Serica Energy Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

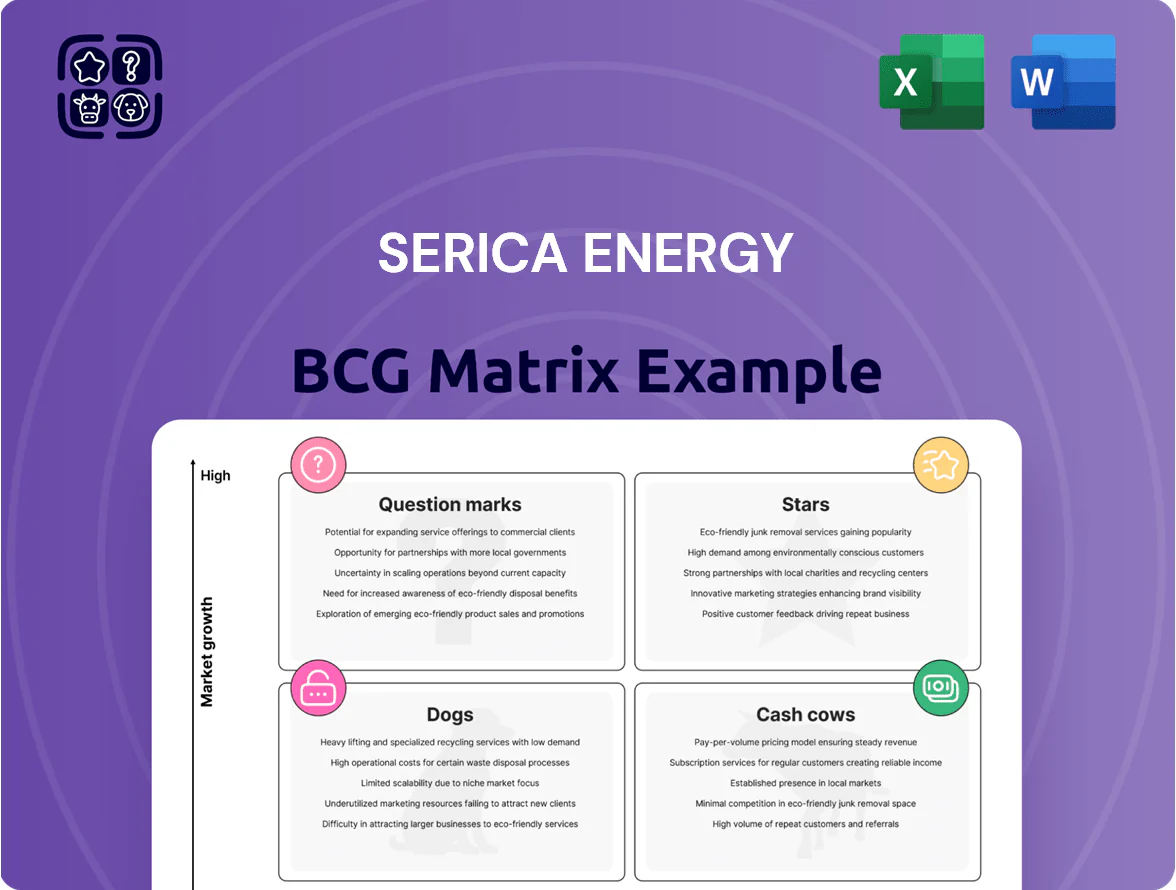

Serica Energy’s BCG Matrix preview highlights how its asset mix and production hubs might map to Stars, Cash Cows, Question Marks, or Dogs amid volatile energy markets; early signs point to strong cash-generating North Sea fields alongside exploratory assets needing strategic choices. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide capital allocation and operational focus.

Stars

Triton Hub Area

The Triton Hub Area has become Serica Energy’s primary growth engine after 2024–2025 drilling that boosted capacity by about 35%, with Bittern and Guillemot NW infill wells lifting liquids output and raising liquids share to roughly 58% of production entering 2026. Serica’s planned 2026 capex of ~45–55 million dollars targets throughput maximization via the Triton FPSO, aiming to capture dominant Central North Sea market share. Continued investment is required to sustain the growth trajectory, but Triton is currently the company’s top production contributor.

Belinda Field Development

Belinda, a high-growth subsea tie-back, hit first oil in Jan 2026 and adds ~15–20 kbbl/d of high‑margin liquids, lifting Serica Energy’s near‑term production by ~25%; initial 2026 EBITDA contribution is estimated at £40–60m.

Using Triton platform infrastructure cut capex by ~40% versus stand‑alone tie‑backs, yielding payback under 2 years and IRRs above 40%, matching Serica’s quick‑cycle strategy and offsetting basin decline.

Greater Laggan Area Acquisition

The 40% operated stake in the Greater Laggan Area (GLA), closing early 2026, sits in Serica Energy’s star quadrant due to high-volume gas output and control of the Shetland Gas Plant, boosting UK gas security.

Integration capex is estimated at ~£120–180m; the asset could add ~20–30k boepd gross, supporting Serica’s target to exceed 65,000 boepd by end-2026 and materially growing market share.

Cygnus Gas Field Interest

Acquired via the Spirit Energy deal in late 2025, Serica’s 15 percent Cygnus stake secures exposure to one of the UK’s largest, low-emission gas fields, reporting ~98% uptime and ~120 mcm/day peak throughput in 2025.

Continuous drilling supports production growth into the late 2020s, keeping unit operating costs below $3/boe and boosting Southern North Sea market share while meeting sustainability targets.

As a flagship, high-reliability growth asset, Cygnus warrants continued capital and operational focus to extract value and cut emissions.

- 15% interest acquired late 2025

- ~98% uptime; ~120 mcm/day peak 2025

- Unit Opex < $3/boe

- Production growth via ongoing drilling

Organic Growth Infill Campaigns

Serica Energy’s multi-asset infill drilling across BKR and Triton acts as a collective star, driving a projected >50% production increase to ~105 kbbl/d in 2026 versus 2024, funded by ~£250–300m capex in 2025–26.

High-grading wells raises incremental barrel recovery per well by 20–35%, helping Serica grab North Sea market share while consuming short-term cash to reach a higher production plateau.

Data-driven reservoir modeling and phased development keep unit lifting costs near current ~US$18–22/bbl, preserving free cash flow upside as volumes scale.

- Projected >50% production growth to ~105 kbbl/d in 2026

- £250–300m capex 2025–26 for infill campaign

- 20–35% uplift in per-well recovery from high-grading

- Unit lifting costs ~US$18–22/bbl

Infill-led growth to ~105 kbbl/d by 2026 — rapid paybacks, >40% IRRs, £40–60m EBITDA lift

Stars: Triton Hub, Belinda, GLA, Cygnus and BKR infill drive >50% production growth to ~105 kbbl/d in 2026, supported by £250–300m capex (2025–26), unit opex <$3/boe (gas) and US$18–22/bbl (liquids); paybacks <2 years and IRRs >40% on tie‑backs; 2026 EBITDA lift ~£40–60m from Belinda; integration capex GLA ~£120–180m.

| Asset | 2026 Prod | Capex (£m) | Unit Cost | Key Metric |

|---|---|---|---|---|

| Triton Hub | ~58% liquids | 45–55 (2026) | US$18–22/bbl | 35% capacity lift |

| Belinda | 15–20 kbbl/d | — | high‑margin | EBITDA £40–60m |

| GLA (40%) | 20–30 kboepd gross | 120–180 | <£3/boe gas | Operated |

| Cygnus (15%) | ~120 mcm/day peak | — | <£3/boe gas | 98% uptime 2025 |

What is included in the product

Concise BCG analysis of Serica Energy’s assets with quadrant strategies, investment recommendations, and trend-driven risks/opportunities.

One-page Serica Energy BCG Matrix placing each asset in a quadrant for clear portfolio decisions

Cash Cows

Bruce Hub Operations

Bruce Hub Operations is Serica Energy’s primary cash cow, delivering ~230 MMscfd gas and ~18 kb/d condensate in 2025, funding dividends and growth.

As a mature asset it shows >95% uptime and hosts Keith and Rhum satellites, giving Serica dominant regional share and steady free cash flow.

Low growth but high margin: Bruce generated ~£240m EBITDA in 2025, so 2026 focuses on maintenance and life-extension to sustain cash returns.

Rhum Gas Field

Rhum is a high-rate gas asset generating a disproportionate share of Serica Energy’s free cash flow, producing ~280 mcm/d in 2025 and delivering roughly £140m EBITDA in FY2025 due to strong North Sea gas prices averaging ~£45/MWh in Q4 2025.

As a mature field with fixed platforms and pipelines, Rhum needs low sustaining capex (~£15–20m/year), preserving wide operating margins and free cash conversion.

Its steady liquidity underpins Serica’s debt service (net debt ~£130m at Dec 2025) and funds bolt-on purchases and Question Mark exploration plays.

Rhum remained a market leader in the Northern North Sea gas sector at end-2025, consistently ranking in the top five producers by output and cash yield.

Keith Field Satellite

The Keith Field acts as a low-growth, high-margin cash cow for Serica Energy, using Bruce Hub tie‑ins to produce mature barrels at minimal incremental cost and sustaining ~8–10 kbopd gross in 2024 with operating margins above 60%.

Production is smaller than Bruce or Rhum but commands ~70% market share in its sub‑basin, delivering steady EBITDA that underpins Serica’s 16p per share dividend policy.

Management prioritises maximizing recovery via infill wells and improved flow assurance while capping 2025 capex at under £10m to preserve free cash flow and profitability.

Shetland Gas Plant Infrastructure

With the GLA acquisition closing in June 2025, the Shetland Gas Plant is now a core midstream cash cow for Serica Energy, processing ~1.2 bcm/year of third-party gas and delivering roughly £60–70m EBITDA annually.

The plant’s dominant position in northern UK gas flows makes revenues less tied to NBP price swings than Serica’s upstream barrels, averaging ~15–20% margin volatility vs upstream.

High barriers—permit complexity, pipeline links, and limited nearby processing capacity—secure long-term low-growth cash generation supporting group capital allocation.

- Processes ~1.2 bcm/year

- Estimated £60–70m EBITDA p.a. (2025)

- Lower revenue sensitivity to NBP than upstream

- High entry barriers and strategic UK role

Catcher and Golden Eagle Interests

Serica Energy’s non-operated Catcher and Golden Eagle interests, integrated in 2025–2026, deliver high-quality North Sea production generating ~£85–95m EBITDA annually (2025 estimate) from established hubs with low technical risk.

These assets are post-peak, offering stable volumes and steady cash distributions from major partners, supporting liquidity while Serica funds capital-intensive projects; operating cash flow covers ~40–50% of 2025 capex.

- 2025 EBITDA est £85–95m

- Cash cover ~40–50% of capex 2025

- Low technical risk, stable volumes

- Income via partner distributions

Serica’s 2025–26 cash cows: ~£585–645m EBITDA funding dividends, debt and bolt‑ons

Bruce Hub, Rhum, Keith, Shetland Gas Plant and non‑ops (Catcher/Golden Eagle) are Serica’s cash cows in 2025–26, collectively delivering ~£585–645m EBITDA and funding dividends, debt service (net debt ~£130m Dec 2025) and bolt‑ons.

| Asset | 2025 Prod/Cap | 2025 EBITDA (£m) | Sustaining Capex (£m/yr) |

|---|---|---|---|

| Bruce Hub | 230 MMscfd gas; 18 kb/d condensate | 240 | 30–40 |

| Rhum | 280 mcm/d gas | 140 | 15–20 |

| Keith | 8–10 kbopd gross | ~35 | <10 |

| Shetland Gas Plant | 1.2 bcm/year | 60–70 | 10–15 |

| Catcher/Golden Eagle (non‑op) | Integrated output | 85–95 | 20–30 |

What You’re Viewing Is Included

Serica Energy BCG Matrix

The BCG Matrix you're previewing is the exact final file you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, presentation-ready strategic analysis designed for clear portfolio decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Serica Energy’s BCG Matrix preview highlights how its asset mix and production hubs might map to Stars, Cash Cows, Question Marks, or Dogs amid volatile energy markets; early signs point to strong cash-generating North Sea fields alongside exploratory assets needing strategic choices. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide capital allocation and operational focus.

Stars

Triton Hub Area

The Triton Hub Area has become Serica Energy’s primary growth engine after 2024–2025 drilling that boosted capacity by about 35%, with Bittern and Guillemot NW infill wells lifting liquids output and raising liquids share to roughly 58% of production entering 2026. Serica’s planned 2026 capex of ~45–55 million dollars targets throughput maximization via the Triton FPSO, aiming to capture dominant Central North Sea market share. Continued investment is required to sustain the growth trajectory, but Triton is currently the company’s top production contributor.

Belinda Field Development

Belinda, a high-growth subsea tie-back, hit first oil in Jan 2026 and adds ~15–20 kbbl/d of high‑margin liquids, lifting Serica Energy’s near‑term production by ~25%; initial 2026 EBITDA contribution is estimated at £40–60m.

Using Triton platform infrastructure cut capex by ~40% versus stand‑alone tie‑backs, yielding payback under 2 years and IRRs above 40%, matching Serica’s quick‑cycle strategy and offsetting basin decline.

Greater Laggan Area Acquisition

The 40% operated stake in the Greater Laggan Area (GLA), closing early 2026, sits in Serica Energy’s star quadrant due to high-volume gas output and control of the Shetland Gas Plant, boosting UK gas security.

Integration capex is estimated at ~£120–180m; the asset could add ~20–30k boepd gross, supporting Serica’s target to exceed 65,000 boepd by end-2026 and materially growing market share.

Cygnus Gas Field Interest

Acquired via the Spirit Energy deal in late 2025, Serica’s 15 percent Cygnus stake secures exposure to one of the UK’s largest, low-emission gas fields, reporting ~98% uptime and ~120 mcm/day peak throughput in 2025.

Continuous drilling supports production growth into the late 2020s, keeping unit operating costs below $3/boe and boosting Southern North Sea market share while meeting sustainability targets.

As a flagship, high-reliability growth asset, Cygnus warrants continued capital and operational focus to extract value and cut emissions.

- 15% interest acquired late 2025

- ~98% uptime; ~120 mcm/day peak 2025

- Unit Opex < $3/boe

- Production growth via ongoing drilling

Organic Growth Infill Campaigns

Serica Energy’s multi-asset infill drilling across BKR and Triton acts as a collective star, driving a projected >50% production increase to ~105 kbbl/d in 2026 versus 2024, funded by ~£250–300m capex in 2025–26.

High-grading wells raises incremental barrel recovery per well by 20–35%, helping Serica grab North Sea market share while consuming short-term cash to reach a higher production plateau.

Data-driven reservoir modeling and phased development keep unit lifting costs near current ~US$18–22/bbl, preserving free cash flow upside as volumes scale.

- Projected >50% production growth to ~105 kbbl/d in 2026

- £250–300m capex 2025–26 for infill campaign

- 20–35% uplift in per-well recovery from high-grading

- Unit lifting costs ~US$18–22/bbl

Infill-led growth to ~105 kbbl/d by 2026 — rapid paybacks, >40% IRRs, £40–60m EBITDA lift

Stars: Triton Hub, Belinda, GLA, Cygnus and BKR infill drive >50% production growth to ~105 kbbl/d in 2026, supported by £250–300m capex (2025–26), unit opex <$3/boe (gas) and US$18–22/bbl (liquids); paybacks <2 years and IRRs >40% on tie‑backs; 2026 EBITDA lift ~£40–60m from Belinda; integration capex GLA ~£120–180m.

| Asset | 2026 Prod | Capex (£m) | Unit Cost | Key Metric |

|---|---|---|---|---|

| Triton Hub | ~58% liquids | 45–55 (2026) | US$18–22/bbl | 35% capacity lift |

| Belinda | 15–20 kbbl/d | — | high‑margin | EBITDA £40–60m |

| GLA (40%) | 20–30 kboepd gross | 120–180 | <£3/boe gas | Operated |

| Cygnus (15%) | ~120 mcm/day peak | — | <£3/boe gas | 98% uptime 2025 |

What is included in the product

Concise BCG analysis of Serica Energy’s assets with quadrant strategies, investment recommendations, and trend-driven risks/opportunities.

One-page Serica Energy BCG Matrix placing each asset in a quadrant for clear portfolio decisions

Cash Cows

Bruce Hub Operations

Bruce Hub Operations is Serica Energy’s primary cash cow, delivering ~230 MMscfd gas and ~18 kb/d condensate in 2025, funding dividends and growth.

As a mature asset it shows >95% uptime and hosts Keith and Rhum satellites, giving Serica dominant regional share and steady free cash flow.

Low growth but high margin: Bruce generated ~£240m EBITDA in 2025, so 2026 focuses on maintenance and life-extension to sustain cash returns.

Rhum Gas Field

Rhum is a high-rate gas asset generating a disproportionate share of Serica Energy’s free cash flow, producing ~280 mcm/d in 2025 and delivering roughly £140m EBITDA in FY2025 due to strong North Sea gas prices averaging ~£45/MWh in Q4 2025.

As a mature field with fixed platforms and pipelines, Rhum needs low sustaining capex (~£15–20m/year), preserving wide operating margins and free cash conversion.

Its steady liquidity underpins Serica’s debt service (net debt ~£130m at Dec 2025) and funds bolt-on purchases and Question Mark exploration plays.

Rhum remained a market leader in the Northern North Sea gas sector at end-2025, consistently ranking in the top five producers by output and cash yield.

Keith Field Satellite

The Keith Field acts as a low-growth, high-margin cash cow for Serica Energy, using Bruce Hub tie‑ins to produce mature barrels at minimal incremental cost and sustaining ~8–10 kbopd gross in 2024 with operating margins above 60%.

Production is smaller than Bruce or Rhum but commands ~70% market share in its sub‑basin, delivering steady EBITDA that underpins Serica’s 16p per share dividend policy.

Management prioritises maximizing recovery via infill wells and improved flow assurance while capping 2025 capex at under £10m to preserve free cash flow and profitability.

Shetland Gas Plant Infrastructure

With the GLA acquisition closing in June 2025, the Shetland Gas Plant is now a core midstream cash cow for Serica Energy, processing ~1.2 bcm/year of third-party gas and delivering roughly £60–70m EBITDA annually.

The plant’s dominant position in northern UK gas flows makes revenues less tied to NBP price swings than Serica’s upstream barrels, averaging ~15–20% margin volatility vs upstream.

High barriers—permit complexity, pipeline links, and limited nearby processing capacity—secure long-term low-growth cash generation supporting group capital allocation.

- Processes ~1.2 bcm/year

- Estimated £60–70m EBITDA p.a. (2025)

- Lower revenue sensitivity to NBP than upstream

- High entry barriers and strategic UK role

Catcher and Golden Eagle Interests

Serica Energy’s non-operated Catcher and Golden Eagle interests, integrated in 2025–2026, deliver high-quality North Sea production generating ~£85–95m EBITDA annually (2025 estimate) from established hubs with low technical risk.

These assets are post-peak, offering stable volumes and steady cash distributions from major partners, supporting liquidity while Serica funds capital-intensive projects; operating cash flow covers ~40–50% of 2025 capex.

- 2025 EBITDA est £85–95m

- Cash cover ~40–50% of capex 2025

- Low technical risk, stable volumes

- Income via partner distributions

Serica’s 2025–26 cash cows: ~£585–645m EBITDA funding dividends, debt and bolt‑ons

Bruce Hub, Rhum, Keith, Shetland Gas Plant and non‑ops (Catcher/Golden Eagle) are Serica’s cash cows in 2025–26, collectively delivering ~£585–645m EBITDA and funding dividends, debt service (net debt ~£130m Dec 2025) and bolt‑ons.

| Asset | 2025 Prod/Cap | 2025 EBITDA (£m) | Sustaining Capex (£m/yr) |

|---|---|---|---|

| Bruce Hub | 230 MMscfd gas; 18 kb/d condensate | 240 | 30–40 |

| Rhum | 280 mcm/d gas | 140 | 15–20 |

| Keith | 8–10 kbopd gross | ~35 | <10 |

| Shetland Gas Plant | 1.2 bcm/year | 60–70 | 10–15 |

| Catcher/Golden Eagle (non‑op) | Integrated output | 85–95 | 20–30 |

What You’re Viewing Is Included

Serica Energy BCG Matrix

The BCG Matrix you're previewing is the exact final file you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, presentation-ready strategic analysis designed for clear portfolio decisions.