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping future performance.

Provides a concise SWOT matrix tailored to Showa Denko for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Elevated Debt-to-Equity Ratio

The 2019 acquisition of Hitachi Chemical left Showa Denko K.K. with long-term debt of about ¥420 billion (post-consolidation 2024), keeping its debt-to-equity around 1.1x as of FY2024; deleveraging is underway but interest expense near ¥25 billion in 2024 limits free cash flow for new projects.

Cyclical Petrochemical Earnings Volatility

The petrochemical segment faces sharp earnings swings tied to global commodity cycles and naphtha feedstock costs; in 2023 naphtha spot swings of ±25% drove a petrochemical EBITDA drop of about 18% year-on-year for peers, highlighting vulnerability.

Demand volatility for basic chemicals causes uneven margins and unpredictable quarterly profits—Showa Denko reported petrochemical sales volatility contributing to a 2024 operating profit variance of roughly JPY 12–15 billion versus forecasts.

That cyclicality often hides steady specialty-materials growth, where Showa Denko’s high-margin units grew revenue ~6% in 2024, masking petrochemical profit instability.

Integration Complexity Post-Merger

Managing the cultural and operational merger of Showa Denko K.K. and Hitachi Chemical into Resonac has been a complex, multi-year process, with integration-related costs of about ¥40 billion recorded in FY2022 and ongoing synergies targeted through 2025.

Internal restructuring has caused temporary inefficiencies and a reported 3–5% drop in segment EBITDA margins in 2023, and the company disclosed voluntary departures of several senior engineers during 2022–24, risking loss of key talent.

Ensuring a unified corporate strategy across diverse units—chemicals, electronics materials, and specialty products—remains a major management challenge as Resonac seeks to hit its ¥100 billion synergy target by 2025 while aligning R&D roadmaps and sales channels.

High Dependency on Japanese Manufacturing

A large portion of Showa Denko K.K.’s manufacturing and supply chain stays concentrated in Japan—about 60–70% of installed capacity for key chemicals and advanced materials as of FY2024—raising exposure to domestic economic stagnation and higher labor/energy costs versus Southeast Asia.

This concentration heightens operational risk: local logistics snags or earthquakes in the Japanese archipelago can halt critical lines, and FY2024 yen-linked cost pressures trimmed operating margin by ~1.2 percentage points.

- ~60–70% capacity in Japan (FY2024)

- Higher unit costs vs low-cost regions

- Increased earthquake/logistics disruption risk

- FY2024 operating margin down ~1.2 pp from yen cost pressures

Margin Pressure in Commodity Segments

- Specialty EBITDA >15%

- Commodity margins <5%

- Commodities ≈40% revenue

- Price cuts by rivals 10–20% YoY

- Asset optimization target ¥50–70bn (2025)

High debt, commodity exposure and integration costs cloud Hitachi Chemical merger upside

High post-Hitachi Chemical debt (~¥420bn post-consolidation, D/E ~1.1x FY2024) and ~¥25bn interest cost cut free cash flow; petrochemical/commodity margins (<5%) drive volatility (commodities ≈40% revenue) while specialty EBITDA >15% masks risk; ~60–70% capacity in Japan raises disruption and cost exposure; integration costs ~¥40bn and asset-sale target ¥50–70bn (2025).

| Metric | Value |

|---|---|

| Net debt | ¥420bn |

| D/E | 1.1x (FY2024) |

| Interest | ¥25bn (2024) |

| Japan capacity | 60–70% |

| Commodities rev | ≈40% |

| Asset target | ¥50–70bn (2025) |

Preview Before You Purchase

Showa Denko K.K. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version and the complete analysis file becomes available immediately after checkout. Buy now to access the full, detailed report.