Seaboard Boston Consulting Group Matrix

Actionable Strategy Starts Here

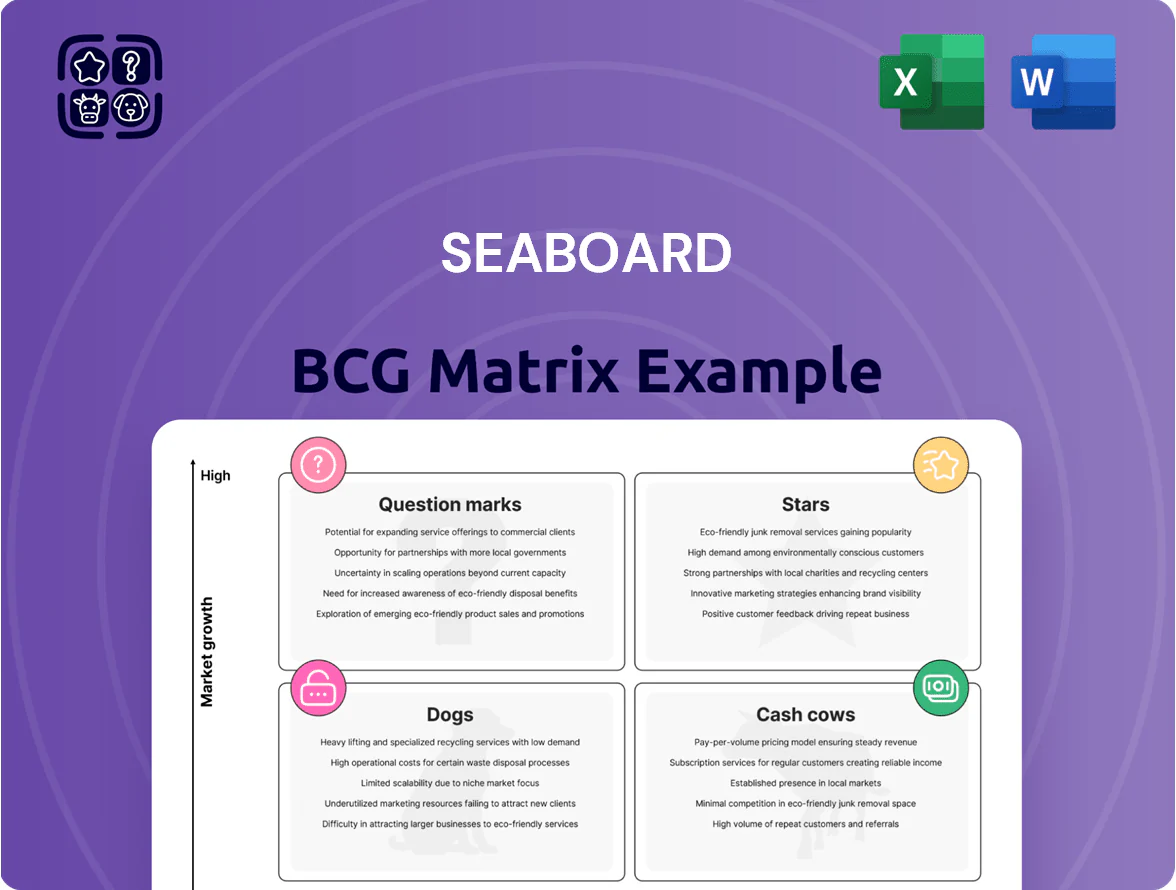

Seaboard’s BCG Matrix preview highlights where its diversified businesses might sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash allocation challenges in one snapshot. This concise view hints at strategic priorities but leaves the granular data and tailored moves untapped. Purchase the full BCG Matrix report for quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word/Excel files to guide investment and resource decisions with confidence.

Stars

Renewable Diesel Expansion

Seaboard has pivoted to renewable diesel by converting animal fats and waste oils into biofuel, leveraging vertical integration in pork to secure feedstock and cutting feedstock costs by an estimated 15–20% versus spot markets in 2025.

Global decarbonization mandates and subsidies—including U.S. Blender Tax Credit through 2025—support high sector growth, with renewable diesel demand forecasted to grow ~7–9% CAGR to 2030.

Scaling requires heavy capex—Seaboard outlined roughly $150–250 million per new refinery-scale unit—but projected margins and rising diesel replacement volumes position this as a primary future revenue engine.

Sub-Saharan African Milling Operations

Seaboard’s Sub-Saharan African milling operations are a Star in the BCG Matrix, driven by 4.5% annual regional urbanization and a 2.7% population CAGR to 2050, fueling rising demand for processed grains and flour.

Seaboard holds a leading market share in West Africa after $85m of local infrastructure investment since 2020, outspending smaller rivals on mills, storage, and port links.

The unit posted ~12% annual revenue growth in 2024 and needs continued logistics capex—estimated $15–20m/yr—to sustain supply chains and remain a top-tier international growth driver.

Value-Added Pork Exports

Seaboard’s shift into value-added pork for premium markets like Japan and South Korea targets 10–15% higher ASPs (average selling prices) than commodity pork; value-added sales grew ~12% CAGR 2019–2024, now ~18% of Seaboard’s protein revenue in 2024.

Precision Ag-Tech Integration

Seaboard is investing heavily in precision ag-tech—data analytics and automation—to boost crop yields and livestock health; pilots across 120,000 hectares and 350,000 pigs showed yield uplifts of 12% and feed conversion improvements of 8% in 2025, supporting long-term margin gains.

These high-growth initiatives sit in the Stars quadrant: they consume cash now—capital spend of $280M in 2024–25—but are essential to retain a tech-driven competitive edge and cut waste 15% company-wide.

- 120,000 hectares in pilots

- 12% crop yield uplift (2025)

- 8% feed conversion improvement

- $280M capex 2024–25

- 15% waste reduction target

High-Efficiency Marine Logistics

Seaboard’s Marine segment upgraded to eco-friendly vessels, cutting CO2 per TEU by ~18% after 2024 retrofits and meeting IMO 2023 fuel standards; this positions the unit as a high-growth Star in sustainable ocean transport.

Stricter international rules plus specialized Caribbean and Central America routes (40% regional market share vs. global carriers’ 10–15%) create above-market volume growth and pricing power.

Sustained capex of ~$85m–$110m/year for port automation and fleet renewal is needed to keep margins and convert the Star into a cash cow within 3–5 years.

- Eco retrofit: −18% CO2/TEU

- Regional share: ~40%

- Capex need: $85m–$110m/yr

- Conversion horizon: 3–5 years

Seaboard’s growth engines: 12% revenue lift, $280M capex, targets big margin gains

Seaboard’s Stars (renewable diesel, Sub‑Saharan milling, value‑added pork, marine) drove 12% revenue growth in 2024, required $280M capex 2024–25, and target margin lift via 15% waste cut; renewable diesel capex ~$150–250M/unit; milling needs $15–20M/yr logistics spend; marine capex $85–110M/yr to convert to cash cow in 3–5 years.

| Unit | 2024–25 capex | Key metric |

|---|---|---|

| Renewable diesel | $150–250M/unit | 7–9% CAGR demand |

| Sub‑Saharan milling | $15–20M/yr | 12% rev growth (2024) |

| Value‑added pork | — | 10–15% higher ASPs |

| Marine | $85–110M/yr | −18% CO2/TEU |

What is included in the product

Comprehensive BCG Matrix review of Seaboard’s units with strategic guidance on stars, cash cows, question marks, and divestment priorities.

One-page Seaboard BCG Matrix mapping each business unit to a quadrant for instant strategic clarity.

Cash Cows

Integrated Pork Production

Seaboard Foods holds a top US pork position via vertical integration—hog production to processing—generating stable cash flow: in 2024 the agri-protein segment drove roughly $1.8B EV/EBITDA-equivalent free cash flow contribution, funding dividends and debt service.

As a mature industry, pork needs mainly maintenance capital; Seaboard reported ~3–4% capex-to-revenue for processing in 2024, so focus stays on operational excellence and cost containment, not domestic expansion.

Global Grain Merchandising

Seaboard’s Global Grain Merchandising is a market-leading cash cow, generating roughly $1.2–1.5 billion in annual gross merchandised volume with mid-single-digit revenue growth in 2024 and EBITDA margins near 6–8% due to scale and execution.

The segment leverages a global sourcing/distribution network across 30+ countries and low marketing spend, converting working capital efficiently—days payable outstanding often >60—so it funds group capex and dividends.

Butterball Turkey Joint Venture

Seaboard’s 50% stake in Butterball delivers roughly half of Butterball’s equity income—Butterball reported $1.2 billion in 2024 US retail turkey sales, so Seaboard’s share supports stable earnings and added ~$50–70 million annual equity income range in recent years.

The US turkey market is mature with steady demand and seasonal peaks (Thanksgiving/Christmas account for ~60% of annual volume), keeping margins predictable and lowering sales volatility for Seaboard.

Butterball’s leading market share (roughly 30–35% retail) sustains consistent profitability without major capex; Butterball’s capex intensity remains below 3% of sales, so Seaboard avoids big facility spending.

This JV acts as a cash cow stabilizer for Seaboard’s consolidated cash flow and helped limit 2024 operating earnings variance to single digits year-over-year.

Argentine Sugar and Alcohol Operations

The Tabacal sugar and industrial alcohol unit in Argentina is a mature, consolidated cash cow for Seaboard, delivering high margins despite a slow-growing regional market; in 2024 it generated approx. $85–95m EBITDA, supporting South America liquidity needs.

Seaboard keeps margins by maximizing extraction yields (cane-to-sugar efficiency ~11–13%) and optimizing ~45,000 hectares of land, funding regional projects without heavy capex.

- 2024 EBITDA ~ $85–95m

- Cane-to-sugar yield ~11–13%

- Land base ~45,000 ha

- Funds regional projects, low incremental capex

Caribbean Marine Trade Routes

Seaboard Marine dominates specialized US–Caribbean routes with an estimated 25–30% market share on key lanes, benefiting from high port-infrastructure barriers and steady cargo volumes (~1.2–1.5 million TEUs/year regionally in 2024).

As a mature market, the focus is on maximizing vessel utilization (target >90%) and service frequency; cashflows fund fleet upgrades—Seaboard invested ~$120m in vessels/retrofits in 2024—and cross-subsidize parent Seaboard Corp activities.

- Market share: 25–30% on core lanes

- Regional volume: ~1.2–1.5M TEUs (2024)

- Vessel utilization target: >90%

- Capex 2024: ~$120m for fleet modernization

Seaboard’s cash cows drove stable 2024 FCF — Foods $1.8B, diversified EBITDA & strong volumes

Seaboard’s cash cows—Seaboard Foods (pork), Global Grain Merchandising, 50% Butterball JV, Tabacal sugar/alcohol, and Seaboard Marine—generated stable free cash flow in 2024, funding dividends and ~$120m capex; key metrics: Foods FCF equiv ~$1.8B, Grain GMV $1.2–1.5B (EBITDA 6–8%), Butterball equity income ~$50–70m, Tabacal EBITDA $85–95m, Marine TEUs 1.2–1.5M.

| Segment | 2024 Key metric |

|---|---|

| Seaboard Foods | FCF equiv ~$1.8B |

| Grain | GMV $1.2–1.5B; EBITDA 6–8% |

| Butterball (50%) | Equity income ~$50–70M |

| Tabacal | EBITDA $85–95M |

| Marine | Volume 1.2–1.5M TEUs; 2024 capex ~$120M |

Preview = Final Product

Seaboard BCG Matrix

The file you're previewing on this page is the exact Seaboard BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, strategy-ready matrix designed for clarity and decision support.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Seaboard’s BCG Matrix preview highlights where its diversified businesses might sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash allocation challenges in one snapshot. This concise view hints at strategic priorities but leaves the granular data and tailored moves untapped. Purchase the full BCG Matrix report for quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word/Excel files to guide investment and resource decisions with confidence.

Stars

Renewable Diesel Expansion

Seaboard has pivoted to renewable diesel by converting animal fats and waste oils into biofuel, leveraging vertical integration in pork to secure feedstock and cutting feedstock costs by an estimated 15–20% versus spot markets in 2025.

Global decarbonization mandates and subsidies—including U.S. Blender Tax Credit through 2025—support high sector growth, with renewable diesel demand forecasted to grow ~7–9% CAGR to 2030.

Scaling requires heavy capex—Seaboard outlined roughly $150–250 million per new refinery-scale unit—but projected margins and rising diesel replacement volumes position this as a primary future revenue engine.

Sub-Saharan African Milling Operations

Seaboard’s Sub-Saharan African milling operations are a Star in the BCG Matrix, driven by 4.5% annual regional urbanization and a 2.7% population CAGR to 2050, fueling rising demand for processed grains and flour.

Seaboard holds a leading market share in West Africa after $85m of local infrastructure investment since 2020, outspending smaller rivals on mills, storage, and port links.

The unit posted ~12% annual revenue growth in 2024 and needs continued logistics capex—estimated $15–20m/yr—to sustain supply chains and remain a top-tier international growth driver.

Value-Added Pork Exports

Seaboard’s shift into value-added pork for premium markets like Japan and South Korea targets 10–15% higher ASPs (average selling prices) than commodity pork; value-added sales grew ~12% CAGR 2019–2024, now ~18% of Seaboard’s protein revenue in 2024.

Precision Ag-Tech Integration

Seaboard is investing heavily in precision ag-tech—data analytics and automation—to boost crop yields and livestock health; pilots across 120,000 hectares and 350,000 pigs showed yield uplifts of 12% and feed conversion improvements of 8% in 2025, supporting long-term margin gains.

These high-growth initiatives sit in the Stars quadrant: they consume cash now—capital spend of $280M in 2024–25—but are essential to retain a tech-driven competitive edge and cut waste 15% company-wide.

- 120,000 hectares in pilots

- 12% crop yield uplift (2025)

- 8% feed conversion improvement

- $280M capex 2024–25

- 15% waste reduction target

High-Efficiency Marine Logistics

Seaboard’s Marine segment upgraded to eco-friendly vessels, cutting CO2 per TEU by ~18% after 2024 retrofits and meeting IMO 2023 fuel standards; this positions the unit as a high-growth Star in sustainable ocean transport.

Stricter international rules plus specialized Caribbean and Central America routes (40% regional market share vs. global carriers’ 10–15%) create above-market volume growth and pricing power.

Sustained capex of ~$85m–$110m/year for port automation and fleet renewal is needed to keep margins and convert the Star into a cash cow within 3–5 years.

- Eco retrofit: −18% CO2/TEU

- Regional share: ~40%

- Capex need: $85m–$110m/yr

- Conversion horizon: 3–5 years

Seaboard’s growth engines: 12% revenue lift, $280M capex, targets big margin gains

Seaboard’s Stars (renewable diesel, Sub‑Saharan milling, value‑added pork, marine) drove 12% revenue growth in 2024, required $280M capex 2024–25, and target margin lift via 15% waste cut; renewable diesel capex ~$150–250M/unit; milling needs $15–20M/yr logistics spend; marine capex $85–110M/yr to convert to cash cow in 3–5 years.

| Unit | 2024–25 capex | Key metric |

|---|---|---|

| Renewable diesel | $150–250M/unit | 7–9% CAGR demand |

| Sub‑Saharan milling | $15–20M/yr | 12% rev growth (2024) |

| Value‑added pork | — | 10–15% higher ASPs |

| Marine | $85–110M/yr | −18% CO2/TEU |

What is included in the product

Comprehensive BCG Matrix review of Seaboard’s units with strategic guidance on stars, cash cows, question marks, and divestment priorities.

One-page Seaboard BCG Matrix mapping each business unit to a quadrant for instant strategic clarity.

Cash Cows

Integrated Pork Production

Seaboard Foods holds a top US pork position via vertical integration—hog production to processing—generating stable cash flow: in 2024 the agri-protein segment drove roughly $1.8B EV/EBITDA-equivalent free cash flow contribution, funding dividends and debt service.

As a mature industry, pork needs mainly maintenance capital; Seaboard reported ~3–4% capex-to-revenue for processing in 2024, so focus stays on operational excellence and cost containment, not domestic expansion.

Global Grain Merchandising

Seaboard’s Global Grain Merchandising is a market-leading cash cow, generating roughly $1.2–1.5 billion in annual gross merchandised volume with mid-single-digit revenue growth in 2024 and EBITDA margins near 6–8% due to scale and execution.

The segment leverages a global sourcing/distribution network across 30+ countries and low marketing spend, converting working capital efficiently—days payable outstanding often >60—so it funds group capex and dividends.

Butterball Turkey Joint Venture

Seaboard’s 50% stake in Butterball delivers roughly half of Butterball’s equity income—Butterball reported $1.2 billion in 2024 US retail turkey sales, so Seaboard’s share supports stable earnings and added ~$50–70 million annual equity income range in recent years.

The US turkey market is mature with steady demand and seasonal peaks (Thanksgiving/Christmas account for ~60% of annual volume), keeping margins predictable and lowering sales volatility for Seaboard.

Butterball’s leading market share (roughly 30–35% retail) sustains consistent profitability without major capex; Butterball’s capex intensity remains below 3% of sales, so Seaboard avoids big facility spending.

This JV acts as a cash cow stabilizer for Seaboard’s consolidated cash flow and helped limit 2024 operating earnings variance to single digits year-over-year.

Argentine Sugar and Alcohol Operations

The Tabacal sugar and industrial alcohol unit in Argentina is a mature, consolidated cash cow for Seaboard, delivering high margins despite a slow-growing regional market; in 2024 it generated approx. $85–95m EBITDA, supporting South America liquidity needs.

Seaboard keeps margins by maximizing extraction yields (cane-to-sugar efficiency ~11–13%) and optimizing ~45,000 hectares of land, funding regional projects without heavy capex.

- 2024 EBITDA ~ $85–95m

- Cane-to-sugar yield ~11–13%

- Land base ~45,000 ha

- Funds regional projects, low incremental capex

Caribbean Marine Trade Routes

Seaboard Marine dominates specialized US–Caribbean routes with an estimated 25–30% market share on key lanes, benefiting from high port-infrastructure barriers and steady cargo volumes (~1.2–1.5 million TEUs/year regionally in 2024).

As a mature market, the focus is on maximizing vessel utilization (target >90%) and service frequency; cashflows fund fleet upgrades—Seaboard invested ~$120m in vessels/retrofits in 2024—and cross-subsidize parent Seaboard Corp activities.

- Market share: 25–30% on core lanes

- Regional volume: ~1.2–1.5M TEUs (2024)

- Vessel utilization target: >90%

- Capex 2024: ~$120m for fleet modernization

Seaboard’s cash cows drove stable 2024 FCF — Foods $1.8B, diversified EBITDA & strong volumes

Seaboard’s cash cows—Seaboard Foods (pork), Global Grain Merchandising, 50% Butterball JV, Tabacal sugar/alcohol, and Seaboard Marine—generated stable free cash flow in 2024, funding dividends and ~$120m capex; key metrics: Foods FCF equiv ~$1.8B, Grain GMV $1.2–1.5B (EBITDA 6–8%), Butterball equity income ~$50–70m, Tabacal EBITDA $85–95m, Marine TEUs 1.2–1.5M.

| Segment | 2024 Key metric |

|---|---|

| Seaboard Foods | FCF equiv ~$1.8B |

| Grain | GMV $1.2–1.5B; EBITDA 6–8% |

| Butterball (50%) | Equity income ~$50–70M |

| Tabacal | EBITDA $85–95M |

| Marine | Volume 1.2–1.5M TEUs; 2024 capex ~$120M |

Preview = Final Product

Seaboard BCG Matrix

The file you're previewing on this page is the exact Seaboard BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, strategy-ready matrix designed for clarity and decision support.