SDCL Energy Efficiency Income Trust Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

The SDCL Energy Efficiency Income Trust operates within a sector influenced by moderate buyer power and significant supplier leverage, particularly for specialized components. The threat of new entrants is somewhat constrained by capital requirements and regulatory hurdles, while the intensity of rivalry among existing players is notable. The availability of substitutes, though present, often comes with performance trade-offs.

The complete report reveals the real forces shaping SDCL Energy Efficiency Income Trust’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Specialization

The energy efficiency sector, especially for niche infrastructure like trigeneration plants, often depends on a small group of specialized equipment makers. For instance, advanced waste heat recovery systems might only have a few global manufacturers with the necessary patents and technical know-how.

When these suppliers are few and their technology is unique, they gain considerable leverage. This concentration means SEEIT might face higher equipment prices or longer delivery schedules, directly impacting project economics and the trust's ability to deploy capital efficiently.

Switching Costs for SEEIT

Switching suppliers for SEEIT's energy efficiency infrastructure can incur substantial costs. These include expenses related to redesigning systems, re-qualifying components, and retraining personnel, all of which can significantly disrupt ongoing operations and future project timelines. For instance, the integration of new, specialized energy management systems might require extensive testing and validation, potentially delaying project completion by several months.

These high switching costs effectively increase the bargaining power of SEEIT's current suppliers. Suppliers are aware that moving to an alternative provider would be both time-consuming and expensive for SEEIT, allowing them to negotiate more favorable pricing and contract terms. This dynamic can lead to higher operational costs for SEEIT if suppliers leverage this advantage. In 2024, the average cost for re-engineering and re-qualifying specialized industrial components across the energy sector has been estimated to range from 15% to 25% of the initial system's value.

Uniqueness of Inputs

The uniqueness of inputs significantly impacts the bargaining power of suppliers for SDCL Energy Efficiency Income Trust (SEEIT). For instance, specialized energy efficiency solutions like advanced metering infrastructure or proprietary optimization software may only be available from a limited number of suppliers. If these unique inputs are crucial for SEEIT's projects, suppliers can exert considerable leverage, particularly when dealing with patented or highly specialized technologies.

Threat of Forward Integration by Suppliers

Suppliers possessing substantial technical acumen or significant financial resources might consider integrating forward. This means they could start developing and operating energy efficiency projects directly, effectively becoming competitors to SDCL Energy Efficiency Income Trust (SEEIT).

While this is less likely for straightforward equipment manufacturers, it's a plausible scenario for large engineering or technology companies. These firms could decide to offer complete energy solutions, thereby bypassing investment entities like SEEIT.

- Potential Competitors: Large engineering firms or technology providers with capital could enter the project development space.

- Market Disruption: Forward integration by suppliers could directly challenge SEEIT's business model.

- Expertise Leverage: Suppliers with deep technical knowledge are well-positioned to undertake project development.

Impact of Regulatory and Policy Landscape on Suppliers

The evolving regulatory landscape, particularly concerning energy efficiency and decarbonization, significantly influences supplier bargaining power. These mandates can boost demand for suppliers offering compliant solutions, but stringent standards can also reduce the pool of qualified providers. This limitation, coupled with compliance and certification hurdles, grants those who meet the criteria enhanced leverage.

For instance, in 2024, the EU's updated Ecodesign for Sustainable Products Regulation (ESPR) is expected to further tighten requirements for energy-consuming products, potentially consolidating the market around a smaller number of highly specialized suppliers. This regulatory push creates a scenario where suppliers with proven track records in meeting these advanced efficiency and environmental standards can command higher prices and more favorable terms.

- Increased Demand: Regulatory mandates for energy efficiency drive demand for compliant products and services.

- Supplier Consolidation: Stringent standards can limit the number of qualified suppliers, creating a more concentrated market.

- Compliance Costs: The expense and complexity of meeting new regulations can act as a barrier to entry, further empowering existing compliant suppliers.

- Certification Advantage: Suppliers holding relevant certifications (e.g., ISO 14001, energy performance labels) gain a competitive edge and stronger bargaining power.

Supplier Leverage: A Critical Factor for Energy Efficiency Trust

The bargaining power of suppliers for SDCL Energy Efficiency Income Trust (SEEIT) is moderately high due to the specialized nature of energy efficiency equipment and the potential for forward integration by key providers. The trust often relies on a limited number of manufacturers for critical components like advanced trigeneration systems or proprietary energy management software. This reliance is exacerbated by high switching costs, which can involve significant re-engineering and re-qualification expenses, estimated in 2024 to be between 15% and 25% of initial system value.

| Factor | Impact on SEEIT | 2024 Data/Example |

| Supplier Concentration | High | Limited number of manufacturers for specialized trigeneration components. |

| Uniqueness of Inputs | High | Proprietary energy management software, patented heat recovery systems. |

| Switching Costs | High | Estimated 15-25% of system value for re-engineering/re-qualification in 2024. |

| Forward Integration Threat | Moderate | Large engineering firms could offer complete energy solutions, bypassing investment trusts. |

| Regulatory Influence | High | EU's ESPR 2024 may consolidate market around compliant, specialized suppliers. |

What is included in the product

This Porter's Five Forces analysis for SDCL Energy Efficiency Income Trust assesses the competitive intensity and attractiveness of the energy efficiency investment market, examining supplier power, buyer power, threat of new entrants, threat of substitutes, and industry rivalry.

Effortlessly navigate the competitive landscape of energy efficiency investments by understanding the SDCL Energy Efficiency Income Trust's Porter's Five Forces analysis, presented in a clear, one-sheet summary ideal for quick strategic decision-making.

Customers Bargaining Power

Long-Term Contractual Agreements

SDCL Energy Efficiency Income Trust (SEEIT) strategically utilizes long-term contractual agreements with strong, creditworthy customers. This approach significantly dampens the bargaining power of these customers throughout the contract's duration, ensuring predictable revenue for SEEIT.

These extended contracts, often spanning many years, lock in terms and limit the customer's ability to seek alternative providers or demand frequent renegotiations, thereby solidifying SEEIT's income stability.

High Switching Costs for Customers

For commercial, industrial, and public sector clients of SDCL Energy Efficiency Income Trust, the decision to switch away from an integrated energy efficiency solution, such as a trigeneration plant or district heating system, carries significant switching costs. These costs encompass the financial outlay and operational disruption associated with decommissioning existing infrastructure and installing new systems.

The process of switching providers can also lead to potential operational downtime, further increasing the overall expense and inconvenience for customers. Consequently, once a client has invested in and integrated an energy efficiency solution provided by SDCL, they become less inclined to seek alternative providers due to these substantial barriers to entry.

Customer's Importance to SEEIT's Portfolio

While SDCL Energy Efficiency Income Trust (SEEIT) boasts a diversified portfolio, certain large anchor clients or significant industrial users can represent a substantial portion of revenue for specific projects. This concentration means the loss of a major customer could indeed impact a project's financial viability, granting these larger clients some negotiation leverage, especially if their energy needs change.

Price Sensitivity vs. Value Proposition

Customers are indeed influenced by cost savings, the desire for cleaner energy solutions, and reliable energy supply. While price sensitivity is a natural consideration, SDCL Energy Efficiency Income Trust's (SEEIT) value proposition often shifts the focus beyond mere cost.

The long-term operational savings, coupled with significant reductions in carbon emissions and improvements in energy security, can present a compelling case that outweighs a purely price-driven decision for many clients. This emphasis on holistic value, particularly for environmentally conscious customers, can mitigate the direct price bargaining power they might otherwise exert.

- Customer Focus: Driven by cost savings, cleaner energy, and reliability.

- Value Beyond Price: Long-term operational savings, reduced carbon emissions, and enhanced energy security are key differentiators.

- ESG Influence: Prioritizing Environmental, Social, and Governance (ESG) goals can reduce direct price bargaining power.

- SEEIT's Position: The trust's focus on value rather than just cost strengthens its ability to command favorable terms.

Limited Threat of Backward Integration by Customers

Most of SDCL Energy Efficiency Income Trust's (SEEIT) commercial, industrial, and public sector customers find it difficult to integrate backward. This is due to the significant specialized expertise, substantial capital investment, and crucial regulatory approvals needed to build and manage sophisticated energy efficiency infrastructure. For instance, developing a district heating network or a large-scale solar farm requires deep technical knowledge and compliance with numerous environmental and safety standards.

These high barriers to entry effectively prevent customers from becoming their own energy efficiency solution providers. Consequently, this limits their ability to exert significant bargaining power over SEEIT, as they are reliant on the trust’s specialized services and infrastructure development capabilities.

- High Capital Requirements: Developing energy efficiency projects often demands millions, if not billions, in upfront investment, a significant hurdle for most individual customers.

- Specialized Expertise Needed: Operating complex systems like combined heat and power (CHP) plants or advanced building management systems requires highly skilled engineers and technicians.

- Regulatory Hurdles: Obtaining permits and adhering to energy regulations can be a lengthy and complex process, discouraging backward integration.

- Limited Customer Scale: For many individual customers, the scale of their energy needs may not justify the immense cost and effort of developing their own integrated energy efficiency solutions.

Customer Power: Limited by Long-Term Contracts & ESG Focus

Customers of SDCL Energy Efficiency Income Trust (SEEIT) have limited bargaining power due to high switching costs and the trust's integrated service model. Long-term contracts, often exceeding 10-15 years, lock in terms and reduce the incentive for customers to renegotiate or seek alternatives. For example, a customer investing in a district heating system faces substantial costs and operational disruption if they were to switch providers.

While cost savings are a primary driver for customers, SEEIT's value proposition extends to reliable energy and significant carbon emission reductions. This focus on holistic benefits, particularly ESG advantages, often outweighs purely price-based negotiations. For instance, in 2024, SEEIT reported that its projects contributed to a reduction of over 500,000 tonnes of CO2 equivalent annually across its portfolio.

Furthermore, customers generally lack the specialized expertise and capital required for backward integration into energy efficiency solutions. This reliance on SEEIT's capabilities limits their ability to exert significant pressure on pricing or contract terms, reinforcing the trust's stable revenue streams.

Same Document Delivered

SDCL Energy Efficiency Income Trust Porter's Five Forces Analysis

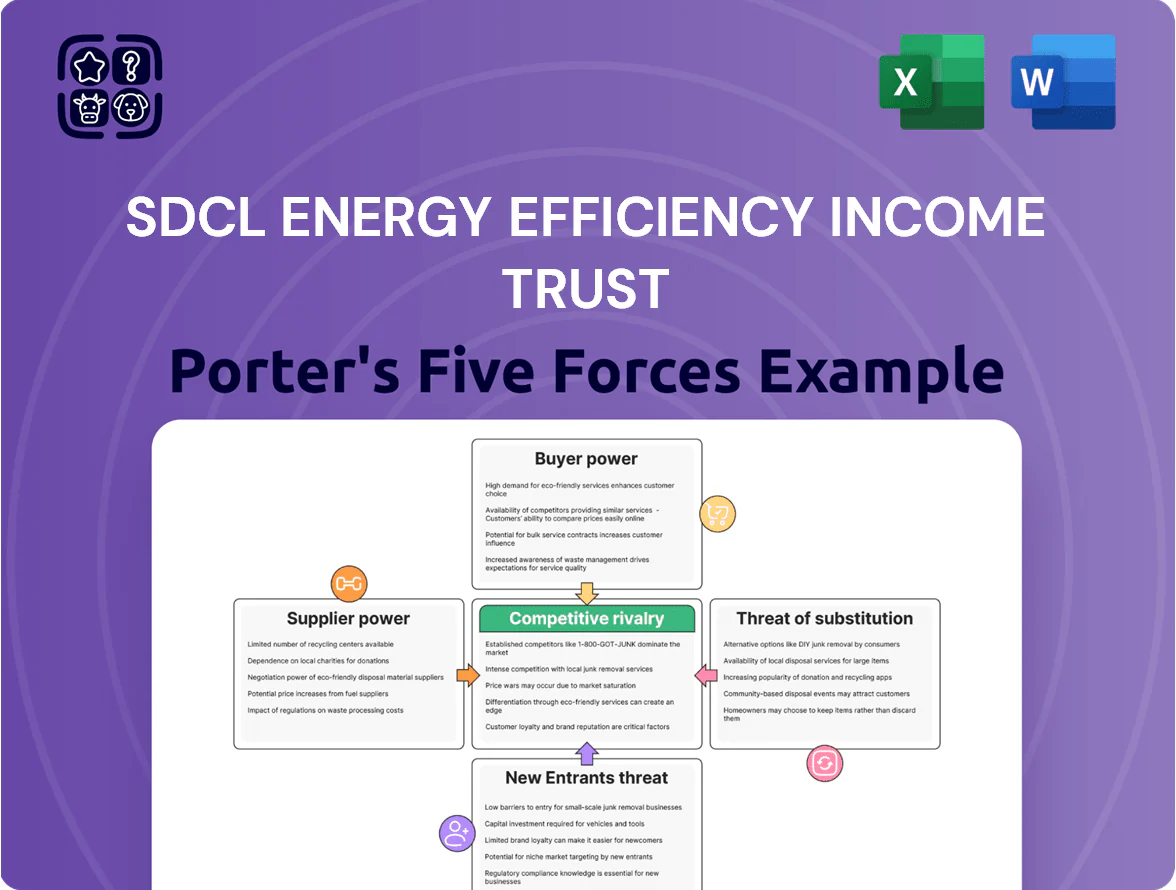

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Porter's Five Forces analysis for SDCL Energy Efficiency Income Trust details the intense competitive rivalry, highlighting how the trust navigates a market with numerous similar income-generating entities. It also thoroughly examines the moderate threat of new entrants, influenced by capital requirements and regulatory hurdles, and the low bargaining power of buyers due to the essential nature of energy efficiency services. Furthermore, the analysis assesses the moderate threat of substitutes, considering alternative investment vehicles, and the low bargaining power of suppliers, reflecting the trust's diversified operational base.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

The SDCL Energy Efficiency Income Trust operates within a sector influenced by moderate buyer power and significant supplier leverage, particularly for specialized components. The threat of new entrants is somewhat constrained by capital requirements and regulatory hurdles, while the intensity of rivalry among existing players is notable. The availability of substitutes, though present, often comes with performance trade-offs.

The complete report reveals the real forces shaping SDCL Energy Efficiency Income Trust’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Specialization

The energy efficiency sector, especially for niche infrastructure like trigeneration plants, often depends on a small group of specialized equipment makers. For instance, advanced waste heat recovery systems might only have a few global manufacturers with the necessary patents and technical know-how.

When these suppliers are few and their technology is unique, they gain considerable leverage. This concentration means SEEIT might face higher equipment prices or longer delivery schedules, directly impacting project economics and the trust's ability to deploy capital efficiently.

Switching Costs for SEEIT

Switching suppliers for SEEIT's energy efficiency infrastructure can incur substantial costs. These include expenses related to redesigning systems, re-qualifying components, and retraining personnel, all of which can significantly disrupt ongoing operations and future project timelines. For instance, the integration of new, specialized energy management systems might require extensive testing and validation, potentially delaying project completion by several months.

These high switching costs effectively increase the bargaining power of SEEIT's current suppliers. Suppliers are aware that moving to an alternative provider would be both time-consuming and expensive for SEEIT, allowing them to negotiate more favorable pricing and contract terms. This dynamic can lead to higher operational costs for SEEIT if suppliers leverage this advantage. In 2024, the average cost for re-engineering and re-qualifying specialized industrial components across the energy sector has been estimated to range from 15% to 25% of the initial system's value.

Uniqueness of Inputs

The uniqueness of inputs significantly impacts the bargaining power of suppliers for SDCL Energy Efficiency Income Trust (SEEIT). For instance, specialized energy efficiency solutions like advanced metering infrastructure or proprietary optimization software may only be available from a limited number of suppliers. If these unique inputs are crucial for SEEIT's projects, suppliers can exert considerable leverage, particularly when dealing with patented or highly specialized technologies.

Threat of Forward Integration by Suppliers

Suppliers possessing substantial technical acumen or significant financial resources might consider integrating forward. This means they could start developing and operating energy efficiency projects directly, effectively becoming competitors to SDCL Energy Efficiency Income Trust (SEEIT).

While this is less likely for straightforward equipment manufacturers, it's a plausible scenario for large engineering or technology companies. These firms could decide to offer complete energy solutions, thereby bypassing investment entities like SEEIT.

- Potential Competitors: Large engineering firms or technology providers with capital could enter the project development space.

- Market Disruption: Forward integration by suppliers could directly challenge SEEIT's business model.

- Expertise Leverage: Suppliers with deep technical knowledge are well-positioned to undertake project development.

Impact of Regulatory and Policy Landscape on Suppliers

The evolving regulatory landscape, particularly concerning energy efficiency and decarbonization, significantly influences supplier bargaining power. These mandates can boost demand for suppliers offering compliant solutions, but stringent standards can also reduce the pool of qualified providers. This limitation, coupled with compliance and certification hurdles, grants those who meet the criteria enhanced leverage.

For instance, in 2024, the EU's updated Ecodesign for Sustainable Products Regulation (ESPR) is expected to further tighten requirements for energy-consuming products, potentially consolidating the market around a smaller number of highly specialized suppliers. This regulatory push creates a scenario where suppliers with proven track records in meeting these advanced efficiency and environmental standards can command higher prices and more favorable terms.

- Increased Demand: Regulatory mandates for energy efficiency drive demand for compliant products and services.

- Supplier Consolidation: Stringent standards can limit the number of qualified suppliers, creating a more concentrated market.

- Compliance Costs: The expense and complexity of meeting new regulations can act as a barrier to entry, further empowering existing compliant suppliers.

- Certification Advantage: Suppliers holding relevant certifications (e.g., ISO 14001, energy performance labels) gain a competitive edge and stronger bargaining power.

Supplier Leverage: A Critical Factor for Energy Efficiency Trust

The bargaining power of suppliers for SDCL Energy Efficiency Income Trust (SEEIT) is moderately high due to the specialized nature of energy efficiency equipment and the potential for forward integration by key providers. The trust often relies on a limited number of manufacturers for critical components like advanced trigeneration systems or proprietary energy management software. This reliance is exacerbated by high switching costs, which can involve significant re-engineering and re-qualification expenses, estimated in 2024 to be between 15% and 25% of initial system value.

| Factor | Impact on SEEIT | 2024 Data/Example |

| Supplier Concentration | High | Limited number of manufacturers for specialized trigeneration components. |

| Uniqueness of Inputs | High | Proprietary energy management software, patented heat recovery systems. |

| Switching Costs | High | Estimated 15-25% of system value for re-engineering/re-qualification in 2024. |

| Forward Integration Threat | Moderate | Large engineering firms could offer complete energy solutions, bypassing investment trusts. |

| Regulatory Influence | High | EU's ESPR 2024 may consolidate market around compliant, specialized suppliers. |

What is included in the product

This Porter's Five Forces analysis for SDCL Energy Efficiency Income Trust assesses the competitive intensity and attractiveness of the energy efficiency investment market, examining supplier power, buyer power, threat of new entrants, threat of substitutes, and industry rivalry.

Effortlessly navigate the competitive landscape of energy efficiency investments by understanding the SDCL Energy Efficiency Income Trust's Porter's Five Forces analysis, presented in a clear, one-sheet summary ideal for quick strategic decision-making.

Customers Bargaining Power

Long-Term Contractual Agreements

SDCL Energy Efficiency Income Trust (SEEIT) strategically utilizes long-term contractual agreements with strong, creditworthy customers. This approach significantly dampens the bargaining power of these customers throughout the contract's duration, ensuring predictable revenue for SEEIT.

These extended contracts, often spanning many years, lock in terms and limit the customer's ability to seek alternative providers or demand frequent renegotiations, thereby solidifying SEEIT's income stability.

High Switching Costs for Customers

For commercial, industrial, and public sector clients of SDCL Energy Efficiency Income Trust, the decision to switch away from an integrated energy efficiency solution, such as a trigeneration plant or district heating system, carries significant switching costs. These costs encompass the financial outlay and operational disruption associated with decommissioning existing infrastructure and installing new systems.

The process of switching providers can also lead to potential operational downtime, further increasing the overall expense and inconvenience for customers. Consequently, once a client has invested in and integrated an energy efficiency solution provided by SDCL, they become less inclined to seek alternative providers due to these substantial barriers to entry.

Customer's Importance to SEEIT's Portfolio

While SDCL Energy Efficiency Income Trust (SEEIT) boasts a diversified portfolio, certain large anchor clients or significant industrial users can represent a substantial portion of revenue for specific projects. This concentration means the loss of a major customer could indeed impact a project's financial viability, granting these larger clients some negotiation leverage, especially if their energy needs change.

Price Sensitivity vs. Value Proposition

Customers are indeed influenced by cost savings, the desire for cleaner energy solutions, and reliable energy supply. While price sensitivity is a natural consideration, SDCL Energy Efficiency Income Trust's (SEEIT) value proposition often shifts the focus beyond mere cost.

The long-term operational savings, coupled with significant reductions in carbon emissions and improvements in energy security, can present a compelling case that outweighs a purely price-driven decision for many clients. This emphasis on holistic value, particularly for environmentally conscious customers, can mitigate the direct price bargaining power they might otherwise exert.

- Customer Focus: Driven by cost savings, cleaner energy, and reliability.

- Value Beyond Price: Long-term operational savings, reduced carbon emissions, and enhanced energy security are key differentiators.

- ESG Influence: Prioritizing Environmental, Social, and Governance (ESG) goals can reduce direct price bargaining power.

- SEEIT's Position: The trust's focus on value rather than just cost strengthens its ability to command favorable terms.

Limited Threat of Backward Integration by Customers

Most of SDCL Energy Efficiency Income Trust's (SEEIT) commercial, industrial, and public sector customers find it difficult to integrate backward. This is due to the significant specialized expertise, substantial capital investment, and crucial regulatory approvals needed to build and manage sophisticated energy efficiency infrastructure. For instance, developing a district heating network or a large-scale solar farm requires deep technical knowledge and compliance with numerous environmental and safety standards.

These high barriers to entry effectively prevent customers from becoming their own energy efficiency solution providers. Consequently, this limits their ability to exert significant bargaining power over SEEIT, as they are reliant on the trust’s specialized services and infrastructure development capabilities.

- High Capital Requirements: Developing energy efficiency projects often demands millions, if not billions, in upfront investment, a significant hurdle for most individual customers.

- Specialized Expertise Needed: Operating complex systems like combined heat and power (CHP) plants or advanced building management systems requires highly skilled engineers and technicians.

- Regulatory Hurdles: Obtaining permits and adhering to energy regulations can be a lengthy and complex process, discouraging backward integration.

- Limited Customer Scale: For many individual customers, the scale of their energy needs may not justify the immense cost and effort of developing their own integrated energy efficiency solutions.

Customer Power: Limited by Long-Term Contracts & ESG Focus

Customers of SDCL Energy Efficiency Income Trust (SEEIT) have limited bargaining power due to high switching costs and the trust's integrated service model. Long-term contracts, often exceeding 10-15 years, lock in terms and reduce the incentive for customers to renegotiate or seek alternatives. For example, a customer investing in a district heating system faces substantial costs and operational disruption if they were to switch providers.

While cost savings are a primary driver for customers, SEEIT's value proposition extends to reliable energy and significant carbon emission reductions. This focus on holistic benefits, particularly ESG advantages, often outweighs purely price-based negotiations. For instance, in 2024, SEEIT reported that its projects contributed to a reduction of over 500,000 tonnes of CO2 equivalent annually across its portfolio.

Furthermore, customers generally lack the specialized expertise and capital required for backward integration into energy efficiency solutions. This reliance on SEEIT's capabilities limits their ability to exert significant pressure on pricing or contract terms, reinforcing the trust's stable revenue streams.

Same Document Delivered

SDCL Energy Efficiency Income Trust Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Porter's Five Forces analysis for SDCL Energy Efficiency Income Trust details the intense competitive rivalry, highlighting how the trust navigates a market with numerous similar income-generating entities. It also thoroughly examines the moderate threat of new entrants, influenced by capital requirements and regulatory hurdles, and the low bargaining power of buyers due to the essential nature of energy efficiency services. Furthermore, the analysis assesses the moderate threat of substitutes, considering alternative investment vehicles, and the low bargaining power of suppliers, reflecting the trust's diversified operational base.