SentinelOne Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

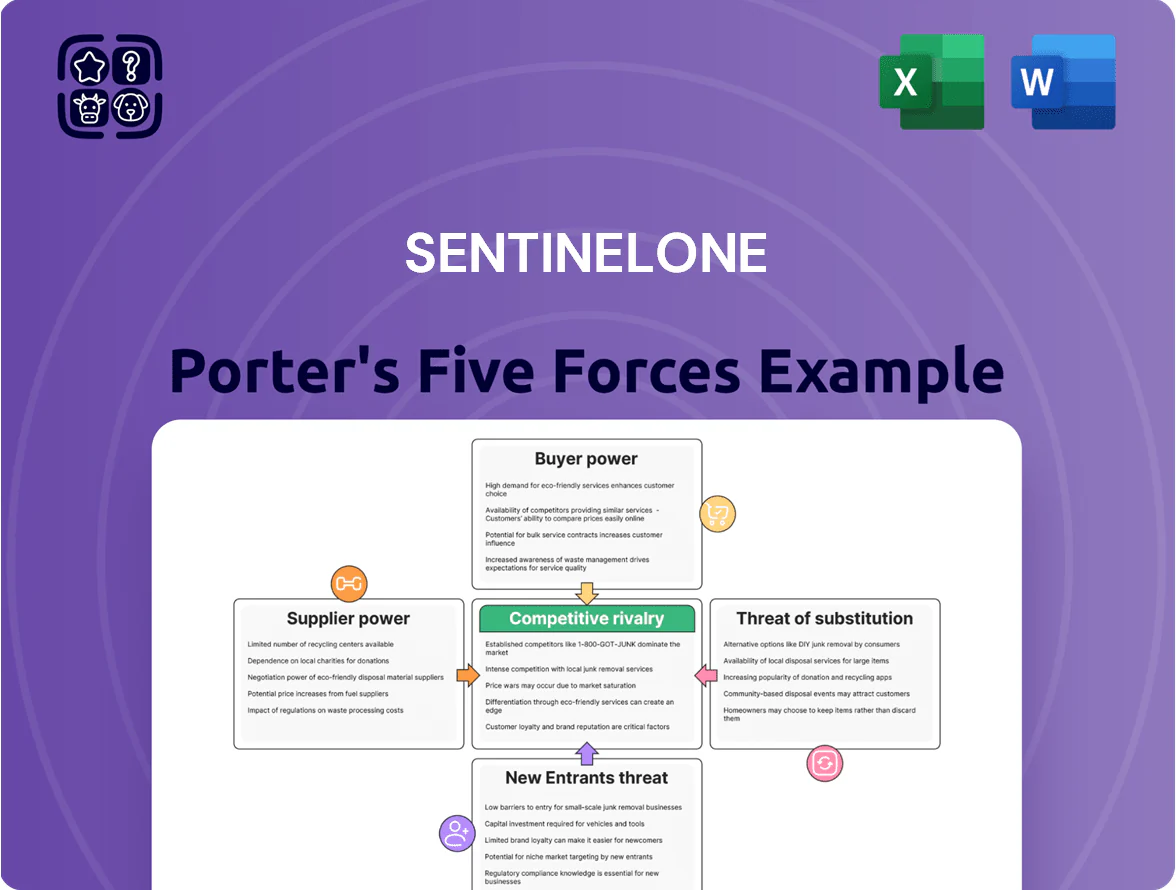

SentinelOne faces intense competitive rivalry and evolving substitute threats as endpoint security pivots toward integrated XDR solutions, while buyer sophistication and zero-day innovation raise switching risks and supplier leverage; this snapshot highlights key pressures but only skims the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategic moves.

Suppliers Bargaining Power

Cloud Infrastructure Providers

SentinelOne depends on hyperscalers—Amazon Web Services and Google Cloud—to host Singularity and process petabyte-scale telemetry; in 2025 SentinelOne disclosed cloud spend grew ~32% year-over-year to roughly $160M, showing material dependency. Migrating large-scale AI workloads carries multi-million-dollar replatforming costs and months of engineering, so hyperscalers wield pricing power; with AWS/GCP controlling ~62% of global cloud IaaS in 2024, SentinelOne has limited negotiation leverage on compute and storage.

Specialized Semiconductor Developers

SentinelOne's AI model performance depends on high-performance GPUs from suppliers like NVIDIA, which held ~80% market share in data-center GPUs in 2024 and raised average selling prices by ~12% YoY in 2024, giving suppliers pricing power through 2025.

Cybersecurity Talent and Researchers

The pool of researchers and engineers who build autonomous AI and run threat research is small and in high demand, giving suppliers strong bargaining power.

Top talent commands high pay and equity—US median AI engineer salary exceeded $190,000 in 2024 and stock-heavy offers are common—raising SentinelOne’s R&D cost base.

SentinelOne competes with Big Tech (Google, Microsoft, Meta) and well-funded startups, risking talent poaching and higher churn unless it matches cash and equity packages.

Third-Party Data Feed Providers

SentinelOne relies on multiple third-party threat feeds and software libraries to keep detection models current; in 2024 the company reported integrating over 50 external feeds and partnerships that feed its Singularity XDR telemetry.

Dependence on a few high-fidelity providers creates supplier power: if a major partner changes pricing or cuts access, detection quality could drop and mean-time-to-detect could rise weeks while models retrain.

Here’s the quick math: losing one top feed that supplies 20% of unique IOCs could reduce coverage materially until replacements are onboarded.

- 50+ external feeds (2024)

- Top feeds can supply ~20% unique IOCs

- Term changes risk temporary detection degradation

- Onboarding replacements can take weeks

Regulatory and Compliance Auditors

Regulatory and compliance auditors wield institutional power over SentinelOne by certifying data sovereignty and security standards needed for global contracts; failing to obtain FedRAMP, UK NCSC, or GDPR-aligned attestations can bar access to markets that represented over 35% of enterprise security spend in 2024.

These auditors are essential partners: losing certification risks multi-million-dollar contract exclusions (typical government deals range $5–50M) and slows deployment timelines by months, raising go-to-market costs and customer churn.

- Certifications dictate market access

- 2024: 35%+ enterprise spend tied to compliance

- Govt deals often $5–50M

- Audit delays add months and higher churn

Supplier concentration (hyperscalers/GPUs/feeds/auditors) threatens SentinelOne’s deals

Suppliers—hyperscalers (AWS/GCP ~62% IaaS share 2024), NVIDIA GPUs (~80% DC GPU share 2024), top threat-feed vendors (50+ feeds; top feed ≈20% unique IOCs), and compliance auditors (FedRAMP/UK NCSC/GDPR)—hold strong bargaining power, raising SentinelOne’s operational and R&D costs, creating single-point risks, and imposing multi-month remediation timelines that can block $5–50M government deals.

| Supplier | Key Metric | Impact |

|---|---|---|

| Hyperscalers | AWS/GCP ~62% IaaS (2024) | Pricing, replatform cost |

| GPUs | NVIDIA ~80% DC share (2024) | Price & supply risk |

| Threat feeds | 50+ feeds; top ~20% IOCs | Detection gaps if lost |

| Auditors | Certs required; gov't deals $5–50M | Market access risk |

What is included in the product

Tailored exclusively for SentinelOne, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer influence, entry barriers, substitutes, and emerging threats shaping its cybersecurity market position.

A concise Porter's Five Forces one-sheet for SentinelOne—quickly assess competitive pressures and tailor strategies with an editable radar chart and simple layout for decks or dashboards.

Customers Bargaining Power

Concentrated Enterprise Buying Power

Large enterprise clients and government agencies account for roughly 45–55% of SentinelOne’s ARR (2024 filings) and can demand custom features and steep volume discounts; procurements often run bake-offs against CrowdStrike and Microsoft Defender, driving price pressure. These buyers can shift thousands of seats at contract renewal—typical enterprise deals exceed $1m—so renewal leverage materially affects average contract value and gross retention.

Low Switching Costs for SaaS Models

The cloud-native shift lowers switching costs for SaaS security: automated orchestration and APIs let customers deploy new agents in hours vs months for on‑prem, making churn easier. In 2024, 42% of enterprises reported piloting alternative EDR/XDR vendors within 12 months, pressuring SentinelOne to prove superior ROI—SentinelOne must show measurable cost savings and reduce breach dwell time below industry avg 74 days to retain clients.

Channel Partner Influence

Channel partners—MSSPs and resellers—drive roughly 50–60% of SentinelOne’s 2024 ARR (company filings), so they can steer end-customer choice by preferring vendors with higher margins or simpler integration.

That buying concentration gives partners tangible bargaining power: switching product recommendations can shift large deal flow and affect renewal rates.

SentinelOne therefore must offer competitive partner margins, co-sell support, and tight integrations; in 2024 the company increased channel incentives by ~10% to defend share.

Budget Sensitivity in Economic Volatility

As IT budgets tightened in 2024–25, 62% of enterprises reported increased scrutiny on cybersecurity spend, pushing buyers toward platform consolidation to cut total cost of ownership (Gartner, 2024).

Customers now demand multi-module platforms under one license, forcing vendors like SentinelOne to include integrated features at stable price points and compress per-module margins.

Here’s the quick math: if a bundled deal raises seat revenue 10% but cuts per-module price 25%, margin per module falls sharply—pressure that scales with large enterprise deals.

- 62% of enterprises increased cybersecurity scrutiny (Gartner 2024)

- Buyers favor bundled licenses to lower TCO

- Demand for integrated features squeezes per-module margins

- Large deals amplify margin pressure—example: 10% seat revenue vs 25% per-module price cut

Information Transparency and Peer Reviews

Availability of transparent MITRE Engenuity results and peer reviews lets buyers verify SentinelOne’s efficacy; MITRE v4 tests (2024) show leading EDR detection rates ~98%, used in negotiations.

Customers cite lab benchmarks to rebut vendor claims and demand SLAs tied to measured metrics, lowering pricing power.

High transparency cuts vendor-favored information asymmetry, shifting leverage to informed buyers.

- MITRE v4 ~98% detection cited

Channel-driven price pressure and budget cuts force SentinelOne to boost incentives

Large enterprises and govts (45–55% of ARR, 2024) plus channel partners (50–60% of ARR) exert strong price and feature demands; 62% of firms tightened cyber budgets (Gartner 2024) and buyers pilot alternatives (42% in 12 months), pressuring renewals and margins—MITRE v4 (~98% detection) raises transparency, so SentinelOne boosts channel incentives (~+10% in 2024) to defend share.

| Metric | 2024 |

|---|---|

| Enterprise ARR share | 45–55% |

| Channel ARR share | 50–60% |

| Budget scrutiny | 62% |

| Piloting alternatives | 42% |

Same Document Delivered

SentinelOne Porter's Five Forces Analysis

This preview shows the exact SentinelOne Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SentinelOne faces intense competitive rivalry and evolving substitute threats as endpoint security pivots toward integrated XDR solutions, while buyer sophistication and zero-day innovation raise switching risks and supplier leverage; this snapshot highlights key pressures but only skims the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategic moves.

Suppliers Bargaining Power

Cloud Infrastructure Providers

SentinelOne depends on hyperscalers—Amazon Web Services and Google Cloud—to host Singularity and process petabyte-scale telemetry; in 2025 SentinelOne disclosed cloud spend grew ~32% year-over-year to roughly $160M, showing material dependency. Migrating large-scale AI workloads carries multi-million-dollar replatforming costs and months of engineering, so hyperscalers wield pricing power; with AWS/GCP controlling ~62% of global cloud IaaS in 2024, SentinelOne has limited negotiation leverage on compute and storage.

Specialized Semiconductor Developers

SentinelOne's AI model performance depends on high-performance GPUs from suppliers like NVIDIA, which held ~80% market share in data-center GPUs in 2024 and raised average selling prices by ~12% YoY in 2024, giving suppliers pricing power through 2025.

Cybersecurity Talent and Researchers

The pool of researchers and engineers who build autonomous AI and run threat research is small and in high demand, giving suppliers strong bargaining power.

Top talent commands high pay and equity—US median AI engineer salary exceeded $190,000 in 2024 and stock-heavy offers are common—raising SentinelOne’s R&D cost base.

SentinelOne competes with Big Tech (Google, Microsoft, Meta) and well-funded startups, risking talent poaching and higher churn unless it matches cash and equity packages.

Third-Party Data Feed Providers

SentinelOne relies on multiple third-party threat feeds and software libraries to keep detection models current; in 2024 the company reported integrating over 50 external feeds and partnerships that feed its Singularity XDR telemetry.

Dependence on a few high-fidelity providers creates supplier power: if a major partner changes pricing or cuts access, detection quality could drop and mean-time-to-detect could rise weeks while models retrain.

Here’s the quick math: losing one top feed that supplies 20% of unique IOCs could reduce coverage materially until replacements are onboarded.

- 50+ external feeds (2024)

- Top feeds can supply ~20% unique IOCs

- Term changes risk temporary detection degradation

- Onboarding replacements can take weeks

Regulatory and Compliance Auditors

Regulatory and compliance auditors wield institutional power over SentinelOne by certifying data sovereignty and security standards needed for global contracts; failing to obtain FedRAMP, UK NCSC, or GDPR-aligned attestations can bar access to markets that represented over 35% of enterprise security spend in 2024.

These auditors are essential partners: losing certification risks multi-million-dollar contract exclusions (typical government deals range $5–50M) and slows deployment timelines by months, raising go-to-market costs and customer churn.

- Certifications dictate market access

- 2024: 35%+ enterprise spend tied to compliance

- Govt deals often $5–50M

- Audit delays add months and higher churn

Supplier concentration (hyperscalers/GPUs/feeds/auditors) threatens SentinelOne’s deals

Suppliers—hyperscalers (AWS/GCP ~62% IaaS share 2024), NVIDIA GPUs (~80% DC GPU share 2024), top threat-feed vendors (50+ feeds; top feed ≈20% unique IOCs), and compliance auditors (FedRAMP/UK NCSC/GDPR)—hold strong bargaining power, raising SentinelOne’s operational and R&D costs, creating single-point risks, and imposing multi-month remediation timelines that can block $5–50M government deals.

| Supplier | Key Metric | Impact |

|---|---|---|

| Hyperscalers | AWS/GCP ~62% IaaS (2024) | Pricing, replatform cost |

| GPUs | NVIDIA ~80% DC share (2024) | Price & supply risk |

| Threat feeds | 50+ feeds; top ~20% IOCs | Detection gaps if lost |

| Auditors | Certs required; gov't deals $5–50M | Market access risk |

What is included in the product

Tailored exclusively for SentinelOne, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer influence, entry barriers, substitutes, and emerging threats shaping its cybersecurity market position.

A concise Porter's Five Forces one-sheet for SentinelOne—quickly assess competitive pressures and tailor strategies with an editable radar chart and simple layout for decks or dashboards.

Customers Bargaining Power

Concentrated Enterprise Buying Power

Large enterprise clients and government agencies account for roughly 45–55% of SentinelOne’s ARR (2024 filings) and can demand custom features and steep volume discounts; procurements often run bake-offs against CrowdStrike and Microsoft Defender, driving price pressure. These buyers can shift thousands of seats at contract renewal—typical enterprise deals exceed $1m—so renewal leverage materially affects average contract value and gross retention.

Low Switching Costs for SaaS Models

The cloud-native shift lowers switching costs for SaaS security: automated orchestration and APIs let customers deploy new agents in hours vs months for on‑prem, making churn easier. In 2024, 42% of enterprises reported piloting alternative EDR/XDR vendors within 12 months, pressuring SentinelOne to prove superior ROI—SentinelOne must show measurable cost savings and reduce breach dwell time below industry avg 74 days to retain clients.

Channel Partner Influence

Channel partners—MSSPs and resellers—drive roughly 50–60% of SentinelOne’s 2024 ARR (company filings), so they can steer end-customer choice by preferring vendors with higher margins or simpler integration.

That buying concentration gives partners tangible bargaining power: switching product recommendations can shift large deal flow and affect renewal rates.

SentinelOne therefore must offer competitive partner margins, co-sell support, and tight integrations; in 2024 the company increased channel incentives by ~10% to defend share.

Budget Sensitivity in Economic Volatility

As IT budgets tightened in 2024–25, 62% of enterprises reported increased scrutiny on cybersecurity spend, pushing buyers toward platform consolidation to cut total cost of ownership (Gartner, 2024).

Customers now demand multi-module platforms under one license, forcing vendors like SentinelOne to include integrated features at stable price points and compress per-module margins.

Here’s the quick math: if a bundled deal raises seat revenue 10% but cuts per-module price 25%, margin per module falls sharply—pressure that scales with large enterprise deals.

- 62% of enterprises increased cybersecurity scrutiny (Gartner 2024)

- Buyers favor bundled licenses to lower TCO

- Demand for integrated features squeezes per-module margins

- Large deals amplify margin pressure—example: 10% seat revenue vs 25% per-module price cut

Information Transparency and Peer Reviews

Availability of transparent MITRE Engenuity results and peer reviews lets buyers verify SentinelOne’s efficacy; MITRE v4 tests (2024) show leading EDR detection rates ~98%, used in negotiations.

Customers cite lab benchmarks to rebut vendor claims and demand SLAs tied to measured metrics, lowering pricing power.

High transparency cuts vendor-favored information asymmetry, shifting leverage to informed buyers.

- MITRE v4 ~98% detection cited

Channel-driven price pressure and budget cuts force SentinelOne to boost incentives

Large enterprises and govts (45–55% of ARR, 2024) plus channel partners (50–60% of ARR) exert strong price and feature demands; 62% of firms tightened cyber budgets (Gartner 2024) and buyers pilot alternatives (42% in 12 months), pressuring renewals and margins—MITRE v4 (~98% detection) raises transparency, so SentinelOne boosts channel incentives (~+10% in 2024) to defend share.

| Metric | 2024 |

|---|---|

| Enterprise ARR share | 45–55% |

| Channel ARR share | 50–60% |

| Budget scrutiny | 62% |

| Piloting alternatives | 42% |

Same Document Delivered

SentinelOne Porter's Five Forces Analysis

This preview shows the exact SentinelOne Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.