Sumitomo Electric Boston Consulting Group Matrix

Unlock Strategic Clarity

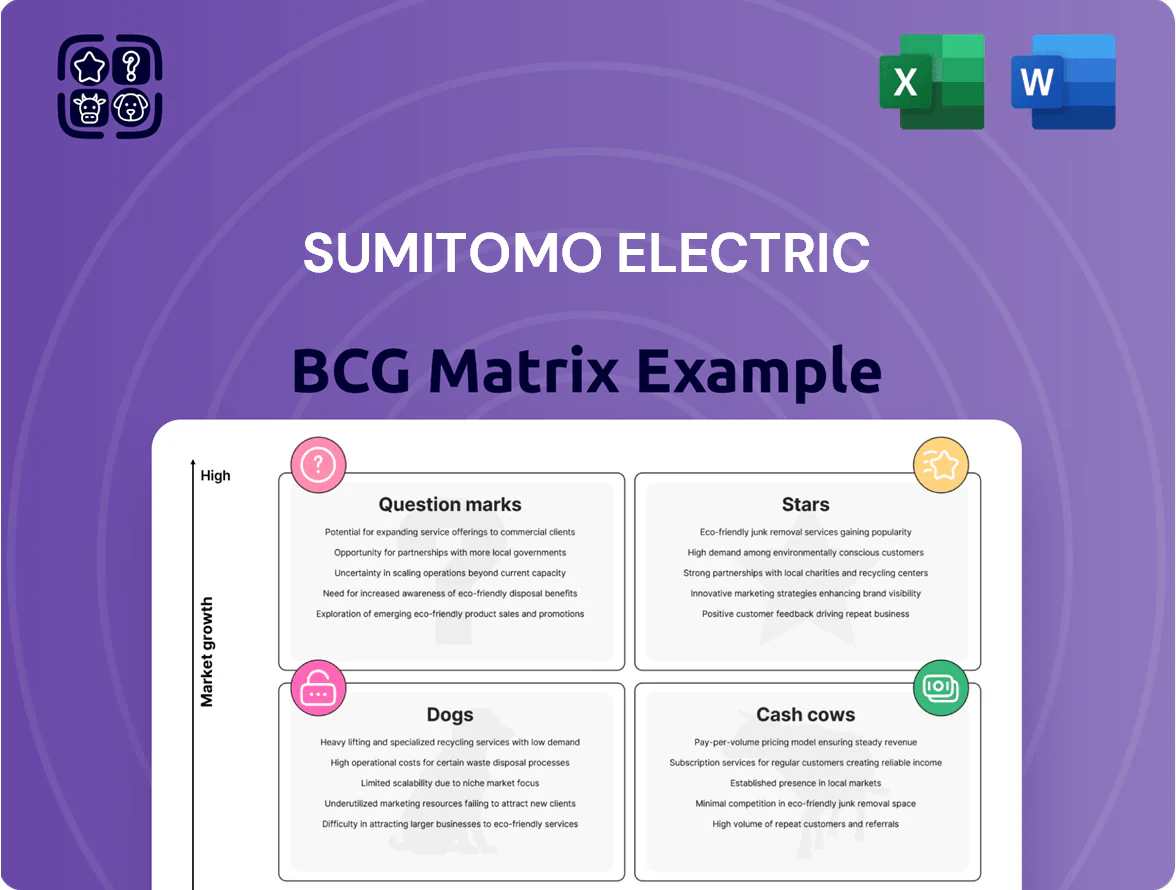

Sumitomo Electric’s BCG Matrix preview highlights how its diverse portfolio—spanning power cables, automotive wire harnesses, and electronic materials—maps across growth and market share; some segments show star potential in EV and renewable infrastructure, while legacy businesses act as steady cash cows. This snapshot reveals strategic pressures and capital allocation choices critical for future competitiveness. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a ready-to-use Word + Excel package to guide investment and operational decisions.

Stars

High-Voltage Direct Current (HVDC) Cables

Sumitomo Electric holds a top global share in HVDC subsea and terrestrial cables, supplying roughly 25% of large-scale offshore interconnector projects in 2024 while revenues from power-cable systems rose 18% to ¥210 billion in FY2024 (ended Mar 2025).

HVDC links are critical for tying offshore wind to grids; project backlog for HVDC contracts grew to ¥430 billion by Dec 2025, driven by Europe and Asia tenders.

The company is expanding HVDC manufacturing with ¥120 billion CAPEX planned through 2026 to lift capacity ~40%, aiming to meet projected global demand of 40–60 GW annual HVDC installations by 2030.

Next-Generation Automotive Wiring Harnesses

The shift to EVs and software-defined vehicles has raised wiring harness complexity and value; global high-voltage harness content per EV rose to about $750–1,200 in 2024, boosting addressable market to ~$18bn by 2025.

Sumitomo Electric, world's top supplier for EV harnesses, reported automotive segment sales of ¥1.1 trillion in FY2024, with high-voltage harnesses driving double-digit growth and >20% segment operating margin.

These harnesses demand heavy R&D—Sumitomo spent ¥46.3 billion on R&D in FY2024, much allocated to EV/high-voltage systems—but they remain the automotive division’s primary growth engine.

Optical Fiber and Communication Infrastructure

Optical Fiber and Communication Infrastructure sits as a Star: global 5G rollouts and AI-driven data center growth keep high-density fiber demand at peak—global fiber market hit $15.6B in 2024, growing ~8% CAGR to 2029. Sumitomo Electric, a top-tier supplier, uses proprietary manufacturing (e.g., advanced MCVD processes) to sustain margins; FY2024 optical segment revenue ~¥300bn. Heavy, continuous capex is required to match node densification and tech shifts.

Power Modules for Electric Vehicles

Sumitomo Electric’s Power Modules for EVs sits in the BCG Matrix as a star: the company holds roughly 18–22% share of the specialized EV inverter module market (2025 estimate) while the segment grows ~25% CAGR to 2028 as vehicle electrification reaches mass market.

SiC (silicon carbide) integration drives competitive advantage—Sumitomo plans capacity expansions in 2024–25 targeting >30% SiC content in modules by 2026 to cut losses and boost efficiency, supporting sustained high growth.

- High market share: ~18–22% (2025 est.)

- Segment growth: ~25% CAGR to 2028

- SiC target: >30% module content by 2026

- CapEx: ramped 2024–25 to expand SiC capacity

Advanced Traffic Management Systems

Advanced Traffic Management Systems are a Star for Sumitomo Electric: their sensing and V2X (vehicle-to-everything) comms are critical to smart cities and autonomous-driving infrastructure, supporting a c.35% market share in Japan and contributing to a segment that McKinsey estimated at $130–$180bn global mobility infrastructure spend by 2030.

High R&D intensity: Sumitomo spent ¥92.4bn on R&D in FY2024, with a growing portion toward sensors and roadside units as urban centers modernize transport grids worldwide.

Rapid market expansion: global demand for ITS (intelligent transport systems) is growing ~8–10% CAGR (2024–2030), positioning this unit for revenue and margin expansion versus mature cables and optical businesses.

- Strong Japan share ~35%

- R&D FY2024 ¥92.4bn

- Global ITS CAGR ~8–10% (2024–2030)

- Market opportunity: $130–$180bn by 2030

High-growth leaders: HVDC, EV harnesses, fiber, SiC modules & ITS power expansion

Stars: HVDC & EV harnesses, optical fiber, SiC power modules, ITS—each shows high market share and fast growth with FY2024/FY2025 figures supporting expansion.

| Business | Share | Growth | Key FY |

|---|---|---|---|

| HVDC cables | ~25% | backlog ↑ to ¥430bn (Dec 2025) | Power cables ¥210bn FY2024 |

| EV harnesses | world lead | addressable ~$18bn (2025) | Auto ¥1.1tn FY2024 |

| Optical fiber | top-tier | global market $15.6bn (2024) | Optical ¥300bn FY2024 |

| Power modules (SiC) | 18–22% (2025 est.) | ~25% CAGR to 2028 | SiC target >30% by 2026 |

| ITS / V2X | ~35% Japan | 8–10% CAGR (2024–30) | Mobility $130–180bn by 2030 |

What is included in the product

Comprehensive BCG Matrix of Sumitomo Electric: quadrant-by-quadrant strategic guidance on investment, retention, or divestment amid market trends.

One-page overview placing each Sumitomo Electric business unit in a BCG quadrant for clear portfolio decisions

Cash Cows

Standard Automotive Wiring Harnesses

Standard automotive wiring harnesses for internal combustion engine vehicles remain a cash cow for Sumitomo Electric, delivering steady revenue—about ¥220 billion in FY2024 (roughly $1.6 billion)—and sustaining high market share in a mature global market. Manufacturing is optimized with >80% capacity utilization and gross margins near 18–20%, producing predictable free cash flow. This reliable cash funds R&D and capital allocation toward green-energy products and high-voltage systems development. The segment’s stability offsets volatility as the company scales EV and advanced-electronics investments.

Flexible Printed Circuits (FPCs)

Sumitomo Electric’s Flexible Printed Circuits (FPCs) business is a market leader for smartphones, tablets and consumer electronics, delivering steady operating cash given a global FPC market share estimated around 12–15% in 2024 and annual sales roughly JPY 120–150 billion (≈USD 0.8–1.1bn) for the unit.

Smartphone unit volume growth slowed to ~2% CAGR 2021–2024, so FPCs are low-growth but high-margin cash cows, requiring minimal capex—management reports capex intensity below 5% of sales for the segment in FY2024.

Long-term OEM contracts with Apple, Samsung and other major electronics manufacturers secure predictable order flow and working-capital generation, keeping free cash flow conversion high (estimated >15% FCF margin in 2024).

Cemented Carbide Tools

Sumitomo Electric’s industrial materials division, led by cemented carbide cutting tools, sits in a mature global market worth about $25bn in 2024, growing ~2% annually; Sumitomo holds an estimated 12–15% share in high-precision aerospace and automotive niches.

These tools deliver high gross margins—roughly 40–50% on product lines—and steady free cash flow, with R&D capex under 3% of sales and minimal promo spend versus emerging tech segments.

Traditional Power Transmission Cables

Traditional power transmission cables deliver steady revenue from maintenance and grid replacement; Japan and Southeast Asia upkeep spending keeps demand stable, with regional transmission capex ~USD 18.5bn in 2024 (IEA/Asian Development Bank), supporting predictable margins for Sumitomo Electric.

Sumitomo’s strong market share and manufacturing footprint in Japan and ASEAN secure cash flow in a low-growth segment; cable products generated ~¥210bn revenue in FY2024 (Sumitomo Electric consolidated), funding dividends and debt service.

As a cash cow in the BCG matrix, these cables provide liquidity to pay interest on ~¥1.2trn corporate debt and maintain shareholder returns while the company invests in growth areas.

- Stable demand: national grid upkeep

- FY2024 cable revenue ~¥210bn

- Regional transmission capex ~USD18.5bn (2024)

- Supports ¥1.2trn debt service and dividends

Prestressed Concrete (PC) Steel Wires

Prestressed Concrete (PC) steel wires are used mainly in civil engineering and bridge construction within a mature infrastructure market; Sumitomo Electric holds a leading share and reports stable margins—its 2024 wire & cable segment operating margin ~12%, supporting steady cash flow.

Low growth in developed-region construction (OECD construction CAGR ~1.2% 2023–2025) makes PC wires a classic cash cow: high asset turnover, low capex, reliable dividends to corporate cash reserves.

- Market: mature infrastructure, bridges/highways

- Position: strong market share, efficient production

- Financials: ~12% operating margin (2024, segment)

- Growth: OECD construction CAGR ~1.2% (2023–2025)

- Role: steady cash generation, low reinvestment need

Sumitomo Electric’s cash cows: wiring, FPCs & cables drive strong margins and cash flow

Sumitomo Electric cash cows: wiring harnesses (FY2024 rev ¥220bn, gross margin 18–20%, >80% capacity), FPCs (share 12–15%, rev ¥120–150bn, FCF margin >15%), cables (FY2024 rev ¥210bn, funds debt ¥1.2trn), cutting tools (margins 40–50%), PC wires (segment op margin ~12%).

| Segment | FY2024 rev | Margin | Notes |

|---|---|---|---|

| Wiring | ¥220bn | 18–20% | >80% util |

| FPC | ¥120–150bn | — | 12–15% share |

| Cables | ¥210bn | — | supports ¥1.2trn debt |

Preview = Final Product

Sumitomo Electric BCG Matrix

The file you're previewing on this page is the exact Sumitomo Electric BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just a fully formatted, ready-to-use strategic analysis tailored for clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Sumitomo Electric’s BCG Matrix preview highlights how its diverse portfolio—spanning power cables, automotive wire harnesses, and electronic materials—maps across growth and market share; some segments show star potential in EV and renewable infrastructure, while legacy businesses act as steady cash cows. This snapshot reveals strategic pressures and capital allocation choices critical for future competitiveness. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a ready-to-use Word + Excel package to guide investment and operational decisions.

Stars

High-Voltage Direct Current (HVDC) Cables

Sumitomo Electric holds a top global share in HVDC subsea and terrestrial cables, supplying roughly 25% of large-scale offshore interconnector projects in 2024 while revenues from power-cable systems rose 18% to ¥210 billion in FY2024 (ended Mar 2025).

HVDC links are critical for tying offshore wind to grids; project backlog for HVDC contracts grew to ¥430 billion by Dec 2025, driven by Europe and Asia tenders.

The company is expanding HVDC manufacturing with ¥120 billion CAPEX planned through 2026 to lift capacity ~40%, aiming to meet projected global demand of 40–60 GW annual HVDC installations by 2030.

Next-Generation Automotive Wiring Harnesses

The shift to EVs and software-defined vehicles has raised wiring harness complexity and value; global high-voltage harness content per EV rose to about $750–1,200 in 2024, boosting addressable market to ~$18bn by 2025.

Sumitomo Electric, world's top supplier for EV harnesses, reported automotive segment sales of ¥1.1 trillion in FY2024, with high-voltage harnesses driving double-digit growth and >20% segment operating margin.

These harnesses demand heavy R&D—Sumitomo spent ¥46.3 billion on R&D in FY2024, much allocated to EV/high-voltage systems—but they remain the automotive division’s primary growth engine.

Optical Fiber and Communication Infrastructure

Optical Fiber and Communication Infrastructure sits as a Star: global 5G rollouts and AI-driven data center growth keep high-density fiber demand at peak—global fiber market hit $15.6B in 2024, growing ~8% CAGR to 2029. Sumitomo Electric, a top-tier supplier, uses proprietary manufacturing (e.g., advanced MCVD processes) to sustain margins; FY2024 optical segment revenue ~¥300bn. Heavy, continuous capex is required to match node densification and tech shifts.

Power Modules for Electric Vehicles

Sumitomo Electric’s Power Modules for EVs sits in the BCG Matrix as a star: the company holds roughly 18–22% share of the specialized EV inverter module market (2025 estimate) while the segment grows ~25% CAGR to 2028 as vehicle electrification reaches mass market.

SiC (silicon carbide) integration drives competitive advantage—Sumitomo plans capacity expansions in 2024–25 targeting >30% SiC content in modules by 2026 to cut losses and boost efficiency, supporting sustained high growth.

- High market share: ~18–22% (2025 est.)

- Segment growth: ~25% CAGR to 2028

- SiC target: >30% module content by 2026

- CapEx: ramped 2024–25 to expand SiC capacity

Advanced Traffic Management Systems

Advanced Traffic Management Systems are a Star for Sumitomo Electric: their sensing and V2X (vehicle-to-everything) comms are critical to smart cities and autonomous-driving infrastructure, supporting a c.35% market share in Japan and contributing to a segment that McKinsey estimated at $130–$180bn global mobility infrastructure spend by 2030.

High R&D intensity: Sumitomo spent ¥92.4bn on R&D in FY2024, with a growing portion toward sensors and roadside units as urban centers modernize transport grids worldwide.

Rapid market expansion: global demand for ITS (intelligent transport systems) is growing ~8–10% CAGR (2024–2030), positioning this unit for revenue and margin expansion versus mature cables and optical businesses.

- Strong Japan share ~35%

- R&D FY2024 ¥92.4bn

- Global ITS CAGR ~8–10% (2024–2030)

- Market opportunity: $130–$180bn by 2030

High-growth leaders: HVDC, EV harnesses, fiber, SiC modules & ITS power expansion

Stars: HVDC & EV harnesses, optical fiber, SiC power modules, ITS—each shows high market share and fast growth with FY2024/FY2025 figures supporting expansion.

| Business | Share | Growth | Key FY |

|---|---|---|---|

| HVDC cables | ~25% | backlog ↑ to ¥430bn (Dec 2025) | Power cables ¥210bn FY2024 |

| EV harnesses | world lead | addressable ~$18bn (2025) | Auto ¥1.1tn FY2024 |

| Optical fiber | top-tier | global market $15.6bn (2024) | Optical ¥300bn FY2024 |

| Power modules (SiC) | 18–22% (2025 est.) | ~25% CAGR to 2028 | SiC target >30% by 2026 |

| ITS / V2X | ~35% Japan | 8–10% CAGR (2024–30) | Mobility $130–180bn by 2030 |

What is included in the product

Comprehensive BCG Matrix of Sumitomo Electric: quadrant-by-quadrant strategic guidance on investment, retention, or divestment amid market trends.

One-page overview placing each Sumitomo Electric business unit in a BCG quadrant for clear portfolio decisions

Cash Cows

Standard Automotive Wiring Harnesses

Standard automotive wiring harnesses for internal combustion engine vehicles remain a cash cow for Sumitomo Electric, delivering steady revenue—about ¥220 billion in FY2024 (roughly $1.6 billion)—and sustaining high market share in a mature global market. Manufacturing is optimized with >80% capacity utilization and gross margins near 18–20%, producing predictable free cash flow. This reliable cash funds R&D and capital allocation toward green-energy products and high-voltage systems development. The segment’s stability offsets volatility as the company scales EV and advanced-electronics investments.

Flexible Printed Circuits (FPCs)

Sumitomo Electric’s Flexible Printed Circuits (FPCs) business is a market leader for smartphones, tablets and consumer electronics, delivering steady operating cash given a global FPC market share estimated around 12–15% in 2024 and annual sales roughly JPY 120–150 billion (≈USD 0.8–1.1bn) for the unit.

Smartphone unit volume growth slowed to ~2% CAGR 2021–2024, so FPCs are low-growth but high-margin cash cows, requiring minimal capex—management reports capex intensity below 5% of sales for the segment in FY2024.

Long-term OEM contracts with Apple, Samsung and other major electronics manufacturers secure predictable order flow and working-capital generation, keeping free cash flow conversion high (estimated >15% FCF margin in 2024).

Cemented Carbide Tools

Sumitomo Electric’s industrial materials division, led by cemented carbide cutting tools, sits in a mature global market worth about $25bn in 2024, growing ~2% annually; Sumitomo holds an estimated 12–15% share in high-precision aerospace and automotive niches.

These tools deliver high gross margins—roughly 40–50% on product lines—and steady free cash flow, with R&D capex under 3% of sales and minimal promo spend versus emerging tech segments.

Traditional Power Transmission Cables

Traditional power transmission cables deliver steady revenue from maintenance and grid replacement; Japan and Southeast Asia upkeep spending keeps demand stable, with regional transmission capex ~USD 18.5bn in 2024 (IEA/Asian Development Bank), supporting predictable margins for Sumitomo Electric.

Sumitomo’s strong market share and manufacturing footprint in Japan and ASEAN secure cash flow in a low-growth segment; cable products generated ~¥210bn revenue in FY2024 (Sumitomo Electric consolidated), funding dividends and debt service.

As a cash cow in the BCG matrix, these cables provide liquidity to pay interest on ~¥1.2trn corporate debt and maintain shareholder returns while the company invests in growth areas.

- Stable demand: national grid upkeep

- FY2024 cable revenue ~¥210bn

- Regional transmission capex ~USD18.5bn (2024)

- Supports ¥1.2trn debt service and dividends

Prestressed Concrete (PC) Steel Wires

Prestressed Concrete (PC) steel wires are used mainly in civil engineering and bridge construction within a mature infrastructure market; Sumitomo Electric holds a leading share and reports stable margins—its 2024 wire & cable segment operating margin ~12%, supporting steady cash flow.

Low growth in developed-region construction (OECD construction CAGR ~1.2% 2023–2025) makes PC wires a classic cash cow: high asset turnover, low capex, reliable dividends to corporate cash reserves.

- Market: mature infrastructure, bridges/highways

- Position: strong market share, efficient production

- Financials: ~12% operating margin (2024, segment)

- Growth: OECD construction CAGR ~1.2% (2023–2025)

- Role: steady cash generation, low reinvestment need

Sumitomo Electric’s cash cows: wiring, FPCs & cables drive strong margins and cash flow

Sumitomo Electric cash cows: wiring harnesses (FY2024 rev ¥220bn, gross margin 18–20%, >80% capacity), FPCs (share 12–15%, rev ¥120–150bn, FCF margin >15%), cables (FY2024 rev ¥210bn, funds debt ¥1.2trn), cutting tools (margins 40–50%), PC wires (segment op margin ~12%).

| Segment | FY2024 rev | Margin | Notes |

|---|---|---|---|

| Wiring | ¥220bn | 18–20% | >80% util |

| FPC | ¥120–150bn | — | 12–15% share |

| Cables | ¥210bn | — | supports ¥1.2trn debt |

Preview = Final Product

Sumitomo Electric BCG Matrix

The file you're previewing on this page is the exact Sumitomo Electric BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just a fully formatted, ready-to-use strategic analysis tailored for clarity and professional presentation.