Security National PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover the critical political, economic, and technological forces shaping Security National's trajectory. Our comprehensive PESTLE analysis provides actionable intelligence to inform your strategic decisions and competitive advantage. Download the full report now for expert insights.

Political factors

Government Regulatory Stance

Government policies and regulatory frameworks are pivotal for financial services, insurance, and mortgage sectors. For Security National Financial Corporation, shifts in oversight, such as increased capital requirements or enhanced consumer protection measures, directly influence profitability and operational expenses. For instance, the Dodd-Frank Act's ongoing impact, coupled with potential future regulatory adjustments in 2024 and 2025, necessitates continuous adaptation.

Political stability and the government's stance on market intervention are critical for investor confidence and strategic planning. A stable political environment fosters predictability, allowing companies like Security National to forecast growth and manage risks effectively. Conversely, political uncertainty or sudden policy changes can introduce volatility, impacting investment decisions and long-term business strategies.

Taxation Policies

Fluctuations in corporate tax rates directly impact Security National's bottom line. For instance, a potential increase in the U.S. federal corporate tax rate from 21% to 28% could reduce net income, affecting reinvestment and dividend capacity. Tax incentives for specific financial products, such as changes to mortgage interest deductibility or capital gains tax rates, can significantly alter consumer demand for Security National's mortgage and investment offerings.

Moreover, shifts in estate tax laws could influence the attractiveness of life insurance products, a key revenue driver for Security National. For example, if estate tax exemptions are lowered, demand for life insurance as an estate planning tool might rise. Conversely, unfavorable tax changes could dampen demand, impacting Security National's revenue streams and overall financial health.

Monetary Policy Influence

Central bank decisions significantly shape the mortgage market. For instance, the Federal Reserve's aggressive rate hikes throughout 2022 and 2023, pushing the federal funds rate from near zero to over 5%, directly impacted mortgage rates, which climbed from around 3% to over 7% for a 30-year fixed loan. This surge in borrowing costs cooled housing demand and refinancing, as anticipated, affecting loan origination volumes for institutions like Security National.

Looking ahead to 2024 and 2025, the trajectory of monetary policy remains a critical factor. Analysts anticipate potential rate cuts by the Federal Reserve in late 2024 or early 2025, contingent on inflation trends. Should inflation continue to moderate, a decrease in interest rates could reignite mortgage demand and refinancing, potentially boosting Security National's business, while persistent inflation might necessitate maintaining higher rates, thus continuing to pressure the housing market.

International Relations and Trade Policies

While Security National primarily operates domestically, shifts in international relations and trade policies can create ripple effects. For instance, changes in global trade agreements, such as potential renegotiations of existing pacts or the imposition of new tariffs, could indirectly impact the U.S. economy. This, in turn, influences consumer confidence and investment decisions, affecting demand for Security National's financial offerings.

The ongoing geopolitical landscape, including major power dynamics and regional conflicts, also plays a role. Instability abroad can lead to market volatility and affect investor sentiment, potentially dampening investment patterns. For example, the International Monetary Fund (IMF) projected global growth to be 3.2% in 2024, a slight slowdown from 2023, highlighting the interconnectedness of economies and the impact of global events on domestic financial markets.

- Trade Policy Impact: Fluctuations in trade tariffs and agreements can alter the cost of goods and services, indirectly affecting consumer spending power and business investment.

- Geopolitical Stability: Major international conflicts or political realignments can trigger global economic uncertainty, influencing investor confidence and capital flows into the U.S.

- Global Economic Growth: Slowdowns in major international economies, as indicated by IMF projections, can reduce export opportunities and dampen overall U.S. economic activity, impacting financial sector demand.

- Currency Fluctuations: International trade and investment often involve currency exchange, and significant shifts in exchange rates can impact the profitability of U.S. companies involved in international trade, indirectly affecting the broader financial environment.

Political Stability and Geopolitical Risks

Political stability is a cornerstone for business confidence, encouraging long-term investments. In 2024, countries with robust democratic institutions and predictable policy environments are likely to attract more foreign direct investment. For instance, the World Bank’s 2023 report highlighted that political stability is a key driver for economic growth, with stable nations seeing an average GDP growth rate 1.5% higher than unstable ones.

Conversely, geopolitical tensions and domestic political instability can inject significant economic uncertainty. This volatility can dampen consumer spending, particularly on discretionary financial products like life insurance. The ongoing conflicts in Eastern Europe, for example, have contributed to energy price volatility and supply chain disruptions globally, impacting consumer purchasing power and investment sentiment throughout 2024.

Market volatility often escalates during periods of political uncertainty. Investors tend to become more risk-averse, leading to capital flight from emerging markets or sectors perceived as politically exposed. This can affect the stability of real estate markets as well, with potential buyers delaying purchases amidst economic unpredictability. For example, in late 2023 and early 2024, several major economies experienced sharp, albeit temporary, downturns in real estate investment following unexpected political developments.

- Political Stability: Fosters business confidence and long-term investment.

- Geopolitical Risks: Can cause economic uncertainty and market volatility.

- Consumer Spending: Reduced during periods of political instability, impacting discretionary financial products.

- Real Estate Market: Susceptible to volatility due to economic uncertainty stemming from political factors.

Government, Tax, & Rates: Financial Market Dynamics

Government policies and regulatory frameworks are pivotal for financial services. Shifts in oversight, such as increased capital requirements or enhanced consumer protection measures, directly influence profitability and operational expenses for companies like Security National. For instance, the ongoing impact of the Dodd-Frank Act, coupled with potential future regulatory adjustments in 2024 and 2025, necessitates continuous adaptation.

Political stability and the government's stance on market intervention are critical for investor confidence and strategic planning. A stable political environment fosters predictability, allowing companies like Security National to forecast growth and manage risks effectively. Conversely, political uncertainty or sudden policy changes can introduce volatility, impacting investment decisions and long-term business strategies.

Fluctuations in corporate tax rates directly impact a company's bottom line. For example, a potential increase in the U.S. federal corporate tax rate from 21% could reduce net income, affecting reinvestment and dividend capacity. Tax incentives for specific financial products can also significantly alter consumer demand for offerings like mortgages and investments.

Central bank decisions significantly shape markets. For instance, the Federal Reserve's rate hikes throughout 2022 and 2023, pushing the federal funds rate from near zero to over 5%, directly impacted mortgage rates, which climbed from around 3% to over 7%. This surge in borrowing costs cooled housing demand and refinancing, affecting loan origination volumes.

What is included in the product

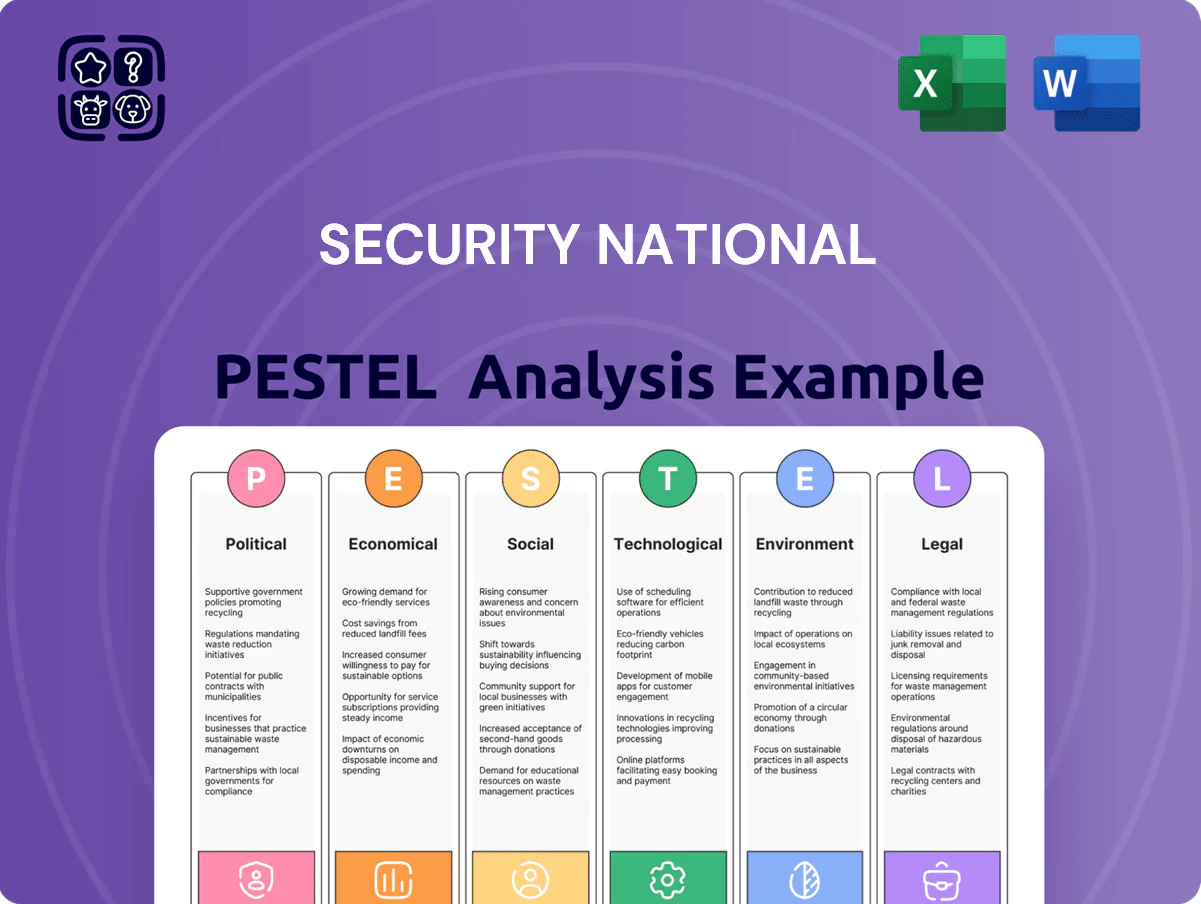

This PESTLE analysis provides a comprehensive examination of the external macro-environmental factors influencing Security National, detailing how Political, Economic, Social, Technological, Environmental, and Legal forces create both challenges and strategic advantages.

Provides a concise version that can be dropped into PowerPoints or used in group planning sessions, simplifying complex external factors into actionable insights.

Economic factors

Interest Rate Environment

The prevailing interest rate environment significantly impacts Security National, especially its mortgage loan operations. As of mid-2025, the Federal Reserve's benchmark interest rate remains elevated, hovering around 5.25%-5.50%, which generally dampens mortgage origination volumes. This higher cost of borrowing can slow housing market activity, consequently affecting Security National's revenue from new loans and refinancing.

Furthermore, the company's cost of capital is directly tied to these interest rate trends. Higher rates increase the expense of funding operations and managing existing debt, potentially squeezing profit margins. For instance, if Security National relies heavily on variable-rate funding, a sustained period of elevated rates could lead to a noticeable increase in its operating expenses.

Inflation and Deflation

Inflationary pressures in 2024 and early 2025 continue to be a significant concern, potentially eroding the purchasing power of Security National's insurance payouts. For instance, if inflation averages 3.5% in 2024, a $100,000 payout today would effectively be worth less in future terms, impacting long-term policy value. This also raises the cost of doing business, from claims processing to employee wages, requiring careful repricing strategies.

Conversely, deflationary trends, while less prevalent currently, could lead to a decrease in asset values held by Security National, impacting investment returns. Reduced consumer spending during deflationary periods might also slow premium growth. Managing these opposing economic forces necessitates a robust approach to investment allocation and dynamic pricing models to safeguard profitability and policyholder interests.

Economic Growth and Recession Cycles

The overall health of the economy, measured by Gross Domestic Product (GDP) growth, significantly impacts consumer spending power and confidence. For instance, in the United States, real GDP grew at an annualized rate of 1.3% in the first quarter of 2024, a slowdown from previous periods, indicating a more cautious consumer environment.

Periods of economic expansion typically boost demand across various financial services. Higher disposable incomes during growth phases often translate to increased uptake of mortgage loans, life insurance policies, and even services like pre-need funeral planning as consumers feel more financially secure.

Conversely, economic downturns, or recessions, present considerable challenges. A recession can dampen demand for financial products, leading to higher mortgage default rates and an increase in life insurance policy lapses as individuals cut back on expenses or face financial hardship. For example, during the 2008 financial crisis, mortgage defaults surged, and insurance policy lapses rose, demonstrating the direct correlation between economic cycles and the financial services sector.

Consumer Spending and Debt Levels

Consumer spending is a critical driver for Security National, influencing demand for its diverse financial products. In the U.S., personal consumption expenditures rose by an annualized rate of 3.1% in the first quarter of 2024, indicating continued consumer confidence and a willingness to spend. This trend supports Security National's revenue streams from loans, investments, and insurance products.

Household debt levels also play a significant role. As of the first quarter of 2024, total household debt in the U.S. reached $17.7 trillion, with mortgage debt making up the largest portion. While this indicates borrowing activity, rising interest rates could strain consumers' ability to take on new debt or service existing obligations, potentially impacting Security National's mortgage and credit offerings.

- Consumer Spending Growth: U.S. personal consumption expenditures increased by 3.1% (annualized) in Q1 2024.

- Household Debt: Total U.S. household debt stood at $17.7 trillion in Q1 2024.

- Impact on Security National: Strong spending supports demand for financial services, while high debt could temper new borrowing.

- Interest Rate Sensitivity: Rising rates may affect consumers' capacity for new debt, impacting loan origination volumes.

Unemployment Rates

Unemployment rates are a critical barometer of an economy's well-being, directly influencing the financial resilience of households. For Security National, elevated unemployment presents a tangible risk. For instance, if unemployment climbs, we could see a rise in mortgage defaults, a slowdown in the uptake of new insurance products, and potentially an increase in claims from policyholders experiencing financial strain.

As of May 2024, the U.S. unemployment rate stood at 4.0%, a slight uptick from April's 3.9%. This figure, while still historically low, indicates a softening labor market.

- U.S. Unemployment Rate (May 2024): 4.0%

- Impact on Financial Services: Higher unemployment can correlate with increased loan delinquencies and reduced consumer spending on new financial products.

- Sector Vulnerability: Segments like mortgage insurance and life insurance can be particularly sensitive to economic downturns reflected in unemployment data.

- Risk Mitigation: Security National must monitor employment trends to adjust risk assessments and product offerings accordingly.

Financial Sector Faces Economic Crosscurrents

The economic landscape for Security National is shaped by a confluence of interest rates, inflation, and overall economic growth. Elevated interest rates, around 5.25%-5.50% as of mid-2025, temper mortgage demand and increase funding costs. Persistent inflation, averaging around 3.5% in 2024, erodes the real value of payouts and raises operational expenses.

Economic growth, reflected in a 1.3% annualized GDP increase in Q1 2024, influences consumer spending, which rose 3.1% in the same quarter. However, household debt, reaching $17.7 trillion in Q1 2024, combined with a 4.0% unemployment rate in May 2024, signals potential strain on consumers' ability to engage with financial products.

| Economic Factor | Metric/Trend | Impact on Security National |

|---|---|---|

| Interest Rates | 5.25%-5.50% (mid-2025 benchmark) | Dampens mortgage origination, increases funding costs. |

| Inflation | ~3.5% average in 2024 | Reduces purchasing power of payouts, raises operating costs. |

| GDP Growth (US) | 1.3% annualized (Q1 2024) | Indicates a more cautious consumer environment, potentially slowing demand. |

| Consumer Spending (US) | 3.1% annualized increase (Q1 2024) | Supports revenue from loans, investments, and insurance. |

| Household Debt (US) | $17.7 trillion (Q1 2024) | High levels may limit new borrowing capacity for consumers. |

| Unemployment Rate (US) | 4.0% (May 2024) | A softening labor market can lead to increased loan delinquencies and reduced demand. |

Full Version Awaits

Security National PESTLE Analysis

The preview you see here is the exact Security National PESTLE Analysis document you’ll receive after purchase. It's fully formatted and ready to use, providing a comprehensive overview of the factors influencing the company.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover the critical political, economic, and technological forces shaping Security National's trajectory. Our comprehensive PESTLE analysis provides actionable intelligence to inform your strategic decisions and competitive advantage. Download the full report now for expert insights.

Political factors

Government Regulatory Stance

Government policies and regulatory frameworks are pivotal for financial services, insurance, and mortgage sectors. For Security National Financial Corporation, shifts in oversight, such as increased capital requirements or enhanced consumer protection measures, directly influence profitability and operational expenses. For instance, the Dodd-Frank Act's ongoing impact, coupled with potential future regulatory adjustments in 2024 and 2025, necessitates continuous adaptation.

Political stability and the government's stance on market intervention are critical for investor confidence and strategic planning. A stable political environment fosters predictability, allowing companies like Security National to forecast growth and manage risks effectively. Conversely, political uncertainty or sudden policy changes can introduce volatility, impacting investment decisions and long-term business strategies.

Taxation Policies

Fluctuations in corporate tax rates directly impact Security National's bottom line. For instance, a potential increase in the U.S. federal corporate tax rate from 21% to 28% could reduce net income, affecting reinvestment and dividend capacity. Tax incentives for specific financial products, such as changes to mortgage interest deductibility or capital gains tax rates, can significantly alter consumer demand for Security National's mortgage and investment offerings.

Moreover, shifts in estate tax laws could influence the attractiveness of life insurance products, a key revenue driver for Security National. For example, if estate tax exemptions are lowered, demand for life insurance as an estate planning tool might rise. Conversely, unfavorable tax changes could dampen demand, impacting Security National's revenue streams and overall financial health.

Monetary Policy Influence

Central bank decisions significantly shape the mortgage market. For instance, the Federal Reserve's aggressive rate hikes throughout 2022 and 2023, pushing the federal funds rate from near zero to over 5%, directly impacted mortgage rates, which climbed from around 3% to over 7% for a 30-year fixed loan. This surge in borrowing costs cooled housing demand and refinancing, as anticipated, affecting loan origination volumes for institutions like Security National.

Looking ahead to 2024 and 2025, the trajectory of monetary policy remains a critical factor. Analysts anticipate potential rate cuts by the Federal Reserve in late 2024 or early 2025, contingent on inflation trends. Should inflation continue to moderate, a decrease in interest rates could reignite mortgage demand and refinancing, potentially boosting Security National's business, while persistent inflation might necessitate maintaining higher rates, thus continuing to pressure the housing market.

International Relations and Trade Policies

While Security National primarily operates domestically, shifts in international relations and trade policies can create ripple effects. For instance, changes in global trade agreements, such as potential renegotiations of existing pacts or the imposition of new tariffs, could indirectly impact the U.S. economy. This, in turn, influences consumer confidence and investment decisions, affecting demand for Security National's financial offerings.

The ongoing geopolitical landscape, including major power dynamics and regional conflicts, also plays a role. Instability abroad can lead to market volatility and affect investor sentiment, potentially dampening investment patterns. For example, the International Monetary Fund (IMF) projected global growth to be 3.2% in 2024, a slight slowdown from 2023, highlighting the interconnectedness of economies and the impact of global events on domestic financial markets.

- Trade Policy Impact: Fluctuations in trade tariffs and agreements can alter the cost of goods and services, indirectly affecting consumer spending power and business investment.

- Geopolitical Stability: Major international conflicts or political realignments can trigger global economic uncertainty, influencing investor confidence and capital flows into the U.S.

- Global Economic Growth: Slowdowns in major international economies, as indicated by IMF projections, can reduce export opportunities and dampen overall U.S. economic activity, impacting financial sector demand.

- Currency Fluctuations: International trade and investment often involve currency exchange, and significant shifts in exchange rates can impact the profitability of U.S. companies involved in international trade, indirectly affecting the broader financial environment.

Political Stability and Geopolitical Risks

Political stability is a cornerstone for business confidence, encouraging long-term investments. In 2024, countries with robust democratic institutions and predictable policy environments are likely to attract more foreign direct investment. For instance, the World Bank’s 2023 report highlighted that political stability is a key driver for economic growth, with stable nations seeing an average GDP growth rate 1.5% higher than unstable ones.

Conversely, geopolitical tensions and domestic political instability can inject significant economic uncertainty. This volatility can dampen consumer spending, particularly on discretionary financial products like life insurance. The ongoing conflicts in Eastern Europe, for example, have contributed to energy price volatility and supply chain disruptions globally, impacting consumer purchasing power and investment sentiment throughout 2024.

Market volatility often escalates during periods of political uncertainty. Investors tend to become more risk-averse, leading to capital flight from emerging markets or sectors perceived as politically exposed. This can affect the stability of real estate markets as well, with potential buyers delaying purchases amidst economic unpredictability. For example, in late 2023 and early 2024, several major economies experienced sharp, albeit temporary, downturns in real estate investment following unexpected political developments.

- Political Stability: Fosters business confidence and long-term investment.

- Geopolitical Risks: Can cause economic uncertainty and market volatility.

- Consumer Spending: Reduced during periods of political instability, impacting discretionary financial products.

- Real Estate Market: Susceptible to volatility due to economic uncertainty stemming from political factors.

Government, Tax, & Rates: Financial Market Dynamics

Government policies and regulatory frameworks are pivotal for financial services. Shifts in oversight, such as increased capital requirements or enhanced consumer protection measures, directly influence profitability and operational expenses for companies like Security National. For instance, the ongoing impact of the Dodd-Frank Act, coupled with potential future regulatory adjustments in 2024 and 2025, necessitates continuous adaptation.

Political stability and the government's stance on market intervention are critical for investor confidence and strategic planning. A stable political environment fosters predictability, allowing companies like Security National to forecast growth and manage risks effectively. Conversely, political uncertainty or sudden policy changes can introduce volatility, impacting investment decisions and long-term business strategies.

Fluctuations in corporate tax rates directly impact a company's bottom line. For example, a potential increase in the U.S. federal corporate tax rate from 21% could reduce net income, affecting reinvestment and dividend capacity. Tax incentives for specific financial products can also significantly alter consumer demand for offerings like mortgages and investments.

Central bank decisions significantly shape markets. For instance, the Federal Reserve's rate hikes throughout 2022 and 2023, pushing the federal funds rate from near zero to over 5%, directly impacted mortgage rates, which climbed from around 3% to over 7%. This surge in borrowing costs cooled housing demand and refinancing, affecting loan origination volumes.

What is included in the product

This PESTLE analysis provides a comprehensive examination of the external macro-environmental factors influencing Security National, detailing how Political, Economic, Social, Technological, Environmental, and Legal forces create both challenges and strategic advantages.

Provides a concise version that can be dropped into PowerPoints or used in group planning sessions, simplifying complex external factors into actionable insights.

Economic factors

Interest Rate Environment

The prevailing interest rate environment significantly impacts Security National, especially its mortgage loan operations. As of mid-2025, the Federal Reserve's benchmark interest rate remains elevated, hovering around 5.25%-5.50%, which generally dampens mortgage origination volumes. This higher cost of borrowing can slow housing market activity, consequently affecting Security National's revenue from new loans and refinancing.

Furthermore, the company's cost of capital is directly tied to these interest rate trends. Higher rates increase the expense of funding operations and managing existing debt, potentially squeezing profit margins. For instance, if Security National relies heavily on variable-rate funding, a sustained period of elevated rates could lead to a noticeable increase in its operating expenses.

Inflation and Deflation

Inflationary pressures in 2024 and early 2025 continue to be a significant concern, potentially eroding the purchasing power of Security National's insurance payouts. For instance, if inflation averages 3.5% in 2024, a $100,000 payout today would effectively be worth less in future terms, impacting long-term policy value. This also raises the cost of doing business, from claims processing to employee wages, requiring careful repricing strategies.

Conversely, deflationary trends, while less prevalent currently, could lead to a decrease in asset values held by Security National, impacting investment returns. Reduced consumer spending during deflationary periods might also slow premium growth. Managing these opposing economic forces necessitates a robust approach to investment allocation and dynamic pricing models to safeguard profitability and policyholder interests.

Economic Growth and Recession Cycles

The overall health of the economy, measured by Gross Domestic Product (GDP) growth, significantly impacts consumer spending power and confidence. For instance, in the United States, real GDP grew at an annualized rate of 1.3% in the first quarter of 2024, a slowdown from previous periods, indicating a more cautious consumer environment.

Periods of economic expansion typically boost demand across various financial services. Higher disposable incomes during growth phases often translate to increased uptake of mortgage loans, life insurance policies, and even services like pre-need funeral planning as consumers feel more financially secure.

Conversely, economic downturns, or recessions, present considerable challenges. A recession can dampen demand for financial products, leading to higher mortgage default rates and an increase in life insurance policy lapses as individuals cut back on expenses or face financial hardship. For example, during the 2008 financial crisis, mortgage defaults surged, and insurance policy lapses rose, demonstrating the direct correlation between economic cycles and the financial services sector.

Consumer Spending and Debt Levels

Consumer spending is a critical driver for Security National, influencing demand for its diverse financial products. In the U.S., personal consumption expenditures rose by an annualized rate of 3.1% in the first quarter of 2024, indicating continued consumer confidence and a willingness to spend. This trend supports Security National's revenue streams from loans, investments, and insurance products.

Household debt levels also play a significant role. As of the first quarter of 2024, total household debt in the U.S. reached $17.7 trillion, with mortgage debt making up the largest portion. While this indicates borrowing activity, rising interest rates could strain consumers' ability to take on new debt or service existing obligations, potentially impacting Security National's mortgage and credit offerings.

- Consumer Spending Growth: U.S. personal consumption expenditures increased by 3.1% (annualized) in Q1 2024.

- Household Debt: Total U.S. household debt stood at $17.7 trillion in Q1 2024.

- Impact on Security National: Strong spending supports demand for financial services, while high debt could temper new borrowing.

- Interest Rate Sensitivity: Rising rates may affect consumers' capacity for new debt, impacting loan origination volumes.

Unemployment Rates

Unemployment rates are a critical barometer of an economy's well-being, directly influencing the financial resilience of households. For Security National, elevated unemployment presents a tangible risk. For instance, if unemployment climbs, we could see a rise in mortgage defaults, a slowdown in the uptake of new insurance products, and potentially an increase in claims from policyholders experiencing financial strain.

As of May 2024, the U.S. unemployment rate stood at 4.0%, a slight uptick from April's 3.9%. This figure, while still historically low, indicates a softening labor market.

- U.S. Unemployment Rate (May 2024): 4.0%

- Impact on Financial Services: Higher unemployment can correlate with increased loan delinquencies and reduced consumer spending on new financial products.

- Sector Vulnerability: Segments like mortgage insurance and life insurance can be particularly sensitive to economic downturns reflected in unemployment data.

- Risk Mitigation: Security National must monitor employment trends to adjust risk assessments and product offerings accordingly.

Financial Sector Faces Economic Crosscurrents

The economic landscape for Security National is shaped by a confluence of interest rates, inflation, and overall economic growth. Elevated interest rates, around 5.25%-5.50% as of mid-2025, temper mortgage demand and increase funding costs. Persistent inflation, averaging around 3.5% in 2024, erodes the real value of payouts and raises operational expenses.

Economic growth, reflected in a 1.3% annualized GDP increase in Q1 2024, influences consumer spending, which rose 3.1% in the same quarter. However, household debt, reaching $17.7 trillion in Q1 2024, combined with a 4.0% unemployment rate in May 2024, signals potential strain on consumers' ability to engage with financial products.

| Economic Factor | Metric/Trend | Impact on Security National |

|---|---|---|

| Interest Rates | 5.25%-5.50% (mid-2025 benchmark) | Dampens mortgage origination, increases funding costs. |

| Inflation | ~3.5% average in 2024 | Reduces purchasing power of payouts, raises operating costs. |

| GDP Growth (US) | 1.3% annualized (Q1 2024) | Indicates a more cautious consumer environment, potentially slowing demand. |

| Consumer Spending (US) | 3.1% annualized increase (Q1 2024) | Supports revenue from loans, investments, and insurance. |

| Household Debt (US) | $17.7 trillion (Q1 2024) | High levels may limit new borrowing capacity for consumers. |

| Unemployment Rate (US) | 4.0% (May 2024) | A softening labor market can lead to increased loan delinquencies and reduced demand. |

Full Version Awaits

Security National PESTLE Analysis

The preview you see here is the exact Security National PESTLE Analysis document you’ll receive after purchase. It's fully formatted and ready to use, providing a comprehensive overview of the factors influencing the company.