Sequoia Logística Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

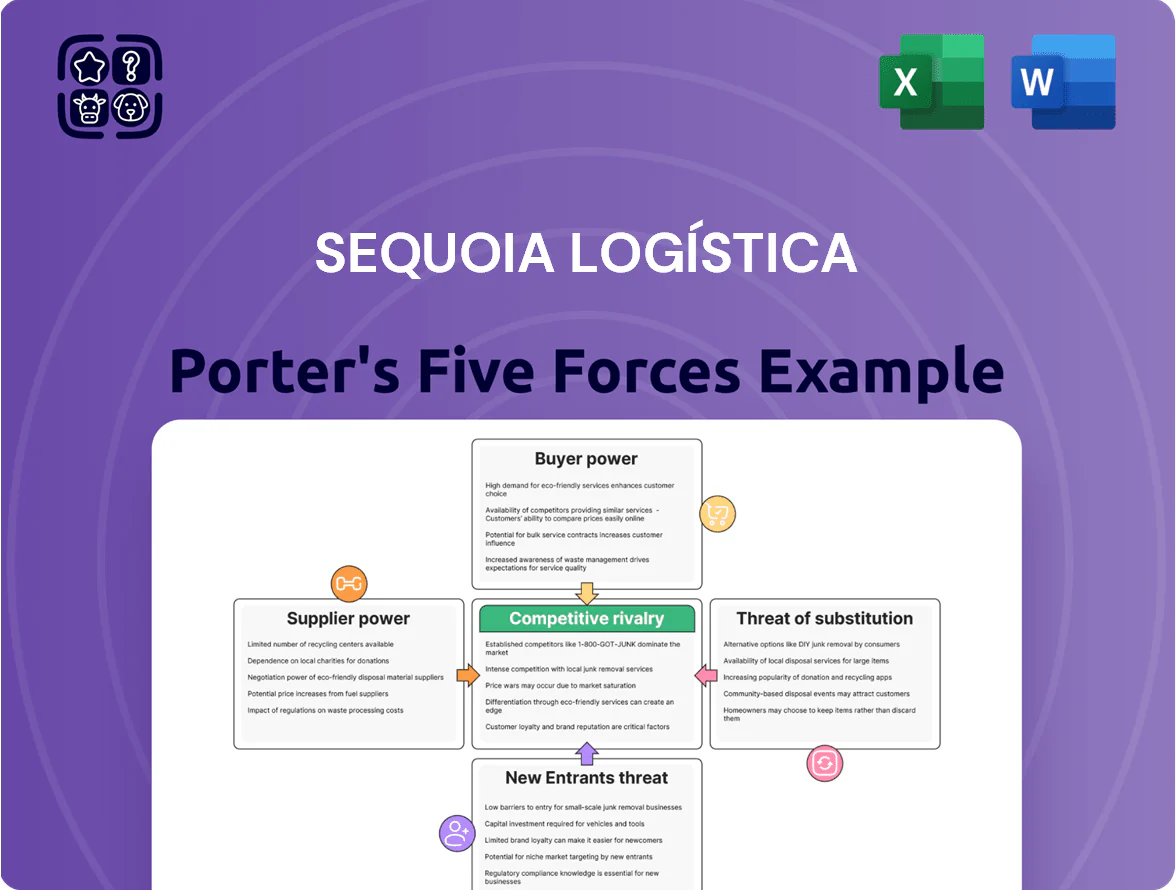

Sequoia Logística faces moderate buyer power and supplier influence, while barriers to entry and competitive rivalry hinge on scale, network reach, and tech integration—creating both resilience and pressure points for margins and growth.

Suppliers Bargaining Power

Volatility of Fuel and Energy Prices

Fuel and energy costs account for roughly 20–30% of operating expenses for Brazilian road freight firms; for Sequoia Logística this exposure is material given long-haul fleets and diesel use.

Sequoia is a price taker: international Brent movements and Petrobras retail pricing (regulated margins) set diesel prices, limiting Sequoia’s control.

Sudden spikes—diesel rose ~35% in 2022–23 in Brazil—can cut margins sharply if Sequoia cannot pass increases to shippers within contracted rates.

Dependency on Vehicle Manufacturers and Parts

The availability and pricing of trucks and vans are critical for Sequoia Logística; commercial vehicles account for ~35% of its FY2024 capex, so procurement costs directly affect margins.

Supplier power is moderate: three OEMs (Volkswagen Caminhões, Mercedes-Benz, and Iveco) held ~60% of South American commercial vehicle market in 2024, limiting Sequoia’s bargaining room.

Global supply shocks—chip shortages and 2023–24 container delays—increased unit acquisition costs by ~12%, risking slower fleet renewal and higher operating costs.

Labor and Third-Party Driver Availability

Sequoia depends on direct staff and ~100,000 agregados (freelance drivers across Brazil), so unions and driver scarcity push wages and fees up; union-led strikes in 2023 raised regional pay rates by ~8–12%.

Specialized Technology and Software Providers

- High license costs: $200k–$1.2M/yr

- Switching friction: complex API integrations

- 62% of outages linked to software

- 8% global WMS/TMS adoption rise in 2024

Strategic Warehouse Real Estate Access

Securing prime distribution and last-mile hubs in São Paulo and Rio de Janeiro is critical because zoned industrial land within 20 km of CBDs is <25% of total stock, pushing rents 20–40% above outskirts (2025 market reports).

Landlords wield strong bargaining power: vacancy rates in core logistics submarkets fell below 3% in 2024, forcing Sequoia into long-term leases with annual inflation clauses (commonly IPCA + 4%), which raises fixed-cost volatility.

What this estimate hides: aggressive rent escalators can erode EBITDA margins by 1–3 percentage points over five years if revenue growth lags.

- Core urban logistics vacancy <3% (2024)

- Prime rents 20–40% premium vs outskirts

- Typical lease indexation IPCA + 4%

- Potential EBITDA hit 1–3 ppt over 5 years

Suppliers Tighten Grip: Fuel, OEMs, WMS/TMS Costs and Scarce Space Squeeze Margins

Suppliers exert moderate-to-strong power: fuel (20–30% opex) and diesel pricing set by Brent/Petrobras limit Sequoia’s control; vehicle OEMs (~60% market share) and 12% higher unit costs from recent shocks constrain fleet procurement; WMS/TMS vendor lock (licenses $200k–$1.2M/yr; 62% outages tied to integrations) and <3% core vacancy with 20–40% rent premium tighten bargaining.

| Metric | Value (2024–25) |

|---|---|

| Fuel % of opex | 20–30% |

| OEM market share | ~60% |

| Unit cost shock | +12% |

| WMS/TMS license | $200k–$1.2M/yr |

| Core vacancy | <3% |

What is included in the product

Tailored exclusively for Sequoia Logística, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape pricing, profitability, and strategic positioning.

Concise five-forces summary tailored for Sequoia Logística—clarifies competitive pressure and relief strategies for rapid boardroom decisions.

Customers Bargaining Power

Concentration of Major E-commerce Clients

A large share of Sequoia Logística’s 2025 revenue—about 55%—comes from three major e-commerce and retail clients, concentrating bargaining power with buyers.

These high-volume customers routinely negotiate price cuts of 8–15% and stricter SLAs, squeezing Sequoia’s margin; in 2024 gross margin fell 220 basis points after similar pressure.

If one top client representing ~20% revenue switches providers, Sequoia’s EBITDA could drop by roughly the same share within 12 months, forcing capacity and pricing adjustments.

Low Switching Costs for Shippers

For many shippers price and delivery speed are the main differentiators, and with 78% of US firms reporting comparable tracking services in 2024, switching providers carries low friction; brokerage churn averaged 12% annually in 2023. This pressure forces Sequoia Logística to invest in continuous innovation and service quality—Sequoia must match sub-48h delivery targets and hold on to net revenue retention above 90% to prevent client losses.

Demand for Integrated Digital Solutions

Modern customers demand seamless API links between sales platforms and Sequoia Logística’s tracking; 68% of logistics buyers in 2024 rated real-time integration as a top purchase criterion, giving buyers leverage to require custom features before contracting.

Clients can push for SLAs tied to visibility and analytics; firms lacking live tracking and BI lose large enterprise accounts—Sequoia risks churn given 54% of corporate shippers switch providers for better tech in 2025.

Price Sensitivity in a Volatile Economy

Brazilian retailers, facing 2023–2025 real wage stagnation and 5–8% annual inflation spikes, push Sequoia Logística to absorb cost increases to keep shelf prices competitive, constraining Sequoia’s pricing power.

When fuel and freight-related inputs rose ~12% YoY in 2024, Sequoia could not fully pass costs through; client churn risk and price-sensitive demand capped price hikes.

- High price sensitivity: retailers pass through shipping to consumers

- 2024 input cost rise ~12% YoY limited pass-through

- Inflation 5–8% (2023–25) increases pressure

- Limits Sequoia’s ability to raise prices

Rise of Performance-Based Contracts

Customers now push for performance-based contracts with strict penalties for delays or damaged goods, shifting operational risk onto Sequoia Logística; a 2024 survey by Armstrong Logistics found 62% of shippers demand penalty clauses.

These clauses mean Sequoia must hit near-perfect execution—each 1% service failure can translate to 0.5–2% revenue loss from penalties and rebates, lowering net price received.

Sequoia should invest in tracking, buffer capacity, and insurance; failing to do so raises churn and margin erosion amid 4–7% industry EBITDA pressures noted in 2023–24.

- 62% shippers demand penalties (Armstrong Logistics 2024)

- 1% failures → 0.5–2% revenue hit

- Industry EBITDA pressure 4–7% (2023–24)

Concentrated buyers squeeze margins—invest in APIs, penalties, and buffers to protect NRR

Buyers hold strong leverage: three clients provide ~55% of 2025 revenue, top client ~20%; they negotiate 8–15% discounts and strict SLAs, pressuring margins (gross margin down 220 bps in 2024).

Switching costs are low—brokerage churn 12% (2023); 68% of buyers rate real-time API integration top criterion (2024), and 62% demand penalty clauses, so Sequoia must invest in tech and buffers to protect >90% NRR.

| Metric | Value |

|---|---|

| Revenue concentration (3 clients) | 55% |

| Top client share | ~20% |

| Buyer discount range | 8–15% |

| Gross margin change (2024) | −220 bps |

| Brokerage churn (2023) | 12% |

| Real-time API priority (2024) | 68% |

| Shippers demanding penalties (2024) | 62% |

Full Version Awaits

Sequoia Logística Porter's Five Forces Analysis

This preview shows the exact Sequoia Logística Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Sequoia Logística faces moderate buyer power and supplier influence, while barriers to entry and competitive rivalry hinge on scale, network reach, and tech integration—creating both resilience and pressure points for margins and growth.

Suppliers Bargaining Power

Volatility of Fuel and Energy Prices

Fuel and energy costs account for roughly 20–30% of operating expenses for Brazilian road freight firms; for Sequoia Logística this exposure is material given long-haul fleets and diesel use.

Sequoia is a price taker: international Brent movements and Petrobras retail pricing (regulated margins) set diesel prices, limiting Sequoia’s control.

Sudden spikes—diesel rose ~35% in 2022–23 in Brazil—can cut margins sharply if Sequoia cannot pass increases to shippers within contracted rates.

Dependency on Vehicle Manufacturers and Parts

The availability and pricing of trucks and vans are critical for Sequoia Logística; commercial vehicles account for ~35% of its FY2024 capex, so procurement costs directly affect margins.

Supplier power is moderate: three OEMs (Volkswagen Caminhões, Mercedes-Benz, and Iveco) held ~60% of South American commercial vehicle market in 2024, limiting Sequoia’s bargaining room.

Global supply shocks—chip shortages and 2023–24 container delays—increased unit acquisition costs by ~12%, risking slower fleet renewal and higher operating costs.

Labor and Third-Party Driver Availability

Sequoia depends on direct staff and ~100,000 agregados (freelance drivers across Brazil), so unions and driver scarcity push wages and fees up; union-led strikes in 2023 raised regional pay rates by ~8–12%.

Specialized Technology and Software Providers

- High license costs: $200k–$1.2M/yr

- Switching friction: complex API integrations

- 62% of outages linked to software

- 8% global WMS/TMS adoption rise in 2024

Strategic Warehouse Real Estate Access

Securing prime distribution and last-mile hubs in São Paulo and Rio de Janeiro is critical because zoned industrial land within 20 km of CBDs is <25% of total stock, pushing rents 20–40% above outskirts (2025 market reports).

Landlords wield strong bargaining power: vacancy rates in core logistics submarkets fell below 3% in 2024, forcing Sequoia into long-term leases with annual inflation clauses (commonly IPCA + 4%), which raises fixed-cost volatility.

What this estimate hides: aggressive rent escalators can erode EBITDA margins by 1–3 percentage points over five years if revenue growth lags.

- Core urban logistics vacancy <3% (2024)

- Prime rents 20–40% premium vs outskirts

- Typical lease indexation IPCA + 4%

- Potential EBITDA hit 1–3 ppt over 5 years

Suppliers Tighten Grip: Fuel, OEMs, WMS/TMS Costs and Scarce Space Squeeze Margins

Suppliers exert moderate-to-strong power: fuel (20–30% opex) and diesel pricing set by Brent/Petrobras limit Sequoia’s control; vehicle OEMs (~60% market share) and 12% higher unit costs from recent shocks constrain fleet procurement; WMS/TMS vendor lock (licenses $200k–$1.2M/yr; 62% outages tied to integrations) and <3% core vacancy with 20–40% rent premium tighten bargaining.

| Metric | Value (2024–25) |

|---|---|

| Fuel % of opex | 20–30% |

| OEM market share | ~60% |

| Unit cost shock | +12% |

| WMS/TMS license | $200k–$1.2M/yr |

| Core vacancy | <3% |

What is included in the product

Tailored exclusively for Sequoia Logística, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape pricing, profitability, and strategic positioning.

Concise five-forces summary tailored for Sequoia Logística—clarifies competitive pressure and relief strategies for rapid boardroom decisions.

Customers Bargaining Power

Concentration of Major E-commerce Clients

A large share of Sequoia Logística’s 2025 revenue—about 55%—comes from three major e-commerce and retail clients, concentrating bargaining power with buyers.

These high-volume customers routinely negotiate price cuts of 8–15% and stricter SLAs, squeezing Sequoia’s margin; in 2024 gross margin fell 220 basis points after similar pressure.

If one top client representing ~20% revenue switches providers, Sequoia’s EBITDA could drop by roughly the same share within 12 months, forcing capacity and pricing adjustments.

Low Switching Costs for Shippers

For many shippers price and delivery speed are the main differentiators, and with 78% of US firms reporting comparable tracking services in 2024, switching providers carries low friction; brokerage churn averaged 12% annually in 2023. This pressure forces Sequoia Logística to invest in continuous innovation and service quality—Sequoia must match sub-48h delivery targets and hold on to net revenue retention above 90% to prevent client losses.

Demand for Integrated Digital Solutions

Modern customers demand seamless API links between sales platforms and Sequoia Logística’s tracking; 68% of logistics buyers in 2024 rated real-time integration as a top purchase criterion, giving buyers leverage to require custom features before contracting.

Clients can push for SLAs tied to visibility and analytics; firms lacking live tracking and BI lose large enterprise accounts—Sequoia risks churn given 54% of corporate shippers switch providers for better tech in 2025.

Price Sensitivity in a Volatile Economy

Brazilian retailers, facing 2023–2025 real wage stagnation and 5–8% annual inflation spikes, push Sequoia Logística to absorb cost increases to keep shelf prices competitive, constraining Sequoia’s pricing power.

When fuel and freight-related inputs rose ~12% YoY in 2024, Sequoia could not fully pass costs through; client churn risk and price-sensitive demand capped price hikes.

- High price sensitivity: retailers pass through shipping to consumers

- 2024 input cost rise ~12% YoY limited pass-through

- Inflation 5–8% (2023–25) increases pressure

- Limits Sequoia’s ability to raise prices

Rise of Performance-Based Contracts

Customers now push for performance-based contracts with strict penalties for delays or damaged goods, shifting operational risk onto Sequoia Logística; a 2024 survey by Armstrong Logistics found 62% of shippers demand penalty clauses.

These clauses mean Sequoia must hit near-perfect execution—each 1% service failure can translate to 0.5–2% revenue loss from penalties and rebates, lowering net price received.

Sequoia should invest in tracking, buffer capacity, and insurance; failing to do so raises churn and margin erosion amid 4–7% industry EBITDA pressures noted in 2023–24.

- 62% shippers demand penalties (Armstrong Logistics 2024)

- 1% failures → 0.5–2% revenue hit

- Industry EBITDA pressure 4–7% (2023–24)

Concentrated buyers squeeze margins—invest in APIs, penalties, and buffers to protect NRR

Buyers hold strong leverage: three clients provide ~55% of 2025 revenue, top client ~20%; they negotiate 8–15% discounts and strict SLAs, pressuring margins (gross margin down 220 bps in 2024).

Switching costs are low—brokerage churn 12% (2023); 68% of buyers rate real-time API integration top criterion (2024), and 62% demand penalty clauses, so Sequoia must invest in tech and buffers to protect >90% NRR.

| Metric | Value |

|---|---|

| Revenue concentration (3 clients) | 55% |

| Top client share | ~20% |

| Buyer discount range | 8–15% |

| Gross margin change (2024) | −220 bps |

| Brokerage churn (2023) | 12% |

| Real-time API priority (2024) | 68% |

| Shippers demanding penalties (2024) | 62% |

Full Version Awaits

Sequoia Logística Porter's Five Forces Analysis

This preview shows the exact Sequoia Logística Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.