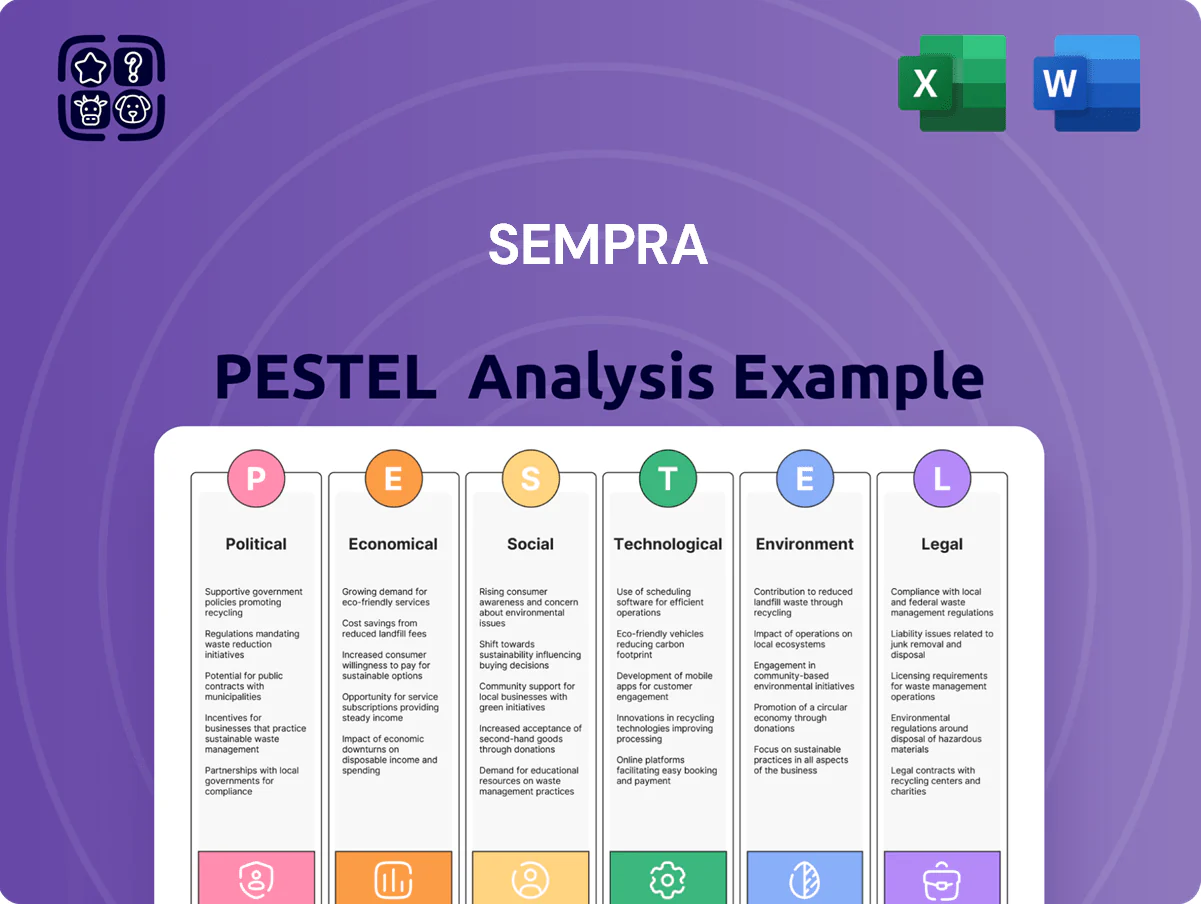

Sempra PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, regulatory pressures, and energy-transition trends are shaping Sempra’s strategic outlook—our concise PESTLE highlights the external forces that matter most to investors and planners; purchase the full, editable analysis to unlock detailed risks, opportunities, and actionable recommendations you can apply immediately.

Political factors

Federal LNG Export Permitting Policies

The US DOE's stance on LNG export authorizations remains a critical political driver for Sempra Infrastructure, with approvals affecting revenue timing for projects like Port Arthur LNG Phase 2 (estimated CAPEX ~$13–15bn). As of late 2025, politicized debate over fossil fuel exports has lengthened average DOE review times to ~9–14 months, slowing project financing and FID schedules. Shifts in federal administration energy priorities can trigger pauses or accelerations, altering projected annual export volumes and cash flows for Sempra's LNG portfolio.

California State Energy Mandates

Sempra subsidiary San Diego Gas & Electric operates under California’s aggressive decarbonization mandates, including state law targeting carbon neutrality by 2045, forcing elevated capital allocation—SDG&E plans roughly $12–14 billion in system investments through 2026 for grid hardening and renewables integration.

Compliance requires ongoing regulatory engagement with the California Public Utilities Commission; recent CPUC decisions have approved multi-year rate plans that materially affect Sempra’s allowed returns and timing of infrastructure cost recovery.

US-Mexico Energy Trade Relations

With over $6.5 billion of assets in Mexico via Sempra Infrastructure, the company is exposed to diplomatic shifts between Washington and Mexico City; recent Mexican policy moves favoring state control cut planned private investment in 2024 by an estimated 12% in the sector, raising operational risk for Sempra’s pipelines and terminals. The USMCA’s energy chapters, in force since 2020, offer legal protections for cross-border investments and dispute resolution, partially mitigating political risk.

Federal Infrastructure Subsidies and Incentives

The continued availability of Inflation Reduction Act tax credits—projected to subsidize up to $369 billion in clean energy investment through 2031—remains a cornerstone of Sempra’s clean energy strategy through 2025, underpinning planned LNG-to-hydrogen pilots and grid modernization investments.

Political support and funding streams for hydrogen and carbon capture—federal H2 tax credits up to $3/kg-equivalent and 45Q carbon capture credits up to $85/ton for 2025-era projects—provide financial offsets enabling Sempra to pilot energy-transition projects with reduced capital strain.

Any congressional move to repeal or scale back these incentives would directly reduce projected project IRRs and extend payback periods, materially altering the economic feasibility of Sempra’s long-term sustainability roadmap.

- IRA credits support ~$369B clean-energy investment (through 2031)

- H2 credits up to ~$3/kg-equivalent; 45Q up to $85/ton (2025 levels)

- Incentive cuts would lower IRRs and delay paybacks on Sempra pilots

Regulatory Oversight of Interstate Pipelines

The Federal Energy Regulatory Commission oversees Sempra's interstate gas transmission and wholesale power markets; in 2025 FERC approved ~$4.2B in LNG and pipeline-related certificates affecting Sempra-linked projects. Political appointments shift environmental review stringency and public-need criteria, altering permitting timelines and cost estimates.

Sempra must actively engage federal policymakers to align midstream expansion with evolving standards to avoid delays that can add 5–15% to capital expenditures.

- FERC jurisdiction over interstate gas and wholesale power

- 2025 ~4.2B in certificates impacting Sempra projects

- Political appointments change review stringency and public-need tests

- Active federal engagement reduces risk of 5–15% capex overruns

Sempra’s LNG, SDG&E capex and IRA credits reshape timing, cash flows, and cross‑border risk

Federal LNG export approvals, FERC certificates (~$4.2B in 2025) and DOE review delays (9–14 months) materially affect Sempra’s project timing and cash flows; California decarbonization drives SDG&E capex ($12–14B through 2026); IRA and H2/45Q credits (IRA ~$369B through 2031; H2 ~$3/kg; 45Q ~$85/ton in 2025) underpin transition projects; Mexico policy shifts raise cross‑border asset risk.

| Item | Value |

|---|---|

| FERC certificates (2025) | $4.2B |

| SDG&E capex thru 2026 | $12–14B |

| IRA clean energy | $369B (thru 2031) |

| H2 / 45Q (2025) | $3/kg ; $85/ton |

What is included in the product

Explores how macro-environmental factors uniquely affect Sempra across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sempra that’s easy to drop into presentations or share across teams, simplifying external risk discussions and market positioning during planning sessions.

Economic factors

Interest Rate Environment and Capital Costs

Sempra’s capital-intensive utilities and LNG businesses are highly sensitive to borrowing costs, with project IRRs shifting materially as debt rates move; the company plans roughly $36–40 billion in capital spending through 2028, making financing rates critical. By end-2025, stabilization of global policy rates (Fed funds ~5.25–5.50% in 2024–25 consensus) will shape Sempra’s ability to deploy its multi-billion-dollar upgrade and pipeline projects. Elevated yields compress margins and raise WACC, whereas a move to lower rates would enable more aggressive LNG and renewable expansion by improving project economics.

Natural Gas Global Market Demand

The economic viability of Sempra’s LNG export facilities hinges on the price spread between Henry Hub and international benchmarks; in 2025 average Henry Hub was about 3.50 USD/MMBtu vs TTF at ~14 USD/MMBtu and JKM near 16 USD/MMBtu, driving healthy margins for exports.

Sustained global demand for natural gas as a transition fuel—IEA projected 2024–25 gas demand growth ~1.3% annually—supports long-term contracting of Sempra’s export capacity.

Economic shifts in importing nations, notably slower EU growth in 2024 (estimated 0.5%) or faster Asian demand, directly affect Sempra’s FID timing for next infrastructure phases.

Inflationary Pressures on Construction Costs

Rising prices for steel (up ~30% YoY in 2024) and copper (up ~22% YoY) plus premium specialized labor have increased Sempra’s LNG and transmission project budgets by an estimated mid-single-digit percentage points per project. Sempra uses forward contracts, commodity hedges and fixed-price procurement to limit overruns; its 2024 guidance assumed $200–300m of procurement hedging benefits. Inflationary cost pressures feed into utility rate cases as Sempra seeks to recover higher O&M and capital costs from customers.

Regional Economic Growth in Texas and California

Regional economic growth in Texas and California drives utility demand; Texas GDP grew 3.5% in 2024 and California 2.6%, supporting higher electricity and gas consumption in Sempra territories.

In Texas, industrial expansion and a 5% annual increase in data center capacity in 2024 raised load forecasts for Oncor, prompting grid upgrades.

Economic resilience supports predictable cash flows—Sempra reports ~60% of regulated earnings tied to CA/TX operations—justifying ongoing modernization investments.

- Texas GDP 2024 +3.5%

- California GDP 2024 +2.6%

- Data center capacity growth TX ~5% (2024)

- ~60% of regulated earnings from CA/TX

Currency Exchange Rate Volatility

Sempra’s international operations generate substantial peso-denominated cash flows—about 30% of 2024 revenues came from its Mexico businesses—exposing earnings to USD/MXN swings.

Movements in the USD/MXN rate have materially affected reported EPS and the USD valuation of Mexican regulated assets on consolidation in recent years.

The company deploys FX derivatives and contract-structured natural hedges (revenue-cost offsets, peso-denominated debt) to mitigate currency volatility.

- ~30% 2024 revenue from Mexico

- USD/MXN volatility affects EPS and asset valuations

- Uses FX derivatives and natural hedges

Sempra’s $36–40B capex, higher rates squeeze IRRs; LNG margins boosted by wide gas spread

Sempra’s $36–40bn capex through 2028 makes financing costs critical; Fed funds ~5.25–5.50% (2024–25 consensus) raises WACC and compresses project IRRs. 2025 avg Henry Hub ~$3.50/MMBtu vs TTF ~$14 and JKM ~$16 supports LNG margins; Mexico ~30% of 2024 revenue exposes FX risk (USD/MXN), mitigated by hedges; CA/TX (~60% regulated earnings) benefit from 2024 GDP: TX +3.5%, CA +2.6%.

| Metric | Value (2024–25) |

|---|---|

| Capex thru 2028 | $36–40bn |

| Fed funds | ~5.25–5.50% |

| Henry Hub / TTF / JKM | $3.5 / $14 / $16 |

| Mexico revenue | ~30% |

| CA/TX regulated earnings | ~60% |

| TX / CA GDP 2024 | +3.5% / +2.6% |

What You See Is What You Get

Sempra PESTLE Analysis

The preview shown here is the exact Sempra PESTLE document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with complete analysis of political, economic, social, technological, legal, and environmental factors affecting Sempra. No placeholders or teasers—what you see is what you’ll download immediately after payment. The layout, content, and structure are professionally prepared for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, regulatory pressures, and energy-transition trends are shaping Sempra’s strategic outlook—our concise PESTLE highlights the external forces that matter most to investors and planners; purchase the full, editable analysis to unlock detailed risks, opportunities, and actionable recommendations you can apply immediately.

Political factors

Federal LNG Export Permitting Policies

The US DOE's stance on LNG export authorizations remains a critical political driver for Sempra Infrastructure, with approvals affecting revenue timing for projects like Port Arthur LNG Phase 2 (estimated CAPEX ~$13–15bn). As of late 2025, politicized debate over fossil fuel exports has lengthened average DOE review times to ~9–14 months, slowing project financing and FID schedules. Shifts in federal administration energy priorities can trigger pauses or accelerations, altering projected annual export volumes and cash flows for Sempra's LNG portfolio.

California State Energy Mandates

Sempra subsidiary San Diego Gas & Electric operates under California’s aggressive decarbonization mandates, including state law targeting carbon neutrality by 2045, forcing elevated capital allocation—SDG&E plans roughly $12–14 billion in system investments through 2026 for grid hardening and renewables integration.

Compliance requires ongoing regulatory engagement with the California Public Utilities Commission; recent CPUC decisions have approved multi-year rate plans that materially affect Sempra’s allowed returns and timing of infrastructure cost recovery.

US-Mexico Energy Trade Relations

With over $6.5 billion of assets in Mexico via Sempra Infrastructure, the company is exposed to diplomatic shifts between Washington and Mexico City; recent Mexican policy moves favoring state control cut planned private investment in 2024 by an estimated 12% in the sector, raising operational risk for Sempra’s pipelines and terminals. The USMCA’s energy chapters, in force since 2020, offer legal protections for cross-border investments and dispute resolution, partially mitigating political risk.

Federal Infrastructure Subsidies and Incentives

The continued availability of Inflation Reduction Act tax credits—projected to subsidize up to $369 billion in clean energy investment through 2031—remains a cornerstone of Sempra’s clean energy strategy through 2025, underpinning planned LNG-to-hydrogen pilots and grid modernization investments.

Political support and funding streams for hydrogen and carbon capture—federal H2 tax credits up to $3/kg-equivalent and 45Q carbon capture credits up to $85/ton for 2025-era projects—provide financial offsets enabling Sempra to pilot energy-transition projects with reduced capital strain.

Any congressional move to repeal or scale back these incentives would directly reduce projected project IRRs and extend payback periods, materially altering the economic feasibility of Sempra’s long-term sustainability roadmap.

- IRA credits support ~$369B clean-energy investment (through 2031)

- H2 credits up to ~$3/kg-equivalent; 45Q up to $85/ton (2025 levels)

- Incentive cuts would lower IRRs and delay paybacks on Sempra pilots

Regulatory Oversight of Interstate Pipelines

The Federal Energy Regulatory Commission oversees Sempra's interstate gas transmission and wholesale power markets; in 2025 FERC approved ~$4.2B in LNG and pipeline-related certificates affecting Sempra-linked projects. Political appointments shift environmental review stringency and public-need criteria, altering permitting timelines and cost estimates.

Sempra must actively engage federal policymakers to align midstream expansion with evolving standards to avoid delays that can add 5–15% to capital expenditures.

- FERC jurisdiction over interstate gas and wholesale power

- 2025 ~4.2B in certificates impacting Sempra projects

- Political appointments change review stringency and public-need tests

- Active federal engagement reduces risk of 5–15% capex overruns

Sempra’s LNG, SDG&E capex and IRA credits reshape timing, cash flows, and cross‑border risk

Federal LNG export approvals, FERC certificates (~$4.2B in 2025) and DOE review delays (9–14 months) materially affect Sempra’s project timing and cash flows; California decarbonization drives SDG&E capex ($12–14B through 2026); IRA and H2/45Q credits (IRA ~$369B through 2031; H2 ~$3/kg; 45Q ~$85/ton in 2025) underpin transition projects; Mexico policy shifts raise cross‑border asset risk.

| Item | Value |

|---|---|

| FERC certificates (2025) | $4.2B |

| SDG&E capex thru 2026 | $12–14B |

| IRA clean energy | $369B (thru 2031) |

| H2 / 45Q (2025) | $3/kg ; $85/ton |

What is included in the product

Explores how macro-environmental factors uniquely affect Sempra across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sempra that’s easy to drop into presentations or share across teams, simplifying external risk discussions and market positioning during planning sessions.

Economic factors

Interest Rate Environment and Capital Costs

Sempra’s capital-intensive utilities and LNG businesses are highly sensitive to borrowing costs, with project IRRs shifting materially as debt rates move; the company plans roughly $36–40 billion in capital spending through 2028, making financing rates critical. By end-2025, stabilization of global policy rates (Fed funds ~5.25–5.50% in 2024–25 consensus) will shape Sempra’s ability to deploy its multi-billion-dollar upgrade and pipeline projects. Elevated yields compress margins and raise WACC, whereas a move to lower rates would enable more aggressive LNG and renewable expansion by improving project economics.

Natural Gas Global Market Demand

The economic viability of Sempra’s LNG export facilities hinges on the price spread between Henry Hub and international benchmarks; in 2025 average Henry Hub was about 3.50 USD/MMBtu vs TTF at ~14 USD/MMBtu and JKM near 16 USD/MMBtu, driving healthy margins for exports.

Sustained global demand for natural gas as a transition fuel—IEA projected 2024–25 gas demand growth ~1.3% annually—supports long-term contracting of Sempra’s export capacity.

Economic shifts in importing nations, notably slower EU growth in 2024 (estimated 0.5%) or faster Asian demand, directly affect Sempra’s FID timing for next infrastructure phases.

Inflationary Pressures on Construction Costs

Rising prices for steel (up ~30% YoY in 2024) and copper (up ~22% YoY) plus premium specialized labor have increased Sempra’s LNG and transmission project budgets by an estimated mid-single-digit percentage points per project. Sempra uses forward contracts, commodity hedges and fixed-price procurement to limit overruns; its 2024 guidance assumed $200–300m of procurement hedging benefits. Inflationary cost pressures feed into utility rate cases as Sempra seeks to recover higher O&M and capital costs from customers.

Regional Economic Growth in Texas and California

Regional economic growth in Texas and California drives utility demand; Texas GDP grew 3.5% in 2024 and California 2.6%, supporting higher electricity and gas consumption in Sempra territories.

In Texas, industrial expansion and a 5% annual increase in data center capacity in 2024 raised load forecasts for Oncor, prompting grid upgrades.

Economic resilience supports predictable cash flows—Sempra reports ~60% of regulated earnings tied to CA/TX operations—justifying ongoing modernization investments.

- Texas GDP 2024 +3.5%

- California GDP 2024 +2.6%

- Data center capacity growth TX ~5% (2024)

- ~60% of regulated earnings from CA/TX

Currency Exchange Rate Volatility

Sempra’s international operations generate substantial peso-denominated cash flows—about 30% of 2024 revenues came from its Mexico businesses—exposing earnings to USD/MXN swings.

Movements in the USD/MXN rate have materially affected reported EPS and the USD valuation of Mexican regulated assets on consolidation in recent years.

The company deploys FX derivatives and contract-structured natural hedges (revenue-cost offsets, peso-denominated debt) to mitigate currency volatility.

- ~30% 2024 revenue from Mexico

- USD/MXN volatility affects EPS and asset valuations

- Uses FX derivatives and natural hedges

Sempra’s $36–40B capex, higher rates squeeze IRRs; LNG margins boosted by wide gas spread

Sempra’s $36–40bn capex through 2028 makes financing costs critical; Fed funds ~5.25–5.50% (2024–25 consensus) raises WACC and compresses project IRRs. 2025 avg Henry Hub ~$3.50/MMBtu vs TTF ~$14 and JKM ~$16 supports LNG margins; Mexico ~30% of 2024 revenue exposes FX risk (USD/MXN), mitigated by hedges; CA/TX (~60% regulated earnings) benefit from 2024 GDP: TX +3.5%, CA +2.6%.

| Metric | Value (2024–25) |

|---|---|

| Capex thru 2028 | $36–40bn |

| Fed funds | ~5.25–5.50% |

| Henry Hub / TTF / JKM | $3.5 / $14 / $16 |

| Mexico revenue | ~30% |

| CA/TX regulated earnings | ~60% |

| TX / CA GDP 2024 | +3.5% / +2.6% |

What You See Is What You Get

Sempra PESTLE Analysis

The preview shown here is the exact Sempra PESTLE document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with complete analysis of political, economic, social, technological, legal, and environmental factors affecting Sempra. No placeholders or teasers—what you see is what you’ll download immediately after payment. The layout, content, and structure are professionally prepared for immediate application.