Servier PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, regulatory pressures, and rapid biotech innovation are shaping Servier’s strategic horizon—our concise PESTLE highlights risks and opportunities you can act on today. Buy the full PESTLE to access granular analysis, scenario-ready insights, and downloadable charts that save you research time and strengthen investment or strategic decisions.

Political factors

Drug Pricing Legislation

Governments in the US and EU tightened price controls by late 2025, with US CMS targeting Medicare drug negotiation savings of an estimated $100–120 billion over 10 years and EU member states pursuing reference pricing and mandatory value assessments that cut list prices 10–25% in recent approvals.

Servier must balance margin pressure—estimated potential revenue impact of 8–15% for specialty portfolios—with ensuring patient access to innovative therapies through tiered pricing and patient-assistance programs.

Strategic negotiation with payers and clear clinical-value dossiers are required: health technology assessments increasingly demand real-world evidence and cost-effectiveness thresholds often below €50,000 per QALY for non-oncology drugs.

EU Health Policy Integration

The EU’s drive to harmonize healthcare rules affects Servier’s product launches and supply-chain compliance; the EU Pharmaceutical Strategy and 2024 MDR updates raise regulatory alignment costs by an estimated 3–5% of revenues for mid-sized pharma firms.

Growing joint procurement (e.g., EU4Health pooled tenders covering ~€10bn 2024–27) offers Servier scale but risks centralized price pressure that could compress margins by 1–3 percentage points.

Servier must adapt regional manufacturing and registration strategies to align with evolving frameworks to protect its European market share (~30% of group sales in 2024).

Global Trade Relations

Geopolitical tensions and shifting trade alliances continue to disrupt pharmaceutical supply chains and market access for international firms; in 2024 global trade tensions saw a 12% increase in export controls across key APIs-producing countries, affecting timelines and costs for companies like Servier.

Servier faces risks from tariffs and export restrictions on essential chemical precursors and finished products, with tariff spikes in 2023–24 raising input costs by an estimated 4–7% in affected routes.

Maintaining a diversified manufacturing footprint—Servier’s 2025 target to source 40% of key intermediates from at least three regions—remains essential to mitigate political instability and ensure continuity of supply.

Government Research Funding

Public-private partnerships and government grants drive pharma innovation; Servier benefited from EU Horizon 2020/2021-like programs and France’s Crédit Impôt Recherche, which reduced R&D costs by up to 30%, supporting its oncology pipeline.

Servier depends on stable political support and targeted funding for oncology—France committed €7.5bn to health research 2024–2027—so shifts in leadership can reallocate grants, forcing agile R&D prioritization.

- Public-private grants and tax credits lower Servier R&D expenses

- France’s €7.5bn health-research pledge (2024–2027) supports oncology

- Policy shifts risk funding reallocation, requiring flexible R&D strategy

Healthcare Access Initiatives

- WHO: 2bn without full UHC (2024)

- Servier 2024 revenue €3.6bn

- Pressure for price-volume/state programs vs R&D funding

Servier faces margin squeeze from US/EU pricing & supply controls despite French support

Political pressures—US Medicare negotiations (~$100–120bn savings/10y), EU price cuts (10–25%) and HTA thresholds (~€50k/QALY)—threaten Servier margins (potential 8–15% hit) while joint procurement (~€10bn 2024–27) and trade controls (+12% export controls 2024) raise supply risks; France’s €7.5bn health pledge and tax credits offset R&D costs (~30%), supporting a €3.6bn 2024 revenue base.

| Metric | Value |

|---|---|

| 2024 revenue | €3.6bn |

| US Medicare savings target | $100–120bn/10y |

| EU joint tenders | €10bn (2024–27) |

| HTA threshold | ~€50k/QALY |

What is included in the product

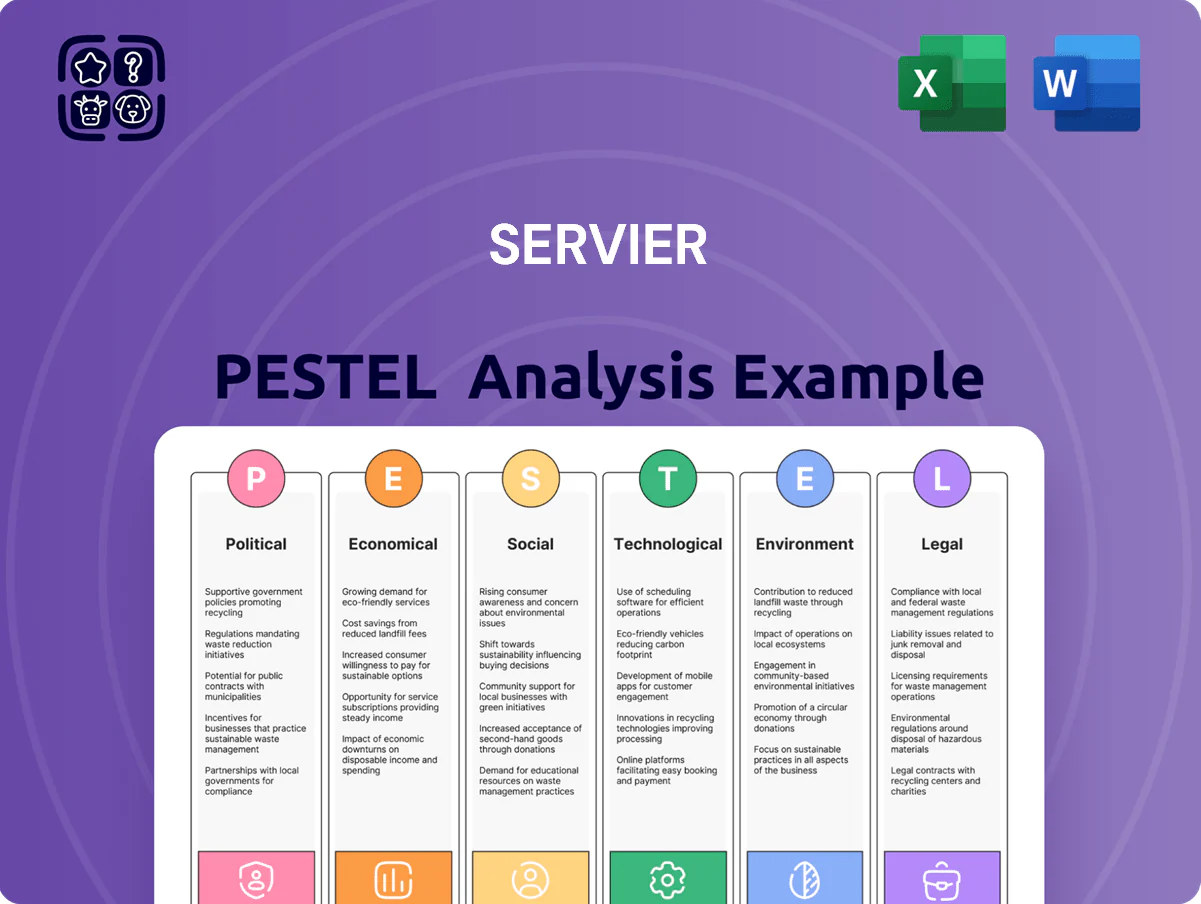

Explores how external macro-environmental factors uniquely affect Servier across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven subpoints and region-specific examples to identify threats and opportunities.

Condenses Servier's PESTLE into a concise, shareable brief—visually segmented by category for quick interpretation and easily dropped into presentations or strategy packs to support risk discussions and cross-team alignment.

Economic factors

Global Inflation Pressures

Persistent global inflation through 2025 has driven pharmaceutical input costs up: raw material prices rose ~12% YoY and energy costs surged ~20% in 2024, increasing Servier’s manufacturing expense base and skilled labor premiums; the group must absorb or manage these rises without materially raising drug prices to payers or patients. Efficient resource allocation and supply‑chain optimization are essential to protect margins amid higher operating costs and potential FX headwinds.

Currency Exchange Volatility

As a Euro-reporting global group, Servier’s 2024 revenue exposed to FX showed a c.8–12% swing vs USD and select emerging currencies, meaning a 10% USD/EUR move could alter reported revenue by roughly €200–300m; overseas clinical-trial costs in 2024 rose ~6% in local-currency terms due to depreciation in several EM currencies. Servier uses dynamic hedging and currency forwards/options covering a significant portion of forecasted cash flows to stabilize P&L.

Emerging Market Expansion

Economic growth in Southeast Asia (GDP growth ~4–5% in 2024) and Latin America (projected ~2.5–3% in 2024) expands market opportunities for Servier to increase market share as middle-class populations—estimated to grow by ~50 million in SEA and ~30 million in LATAM by 2025—gain better healthcare access and demand for specialty drugs; however, market entry requires substantial upfront investment and localized pricing strategies given variable per capita healthcare spending (e.g., SEA ~$500–$1,200; LATAM ~$800–$2,000 annually).

RD Capital Allocation

High global interest rates in 2024–25 raised Servier’s weighted average cost of capital, pressuring financing for long-term R&D where ~25–30% of revenue is typically reinvested into innovation; Servier reported R&D spend of €1.2bn in 2024.

To preserve funding for late-stage trials costing €100–300m each, Servier balances increased use of internal cash flow with selective debt—net debt/EBITDA targets tightened to ~2.0x in 2025—requiring strategic capital allocation across pipeline stages.

- R&D spend 2024: €1.2bn

- R&D reinvestment: ~25–30% revenue

- Late-stage trial cost: €100–300m

- Net debt/EBITDA target ~2.0x (2025)

Healthcare Budget Constraints

- OECD avg health spend 9.6% GDP (2022)

- HTA focus on ICER/QALY and long-term savings

- Need RWE and budget-impact models to justify reimbursement

Pharma margins squeezed: input costs +12–20%, €1.2bn R&D, €200–300m FX hit

Inflation and energy rose pharma input costs ~12–20% in 2024; FX moves (10% USD/EUR) affect revenue by ~€200–300m; SEA/LATAM GDP growth ~4–5%/2.5–3% expands markets; R&D €1.2bn (25–30% rev) with late-stage trials €100–300m; net debt/EBITDA target ~2.0x (2025); OECD health spend 9.6% GDP (2022); HTA focus on ICER/QALY requires RWE.

| Metric | 2024/2025 |

|---|---|

| R&D spend | €1.2bn |

| Input cost rise | ~12–20% |

| FX sensitivity | €200–300m per 10% USD/EUR |

| Net debt/EBITDA | ~2.0x target |

What You See Is What You Get

Servier PESTLE Analysis

The preview shown here is the exact Servier PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are identical to the downloadable file you’ll get instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, regulatory pressures, and rapid biotech innovation are shaping Servier’s strategic horizon—our concise PESTLE highlights risks and opportunities you can act on today. Buy the full PESTLE to access granular analysis, scenario-ready insights, and downloadable charts that save you research time and strengthen investment or strategic decisions.

Political factors

Drug Pricing Legislation

Governments in the US and EU tightened price controls by late 2025, with US CMS targeting Medicare drug negotiation savings of an estimated $100–120 billion over 10 years and EU member states pursuing reference pricing and mandatory value assessments that cut list prices 10–25% in recent approvals.

Servier must balance margin pressure—estimated potential revenue impact of 8–15% for specialty portfolios—with ensuring patient access to innovative therapies through tiered pricing and patient-assistance programs.

Strategic negotiation with payers and clear clinical-value dossiers are required: health technology assessments increasingly demand real-world evidence and cost-effectiveness thresholds often below €50,000 per QALY for non-oncology drugs.

EU Health Policy Integration

The EU’s drive to harmonize healthcare rules affects Servier’s product launches and supply-chain compliance; the EU Pharmaceutical Strategy and 2024 MDR updates raise regulatory alignment costs by an estimated 3–5% of revenues for mid-sized pharma firms.

Growing joint procurement (e.g., EU4Health pooled tenders covering ~€10bn 2024–27) offers Servier scale but risks centralized price pressure that could compress margins by 1–3 percentage points.

Servier must adapt regional manufacturing and registration strategies to align with evolving frameworks to protect its European market share (~30% of group sales in 2024).

Global Trade Relations

Geopolitical tensions and shifting trade alliances continue to disrupt pharmaceutical supply chains and market access for international firms; in 2024 global trade tensions saw a 12% increase in export controls across key APIs-producing countries, affecting timelines and costs for companies like Servier.

Servier faces risks from tariffs and export restrictions on essential chemical precursors and finished products, with tariff spikes in 2023–24 raising input costs by an estimated 4–7% in affected routes.

Maintaining a diversified manufacturing footprint—Servier’s 2025 target to source 40% of key intermediates from at least three regions—remains essential to mitigate political instability and ensure continuity of supply.

Government Research Funding

Public-private partnerships and government grants drive pharma innovation; Servier benefited from EU Horizon 2020/2021-like programs and France’s Crédit Impôt Recherche, which reduced R&D costs by up to 30%, supporting its oncology pipeline.

Servier depends on stable political support and targeted funding for oncology—France committed €7.5bn to health research 2024–2027—so shifts in leadership can reallocate grants, forcing agile R&D prioritization.

- Public-private grants and tax credits lower Servier R&D expenses

- France’s €7.5bn health-research pledge (2024–2027) supports oncology

- Policy shifts risk funding reallocation, requiring flexible R&D strategy

Healthcare Access Initiatives

- WHO: 2bn without full UHC (2024)

- Servier 2024 revenue €3.6bn

- Pressure for price-volume/state programs vs R&D funding

Servier faces margin squeeze from US/EU pricing & supply controls despite French support

Political pressures—US Medicare negotiations (~$100–120bn savings/10y), EU price cuts (10–25%) and HTA thresholds (~€50k/QALY)—threaten Servier margins (potential 8–15% hit) while joint procurement (~€10bn 2024–27) and trade controls (+12% export controls 2024) raise supply risks; France’s €7.5bn health pledge and tax credits offset R&D costs (~30%), supporting a €3.6bn 2024 revenue base.

| Metric | Value |

|---|---|

| 2024 revenue | €3.6bn |

| US Medicare savings target | $100–120bn/10y |

| EU joint tenders | €10bn (2024–27) |

| HTA threshold | ~€50k/QALY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Servier across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven subpoints and region-specific examples to identify threats and opportunities.

Condenses Servier's PESTLE into a concise, shareable brief—visually segmented by category for quick interpretation and easily dropped into presentations or strategy packs to support risk discussions and cross-team alignment.

Economic factors

Global Inflation Pressures

Persistent global inflation through 2025 has driven pharmaceutical input costs up: raw material prices rose ~12% YoY and energy costs surged ~20% in 2024, increasing Servier’s manufacturing expense base and skilled labor premiums; the group must absorb or manage these rises without materially raising drug prices to payers or patients. Efficient resource allocation and supply‑chain optimization are essential to protect margins amid higher operating costs and potential FX headwinds.

Currency Exchange Volatility

As a Euro-reporting global group, Servier’s 2024 revenue exposed to FX showed a c.8–12% swing vs USD and select emerging currencies, meaning a 10% USD/EUR move could alter reported revenue by roughly €200–300m; overseas clinical-trial costs in 2024 rose ~6% in local-currency terms due to depreciation in several EM currencies. Servier uses dynamic hedging and currency forwards/options covering a significant portion of forecasted cash flows to stabilize P&L.

Emerging Market Expansion

Economic growth in Southeast Asia (GDP growth ~4–5% in 2024) and Latin America (projected ~2.5–3% in 2024) expands market opportunities for Servier to increase market share as middle-class populations—estimated to grow by ~50 million in SEA and ~30 million in LATAM by 2025—gain better healthcare access and demand for specialty drugs; however, market entry requires substantial upfront investment and localized pricing strategies given variable per capita healthcare spending (e.g., SEA ~$500–$1,200; LATAM ~$800–$2,000 annually).

RD Capital Allocation

High global interest rates in 2024–25 raised Servier’s weighted average cost of capital, pressuring financing for long-term R&D where ~25–30% of revenue is typically reinvested into innovation; Servier reported R&D spend of €1.2bn in 2024.

To preserve funding for late-stage trials costing €100–300m each, Servier balances increased use of internal cash flow with selective debt—net debt/EBITDA targets tightened to ~2.0x in 2025—requiring strategic capital allocation across pipeline stages.

- R&D spend 2024: €1.2bn

- R&D reinvestment: ~25–30% revenue

- Late-stage trial cost: €100–300m

- Net debt/EBITDA target ~2.0x (2025)

Healthcare Budget Constraints

- OECD avg health spend 9.6% GDP (2022)

- HTA focus on ICER/QALY and long-term savings

- Need RWE and budget-impact models to justify reimbursement

Pharma margins squeezed: input costs +12–20%, €1.2bn R&D, €200–300m FX hit

Inflation and energy rose pharma input costs ~12–20% in 2024; FX moves (10% USD/EUR) affect revenue by ~€200–300m; SEA/LATAM GDP growth ~4–5%/2.5–3% expands markets; R&D €1.2bn (25–30% rev) with late-stage trials €100–300m; net debt/EBITDA target ~2.0x (2025); OECD health spend 9.6% GDP (2022); HTA focus on ICER/QALY requires RWE.

| Metric | 2024/2025 |

|---|---|

| R&D spend | €1.2bn |

| Input cost rise | ~12–20% |

| FX sensitivity | €200–300m per 10% USD/EUR |

| Net debt/EBITDA | ~2.0x target |

What You See Is What You Get

Servier PESTLE Analysis

The preview shown here is the exact Servier PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are identical to the downloadable file you’ll get instantly after payment.