Securitas SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Securitas combines a global footprint and diversified security services with strong recurring revenues, but faces margin pressure from labor costs and technology disruption; regulatory complexity and competitive fragmentation pose medium-term risks. Discover the full SWOT analysis for in-depth, research-backed insights, editable Word and Excel deliverables, and strategic recommendations to inform investment, M&A, or operational plans—available for purchase now.

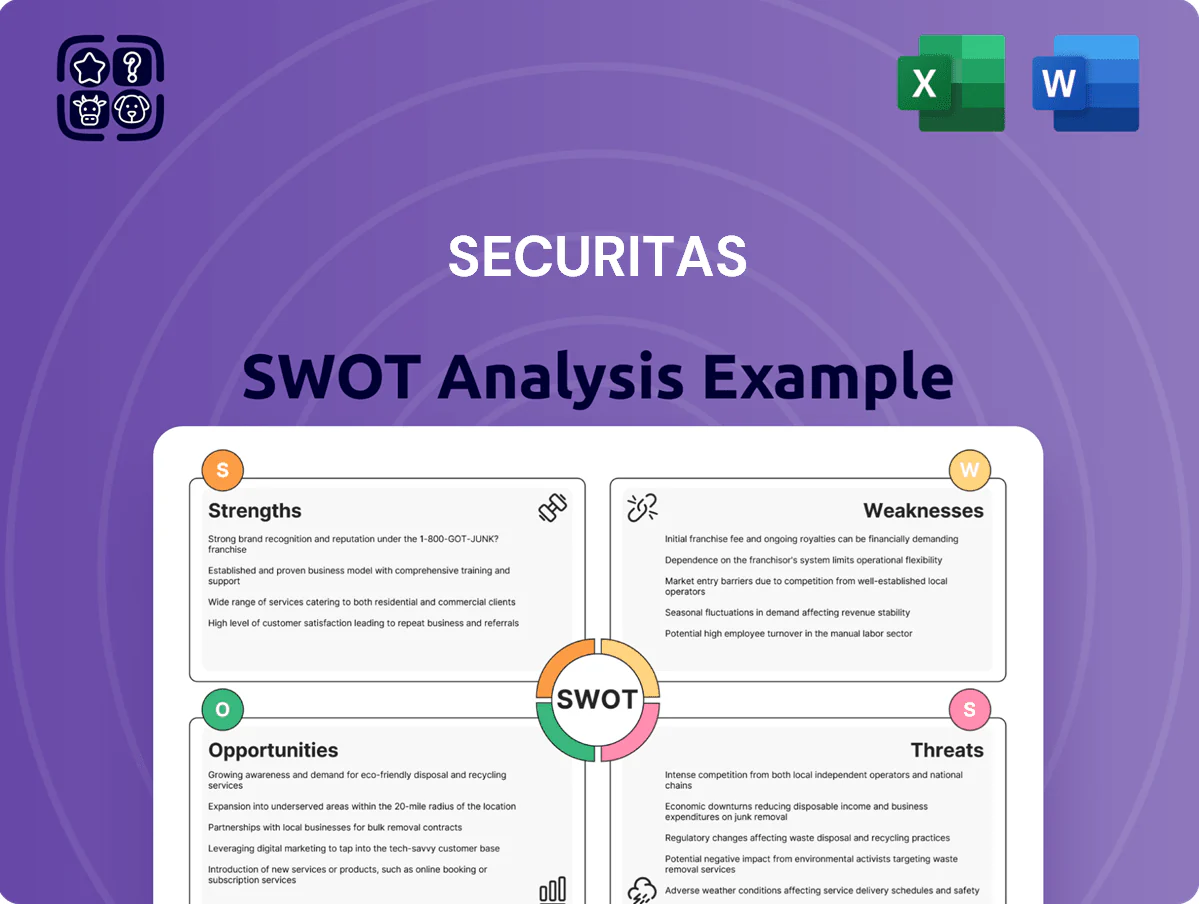

Strengths

Dominant Global Footprint

Securitas operates in over 40 countries and reported SEK 142.1 billion revenue in 2024, giving it scale to serve multinational clients with consistent, standardized security protocols and centralized account management.

That global footprint supports winning large-scale contracts and government tenders; in 2024 Securitas held top-three market share in multiple European and North American markets, making it a default choice for complex, cross-border security needs.

Advanced Technological Integration

The 2021 acquisition of Stanley Security vaulted Securitas into electronic-security leadership, lifting electronic monitoring revenue to about 20% of group sales by 2024 and pushing adjusted operating margin in Solutions toward ~9% (vs 5% pre‑deal).

Strong Brand Equity

With over 85 years of operating history and a 2024 revenue of SEK 171.5 billion (about USD 15.5 billion), Securitas is widely seen as a reliable global security brand, which strengthens client trust in protecting people and high-value assets. This reputation helps Securitas win large, high-margin contracts—its solutions contracts grew 12% in 2024—where buyers prioritize quality and continuity over lowest price, reducing churn and bidding risk.

Diversified Revenue Streams

Focus on Subscription Models

Securitas has shifted a growing share of revenue to subscription-based security-as-a-service, driving recurring monthly revenue that raised recurring sales to about 28% of group revenue by FY2024, improving visibility into future earnings.

This subscription model stabilizes performance versus contract and project work, reduces volatility in operating cash flow, and supports predictable capital allocation for innovation and tech upgrades.

It aligns incentives with long-term client retention—average contract length rose to ~3.4 years in 2024—boosting lifetime value and margin predictability.

- Recurring revenue ~28% of group sales (FY2024)

- Avg contract length ~3.4 years (2024)

- Higher revenue visibility, lower cash-flow volatility

Securitas scales across 40+ countries—SEK171.5bn revenue, 28% recurring, 4.1% organic

Securitas’s global scale (operating in 40+ countries) and leading market positions drove SEK 171.5bn revenue in 2024, strong cross‑selling (4.1% organic growth) and Solutions margins (~9%) after the 2021 Stanley deal; recurring subscription revenue reached ~28% with avg contract length ~3.4 years, supporting revenue visibility and lower cash‑flow volatility.

| Metric | 2024 |

|---|---|

| Revenue | SEK 171.5bn |

| Recurring revenue | ~28% |

| Organic growth | 4.1% |

| Solutions margin | ~9% |

| Avg contract length | ~3.4 yrs |

What is included in the product

Provides a concise SWOT overview of Securitas, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decision-making.

Offers a concise SWOT matrix tailored to Securitas for rapid strategy alignment and executive snapshots, enabling quick edits to reflect evolving security market priorities.

Weaknesses

Labor Intensive Operations

Narrow Operating Margins

Despite shifting toward tech, Securitas AB’s core guarding arm still posts thin operating margins—around 3.5% adjusted operating margin for Global Solutions in 2024—because fierce competition keeps pricing low.

Price wars in the low-end security segment compress revenue per guard and contributed to a 1.2% decline in gross margin in 2024 versus 2023.

Raising margins needs ongoing cost cuts and sustained investment in digital services; Securitas spent SEK 1.1bn on tech R&D and acquisitions in 2024, a heavy but necessary expense.

Significant Debt Burden

The 2021 acquisition of Stanley Security pushed net debt to about SEK 30.5bn (≈$3.0bn) by year-end 2024, and elevated leverage (net debt/EBITDA ~3.3x through 2025) constrained free cash flow available for bolt-on deals or R&D increases.

High interest and amortization needs limit capital for tech upgrades and organic growth, so management lists deleveraging—targeting sub-2.5x net debt/EBITDA—as a top priority to restore credit ratings and flexibility.

Geographic Concentration

- ~65% revenue from NA+EU (2024)

- 2024 organic growth 3.8%

- Operating margin ~4.2% (2024)

- High exposure to regional regulation and GDP cycles

Complex Integration Processes

Large-scale acquisitions since 2021 expanded Securitas AB’s geographic footprint but left complex integration work: merging diverse tech stacks and corporate cultures often takes 12–24 months and consumed an estimated SEK 350–500m in integration costs in 2023–24, slowing margin recovery.

Inefficiencies during integration have caused service gaps and client complaints in select markets, risking churn where SLAs slipped by up to 8% year-over-year in 2024.

Legacy systems still hamper global interoperability; about 20% of sites relied on bespoke platforms at end-2024, raising IT maintenance spend and complicating rollout of unified offerings.

- Integration costs SEK 350–500m (2023–24)

- SLA slips up to 8% in 2024

- 20% of sites on legacy systems (end-2024)

High wages, heavy debt and thin margins leave security services squeezed and regionalized

| Metric | Value (2024) |

|---|---|

| Guards | ~350,000 |

| Net debt | SEK 30.5bn |

| Net debt/EBITDA | ~3.3x |

| Operating margin | ~4.2% |

| Revenue NA+EU | ~65% |

What You See Is What You Get

Securitas SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

The file shown below is not a sample—it’s the real SWOT analysis you'll download post-purchase, in full detail.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Securitas combines a global footprint and diversified security services with strong recurring revenues, but faces margin pressure from labor costs and technology disruption; regulatory complexity and competitive fragmentation pose medium-term risks. Discover the full SWOT analysis for in-depth, research-backed insights, editable Word and Excel deliverables, and strategic recommendations to inform investment, M&A, or operational plans—available for purchase now.

Strengths

Dominant Global Footprint

Securitas operates in over 40 countries and reported SEK 142.1 billion revenue in 2024, giving it scale to serve multinational clients with consistent, standardized security protocols and centralized account management.

That global footprint supports winning large-scale contracts and government tenders; in 2024 Securitas held top-three market share in multiple European and North American markets, making it a default choice for complex, cross-border security needs.

Advanced Technological Integration

The 2021 acquisition of Stanley Security vaulted Securitas into electronic-security leadership, lifting electronic monitoring revenue to about 20% of group sales by 2024 and pushing adjusted operating margin in Solutions toward ~9% (vs 5% pre‑deal).

Strong Brand Equity

With over 85 years of operating history and a 2024 revenue of SEK 171.5 billion (about USD 15.5 billion), Securitas is widely seen as a reliable global security brand, which strengthens client trust in protecting people and high-value assets. This reputation helps Securitas win large, high-margin contracts—its solutions contracts grew 12% in 2024—where buyers prioritize quality and continuity over lowest price, reducing churn and bidding risk.

Diversified Revenue Streams

Focus on Subscription Models

Securitas has shifted a growing share of revenue to subscription-based security-as-a-service, driving recurring monthly revenue that raised recurring sales to about 28% of group revenue by FY2024, improving visibility into future earnings.

This subscription model stabilizes performance versus contract and project work, reduces volatility in operating cash flow, and supports predictable capital allocation for innovation and tech upgrades.

It aligns incentives with long-term client retention—average contract length rose to ~3.4 years in 2024—boosting lifetime value and margin predictability.

- Recurring revenue ~28% of group sales (FY2024)

- Avg contract length ~3.4 years (2024)

- Higher revenue visibility, lower cash-flow volatility

Securitas scales across 40+ countries—SEK171.5bn revenue, 28% recurring, 4.1% organic

Securitas’s global scale (operating in 40+ countries) and leading market positions drove SEK 171.5bn revenue in 2024, strong cross‑selling (4.1% organic growth) and Solutions margins (~9%) after the 2021 Stanley deal; recurring subscription revenue reached ~28% with avg contract length ~3.4 years, supporting revenue visibility and lower cash‑flow volatility.

| Metric | 2024 |

|---|---|

| Revenue | SEK 171.5bn |

| Recurring revenue | ~28% |

| Organic growth | 4.1% |

| Solutions margin | ~9% |

| Avg contract length | ~3.4 yrs |

What is included in the product

Provides a concise SWOT overview of Securitas, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decision-making.

Offers a concise SWOT matrix tailored to Securitas for rapid strategy alignment and executive snapshots, enabling quick edits to reflect evolving security market priorities.

Weaknesses

Labor Intensive Operations

Narrow Operating Margins

Despite shifting toward tech, Securitas AB’s core guarding arm still posts thin operating margins—around 3.5% adjusted operating margin for Global Solutions in 2024—because fierce competition keeps pricing low.

Price wars in the low-end security segment compress revenue per guard and contributed to a 1.2% decline in gross margin in 2024 versus 2023.

Raising margins needs ongoing cost cuts and sustained investment in digital services; Securitas spent SEK 1.1bn on tech R&D and acquisitions in 2024, a heavy but necessary expense.

Significant Debt Burden

The 2021 acquisition of Stanley Security pushed net debt to about SEK 30.5bn (≈$3.0bn) by year-end 2024, and elevated leverage (net debt/EBITDA ~3.3x through 2025) constrained free cash flow available for bolt-on deals or R&D increases.

High interest and amortization needs limit capital for tech upgrades and organic growth, so management lists deleveraging—targeting sub-2.5x net debt/EBITDA—as a top priority to restore credit ratings and flexibility.

Geographic Concentration

- ~65% revenue from NA+EU (2024)

- 2024 organic growth 3.8%

- Operating margin ~4.2% (2024)

- High exposure to regional regulation and GDP cycles

Complex Integration Processes

Large-scale acquisitions since 2021 expanded Securitas AB’s geographic footprint but left complex integration work: merging diverse tech stacks and corporate cultures often takes 12–24 months and consumed an estimated SEK 350–500m in integration costs in 2023–24, slowing margin recovery.

Inefficiencies during integration have caused service gaps and client complaints in select markets, risking churn where SLAs slipped by up to 8% year-over-year in 2024.

Legacy systems still hamper global interoperability; about 20% of sites relied on bespoke platforms at end-2024, raising IT maintenance spend and complicating rollout of unified offerings.

- Integration costs SEK 350–500m (2023–24)

- SLA slips up to 8% in 2024

- 20% of sites on legacy systems (end-2024)

High wages, heavy debt and thin margins leave security services squeezed and regionalized

| Metric | Value (2024) |

|---|---|

| Guards | ~350,000 |

| Net debt | SEK 30.5bn |

| Net debt/EBITDA | ~3.3x |

| Operating margin | ~4.2% |

| Revenue NA+EU | ~65% |

What You See Is What You Get

Securitas SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

The file shown below is not a sample—it’s the real SWOT analysis you'll download post-purchase, in full detail.