Seaspan Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

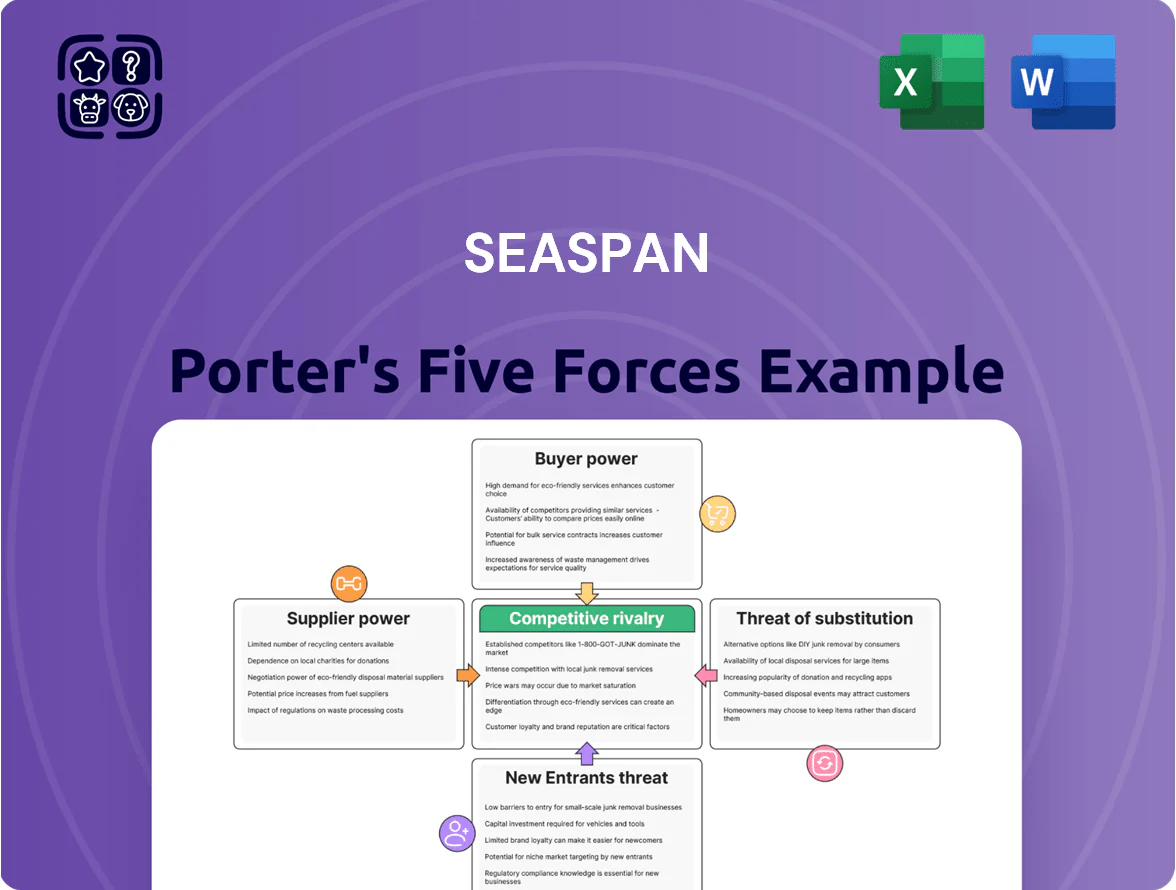

Seaspan operates in a capital-intensive, consolidation-driven shipping sector where bargaining power of large charterers and technological shifts shape margins and asset utilization.

This snapshot highlights supplier concentration, moderate entry barriers, and substitution risks from modal shifts—key inputs for fleet and contract strategy.

Ready to move beyond the basics? Get a full strategic breakdown of Seaspan’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentration of major global shipyards

The global newbuild market is concentrated: South Korea and China built about 70% of mega containerships by deadweight in 2024, so major yards like Hyundai Heavy, Samsung, and CSSC can push prices and schedules. As Seaspan aims to retrofit eco-designs by end-2025, limited berth slots kept average newbuild lead times at 18–30 months in 2024, raising capex per vessel by roughly $10–20m versus standard designs. This concentration forces independents to pay premiums to secure latest tech.

Specialized engine and propulsion technology

Suppliers of dual-fuel engines and carbon-reduction gear hold strong leverage as shipping targets net-zero by 2050; in 2024 green engine orders covered ~18% of newbuild specs, keeping demand tight. Seaspan depends on few makers like MAN Energy Solutions and WinGD for high-spec engines, so supplier pricing and lead times—often 12–36 months—can be imposed. Scarcity of retrofit kits and specialist maintenance skills lets suppliers set warranty and service terms, raising capex and OPEX predictably.

Financial institutions and capital markets

The capital‑intensive nature of shipping leaves Seaspan reliant on banks, leasing firms and bondholders for growth capital; at end‑2024 Seaspan carried $5.8bn of debt, making funding terms decisive. Changes in global rates—US 10‑yr up 1.1ppt in 2024 to ~4.2%—and tighter ESG lending rules by late 2025 will raise cost of debt and limit newbuilding plans. Financial suppliers set leverage covenants and residual‑value clauses that shape fleet expansion and refinancing windows.

Global bunker and alternative fuel providers

The shift to LNG, methanol, and ammonia hands energy firms control over low-carbon bunker supply chains; as of 2025 only ~1.2% of global bunker volume is LNG-ready, letting suppliers set terms and premiums for scarce fuel types.

Seaspan must secure reliable refueling access across key hubs to meet charterer uptime; fuel availability gaps raise operational risk and can trigger penalty payments under time-charter contracts.

Price volatility and limited low-carbon fuel capacity—estimated <100,000 tonnes/day for green methanol in 2025—strengthen suppliers’ negotiating power, increasing long-term fuel cost uncertainty for less-integrated shipowners.

- ~1.2% global LNG bunker readiness (2025)

- <100,000 t/day green methanol capacity (2025)

- High fuel-price volatility raises charter risk

- Infrastructure access critical to avoid penalties

Availability of skilled maritime labor

The global pool of officers and crew able to run high-tech, alternative-fuel ships is shrinking; BIMCO/ICS estimated a shortfall of 147,500 officers by 2025, raising wage premiums for specialists.

Specialized crewing firms and unions can push up Seaspan’s operating costs as demand for LNG, methanol, and battery expertise rises; premium pay rates jumped ~10–15% in 2023–24 for such skills.

Seaspan’s operational reliability hinges on access to this tight labor market; failure to secure talent risks higher OPEX and schedule disruptions.

- 147,500 officer shortfall (BIMCO/ICS, 2025)

- 10–15% premium for alternative-fuel crew (2023–24 market data)

- Dependence on specialist agencies raises OPEX and continuity risk

Suppliers Hold the Leverage: Seaspan Faces Capacity, Fuel, Crew & Debt Constraints

Suppliers—shipyards, engine makers, low‑carbon fuel providers, finance and specialist crewing firms—hold high bargaining power for Seaspan due to concentrated newbuild capacity (≈70% S. Korea/China, 2024), long lead times (18–30 months), scarce green fuels (≈1.2% LNG readiness; <100,000 t/day green methanol, 2025), $5.8bn debt (end‑2024), and a 147,500 officer shortfall (BIMCO/ICS, 2025).

| Metric | Value |

|---|---|

| Newbuild share | ~70% (S. Korea/China, 2024) |

| Lead times | 18–30 months (2024) |

| Green fuel capacity | <100,000 t/day methanol (2025) |

| LNG readiness | ~1.2% (2025) |

| Seaspan debt | $5.8bn (end‑2024) |

| Officer shortfall | 147,500 (BIMCO/ICS, 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Seaspan that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its vessel leasing and shipping services.

Seaspan Porter's Five Forces summarized on one sheet—quickly spot competitive threats and opportunities to streamline strategic decisions.

Customers Bargaining Power

Concentration of global liner companies

The customer base for Seaspan is highly consolidated: MSC, Maersk, and CMA CGM together controlled roughly 55–60% of global container capacity in 2024, giving them strong bargaining power to push charter rates down when vessel supply rises. These giants can extract favorable long-term rates and strict return conditions, and their scale lets them set service and technical specs—e.g., fuel-efficiency and scrubber retrofits—raising capex and compliance costs for less flexible owners like Seaspan.

Long term charter contract structures

Seaspan reduces customer bargaining power through long-term, fixed-rate charters that lock in revenue; as of Q4 2025 roughly 85% of available days are under multi-year contracts, giving multi-year cash visibility.

Staggered expiries mean only about 10–15% of the fleet faces spot re-pricing in any 12-month window by end-2025, so short-term demand shocks have limited impact.

Switching costs for liner operators

Seaspan’s ships can be swapped by liner customers, but embedding a vessel into a long-term east‑west or intra‑Asia route creates logistical switching costs—rerouting schedules, slot deals and terminal allocations can exceed $200k per ship in first-year disruption for large loops. The technical fit of Seaspan’s modern 14–24k TEU fleet to specific network needs (draft, gear, fuel systems) raises integration costs and delays. That technical lock‑in limits customer leverage and helps protect Seaspan against steep rate cuts during contract renewals.

Liner vertical integration and own fleet

Major liner customers increasingly own large fleet pools and use third-party managers like Seaspan for extra capacity; by end-2024, top 20 liners held roughly 55% of the global containership fleet by TEU, limiting charter demand for independents.

When charter rates spike—peak 2021 boxship timecharter rates hit >200,000/day—liners can add owned tonnage, so their buying power caps Seaspan’s pricing; this creates a natural ceiling on independent owners’ rate-setting.

- Top 20 liners ~55% global TEU (2024)

- 2021 peak TC >200,000/day shows rate volatility

- Liners can shift to ownership to control cost

Economic health of major trade routes

The bargaining power of customers depends on trade volume along routes like Trans-Pacific and Asia-Europe; in 2024 Trans-Pacific carried ~11.5m TEU and Asia-Europe ~22m TEU, so demand shifts matter.

If global GDP growth slows toward 2.5% by late 2025, liners could press for flexible contracts or lower rates at renewals; conversely, peak load factors >95% boost vessel owners’ leverage.

- Trans‑Pacific ~11.5m TEU (2024)

- Asia‑Europe ~22m TEU (2024)

- Global GDP forecast ~2.5% (late 2025)

- Load factor >95% favors owners

Seaspan's multi‑year charters cushion rate pressure despite carriers' 55–60% market sway

Customers (MSC, Maersk, CMA CGM ~55–60% capacity in 2024) hold strong price leverage, pressuring rates and specs, but Seaspan’s multi-year charters (≈85% of days fixed by Q4 2025) and staggered expiries (10–15% reprice/year) limit short-term exposure; technical fit of 14–24k TEU ships raises switching costs and cushions renewals.

| Metric | Value |

|---|---|

| Top 3 market share (2024) | 55–60% |

| Seaspan fixed days (Q4 2025) | ~85% |

| Annual reprice at expiry | 10–15% |

| Trans‑Pacific TEU (2024) | ~11.5m |

| Asia‑Europe TEU (2024) | ~22m |

What You See Is What You Get

Seaspan Porter's Five Forces Analysis

This preview shows the exact Seaspan Porter's Five Forces analysis you'll receive—fully formatted, professionally written, and ready to download immediately after purchase with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Seaspan operates in a capital-intensive, consolidation-driven shipping sector where bargaining power of large charterers and technological shifts shape margins and asset utilization.

This snapshot highlights supplier concentration, moderate entry barriers, and substitution risks from modal shifts—key inputs for fleet and contract strategy.

Ready to move beyond the basics? Get a full strategic breakdown of Seaspan’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentration of major global shipyards

The global newbuild market is concentrated: South Korea and China built about 70% of mega containerships by deadweight in 2024, so major yards like Hyundai Heavy, Samsung, and CSSC can push prices and schedules. As Seaspan aims to retrofit eco-designs by end-2025, limited berth slots kept average newbuild lead times at 18–30 months in 2024, raising capex per vessel by roughly $10–20m versus standard designs. This concentration forces independents to pay premiums to secure latest tech.

Specialized engine and propulsion technology

Suppliers of dual-fuel engines and carbon-reduction gear hold strong leverage as shipping targets net-zero by 2050; in 2024 green engine orders covered ~18% of newbuild specs, keeping demand tight. Seaspan depends on few makers like MAN Energy Solutions and WinGD for high-spec engines, so supplier pricing and lead times—often 12–36 months—can be imposed. Scarcity of retrofit kits and specialist maintenance skills lets suppliers set warranty and service terms, raising capex and OPEX predictably.

Financial institutions and capital markets

The capital‑intensive nature of shipping leaves Seaspan reliant on banks, leasing firms and bondholders for growth capital; at end‑2024 Seaspan carried $5.8bn of debt, making funding terms decisive. Changes in global rates—US 10‑yr up 1.1ppt in 2024 to ~4.2%—and tighter ESG lending rules by late 2025 will raise cost of debt and limit newbuilding plans. Financial suppliers set leverage covenants and residual‑value clauses that shape fleet expansion and refinancing windows.

Global bunker and alternative fuel providers

The shift to LNG, methanol, and ammonia hands energy firms control over low-carbon bunker supply chains; as of 2025 only ~1.2% of global bunker volume is LNG-ready, letting suppliers set terms and premiums for scarce fuel types.

Seaspan must secure reliable refueling access across key hubs to meet charterer uptime; fuel availability gaps raise operational risk and can trigger penalty payments under time-charter contracts.

Price volatility and limited low-carbon fuel capacity—estimated <100,000 tonnes/day for green methanol in 2025—strengthen suppliers’ negotiating power, increasing long-term fuel cost uncertainty for less-integrated shipowners.

- ~1.2% global LNG bunker readiness (2025)

- <100,000 t/day green methanol capacity (2025)

- High fuel-price volatility raises charter risk

- Infrastructure access critical to avoid penalties

Availability of skilled maritime labor

The global pool of officers and crew able to run high-tech, alternative-fuel ships is shrinking; BIMCO/ICS estimated a shortfall of 147,500 officers by 2025, raising wage premiums for specialists.

Specialized crewing firms and unions can push up Seaspan’s operating costs as demand for LNG, methanol, and battery expertise rises; premium pay rates jumped ~10–15% in 2023–24 for such skills.

Seaspan’s operational reliability hinges on access to this tight labor market; failure to secure talent risks higher OPEX and schedule disruptions.

- 147,500 officer shortfall (BIMCO/ICS, 2025)

- 10–15% premium for alternative-fuel crew (2023–24 market data)

- Dependence on specialist agencies raises OPEX and continuity risk

Suppliers Hold the Leverage: Seaspan Faces Capacity, Fuel, Crew & Debt Constraints

Suppliers—shipyards, engine makers, low‑carbon fuel providers, finance and specialist crewing firms—hold high bargaining power for Seaspan due to concentrated newbuild capacity (≈70% S. Korea/China, 2024), long lead times (18–30 months), scarce green fuels (≈1.2% LNG readiness; <100,000 t/day green methanol, 2025), $5.8bn debt (end‑2024), and a 147,500 officer shortfall (BIMCO/ICS, 2025).

| Metric | Value |

|---|---|

| Newbuild share | ~70% (S. Korea/China, 2024) |

| Lead times | 18–30 months (2024) |

| Green fuel capacity | <100,000 t/day methanol (2025) |

| LNG readiness | ~1.2% (2025) |

| Seaspan debt | $5.8bn (end‑2024) |

| Officer shortfall | 147,500 (BIMCO/ICS, 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Seaspan that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its vessel leasing and shipping services.

Seaspan Porter's Five Forces summarized on one sheet—quickly spot competitive threats and opportunities to streamline strategic decisions.

Customers Bargaining Power

Concentration of global liner companies

The customer base for Seaspan is highly consolidated: MSC, Maersk, and CMA CGM together controlled roughly 55–60% of global container capacity in 2024, giving them strong bargaining power to push charter rates down when vessel supply rises. These giants can extract favorable long-term rates and strict return conditions, and their scale lets them set service and technical specs—e.g., fuel-efficiency and scrubber retrofits—raising capex and compliance costs for less flexible owners like Seaspan.

Long term charter contract structures

Seaspan reduces customer bargaining power through long-term, fixed-rate charters that lock in revenue; as of Q4 2025 roughly 85% of available days are under multi-year contracts, giving multi-year cash visibility.

Staggered expiries mean only about 10–15% of the fleet faces spot re-pricing in any 12-month window by end-2025, so short-term demand shocks have limited impact.

Switching costs for liner operators

Seaspan’s ships can be swapped by liner customers, but embedding a vessel into a long-term east‑west or intra‑Asia route creates logistical switching costs—rerouting schedules, slot deals and terminal allocations can exceed $200k per ship in first-year disruption for large loops. The technical fit of Seaspan’s modern 14–24k TEU fleet to specific network needs (draft, gear, fuel systems) raises integration costs and delays. That technical lock‑in limits customer leverage and helps protect Seaspan against steep rate cuts during contract renewals.

Liner vertical integration and own fleet

Major liner customers increasingly own large fleet pools and use third-party managers like Seaspan for extra capacity; by end-2024, top 20 liners held roughly 55% of the global containership fleet by TEU, limiting charter demand for independents.

When charter rates spike—peak 2021 boxship timecharter rates hit >200,000/day—liners can add owned tonnage, so their buying power caps Seaspan’s pricing; this creates a natural ceiling on independent owners’ rate-setting.

- Top 20 liners ~55% global TEU (2024)

- 2021 peak TC >200,000/day shows rate volatility

- Liners can shift to ownership to control cost

Economic health of major trade routes

The bargaining power of customers depends on trade volume along routes like Trans-Pacific and Asia-Europe; in 2024 Trans-Pacific carried ~11.5m TEU and Asia-Europe ~22m TEU, so demand shifts matter.

If global GDP growth slows toward 2.5% by late 2025, liners could press for flexible contracts or lower rates at renewals; conversely, peak load factors >95% boost vessel owners’ leverage.

- Trans‑Pacific ~11.5m TEU (2024)

- Asia‑Europe ~22m TEU (2024)

- Global GDP forecast ~2.5% (late 2025)

- Load factor >95% favors owners

Seaspan's multi‑year charters cushion rate pressure despite carriers' 55–60% market sway

Customers (MSC, Maersk, CMA CGM ~55–60% capacity in 2024) hold strong price leverage, pressuring rates and specs, but Seaspan’s multi-year charters (≈85% of days fixed by Q4 2025) and staggered expiries (10–15% reprice/year) limit short-term exposure; technical fit of 14–24k TEU ships raises switching costs and cushions renewals.

| Metric | Value |

|---|---|

| Top 3 market share (2024) | 55–60% |

| Seaspan fixed days (Q4 2025) | ~85% |

| Annual reprice at expiry | 10–15% |

| Trans‑Pacific TEU (2024) | ~11.5m |

| Asia‑Europe TEU (2024) | ~22m |

What You See Is What You Get

Seaspan Porter's Five Forces Analysis

This preview shows the exact Seaspan Porter's Five Forces analysis you'll receive—fully formatted, professionally written, and ready to download immediately after purchase with no placeholders or samples.