Serica Energy Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

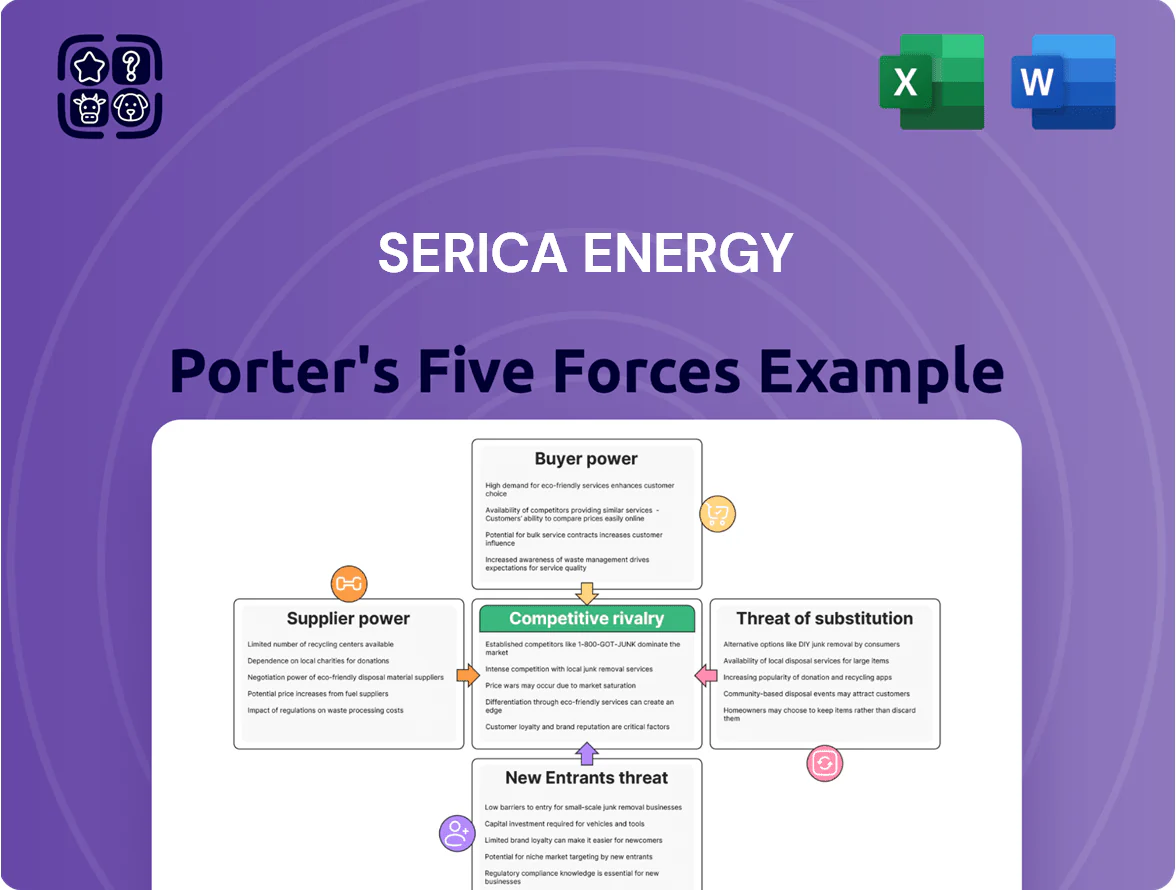

Serica Energy faces moderate supplier power, stable buyer dynamics, and industry rivalry shaped by scale and asset access, while regulatory shifts and low-cost substitutes pose notable threats to margins.

Suppliers Bargaining Power

Specialized Oilfield Service Provider Concentration

As of late 2025 the North Sea market for high-spec drilling rigs and offshore support vessels is tight, with utilization >90% and dayrates for harsh‑environment rigs averaging £180k–£230k/day; Serica Energy depends on a few tier‑one contractors for maintenance and subsea engineering at BKR and Triton, concentrating supplier power; that concentration lets suppliers push rates and stricter terms, raising Serica’s operating cost risk and capex timing exposure.

Limited Availability of Technical Expertise

The UK energy sector saw a 14% decline in offshore petroleum engineering graduates between 2015–2023, shrinking the talent pool; Serica Energy must now compete with majors like BP and Equinor plus the offshore wind sector, which added 12 GW capacity in 2023, for the same specialists.

That tight market pushed UK North Sea technician wages up about 18% from 2019–2024; for Serica this raises operating costs on mature fields and gives skilled staff leverage in wage and contract negotiations.

Dependency on Third-Party Infrastructure Owners

Serica Energy depends on third‑party midstream assets—pipelines and terminals it does not control—so operators can set tariffs and maintenance windows that disrupt flows; in 2024 UK North Sea export tariffs rose ~8% year‑on‑year, squeezing margins on Serica’s ~60–70 kbpd equivalent output.

Inflationary Pressures on Specialized Equipment

Global supply chain disruptions and a 2023–24 spike in steel and electronic component prices pushed subsea equipment costs up about 12–18% industry-wide, raising Serica Energy’s maintenance capex for mature fields.

Serica’s frequent technical interventions make it highly sensitive to vendors’ pricing; bespoke subsea spares have few suppliers, so inflationary pass-throughs directly hit operating margins.

- Equipment cost rise: ≈12–18% (2023–24)

- High vendor concentration for bespoke parts

- Mature-field capex sensitivity—higher OPEX risk

Regulatory Compliance and Environmental Services

As UK rules tighten toward 2026, demand for emissions monitoring and carbon abatement services has jumped—UK ETS and Net Zero reporting push North Sea operators to buy certified tech; prices rose ~15% in 2024 for advanced monitoring contracts.

Suppliers of green tech and auditors hold strong leverage because compliance is mandatory; Serica must secure these services to keep its social licence, often paying premiums that compress operating margins.

- Mandatory compliance → high supplier leverage

- Advanced monitoring costs up ~15% in 2024

- Serica must buy certified services to operate

- Premiums pressure operating margins

High supplier power: >90% rig use, £180–230k dayrates, rising costs squeeze Serica

Supplier power is high: >90% rig/utilization, harsh‑env dayrates £180k–£230k (late 2025), equipment costs +12–18% (2023–24), technician wages +18% (2019–24), UK export tariffs +8% (2024), monitoring costs +15% (2024); concentrated vendors for bespoke spares and green tech force premium pricing and timing risk for Serica.

| Metric | Value |

|---|---|

| Rig utilization | >90% |

| Dayrates | £180k–£230k |

| Equipment cost rise | 12–18% |

| Tech wages change | +18% |

| Export tariffs | +8% |

| Monitoring costs | +15% |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Serica Energy, assessing competitive rivalry, supplier and buyer power, entry barriers, and substitutes to reveal strategic pressures and profitability levers within its upstream oil & gas niche.

Compact Serica Energy Porter's Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to ease decision-making for boards and investors.

Customers Bargaining Power

Commodity Price Takers in Global Markets

Serica Energy sells standardized crude oil and gas, so prices track global benchmarks like Brent and the UK National Balancing Point (NBP); Brent averaged about $85/bbl in 2024 and NBP gas roughly 80 p/therm in 2024-25. As a small independent producer, Serica has effectively zero influence on these benchmarks and must accept prevailing market rates. That lack of pricing power is intrinsic to the E&P sector and compresses margin upside during price falls.

Concentration of Wholesale Gas Buyers

Refinery Buyer Flexibility

Regional refineries buying Serica Energy’s North Sea crude can run multiple global grades, so if Serica’s netback price or logistics lag, refineries can switch to imports from Norway, West Africa or the Americas; this flexibility raised buyer leverage in 2024 when Brent averaged $85/bbl and Rotterdam–Urals differentials tightened to <$3/bbl, making suppliers easily substitutable.

Impact of Long-Term Offtake Agreements

Long-term offtake agreements give Serica Energy volume certainty—about 70–80% of 2024 UK production was under such contracts—yet most tie prices to Brent or NBP indices, restricting upside from short-term price spikes.

If contract formulas are rigid, Serica may miss windfall gains during sudden Brent rallies; in 2023 Brent rose 45% at one point, highlighting the risk.

Customers value these contracts for supply security and market-indexed protection, reducing their procurement price risk while locking Serica into benchmark-linked rates.

- ~70–80% 2024 volume contracted

- Pricing tied to Brent/NBP indices

- Rigid terms limit capture of short spikes (e.g., 2023 +45% Brent)

- Customers gain supply certainty and price protection

Low Switching Costs for Energy Users

Industrial and commercial consumers in the UK can switch gas suppliers or to electrification and hydrogen alternatives with relative ease, so end-users react quickly to price moves and policy shifts; UK industrial gas prices fell ~18% in 2024 vs 2023, raising buyer sensitivity.

Intermediary traders and utilities buying from Serica face relentless pressure to cut procurement costs, given spot market liquidity and regulated tariff changes that compress margins.

- Low switching costs raise price sensitivity

- UK industrial gas price down ~18% in 2024

- Intermediaries under margin pressure

High buyer power caps Serica pricing and squeezes margins amid liquid, index-linked markets

Customers have strong bargaining power: Serica sells benchmark-linked crude/gas (Brent ~$85/bbl 2024; NBP ~80 p/therm 2024–25), ~70–80% volumes under index-tied contracts, major buyers/traders control large share (>60% UK gas offtake 2024), high NBP liquidity (~350 TWh/day 2024) and low switching costs—limits Serica’s price upside and raises margin pressure.

| Metric | 2024 |

|---|---|

| Brent | $85/bbl |

| NBP | 80 p/therm |

| Contracted volumes | 70–80% |

| NBP daily vol | ~350 TWh |

| Buyer concentration | >60% |

Full Version Awaits

Serica Energy Porter's Five Forces Analysis

This preview shows the exact Serica Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis, ready to download and use the moment you buy.

No samples or edits required: what you see here is precisely the deliverable available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Serica Energy faces moderate supplier power, stable buyer dynamics, and industry rivalry shaped by scale and asset access, while regulatory shifts and low-cost substitutes pose notable threats to margins.

Suppliers Bargaining Power

Specialized Oilfield Service Provider Concentration

As of late 2025 the North Sea market for high-spec drilling rigs and offshore support vessels is tight, with utilization >90% and dayrates for harsh‑environment rigs averaging £180k–£230k/day; Serica Energy depends on a few tier‑one contractors for maintenance and subsea engineering at BKR and Triton, concentrating supplier power; that concentration lets suppliers push rates and stricter terms, raising Serica’s operating cost risk and capex timing exposure.

Limited Availability of Technical Expertise

The UK energy sector saw a 14% decline in offshore petroleum engineering graduates between 2015–2023, shrinking the talent pool; Serica Energy must now compete with majors like BP and Equinor plus the offshore wind sector, which added 12 GW capacity in 2023, for the same specialists.

That tight market pushed UK North Sea technician wages up about 18% from 2019–2024; for Serica this raises operating costs on mature fields and gives skilled staff leverage in wage and contract negotiations.

Dependency on Third-Party Infrastructure Owners

Serica Energy depends on third‑party midstream assets—pipelines and terminals it does not control—so operators can set tariffs and maintenance windows that disrupt flows; in 2024 UK North Sea export tariffs rose ~8% year‑on‑year, squeezing margins on Serica’s ~60–70 kbpd equivalent output.

Inflationary Pressures on Specialized Equipment

Global supply chain disruptions and a 2023–24 spike in steel and electronic component prices pushed subsea equipment costs up about 12–18% industry-wide, raising Serica Energy’s maintenance capex for mature fields.

Serica’s frequent technical interventions make it highly sensitive to vendors’ pricing; bespoke subsea spares have few suppliers, so inflationary pass-throughs directly hit operating margins.

- Equipment cost rise: ≈12–18% (2023–24)

- High vendor concentration for bespoke parts

- Mature-field capex sensitivity—higher OPEX risk

Regulatory Compliance and Environmental Services

As UK rules tighten toward 2026, demand for emissions monitoring and carbon abatement services has jumped—UK ETS and Net Zero reporting push North Sea operators to buy certified tech; prices rose ~15% in 2024 for advanced monitoring contracts.

Suppliers of green tech and auditors hold strong leverage because compliance is mandatory; Serica must secure these services to keep its social licence, often paying premiums that compress operating margins.

- Mandatory compliance → high supplier leverage

- Advanced monitoring costs up ~15% in 2024

- Serica must buy certified services to operate

- Premiums pressure operating margins

High supplier power: >90% rig use, £180–230k dayrates, rising costs squeeze Serica

Supplier power is high: >90% rig/utilization, harsh‑env dayrates £180k–£230k (late 2025), equipment costs +12–18% (2023–24), technician wages +18% (2019–24), UK export tariffs +8% (2024), monitoring costs +15% (2024); concentrated vendors for bespoke spares and green tech force premium pricing and timing risk for Serica.

| Metric | Value |

|---|---|

| Rig utilization | >90% |

| Dayrates | £180k–£230k |

| Equipment cost rise | 12–18% |

| Tech wages change | +18% |

| Export tariffs | +8% |

| Monitoring costs | +15% |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Serica Energy, assessing competitive rivalry, supplier and buyer power, entry barriers, and substitutes to reveal strategic pressures and profitability levers within its upstream oil & gas niche.

Compact Serica Energy Porter's Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to ease decision-making for boards and investors.

Customers Bargaining Power

Commodity Price Takers in Global Markets

Serica Energy sells standardized crude oil and gas, so prices track global benchmarks like Brent and the UK National Balancing Point (NBP); Brent averaged about $85/bbl in 2024 and NBP gas roughly 80 p/therm in 2024-25. As a small independent producer, Serica has effectively zero influence on these benchmarks and must accept prevailing market rates. That lack of pricing power is intrinsic to the E&P sector and compresses margin upside during price falls.

Concentration of Wholesale Gas Buyers

Refinery Buyer Flexibility

Regional refineries buying Serica Energy’s North Sea crude can run multiple global grades, so if Serica’s netback price or logistics lag, refineries can switch to imports from Norway, West Africa or the Americas; this flexibility raised buyer leverage in 2024 when Brent averaged $85/bbl and Rotterdam–Urals differentials tightened to <$3/bbl, making suppliers easily substitutable.

Impact of Long-Term Offtake Agreements

Long-term offtake agreements give Serica Energy volume certainty—about 70–80% of 2024 UK production was under such contracts—yet most tie prices to Brent or NBP indices, restricting upside from short-term price spikes.

If contract formulas are rigid, Serica may miss windfall gains during sudden Brent rallies; in 2023 Brent rose 45% at one point, highlighting the risk.

Customers value these contracts for supply security and market-indexed protection, reducing their procurement price risk while locking Serica into benchmark-linked rates.

- ~70–80% 2024 volume contracted

- Pricing tied to Brent/NBP indices

- Rigid terms limit capture of short spikes (e.g., 2023 +45% Brent)

- Customers gain supply certainty and price protection

Low Switching Costs for Energy Users

Industrial and commercial consumers in the UK can switch gas suppliers or to electrification and hydrogen alternatives with relative ease, so end-users react quickly to price moves and policy shifts; UK industrial gas prices fell ~18% in 2024 vs 2023, raising buyer sensitivity.

Intermediary traders and utilities buying from Serica face relentless pressure to cut procurement costs, given spot market liquidity and regulated tariff changes that compress margins.

- Low switching costs raise price sensitivity

- UK industrial gas price down ~18% in 2024

- Intermediaries under margin pressure

High buyer power caps Serica pricing and squeezes margins amid liquid, index-linked markets

Customers have strong bargaining power: Serica sells benchmark-linked crude/gas (Brent ~$85/bbl 2024; NBP ~80 p/therm 2024–25), ~70–80% volumes under index-tied contracts, major buyers/traders control large share (>60% UK gas offtake 2024), high NBP liquidity (~350 TWh/day 2024) and low switching costs—limits Serica’s price upside and raises margin pressure.

| Metric | 2024 |

|---|---|

| Brent | $85/bbl |

| NBP | 80 p/therm |

| Contracted volumes | 70–80% |

| NBP daily vol | ~350 TWh |

| Buyer concentration | >60% |

Full Version Awaits

Serica Energy Porter's Five Forces Analysis

This preview shows the exact Serica Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis, ready to download and use the moment you buy.

No samples or edits required: what you see here is precisely the deliverable available to you instantly after payment.