Sempra Porter's Five Forces Analysis

From Overview to Strategy Blueprint

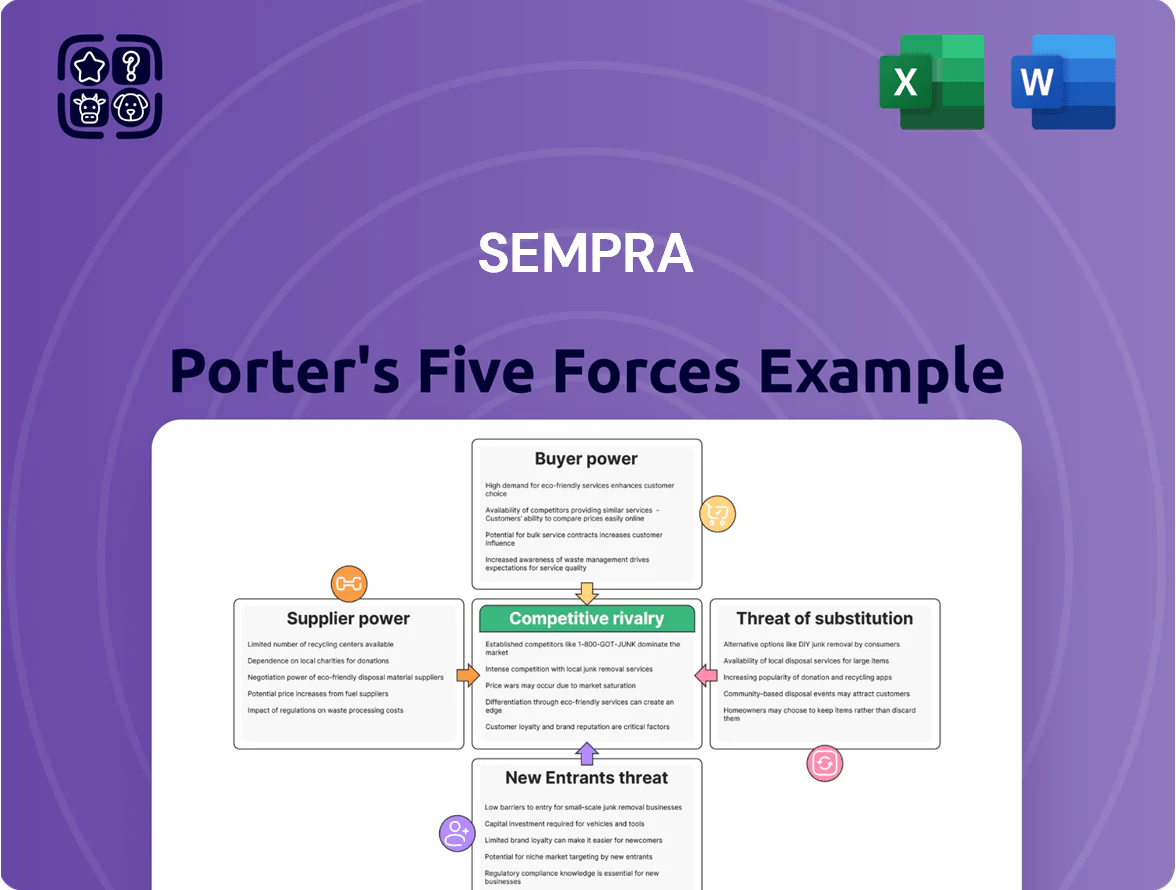

Sempra operates in a capital-intensive, regulated energy landscape where utility-scale bargaining power, high entry barriers, and moderate substitute threats shape competitive dynamics—while regulatory shifts and cross-border LNG expansion create both risks and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sempra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Upstream Producers

Sempra depends on upstream natural gas producers for feedstock across its US distribution and Port Arthur LNG export projects; US marketed gas production averaged 99.7 Bcf/d in 2024, easing supply risk through 2025. Consolidation among drillers—M&A volumes rose 18% in 2024—could boost suppliers’ pricing power versus pipeline and LNG buyers. Sempra limits exposure via diversified supply contracts, 10‑15 year take-or-pay deals, and hedges covering ~60% of expected per-MMBtu input through 2026.

Specialized EPC Contractors

Specialized EPC contractors control scarce skills for LNG terminals like Port Arthur LNG, so their bargaining power is high; only ~10–15 global firms handle such projects, pushing up prices and schedule risk.

Sempra’s $40+ billion capital plan to 2028 depends on timely EPC delivery; a 10% cost overrun on a $3.5B project adds $350M and raises financing strain.

Renewable Energy Equipment Manufacturers

As Sempra scales clean-energy assets, it relies on a global supply chain for PV modules, turbines, and Li-ion cells; in 2024 global polysilicon prices rose ~45% YoY, tightening supplier leverage and raising procurement costs.

Sempra’s ~$10+ billion project pipeline lets it negotiate long-term offtake and volume discounts, but exposure to rare-earth and cobalt markets means commodity-driven price swings still pose material margin risk.

Skilled Labor and Unions

Financial Capital Providers

Sempra’s capital-heavy model needs steady debt and equity access to fund $30–40B planned projects through 2030, so bond markets and equity investors are critical suppliers of capital.

Large institutional lenders and rating firms tie borrowing costs to Sempra’s ESG scores and net debt (~$22.5B end-2024), so their assessments directly shift interest spreads.

By late 2025, higher rates and mixed investor appetite for energy-transition assets narrowed Sempra’s financing runway and raised cost of capital, limiting near-term strategic flexibility.

- Planned capex $30–40B through 2030

- Net debt ~ $22.5B (end-2024)

- ESG ratings impact bond spreads

- Late-2025 rate/investor shifts tightened financing

Sempra squeezed by supplier leverage, hedges steady as debt and rates bite

Sempra faces moderate-to-high supplier power: upstream US gas supply averaged 99.7 Bcf/d in 2024, easing feedstock risk, but driller M&A (+18% in 2024) and scarce LNG EPC firms increase pricing leverage; 10–15 year taker-pay contracts and ~60% hedging to 2026 limit exposure. Capital providers (net debt ~$22.5B end-2024) and rising 2025 rates tighten financing leverage.

| Metric | Value |

|---|---|

| US gas prod. 2024 | 99.7 Bcf/d |

| Driller M&A 2024 | +18% |

| Hedge coverage | ~60% to 2026 |

| Net debt | $22.5B (end-2024) |

What is included in the product

Concise Porter’s Five Forces assessment of Sempra that identifies competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and regulatory/disruptive risks—tailored insights to inform strategic, investment, and operational decisions.

Concise Porter's Five Forces for Sempra—one-sheet clarity to spot competitive threats and opportunities fast, ready to drop into decks or duplicate for scenario comparisons.

Customers Bargaining Power

Regulated Residential Ratepayers

Global LNG Off-takers

Industrial and Commercial Consumers

Large industrial and commercial customers account for roughly 40% of Sempra Energy’s U.S. gas and power load in 2024 and can buy onsite generation or relocate to lower-cost regions, raising bargaining power; in response Sempra must offer tailored energy management, long-term fixed-rate contracts, and demonstrate grid resilience—Sempra reported $5.8B in customer solutions revenue in 2024, showing focus on retaining high-value clients.

State Regulatory Commissions

State regulatory commissions like the California Public Utilities Commission (CPUC) and the Public Utility Commission of Texas (PUCT) effectively stand in for customers by setting allowed return on equity—CPUC approved 9.4% ROE for several utilities in 2022–2024 cases and PUCT targets similar ranges—while approving all major Sempra capital projects and rate changes, directly capping profit margins to balance investor returns and consumer rates.

Regulators also mandate cost recovery timelines and performance metrics; for example, CPUC-authorized rate bases and PUCT-approved cost trackers determined Sempra affiliates’ allowed revenue growth of ~3–6% annually in recent rate cycles, constraining pricing flexibility and capital deployment timing.

- Regulators set ROE (CPUC ~9.4% recent rulings)

- Approve all major investments and rate changes

- Limit revenue growth (recent cycles ~3–6%/yr)

- Enforce consumer protection and performance metrics

Wholesale Electricity Market Participants

Sempra Infrastructure sells into wholesale markets where buyers see real-time prices and multiple generation sources, raising buyer bargaining power because purchasers can chase the lowest marginal cost; U.S. wholesale power prices averaged about 36–45 USD/MWh in 2024 across key hubs, so small price gaps shift demand quickly.

Sempra must keep unit-level costs low—capital recovery, O&M, and fuel—to stay competitive against other generators and gas shippers; a 1–2 USD/MWh cost disadvantage can lose volume in day-ahead and real-time markets.

- High buyer power: real-time price visibility

- Market prices (2024): ~36–45 USD/MWh

- Sempra risk: losing load with $1–2/MWh cost gaps

- Action: focus on cost per MWh, dispatch flexibility

Sempra must balance regulator-led retail limits with powerful LNG buyers and market pricing

Customers wield low individual power but strong collective influence via regulators (CPUC ROE ~9.4%; allowed revenue growth ~3–6%/yr), while large LNG off-takers and big industrials exert high bargaining power through long-term take-or-pay deals (anchors ~2–4 mtpa; contract values $5–10B+) and threat to switch suppliers; wholesale buyers also press on price (U.S. 2024 hubs ~36–45 USD/MWh), so Sempra must match pricing, flexibility, and low unit costs.

| Metric | 2024 |

|---|---|

| SDG&E customers | ~3.7M |

| CPUC ROE | ~9.4% |

| Allowed rev growth | ~3–6%/yr |

| Wholesale price range | ~36–45 USD/MWh |

| Anchor deal size | 2–4 mtpa / $5–10B+ |

Preview the Actual Deliverable

Sempra Porter's Five Forces Analysis

This preview shows the exact Sempra Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No mockups or samples: the document displayed here is the complete deliverable and will be available for instant download once you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Sempra operates in a capital-intensive, regulated energy landscape where utility-scale bargaining power, high entry barriers, and moderate substitute threats shape competitive dynamics—while regulatory shifts and cross-border LNG expansion create both risks and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sempra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Upstream Producers

Sempra depends on upstream natural gas producers for feedstock across its US distribution and Port Arthur LNG export projects; US marketed gas production averaged 99.7 Bcf/d in 2024, easing supply risk through 2025. Consolidation among drillers—M&A volumes rose 18% in 2024—could boost suppliers’ pricing power versus pipeline and LNG buyers. Sempra limits exposure via diversified supply contracts, 10‑15 year take-or-pay deals, and hedges covering ~60% of expected per-MMBtu input through 2026.

Specialized EPC Contractors

Specialized EPC contractors control scarce skills for LNG terminals like Port Arthur LNG, so their bargaining power is high; only ~10–15 global firms handle such projects, pushing up prices and schedule risk.

Sempra’s $40+ billion capital plan to 2028 depends on timely EPC delivery; a 10% cost overrun on a $3.5B project adds $350M and raises financing strain.

Renewable Energy Equipment Manufacturers

As Sempra scales clean-energy assets, it relies on a global supply chain for PV modules, turbines, and Li-ion cells; in 2024 global polysilicon prices rose ~45% YoY, tightening supplier leverage and raising procurement costs.

Sempra’s ~$10+ billion project pipeline lets it negotiate long-term offtake and volume discounts, but exposure to rare-earth and cobalt markets means commodity-driven price swings still pose material margin risk.

Skilled Labor and Unions

Financial Capital Providers

Sempra’s capital-heavy model needs steady debt and equity access to fund $30–40B planned projects through 2030, so bond markets and equity investors are critical suppliers of capital.

Large institutional lenders and rating firms tie borrowing costs to Sempra’s ESG scores and net debt (~$22.5B end-2024), so their assessments directly shift interest spreads.

By late 2025, higher rates and mixed investor appetite for energy-transition assets narrowed Sempra’s financing runway and raised cost of capital, limiting near-term strategic flexibility.

- Planned capex $30–40B through 2030

- Net debt ~ $22.5B (end-2024)

- ESG ratings impact bond spreads

- Late-2025 rate/investor shifts tightened financing

Sempra squeezed by supplier leverage, hedges steady as debt and rates bite

Sempra faces moderate-to-high supplier power: upstream US gas supply averaged 99.7 Bcf/d in 2024, easing feedstock risk, but driller M&A (+18% in 2024) and scarce LNG EPC firms increase pricing leverage; 10–15 year taker-pay contracts and ~60% hedging to 2026 limit exposure. Capital providers (net debt ~$22.5B end-2024) and rising 2025 rates tighten financing leverage.

| Metric | Value |

|---|---|

| US gas prod. 2024 | 99.7 Bcf/d |

| Driller M&A 2024 | +18% |

| Hedge coverage | ~60% to 2026 |

| Net debt | $22.5B (end-2024) |

What is included in the product

Concise Porter’s Five Forces assessment of Sempra that identifies competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and regulatory/disruptive risks—tailored insights to inform strategic, investment, and operational decisions.

Concise Porter's Five Forces for Sempra—one-sheet clarity to spot competitive threats and opportunities fast, ready to drop into decks or duplicate for scenario comparisons.

Customers Bargaining Power

Regulated Residential Ratepayers

Global LNG Off-takers

Industrial and Commercial Consumers

Large industrial and commercial customers account for roughly 40% of Sempra Energy’s U.S. gas and power load in 2024 and can buy onsite generation or relocate to lower-cost regions, raising bargaining power; in response Sempra must offer tailored energy management, long-term fixed-rate contracts, and demonstrate grid resilience—Sempra reported $5.8B in customer solutions revenue in 2024, showing focus on retaining high-value clients.

State Regulatory Commissions

State regulatory commissions like the California Public Utilities Commission (CPUC) and the Public Utility Commission of Texas (PUCT) effectively stand in for customers by setting allowed return on equity—CPUC approved 9.4% ROE for several utilities in 2022–2024 cases and PUCT targets similar ranges—while approving all major Sempra capital projects and rate changes, directly capping profit margins to balance investor returns and consumer rates.

Regulators also mandate cost recovery timelines and performance metrics; for example, CPUC-authorized rate bases and PUCT-approved cost trackers determined Sempra affiliates’ allowed revenue growth of ~3–6% annually in recent rate cycles, constraining pricing flexibility and capital deployment timing.

- Regulators set ROE (CPUC ~9.4% recent rulings)

- Approve all major investments and rate changes

- Limit revenue growth (recent cycles ~3–6%/yr)

- Enforce consumer protection and performance metrics

Wholesale Electricity Market Participants

Sempra Infrastructure sells into wholesale markets where buyers see real-time prices and multiple generation sources, raising buyer bargaining power because purchasers can chase the lowest marginal cost; U.S. wholesale power prices averaged about 36–45 USD/MWh in 2024 across key hubs, so small price gaps shift demand quickly.

Sempra must keep unit-level costs low—capital recovery, O&M, and fuel—to stay competitive against other generators and gas shippers; a 1–2 USD/MWh cost disadvantage can lose volume in day-ahead and real-time markets.

- High buyer power: real-time price visibility

- Market prices (2024): ~36–45 USD/MWh

- Sempra risk: losing load with $1–2/MWh cost gaps

- Action: focus on cost per MWh, dispatch flexibility

Sempra must balance regulator-led retail limits with powerful LNG buyers and market pricing

Customers wield low individual power but strong collective influence via regulators (CPUC ROE ~9.4%; allowed revenue growth ~3–6%/yr), while large LNG off-takers and big industrials exert high bargaining power through long-term take-or-pay deals (anchors ~2–4 mtpa; contract values $5–10B+) and threat to switch suppliers; wholesale buyers also press on price (U.S. 2024 hubs ~36–45 USD/MWh), so Sempra must match pricing, flexibility, and low unit costs.

| Metric | 2024 |

|---|---|

| SDG&E customers | ~3.7M |

| CPUC ROE | ~9.4% |

| Allowed rev growth | ~3–6%/yr |

| Wholesale price range | ~36–45 USD/MWh |

| Anchor deal size | 2–4 mtpa / $5–10B+ |

Preview the Actual Deliverable

Sempra Porter's Five Forces Analysis

This preview shows the exact Sempra Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No mockups or samples: the document displayed here is the complete deliverable and will be available for instant download once you buy.