Sea Porter's Five Forces Analysis

Don't Miss the Bigger Picture

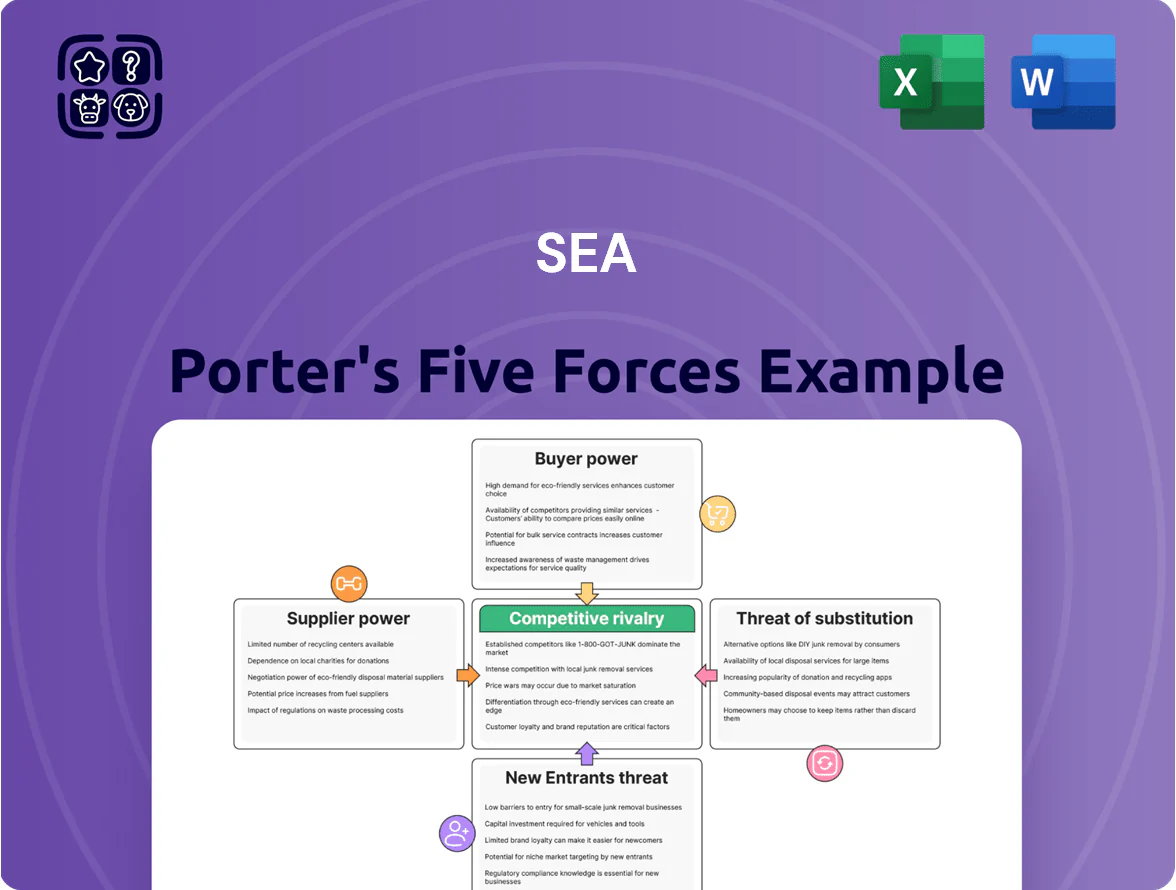

Sea faces intense competitive rivalry and shifting buyer preferences that pressure margins, while supplier leverage and regulatory hurdles temper strategic flexibility—this snapshot highlights key tensions shaping its outlook.

The full Porter's Five Forces Analysis uncovers force-by-force ratings, visualizations, and tactical implications to clarify where Sea can defend or expand its market position.

Ready for a consultant-grade, data-driven report you can use in pitches or strategy? Unlock the complete analysis for actionable insights.

Suppliers Bargaining Power

Dependency on Cloud Infrastructure Providers

Sea Limited depends on AWS and Google Cloud for its digital stack, creating high supplier power: estimated cloud spend exceeded $500m in 2024 and migration costs plus custom integrations make switching costly. Any price increase or outage from these providers could cut margins (Shopee/SeaMoney and Garena uptime) and hurt transaction volumes; a 1% cloud price rise might shave several tens of millions off operating profit.

Reliance on External Game Intellectual Property

Garena (Sea Ltd) builds titles like Free Fire but also distributes external IPs from giants such as Tencent, giving those owners high leverage over revenue-share deals and license renewals.

If Tencent or another major developer withdraws a top title or pushes royalties up 5–15%, Garena digital-entertainment revenue—39% of Sea’s 2024 revenue—would face sharp margin and growth pressure.

Logistics and Last-Mile Delivery Partners

Shopee relies on a vast network of third-party logistics (3PL) partners to reach 650m+ consumers across Southeast Asia and Latin America; in 2024 Sea Group reported fulfillment partnerships handled the majority of orders while Shopee Xpress expanded own fleet to 30% of volume in key markets.

Dependence on external couriers during peak seasons remains a vulnerability: 3PLs can raise rates where road and warehousing infrastructure is weak—last-mile costs in Vietnam and the Philippines run 20–40% higher than urban Singapore, squeezing margins.

Financial Institutions and Payment Networks

SeaMoney must integrate with global networks like Visa and Mastercard and dozens of local banks to process payments; in 2024 card rails handled $36 trillion globally and set fees SeaMoney pays per transaction (0.2–2.5% typical ranges).

These institutions also enforce KYC/AML rules and licensing; by 2025 tighter digital finance rules (eg, EU Digital Operational Resilience Act, expanded AML regimes) raise compliance costs and slow product rollout.

Control of payment rails and licenses gives suppliers bargaining power over pricing, settlement speed, and access to new markets, so SeaMoney faces concentrated supplier leverage.

- Global card volume: $36T (2024)

- Typical fees: 0.2–2.5% per txn

- 2025: tighter AML/KYC and DORA-style rules

- Supplier leverage: pricing, settlement, licensing

Specialized Technical Talent Acquisition

The supply of senior software engineers and data scientists in Southeast Asia is tight versus demand from tech hubs; market salary premiums rose ~12–18% in 2024 in Singapore and Indonesia, keeping talent scarce.

Sea Limited competes with global firms and local unicorns for these hires, raising turnover risk and extending hiring timelines to >60 days for senior roles.

That gives skilled staff strong bargaining power, pushing up personnel costs and equity-based comp; Sea reported R&D and G&A payroll-related expenses up ~22% year-over-year in FY2024.

- Talent scarcity: senior hires >60 days

- Salary premium: +12–18% (2024)

- Comp pressure: payroll costs +22% YoY (FY2024)

Rising Supplier Power: Cloud, IP, 3PLs, Payments & Talent Squeeze Margins

Suppliers hold high leverage: cloud providers (>$500m cloud spend 2024) and game IP owners can raise costs or withdraw titles; 3PLs push last‑mile fees 20–40% higher in weaker markets; payment rails (global card volume $36T in 2024) charge 0.2–2.5% fees and tighter AML/DORA rules raise compliance costs; talent scarcity lifted salaries 12–18% (2024), extending senior hire time >60 days.

| Supplier | Key metric |

|---|---|

| Cloud | >$500m (2024) |

| Game IP | 39% revenue exposure |

| 3PL | +20–40% last‑mile cost |

| Payments | $36T global volume; 0.2–2.5% fees |

| Talent | +12–18% salary; >60 days hires |

What is included in the product

Concise Five Forces assessment tailored to Sea, revealing competitive intensity, buyer and supplier leverage, entry barriers, substitute threats, and strategic levers to protect or expand market share—all editable for integration into reports or pitch decks.

Compact Five Forces summary tailored for Sea Porters—quickly spot competitive pressures and actionable levers to reduce risk and enhance margins.

Customers Bargaining Power

Low Switching Costs for E-commerce Shoppers

Shoppers on Shopee can switch to Lazada or TikTok Shop with almost no friction, and SEA price sensitivity is high: 2024 Nielsen data shows 68% of SEA shoppers prioritize discounts and vouchers.

That behavior pushed Sea Limited (SE US) to spend $4.1B on e-commerce subsidies and marketing in 2024 to protect GMV and active buyers, keeping CAC and promo intensity elevated.

High Price Sensitivity in Emerging Markets

Gamer Engagement and Discretionary Spending

Garena faces high customer bargaining power: its users choose among many free-to-play rivals, so spending on skins and passes is fully discretionary and can drop fast if content quality slips. In 2024 Garena reported 670 million MAUs across Garena titles, yet players churned faster during slow update cycles—a 15% quarterly revenue dip for under-maintained titles in 2023. Frequent live ops and new modes must sustain engagement to protect ARPU and retention.

Merchant Dependence on Platform Traffic

Thousands of SMEs on Shopee depend on platform traffic—Shopee had ~2.6 billion visits monthly in 2024—so Sea (Sea Ltd., SE) can push commission and ad rates without immediate merchant exit.

Still, rising returns on social commerce (e.g., TikTok Shop grew to ~$20B GMV in 2024) let sellers diversify, cutting Shopee's leverage if churn rises.

- Shopee ~2.6B monthly visits (2024)

- Sea can raise commissions/ads

- TikTok Shop GMV ~$20B (2024)

- Merchant diversification reduces long-term leverage

Digital Wallet User Loyalty and Incentives

SeaMoney users pick the wallet mainly for Shopee integration and cashback; in 2024 Shopee reported over 800 million GMV users, driving SeaMoney adoption.

As fintech choice widens—global e-wallets grew ~18% YoY in 2024—loyalty falls unless firms offer ongoing rewards, so Sea must keep incentives to hold users.

This forces Sea into a retention spend cycle: continuous promo costs versus revenue per active user (SeaMoney ARPU was modest vs peers in 2024).

- Integration with Shopee drives core adoption.

- 2024 e-wallet growth ~18% YoY, lowering stickiness.

- Continuous cashback/rewards needed to prevent churn.

- Retention spend trades off with SeaMoney ARPU pressure.

Discount‑driven SEA shoppers force relentless promo spend—Shopee $4.1B, >60% promo orders

Customers have high bargaining power: 68% of SEA shoppers prioritize discounts (Nielsen 2024), Shopee spent $4.1B on e‑commerce subsidies in 2024, and >60% of Shopee orders occur during promotions, limiting take‑rate increases and forcing persistent CAC/promo spend.

| Metric | 2024 |

|---|---|

| SEA shoppers prioritizing discounts | 68% |

| Shopee promo orders | >60% |

| Shopee promo/subsidy spend | $4.1B |

| TikTok Shop GMV | $20B |

Full Version Awaits

Sea Porter's Five Forces Analysis

This preview shows the exact Sea Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this exact document. No mockups or samples—the deliverable you see is precisely what you’ll be able to download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Sea faces intense competitive rivalry and shifting buyer preferences that pressure margins, while supplier leverage and regulatory hurdles temper strategic flexibility—this snapshot highlights key tensions shaping its outlook.

The full Porter's Five Forces Analysis uncovers force-by-force ratings, visualizations, and tactical implications to clarify where Sea can defend or expand its market position.

Ready for a consultant-grade, data-driven report you can use in pitches or strategy? Unlock the complete analysis for actionable insights.

Suppliers Bargaining Power

Dependency on Cloud Infrastructure Providers

Sea Limited depends on AWS and Google Cloud for its digital stack, creating high supplier power: estimated cloud spend exceeded $500m in 2024 and migration costs plus custom integrations make switching costly. Any price increase or outage from these providers could cut margins (Shopee/SeaMoney and Garena uptime) and hurt transaction volumes; a 1% cloud price rise might shave several tens of millions off operating profit.

Reliance on External Game Intellectual Property

Garena (Sea Ltd) builds titles like Free Fire but also distributes external IPs from giants such as Tencent, giving those owners high leverage over revenue-share deals and license renewals.

If Tencent or another major developer withdraws a top title or pushes royalties up 5–15%, Garena digital-entertainment revenue—39% of Sea’s 2024 revenue—would face sharp margin and growth pressure.

Logistics and Last-Mile Delivery Partners

Shopee relies on a vast network of third-party logistics (3PL) partners to reach 650m+ consumers across Southeast Asia and Latin America; in 2024 Sea Group reported fulfillment partnerships handled the majority of orders while Shopee Xpress expanded own fleet to 30% of volume in key markets.

Dependence on external couriers during peak seasons remains a vulnerability: 3PLs can raise rates where road and warehousing infrastructure is weak—last-mile costs in Vietnam and the Philippines run 20–40% higher than urban Singapore, squeezing margins.

Financial Institutions and Payment Networks

SeaMoney must integrate with global networks like Visa and Mastercard and dozens of local banks to process payments; in 2024 card rails handled $36 trillion globally and set fees SeaMoney pays per transaction (0.2–2.5% typical ranges).

These institutions also enforce KYC/AML rules and licensing; by 2025 tighter digital finance rules (eg, EU Digital Operational Resilience Act, expanded AML regimes) raise compliance costs and slow product rollout.

Control of payment rails and licenses gives suppliers bargaining power over pricing, settlement speed, and access to new markets, so SeaMoney faces concentrated supplier leverage.

- Global card volume: $36T (2024)

- Typical fees: 0.2–2.5% per txn

- 2025: tighter AML/KYC and DORA-style rules

- Supplier leverage: pricing, settlement, licensing

Specialized Technical Talent Acquisition

The supply of senior software engineers and data scientists in Southeast Asia is tight versus demand from tech hubs; market salary premiums rose ~12–18% in 2024 in Singapore and Indonesia, keeping talent scarce.

Sea Limited competes with global firms and local unicorns for these hires, raising turnover risk and extending hiring timelines to >60 days for senior roles.

That gives skilled staff strong bargaining power, pushing up personnel costs and equity-based comp; Sea reported R&D and G&A payroll-related expenses up ~22% year-over-year in FY2024.

- Talent scarcity: senior hires >60 days

- Salary premium: +12–18% (2024)

- Comp pressure: payroll costs +22% YoY (FY2024)

Rising Supplier Power: Cloud, IP, 3PLs, Payments & Talent Squeeze Margins

Suppliers hold high leverage: cloud providers (>$500m cloud spend 2024) and game IP owners can raise costs or withdraw titles; 3PLs push last‑mile fees 20–40% higher in weaker markets; payment rails (global card volume $36T in 2024) charge 0.2–2.5% fees and tighter AML/DORA rules raise compliance costs; talent scarcity lifted salaries 12–18% (2024), extending senior hire time >60 days.

| Supplier | Key metric |

|---|---|

| Cloud | >$500m (2024) |

| Game IP | 39% revenue exposure |

| 3PL | +20–40% last‑mile cost |

| Payments | $36T global volume; 0.2–2.5% fees |

| Talent | +12–18% salary; >60 days hires |

What is included in the product

Concise Five Forces assessment tailored to Sea, revealing competitive intensity, buyer and supplier leverage, entry barriers, substitute threats, and strategic levers to protect or expand market share—all editable for integration into reports or pitch decks.

Compact Five Forces summary tailored for Sea Porters—quickly spot competitive pressures and actionable levers to reduce risk and enhance margins.

Customers Bargaining Power

Low Switching Costs for E-commerce Shoppers

Shoppers on Shopee can switch to Lazada or TikTok Shop with almost no friction, and SEA price sensitivity is high: 2024 Nielsen data shows 68% of SEA shoppers prioritize discounts and vouchers.

That behavior pushed Sea Limited (SE US) to spend $4.1B on e-commerce subsidies and marketing in 2024 to protect GMV and active buyers, keeping CAC and promo intensity elevated.

High Price Sensitivity in Emerging Markets

Gamer Engagement and Discretionary Spending

Garena faces high customer bargaining power: its users choose among many free-to-play rivals, so spending on skins and passes is fully discretionary and can drop fast if content quality slips. In 2024 Garena reported 670 million MAUs across Garena titles, yet players churned faster during slow update cycles—a 15% quarterly revenue dip for under-maintained titles in 2023. Frequent live ops and new modes must sustain engagement to protect ARPU and retention.

Merchant Dependence on Platform Traffic

Thousands of SMEs on Shopee depend on platform traffic—Shopee had ~2.6 billion visits monthly in 2024—so Sea (Sea Ltd., SE) can push commission and ad rates without immediate merchant exit.

Still, rising returns on social commerce (e.g., TikTok Shop grew to ~$20B GMV in 2024) let sellers diversify, cutting Shopee's leverage if churn rises.

- Shopee ~2.6B monthly visits (2024)

- Sea can raise commissions/ads

- TikTok Shop GMV ~$20B (2024)

- Merchant diversification reduces long-term leverage

Digital Wallet User Loyalty and Incentives

SeaMoney users pick the wallet mainly for Shopee integration and cashback; in 2024 Shopee reported over 800 million GMV users, driving SeaMoney adoption.

As fintech choice widens—global e-wallets grew ~18% YoY in 2024—loyalty falls unless firms offer ongoing rewards, so Sea must keep incentives to hold users.

This forces Sea into a retention spend cycle: continuous promo costs versus revenue per active user (SeaMoney ARPU was modest vs peers in 2024).

- Integration with Shopee drives core adoption.

- 2024 e-wallet growth ~18% YoY, lowering stickiness.

- Continuous cashback/rewards needed to prevent churn.

- Retention spend trades off with SeaMoney ARPU pressure.

Discount‑driven SEA shoppers force relentless promo spend—Shopee $4.1B, >60% promo orders

Customers have high bargaining power: 68% of SEA shoppers prioritize discounts (Nielsen 2024), Shopee spent $4.1B on e‑commerce subsidies in 2024, and >60% of Shopee orders occur during promotions, limiting take‑rate increases and forcing persistent CAC/promo spend.

| Metric | 2024 |

|---|---|

| SEA shoppers prioritizing discounts | 68% |

| Shopee promo orders | >60% |

| Shopee promo/subsidy spend | $4.1B |

| TikTok Shop GMV | $20B |

Full Version Awaits

Sea Porter's Five Forces Analysis

This preview shows the exact Sea Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this exact document. No mockups or samples—the deliverable you see is precisely what you’ll be able to download after payment.