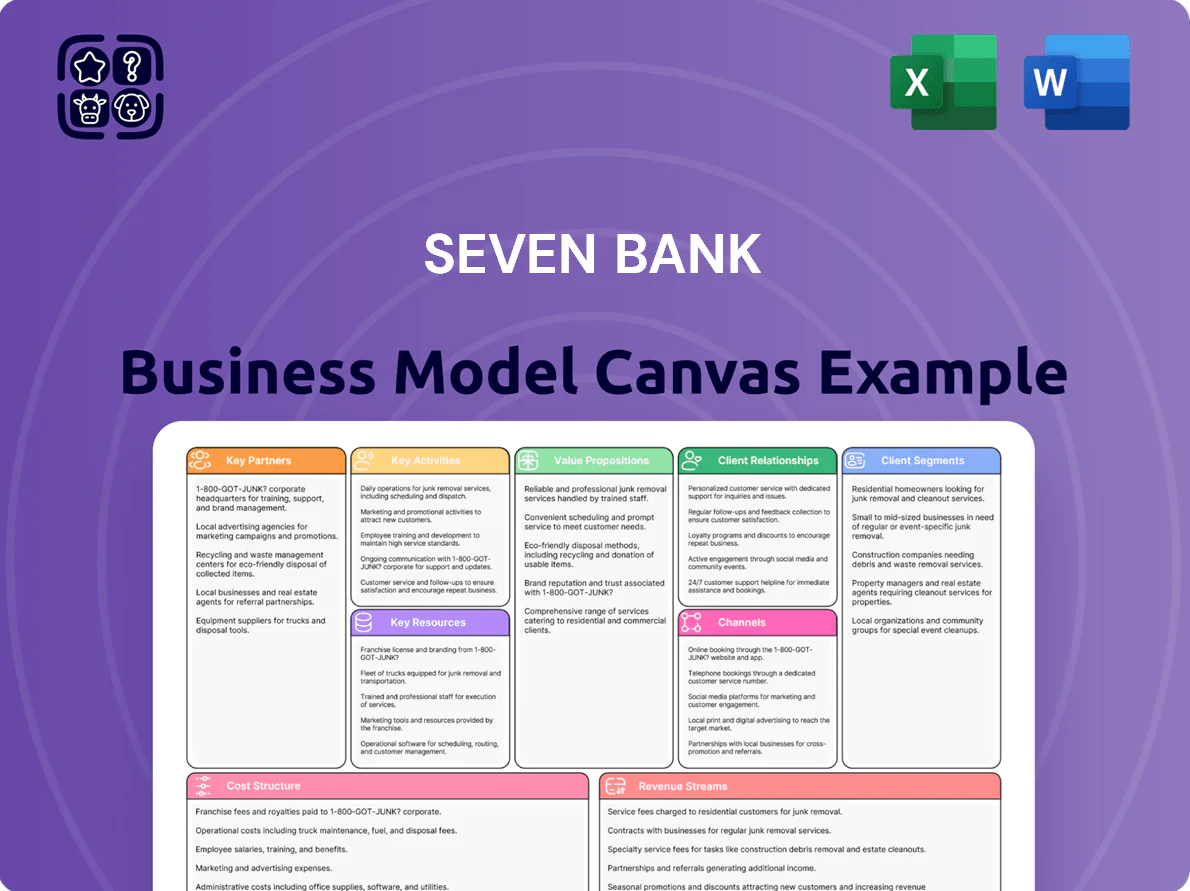

Seven Bank Business Model Canvas

Seven Bank Business Model Canvas: Strategy, Customers & Revenue at a Glance

Unlock the full strategic blueprint behind Seven Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, and revenue streams to show how the bank scales and sustains growth.

Partnerships

Seven and i Holdings and Retail Affiliates

The bank partners with Seven & i Holdings to host 20,000+ ATMs inside 7-Eleven stores nationwide, giving Seven Bank an unmatched high-density footprint versus traditional banks.

By end-2025 the link extends into 7-ID account integration and loyalty ties, boosting retail-driven deposits and transaction volumes—card-linked payments up ~18% YoY in 2024.

Domestic Financial Institution Partners

Seven Bank partners with over 600 Japanese banks, credit unions, and securities firms, letting their customers withdraw cash from Seven Bank’s ~20,000 ATMs nationwide; in 2024 interchange fees from these partners made up roughly 48% of Seven Bank’s ¥92.3 billion operating revenue, cementing its role as an essential payment utility in Japan’s financial ecosystem.

Western Union and Global Remittance Providers

Strategic alliances with Western Union and other global remittance providers let Seven Bank offer real-time international transfers from ATMs and mobile apps, handling over ¥350 billion (about $2.3 billion) in outbound remittances in FY2024 to serve 2.9 million foreign residents in Japan.

Technology and Hardware Vendors

The bank maintains multi-year contracts with tech vendors like NEC to supply and service high-security ATMs; by 2025 biometric (fingerprint/vein) and facial-recognition modules now cover over 70% of Seven Bank’s 15,000 ATM network, cutting card-fraud losses by ~28% in 2024.

- 15,000 ATMs upgraded by 2025

- 70% use biometrics/facial ID

- 28% reduction in card-fraud losses (2024)

- Annual vendor audits and patch cycles quarterly

International Card Networks

Partnerships with Visa, Mastercard, and UnionPay let Seven Bank process withdrawals on foreign cards, capturing ATM fees and interchange revenue—about ¥4.2 billion in non-interest income from international transactions in FY2024 (ending Mar 2025), concentrated in Q2–Q3 tourist season.

This connectivity makes Seven Bank a primary financial touchpoint for inbound tourists, handling roughly 45% of airport and convenience-store ATM withdrawals by non-residents in 2024.

- Enables foreign-card cash withdrawals

- Generated ¥4.2B in FY2024 from international transactions

- Handles ~45% of non-resident ATM withdrawals (2024)

Seven Bank: 20K+ ATMs, ¥44.3B interchange, ¥350B remittances & 28% fraud cut

Seven Bank anchors 20,000+ ATMs via Seven & i, earning ~¥44.3B (48% of ¥92.3B) in interchange in FY2024 and ¥4.2B from international card fees; remittances handled ¥350B and biometric upgrades (70% of 15,000 ATMs) cut fraud 28% in 2024.

| Metric | Value |

|---|---|

| ATMs (total) | 20,000+ |

| Interchange revenue | ¥44.3B (48% of ¥92.3B) |

| Intl transaction income | ¥4.2B |

| Remittances (FY2024) | ¥350B |

| Biometric coverage | 70% of 15,000 ATMs |

| Fraud reduction (2024) | 28% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Seven Bank’s strategy, covering customer segments, channels, value propositions, revenue streams, key activities, partners, resources, cost structure and metrics with competitive analysis and SWOT-linked insights for presentations, investor discussions, and strategic decision-making.

Condenses Seven Bank’s retail and digital banking strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

ATM Network Operation and Maintenance

The bank manages uptime and technical health for over 27,000 ATMs across Japan, scheduling hardware repairs, OS and application patches, and daily physical cleaning to sustain near 99.5% availability; in 2024 the ATM fleet processed roughly 1.8 billion transactions, generating ~¥120 billion in fees and interchange. Efficient operation of this fleet is Seven Bank’s top operational priority, driving ~40% of branchless customer touchpoints and directly affecting transaction revenue and customer retention.

Transaction Processing and Settlement

Seven Bank processes millions of daily transactions as a high-volume clearinghouse—about 3.2 million transactions per day in 2024—requiring real-time recording and settlement for deposits, withdrawals, and transfers.

To meet sub-second settlement SLAs and handle peak throughput (over 40,000 TPS), Seven Bank runs a low-latency backend with horizontal scaling, in-memory ledgers, and redundancy to keep error rates below 0.001%.

Digital Banking Product Development

As of late 2025 Seven Bank moved 35% of IT spend to mobile-first initiatives, upgrading the My Seven Bank app with integrated budgeting (beta 120k users) and contactless ATM access (pilot 250 ATMs), aiming to shift customer engagement from branch visits (down 18% YoY) to a full digital financial partner.

Compliance and Anti-Money Laundering Monitoring

Maintaining strict adherence to regulatory standards is ongoing to prevent financial crime and keep institutional stability; Seven Bank runs AI-driven monitoring that flagged 1.2% of remittance volume as suspicious in FY2024, covering ~¥3.6 trillion flows.

Continuous audits and monthly reports to the Financial Services Agency are mandatory for license maintenance, with AML remediation reducing SAR (suspicious activity report) false positives by 28% in 2024.

- AI monitoring: 1.2% suspicious remittances (FY2024)

- Covered flows: ~¥3.6 trillion (2024)

- SAR false positives cut 28% (2024)

- Monthly audits/reports to FSA mandatory

Customer Support and Multilingual Services

Seven Bank runs support centers handling 24/7 technical and transactional queries, resolving 85% of cases on first contact and averaging 3.2-minute wait times in 2024.

They offer multilingual support in over 10 languages (including English, Chinese, Korean, Tagalog), lowering entry barriers for ~18% of foreign resident customers and boosting cross-border ATM/inflow usage by 12% y/y.

- 24/7 centers; 85% first-contact resolution

- Avg wait 3.2 minutes (2024)

- Support in 10+ languages

- Serves ~18% foreign customers

- Cross-border usage +12% y/y

27,000 ATMs | 1.8bn tx/yr | ¥120bn fees — 40k TPS, AI AML cuts false positives 28%

Operate 27,000 ATMs (99.5% uptime) processing ~1.8bn tx/yr (¥120bn fees), clear ~3.2m tx/day, run low-latency backend (40k TPS, <0.001% errors), shift 35% IT spend to mobile (120k beta users), AI AML flagged 1.2% (~¥3.6tn) with SAR false positives down 28%, 24/7 support (85% FCR, 3.2 min wait), multilingual for ~18% foreign customers.

| Metric | 2024/late‑2025 |

|---|---|

| ATMs | 27,000 |

| Transactions/yr | 1.8bn |

| Fees | ¥120bn |

| Tx/day | 3.2m |

| Peak TPS | 40,000 |

| AML flagged | 1.2% (~¥3.6tn) |

| FCR | 85% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Seven Bank Business Model Canvas, not a mockup or sample—it's a direct snapshot of the actual file you will receive after purchase.

Upon completing your order, you’ll get full access to this same professional, ready-to-use document in editable Word and Excel formats, structured exactly as shown here.

No surprises or fillers: what you see in the preview is the exact deliverable, instantly downloadable and ready for editing, presenting, or sharing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Seven Bank Business Model Canvas: Strategy, Customers & Revenue at a Glance

Unlock the full strategic blueprint behind Seven Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, and revenue streams to show how the bank scales and sustains growth.

Partnerships

Seven and i Holdings and Retail Affiliates

The bank partners with Seven & i Holdings to host 20,000+ ATMs inside 7-Eleven stores nationwide, giving Seven Bank an unmatched high-density footprint versus traditional banks.

By end-2025 the link extends into 7-ID account integration and loyalty ties, boosting retail-driven deposits and transaction volumes—card-linked payments up ~18% YoY in 2024.

Domestic Financial Institution Partners

Seven Bank partners with over 600 Japanese banks, credit unions, and securities firms, letting their customers withdraw cash from Seven Bank’s ~20,000 ATMs nationwide; in 2024 interchange fees from these partners made up roughly 48% of Seven Bank’s ¥92.3 billion operating revenue, cementing its role as an essential payment utility in Japan’s financial ecosystem.

Western Union and Global Remittance Providers

Strategic alliances with Western Union and other global remittance providers let Seven Bank offer real-time international transfers from ATMs and mobile apps, handling over ¥350 billion (about $2.3 billion) in outbound remittances in FY2024 to serve 2.9 million foreign residents in Japan.

Technology and Hardware Vendors

The bank maintains multi-year contracts with tech vendors like NEC to supply and service high-security ATMs; by 2025 biometric (fingerprint/vein) and facial-recognition modules now cover over 70% of Seven Bank’s 15,000 ATM network, cutting card-fraud losses by ~28% in 2024.

- 15,000 ATMs upgraded by 2025

- 70% use biometrics/facial ID

- 28% reduction in card-fraud losses (2024)

- Annual vendor audits and patch cycles quarterly

International Card Networks

Partnerships with Visa, Mastercard, and UnionPay let Seven Bank process withdrawals on foreign cards, capturing ATM fees and interchange revenue—about ¥4.2 billion in non-interest income from international transactions in FY2024 (ending Mar 2025), concentrated in Q2–Q3 tourist season.

This connectivity makes Seven Bank a primary financial touchpoint for inbound tourists, handling roughly 45% of airport and convenience-store ATM withdrawals by non-residents in 2024.

- Enables foreign-card cash withdrawals

- Generated ¥4.2B in FY2024 from international transactions

- Handles ~45% of non-resident ATM withdrawals (2024)

Seven Bank: 20K+ ATMs, ¥44.3B interchange, ¥350B remittances & 28% fraud cut

Seven Bank anchors 20,000+ ATMs via Seven & i, earning ~¥44.3B (48% of ¥92.3B) in interchange in FY2024 and ¥4.2B from international card fees; remittances handled ¥350B and biometric upgrades (70% of 15,000 ATMs) cut fraud 28% in 2024.

| Metric | Value |

|---|---|

| ATMs (total) | 20,000+ |

| Interchange revenue | ¥44.3B (48% of ¥92.3B) |

| Intl transaction income | ¥4.2B |

| Remittances (FY2024) | ¥350B |

| Biometric coverage | 70% of 15,000 ATMs |

| Fraud reduction (2024) | 28% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Seven Bank’s strategy, covering customer segments, channels, value propositions, revenue streams, key activities, partners, resources, cost structure and metrics with competitive analysis and SWOT-linked insights for presentations, investor discussions, and strategic decision-making.

Condenses Seven Bank’s retail and digital banking strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

ATM Network Operation and Maintenance

The bank manages uptime and technical health for over 27,000 ATMs across Japan, scheduling hardware repairs, OS and application patches, and daily physical cleaning to sustain near 99.5% availability; in 2024 the ATM fleet processed roughly 1.8 billion transactions, generating ~¥120 billion in fees and interchange. Efficient operation of this fleet is Seven Bank’s top operational priority, driving ~40% of branchless customer touchpoints and directly affecting transaction revenue and customer retention.

Transaction Processing and Settlement

Seven Bank processes millions of daily transactions as a high-volume clearinghouse—about 3.2 million transactions per day in 2024—requiring real-time recording and settlement for deposits, withdrawals, and transfers.

To meet sub-second settlement SLAs and handle peak throughput (over 40,000 TPS), Seven Bank runs a low-latency backend with horizontal scaling, in-memory ledgers, and redundancy to keep error rates below 0.001%.

Digital Banking Product Development

As of late 2025 Seven Bank moved 35% of IT spend to mobile-first initiatives, upgrading the My Seven Bank app with integrated budgeting (beta 120k users) and contactless ATM access (pilot 250 ATMs), aiming to shift customer engagement from branch visits (down 18% YoY) to a full digital financial partner.

Compliance and Anti-Money Laundering Monitoring

Maintaining strict adherence to regulatory standards is ongoing to prevent financial crime and keep institutional stability; Seven Bank runs AI-driven monitoring that flagged 1.2% of remittance volume as suspicious in FY2024, covering ~¥3.6 trillion flows.

Continuous audits and monthly reports to the Financial Services Agency are mandatory for license maintenance, with AML remediation reducing SAR (suspicious activity report) false positives by 28% in 2024.

- AI monitoring: 1.2% suspicious remittances (FY2024)

- Covered flows: ~¥3.6 trillion (2024)

- SAR false positives cut 28% (2024)

- Monthly audits/reports to FSA mandatory

Customer Support and Multilingual Services

Seven Bank runs support centers handling 24/7 technical and transactional queries, resolving 85% of cases on first contact and averaging 3.2-minute wait times in 2024.

They offer multilingual support in over 10 languages (including English, Chinese, Korean, Tagalog), lowering entry barriers for ~18% of foreign resident customers and boosting cross-border ATM/inflow usage by 12% y/y.

- 24/7 centers; 85% first-contact resolution

- Avg wait 3.2 minutes (2024)

- Support in 10+ languages

- Serves ~18% foreign customers

- Cross-border usage +12% y/y

27,000 ATMs | 1.8bn tx/yr | ¥120bn fees — 40k TPS, AI AML cuts false positives 28%

Operate 27,000 ATMs (99.5% uptime) processing ~1.8bn tx/yr (¥120bn fees), clear ~3.2m tx/day, run low-latency backend (40k TPS, <0.001% errors), shift 35% IT spend to mobile (120k beta users), AI AML flagged 1.2% (~¥3.6tn) with SAR false positives down 28%, 24/7 support (85% FCR, 3.2 min wait), multilingual for ~18% foreign customers.

| Metric | 2024/late‑2025 |

|---|---|

| ATMs | 27,000 |

| Transactions/yr | 1.8bn |

| Fees | ¥120bn |

| Tx/day | 3.2m |

| Peak TPS | 40,000 |

| AML flagged | 1.2% (~¥3.6tn) |

| FCR | 85% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Seven Bank Business Model Canvas, not a mockup or sample—it's a direct snapshot of the actual file you will receive after purchase.

Upon completing your order, you’ll get full access to this same professional, ready-to-use document in editable Word and Excel formats, structured exactly as shown here.

No surprises or fillers: what you see in the preview is the exact deliverable, instantly downloadable and ready for editing, presenting, or sharing.