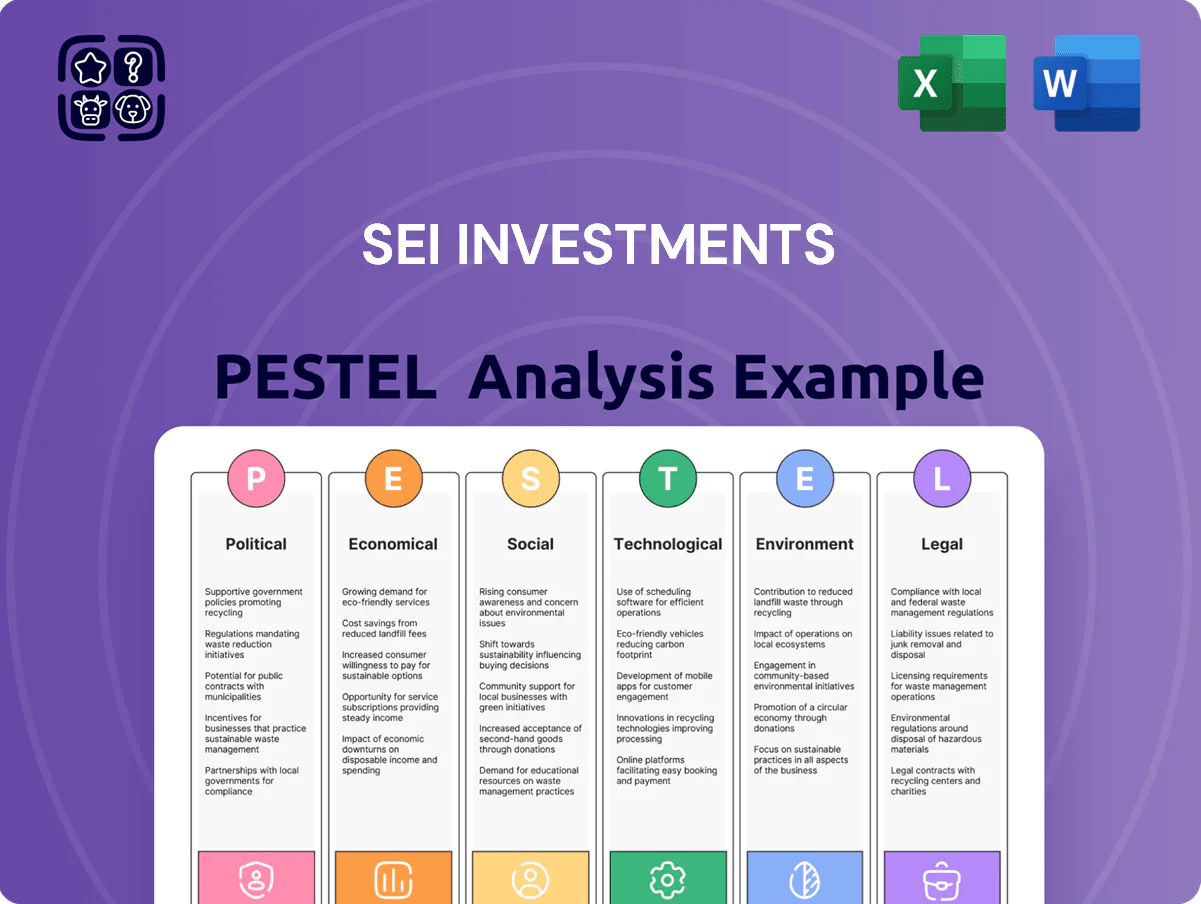

SEI Investments PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, market cycles, and tech disruption are shaping SEI Investments’ strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE to access detailed risk assessments, regulatory implications, and growth opportunities you can use immediately.

Political factors

Global Geopolitical Stability

The ongoing geopolitical tensions in Eastern Europe and the Middle East through late 2025 have elevated global market volatility, with the VIX averaging near 18–20 in 2024–2025 versus a 2010–2019 average of ~16, pressuring SEI Investments’ asset valuations and fee-based revenues tied to AUM fluctuations.

Tax Policy Shifts

Changes in corporate tax rates and capital gains taxation after the 2024 U.S. elections affect SEI’s net margins and client returns; a 2 percentage-point corporate rate rise would reduce S&P 500 after-tax earnings by roughly 3–4%, altering fee-based revenue forecasts. SEI must recalibrate wealth-management advice to reflect new fiscal mandates and sector-specific incentives—2025 tax credits for clean energy could boost client allocations to that sector by an estimated 5–8%. Tax policy remains a key driver of institutional flows, with historical shifts moving up to $50–100 billion annually between asset classes.

Trade Relations and Protectionism

The shift toward bilateral trade agreements and a rise in protectionist rhetoric—with global tariffs rising 6% on average since 2020 and foreign direct investment flows falling 12% in 2023—can constrain cross-border capital movement; SEI must design investment operations to handle data-localization rules (over 60 countries have enacted strict data laws by 2024) and licensing limits on financial services. Sudden diplomatic shifts have closed market access for some institutions within weeks, so contingency routing and modular service delivery are critical.

Government Spending and Deficits

Regulatory Influence of Political Appointments

Leadership shifts at the SEC and FSOC tied to US political cycles affect oversight intensity; since 2021 SEC enforcement actions rose 12% year-over-year, signaling potential volatility for asset servicers like SEI (AUM serviced ~$400B in 2024).[Fact-based regulatory priorities can change rapidly]

SEI must remain agile to adapt to enforcement and rulemaking shifts—compliance spend trends industry-wide grew ~8% annually through 2023, raising operational costs if oversight tightens.

Regulators' political leanings influence innovation pace and compliance burden; pro-innovation stances have accelerated fintech approvals, while stricter regimes slow product launches and increase time-to-market.

- SEC enforcement +12% YoY since 2021

- SEI-related AUM serviced approx $400B (2024)

- Industry compliance spend growth ~8% CAGR to 2023

Geopolitics, protectionism and US debt amplify AUM volatility and compliance costs

Geopolitical tensions (VIX ~18–20 in 2024–25) and rising protectionism (tariffs +6%, FDI down 12% in 2023) heighten AUM volatility for SEI (AUM serviced ≈$400B in 2024), while US debt ~120% of GDP and tax changes shift asset flows; SEC enforcement +12% YoY since 2021 raises compliance costs (~8% industry CAGR to 2023).

| Metric | Value |

|---|---|

| VIX (2024–25) | 18–20 |

| SEI AUM serviced (2024) | $400B |

| US federal debt (2024) | ~120% GDP |

| SEC enforcement change | +12% YoY since 2021 |

| Industry compliance spend CAGR | ~8% to 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect SEI Investments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and entrepreneurs, forward-looking scenario guidance, and clean formatting ready for business plans, pitch decks, or reports.

A concise, visually segmented PESTLE summary of SEI Investments that’s ready to drop into presentations or strategy sessions, easing stakeholder alignment and supporting quick risk/market positioning discussions.

Economic factors

Interest Rate Trajectory

As of late 2025, global policy rates have largely stabilized—US Fed funds at 5.25–5.50% and ECB depo at 4.00%—reducing volatility in SEI’s net interest income but keeping yields on cash solutions elevated; 2024–25 money market yields rose to ~4–5%, boosting fee-bearing cash revenues. Higher rates raise client borrowing costs, pressuring credit-sensitive AUM growth, while SEI must recalibrate portfolio duration and credit allocation to align with central bank stances.

Inflationary Pressures

Persistent or volatile U.S. inflation—4.1% in 2024 CPI year-over-year through November—reduces real returns on portfolios SEI manages, pressing demand for real-return solutions for ultra-high-net-worth and institutional clients.

SEI must expand inflation-hedging strategies such as TIPS, commodities, and real assets; TIPS real yields averaged around 0.2% in late 2024, underscoring client need for active allocation.

Rising inflation also increased operational costs: U.S. wage growth for financial services ran near 4–5% in 2024 and IT cloud spend rose ~15% year-over-year, squeezing SEI’s margins and necessitating efficiency investments.

Global Economic Growth Cycles

Varying recovery speeds—US GDP growth ~2.5% 2024, Eurozone ~0.8%, China ~5%—drive regional demand for SEI’s processing and management services as AUM correlates with market performance; SEI reported $424.5 billion AUC/A in 2024, linking revenue to market health. Economic downturns compress fees and cut advisors’ discretionary tech spend, contributing to margin pressure; global volatility in 2024 reduced industry net flows and elevated fee sensitivity.

Currency Exchange Rate Volatility

As a global provider, SEI faces currency exchange volatility that in 2024 shifted reported international revenues by about 2–3%, with a stronger USD in 2023 reducing translated offshore earnings; such swings materially affect GAAP top-line comparability.

Currency moves also alter returns on globally diversified client portfolios—FX drag added roughly 40–70 bps to volatility in emerging-market exposures in 2023—prompting SEI to deploy advanced hedging and overlay strategies.

US dollar strength remains pivotal: a 5% USD appreciation typically worsens SEI’s competitive pricing abroad and can compress fee revenues from non‑USD mandates.

- Reported international revenue sensitivity: ~2–3%

- EM FX volatility impact: ~40–70 bps (2023)

- 5% USD appreciation → reduced foreign fee competitiveness

Labor Market Dynamics

The availability of skilled financial and technology professionals—critical for SEI’s innovation and scaling—faces constraints as U.S. fintech hiring grew 6% in 2024 while tech role vacancies remained ~20% above pre‑pandemic levels, slowing time‑to‑market for new services.

Wage inflation in fintech (average tech salary rises ~8% in 2024) pressures SEI’s operating expenses and accelerates automation investments to reduce headcount costs.

SEI must balance competitive compensation with efficiency: e.g., 2024 R&D and tech spend represented ~18% of revenues for peer firms, guiding SEI’s tradeoffs.

- Skilled labor scarcity: hiring slowdowns, longer fills

- Wage inflation: ~8% tech salary growth 2024

- Automation: investment to curb operating margins

- Benchmark: peers ~18% revenue on R&D/tech

Higher rates, sticky inflation drive cash yields, TIPS demand; GDP and FX reshape revenue

Higher 2024–25 rates (Fed 5.25–5.50%, MM yields ~4–5%) boosted cash revenues but raised client borrowing costs; 2024 CPI ~4.1% drove demand for TIPS (real yields ~0.2%), commodities and real assets; GDP: US ~2.5%, EU ~0.8%, China ~5% (2024) affecting AUC/A $424.5bn; USD moves altered international revenue ~2–3%.

| Metric | 2024/25 |

|---|---|

| Fed rate | 5.25–5.50% |

| MM yields | ~4–5% |

| CPI (2024) | 4.1% |

| AUC/A | $424.5bn |

| Intl rev sensitivity | ~2–3% |

Full Version Awaits

SEI Investments PESTLE Analysis

The preview shown here is the exact SEI Investments PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the same content, layout, and insights visible in the preview with no placeholders or teasers. After payment you’ll instantly download this final version and can begin applying the PESTLE findings to strategic or investment decisions. What you see is precisely what you’ll own.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, market cycles, and tech disruption are shaping SEI Investments’ strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE to access detailed risk assessments, regulatory implications, and growth opportunities you can use immediately.

Political factors

Global Geopolitical Stability

The ongoing geopolitical tensions in Eastern Europe and the Middle East through late 2025 have elevated global market volatility, with the VIX averaging near 18–20 in 2024–2025 versus a 2010–2019 average of ~16, pressuring SEI Investments’ asset valuations and fee-based revenues tied to AUM fluctuations.

Tax Policy Shifts

Changes in corporate tax rates and capital gains taxation after the 2024 U.S. elections affect SEI’s net margins and client returns; a 2 percentage-point corporate rate rise would reduce S&P 500 after-tax earnings by roughly 3–4%, altering fee-based revenue forecasts. SEI must recalibrate wealth-management advice to reflect new fiscal mandates and sector-specific incentives—2025 tax credits for clean energy could boost client allocations to that sector by an estimated 5–8%. Tax policy remains a key driver of institutional flows, with historical shifts moving up to $50–100 billion annually between asset classes.

Trade Relations and Protectionism

The shift toward bilateral trade agreements and a rise in protectionist rhetoric—with global tariffs rising 6% on average since 2020 and foreign direct investment flows falling 12% in 2023—can constrain cross-border capital movement; SEI must design investment operations to handle data-localization rules (over 60 countries have enacted strict data laws by 2024) and licensing limits on financial services. Sudden diplomatic shifts have closed market access for some institutions within weeks, so contingency routing and modular service delivery are critical.

Government Spending and Deficits

Regulatory Influence of Political Appointments

Leadership shifts at the SEC and FSOC tied to US political cycles affect oversight intensity; since 2021 SEC enforcement actions rose 12% year-over-year, signaling potential volatility for asset servicers like SEI (AUM serviced ~$400B in 2024).[Fact-based regulatory priorities can change rapidly]

SEI must remain agile to adapt to enforcement and rulemaking shifts—compliance spend trends industry-wide grew ~8% annually through 2023, raising operational costs if oversight tightens.

Regulators' political leanings influence innovation pace and compliance burden; pro-innovation stances have accelerated fintech approvals, while stricter regimes slow product launches and increase time-to-market.

- SEC enforcement +12% YoY since 2021

- SEI-related AUM serviced approx $400B (2024)

- Industry compliance spend growth ~8% CAGR to 2023

Geopolitics, protectionism and US debt amplify AUM volatility and compliance costs

Geopolitical tensions (VIX ~18–20 in 2024–25) and rising protectionism (tariffs +6%, FDI down 12% in 2023) heighten AUM volatility for SEI (AUM serviced ≈$400B in 2024), while US debt ~120% of GDP and tax changes shift asset flows; SEC enforcement +12% YoY since 2021 raises compliance costs (~8% industry CAGR to 2023).

| Metric | Value |

|---|---|

| VIX (2024–25) | 18–20 |

| SEI AUM serviced (2024) | $400B |

| US federal debt (2024) | ~120% GDP |

| SEC enforcement change | +12% YoY since 2021 |

| Industry compliance spend CAGR | ~8% to 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect SEI Investments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and entrepreneurs, forward-looking scenario guidance, and clean formatting ready for business plans, pitch decks, or reports.

A concise, visually segmented PESTLE summary of SEI Investments that’s ready to drop into presentations or strategy sessions, easing stakeholder alignment and supporting quick risk/market positioning discussions.

Economic factors

Interest Rate Trajectory

As of late 2025, global policy rates have largely stabilized—US Fed funds at 5.25–5.50% and ECB depo at 4.00%—reducing volatility in SEI’s net interest income but keeping yields on cash solutions elevated; 2024–25 money market yields rose to ~4–5%, boosting fee-bearing cash revenues. Higher rates raise client borrowing costs, pressuring credit-sensitive AUM growth, while SEI must recalibrate portfolio duration and credit allocation to align with central bank stances.

Inflationary Pressures

Persistent or volatile U.S. inflation—4.1% in 2024 CPI year-over-year through November—reduces real returns on portfolios SEI manages, pressing demand for real-return solutions for ultra-high-net-worth and institutional clients.

SEI must expand inflation-hedging strategies such as TIPS, commodities, and real assets; TIPS real yields averaged around 0.2% in late 2024, underscoring client need for active allocation.

Rising inflation also increased operational costs: U.S. wage growth for financial services ran near 4–5% in 2024 and IT cloud spend rose ~15% year-over-year, squeezing SEI’s margins and necessitating efficiency investments.

Global Economic Growth Cycles

Varying recovery speeds—US GDP growth ~2.5% 2024, Eurozone ~0.8%, China ~5%—drive regional demand for SEI’s processing and management services as AUM correlates with market performance; SEI reported $424.5 billion AUC/A in 2024, linking revenue to market health. Economic downturns compress fees and cut advisors’ discretionary tech spend, contributing to margin pressure; global volatility in 2024 reduced industry net flows and elevated fee sensitivity.

Currency Exchange Rate Volatility

As a global provider, SEI faces currency exchange volatility that in 2024 shifted reported international revenues by about 2–3%, with a stronger USD in 2023 reducing translated offshore earnings; such swings materially affect GAAP top-line comparability.

Currency moves also alter returns on globally diversified client portfolios—FX drag added roughly 40–70 bps to volatility in emerging-market exposures in 2023—prompting SEI to deploy advanced hedging and overlay strategies.

US dollar strength remains pivotal: a 5% USD appreciation typically worsens SEI’s competitive pricing abroad and can compress fee revenues from non‑USD mandates.

- Reported international revenue sensitivity: ~2–3%

- EM FX volatility impact: ~40–70 bps (2023)

- 5% USD appreciation → reduced foreign fee competitiveness

Labor Market Dynamics

The availability of skilled financial and technology professionals—critical for SEI’s innovation and scaling—faces constraints as U.S. fintech hiring grew 6% in 2024 while tech role vacancies remained ~20% above pre‑pandemic levels, slowing time‑to‑market for new services.

Wage inflation in fintech (average tech salary rises ~8% in 2024) pressures SEI’s operating expenses and accelerates automation investments to reduce headcount costs.

SEI must balance competitive compensation with efficiency: e.g., 2024 R&D and tech spend represented ~18% of revenues for peer firms, guiding SEI’s tradeoffs.

- Skilled labor scarcity: hiring slowdowns, longer fills

- Wage inflation: ~8% tech salary growth 2024

- Automation: investment to curb operating margins

- Benchmark: peers ~18% revenue on R&D/tech

Higher rates, sticky inflation drive cash yields, TIPS demand; GDP and FX reshape revenue

Higher 2024–25 rates (Fed 5.25–5.50%, MM yields ~4–5%) boosted cash revenues but raised client borrowing costs; 2024 CPI ~4.1% drove demand for TIPS (real yields ~0.2%), commodities and real assets; GDP: US ~2.5%, EU ~0.8%, China ~5% (2024) affecting AUC/A $424.5bn; USD moves altered international revenue ~2–3%.

| Metric | 2024/25 |

|---|---|

| Fed rate | 5.25–5.50% |

| MM yields | ~4–5% |

| CPI (2024) | 4.1% |

| AUC/A | $424.5bn |

| Intl rev sensitivity | ~2–3% |

Full Version Awaits

SEI Investments PESTLE Analysis

The preview shown here is the exact SEI Investments PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the same content, layout, and insights visible in the preview with no placeholders or teasers. After payment you’ll instantly download this final version and can begin applying the PESTLE findings to strategic or investment decisions. What you see is precisely what you’ll own.