Semrush Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

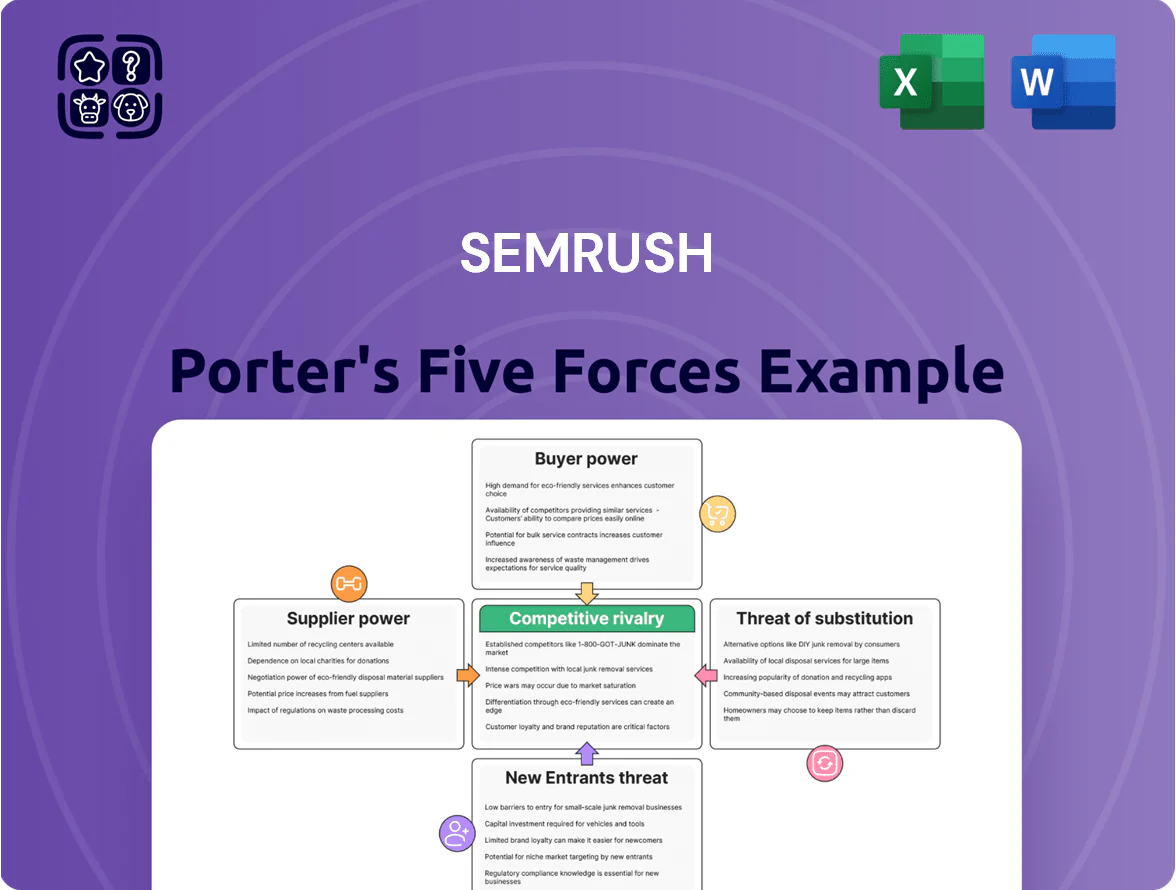

Semrush faces intense rivalry from SEO and marketing platforms, moderate buyer power, rising substitute tools, and barriers that temper new entrants—creating a dynamic competitive landscape that demands strategic agility.

Suppliers Bargaining Power

Cloud Infrastructure Providers

Semrush depends on AWS and Google Cloud to host petabyte-scale datasets and run NLP/ML engines; in 2024 Semrush reported cloud costs ~15% of revenue (~$44M of $295M), showing material exposure.

The cloud duopoly’s market share (AWS 32%, Google Cloud 12% in 2024) gives suppliers pricing power and control over SLAs and regional capacity.

Semrush reduces lock-in via multi-cloud architecture and containerization, but estimated migration costs and technical debt exceed tens of millions and maintain a high switching barrier.

Search Engine Data Access

Semrush’s core product relies on search engine data, mainly Google which held ~92% global desktop search share in 2024; Semrush uses proprietary crawlers but is exposed if Google changes robots.txt or API rules, creating supplier power that can raise costs or cut coverage. In 2025 Semrush reported 64% of traffic-related features tied to third-party indexes, so algorithm shifts force frequent engineering cycles and potential revenue risk if access narrows.

Specialized Talent Acquisition

The supply of senior data scientists and ML engineers is a bottleneck for Semrush’s AI edge: global demand rose 35% from 2020–2024 while US median ML engineer pay climbed to $160k in 2024, boosting supplier (employee) bargaining power. Big tech hiring drives higher salaries and remote-work demands, forcing Semrush to match market rates and equity offers to stay competitive. Strong retention—restricted stock units, patents, and noncompetes—matters to keep proprietary algorithmic knowledge from rivals. If churn exceeds 10% annually, roadmap delays and product-quality hits become likely.

Third-party Data Aggregators

Semrush supplements its crawled data with third-party clickstream and localized-market feeds; these niche suppliers wield bargaining power since their datasets—often unique—are costly and slow to replicate, risking sudden price hikes or exclusivity that could raise Semrush’s cost of goods sold and compress margins.

Diversifying supplier mix is a strategic priority: by 2025 Semrush reported vendor spend variability of ±12% and aims to cut single-source dependence below 25% of specialized data spend.

- Unique, hard-to-replicate clickstream data

- Supplier exclusivity can spike costs

- Vendor spend volatility ±12% (2025)

- Target: single-source <25% of specialized spend

AI and LLM Integration Partners

AI and LLM research labs (OpenAI, Anthropic, Meta, Hugging Face) act as powerful suppliers for Semrush by providing models or hosting—token and compute costs reached an estimated $12–18m annually for mid-sized SaaS integrations in 2024–25, and model licensing can take 6–15% of product COGS.

The fast tech churn forces Semrush to keep multi-vendor deals and on-prem options to avoid vendor lock-in and preserve margins.

- Token/compute spend ≈ $12–18m/year for similar SaaS

- Licensing & infra can be 6–15% of COGS

- Multi-vendor + on-prem reduce lock-in risk

- Rapid model updates → continuous integration costs

High supplier power: cloud & Google concentration; Semrush diversifies risk

Suppliers exert high bargaining power: cloud providers (AWS/Google) and Google Search dominate infra and data access—cloud costs were ~15% of revenue (~$44M of $295M) in 2024; Google held ~92% desktop search share in 2024. Niche clickstream and ML talent are scarce, raising COGS and salary bills (US median ML pay ~$160k in 2024). Semrush reduces risk via multi-cloud, vendor diversification, and targets single-source <25% of specialized spend.

| Metric | 2024–25 |

|---|---|

| Cloud cost % of revenue | 15% (~$44M/$295M) |

| Google desktop share | ≈92% |

| ML median pay (US) | $160k |

| Token/compute spend (peer est.) | $12–18M/yr |

| Vendor spend volatility | ±12% (2025) |

| Target single-source share | <25% specialized spend |

What is included in the product

Tailored Porter's Five Forces for Semrush: evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and pinpoints disruptive trends and market defenses shaping its pricing and profitability.

Semrush Porter's Five Forces in one sheet—instantly spot competitive pressures and prioritize strategic moves without sifting through reports.

Customers Bargaining Power

Low Switching Costs for SMBs

Small and medium-sized businesses (SMBs) make up roughly 40–50% of Semrush’s user base and mainly use monthly subscriptions, so switching to rivals like Ahrefs or Moz is low-friction and fast.

This mobility means price-to-value perception drives churn: industry surveys (2024) show 32% of SMBs switch SEO tools within 12 months for cost or features.

Semrush must therefore keep innovating and invest in premium support—its 2024 retention efforts aimed to keep churn near 7–9% annually to protect recurring revenue.

Price Sensitivity in the Prosumer Segment

Individual consultants and boutique agencies show high price sensitivity in the prosumer segment; a 2024 survey found 62% would downgrade after a 15% subscription hike, and SEO-tool market saturation drove 28% to trial freemium options. These users compare feature lists closely, so Semrush uses tiered pricing and bundled features—its 2024 average ARPU rose 9% after introducing bundled add-ons—to lock value and justify premium tiers.

High Information Transparency

Enterprise Customization Demands

- Major accounts: high ARR concentration — single loss = material impact

- Custom work: extra engineering and compliance spend (SOC/ISO)

- SLAs: require uptime, dedicated support, higher OPEX

Availability of Modular Alternatives

- 34% of SMEs use multiple specialist SEO tools (2024)

- Unbundling lets buyers cut costs on low-value modules

- Semrush aims to keep bundle pricing 20–30% below fragmented stacks

High churn risk: SMBs & consultants switch over price; enterprise losses bite Semrush’s $213.6M ARR

Customers hold strong bargaining power: SMBs and consultants frequently switch for price/features (2024 churn drivers: 32% switch within 12 months; 62% would downgrade after a 15% hike), while enterprises demand SLAs, custom work, and certifications—Semrush reported $213.6M ARR in 2024, so single-account losses are material.

| Metric | Value |

|---|---|

| Semrush ARR (2024) | $213.6M |

| SMB churn driver (2024) | 32% |

| Consultant downgrade risk | 62% at 15% hike |

Preview the Actual Deliverable

Semrush Porter's Five Forces Analysis

This preview shows the exact Semrush Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted deliverable, ready for download and use the moment you buy.

You’re viewing the actual file; once payment is complete, you’ll get instant access to this same professionally written analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Semrush faces intense rivalry from SEO and marketing platforms, moderate buyer power, rising substitute tools, and barriers that temper new entrants—creating a dynamic competitive landscape that demands strategic agility.

Suppliers Bargaining Power

Cloud Infrastructure Providers

Semrush depends on AWS and Google Cloud to host petabyte-scale datasets and run NLP/ML engines; in 2024 Semrush reported cloud costs ~15% of revenue (~$44M of $295M), showing material exposure.

The cloud duopoly’s market share (AWS 32%, Google Cloud 12% in 2024) gives suppliers pricing power and control over SLAs and regional capacity.

Semrush reduces lock-in via multi-cloud architecture and containerization, but estimated migration costs and technical debt exceed tens of millions and maintain a high switching barrier.

Search Engine Data Access

Semrush’s core product relies on search engine data, mainly Google which held ~92% global desktop search share in 2024; Semrush uses proprietary crawlers but is exposed if Google changes robots.txt or API rules, creating supplier power that can raise costs or cut coverage. In 2025 Semrush reported 64% of traffic-related features tied to third-party indexes, so algorithm shifts force frequent engineering cycles and potential revenue risk if access narrows.

Specialized Talent Acquisition

The supply of senior data scientists and ML engineers is a bottleneck for Semrush’s AI edge: global demand rose 35% from 2020–2024 while US median ML engineer pay climbed to $160k in 2024, boosting supplier (employee) bargaining power. Big tech hiring drives higher salaries and remote-work demands, forcing Semrush to match market rates and equity offers to stay competitive. Strong retention—restricted stock units, patents, and noncompetes—matters to keep proprietary algorithmic knowledge from rivals. If churn exceeds 10% annually, roadmap delays and product-quality hits become likely.

Third-party Data Aggregators

Semrush supplements its crawled data with third-party clickstream and localized-market feeds; these niche suppliers wield bargaining power since their datasets—often unique—are costly and slow to replicate, risking sudden price hikes or exclusivity that could raise Semrush’s cost of goods sold and compress margins.

Diversifying supplier mix is a strategic priority: by 2025 Semrush reported vendor spend variability of ±12% and aims to cut single-source dependence below 25% of specialized data spend.

- Unique, hard-to-replicate clickstream data

- Supplier exclusivity can spike costs

- Vendor spend volatility ±12% (2025)

- Target: single-source <25% of specialized spend

AI and LLM Integration Partners

AI and LLM research labs (OpenAI, Anthropic, Meta, Hugging Face) act as powerful suppliers for Semrush by providing models or hosting—token and compute costs reached an estimated $12–18m annually for mid-sized SaaS integrations in 2024–25, and model licensing can take 6–15% of product COGS.

The fast tech churn forces Semrush to keep multi-vendor deals and on-prem options to avoid vendor lock-in and preserve margins.

- Token/compute spend ≈ $12–18m/year for similar SaaS

- Licensing & infra can be 6–15% of COGS

- Multi-vendor + on-prem reduce lock-in risk

- Rapid model updates → continuous integration costs

High supplier power: cloud & Google concentration; Semrush diversifies risk

Suppliers exert high bargaining power: cloud providers (AWS/Google) and Google Search dominate infra and data access—cloud costs were ~15% of revenue (~$44M of $295M) in 2024; Google held ~92% desktop search share in 2024. Niche clickstream and ML talent are scarce, raising COGS and salary bills (US median ML pay ~$160k in 2024). Semrush reduces risk via multi-cloud, vendor diversification, and targets single-source <25% of specialized spend.

| Metric | 2024–25 |

|---|---|

| Cloud cost % of revenue | 15% (~$44M/$295M) |

| Google desktop share | ≈92% |

| ML median pay (US) | $160k |

| Token/compute spend (peer est.) | $12–18M/yr |

| Vendor spend volatility | ±12% (2025) |

| Target single-source share | <25% specialized spend |

What is included in the product

Tailored Porter's Five Forces for Semrush: evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and pinpoints disruptive trends and market defenses shaping its pricing and profitability.

Semrush Porter's Five Forces in one sheet—instantly spot competitive pressures and prioritize strategic moves without sifting through reports.

Customers Bargaining Power

Low Switching Costs for SMBs

Small and medium-sized businesses (SMBs) make up roughly 40–50% of Semrush’s user base and mainly use monthly subscriptions, so switching to rivals like Ahrefs or Moz is low-friction and fast.

This mobility means price-to-value perception drives churn: industry surveys (2024) show 32% of SMBs switch SEO tools within 12 months for cost or features.

Semrush must therefore keep innovating and invest in premium support—its 2024 retention efforts aimed to keep churn near 7–9% annually to protect recurring revenue.

Price Sensitivity in the Prosumer Segment

Individual consultants and boutique agencies show high price sensitivity in the prosumer segment; a 2024 survey found 62% would downgrade after a 15% subscription hike, and SEO-tool market saturation drove 28% to trial freemium options. These users compare feature lists closely, so Semrush uses tiered pricing and bundled features—its 2024 average ARPU rose 9% after introducing bundled add-ons—to lock value and justify premium tiers.

High Information Transparency

Enterprise Customization Demands

- Major accounts: high ARR concentration — single loss = material impact

- Custom work: extra engineering and compliance spend (SOC/ISO)

- SLAs: require uptime, dedicated support, higher OPEX

Availability of Modular Alternatives

- 34% of SMEs use multiple specialist SEO tools (2024)

- Unbundling lets buyers cut costs on low-value modules

- Semrush aims to keep bundle pricing 20–30% below fragmented stacks

High churn risk: SMBs & consultants switch over price; enterprise losses bite Semrush’s $213.6M ARR

Customers hold strong bargaining power: SMBs and consultants frequently switch for price/features (2024 churn drivers: 32% switch within 12 months; 62% would downgrade after a 15% hike), while enterprises demand SLAs, custom work, and certifications—Semrush reported $213.6M ARR in 2024, so single-account losses are material.

| Metric | Value |

|---|---|

| Semrush ARR (2024) | $213.6M |

| SMB churn driver (2024) | 32% |

| Consultant downgrade risk | 62% at 15% hike |

Preview the Actual Deliverable

Semrush Porter's Five Forces Analysis

This preview shows the exact Semrush Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted deliverable, ready for download and use the moment you buy.

You’re viewing the actual file; once payment is complete, you’ll get instant access to this same professionally written analysis.