SFC Energy Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

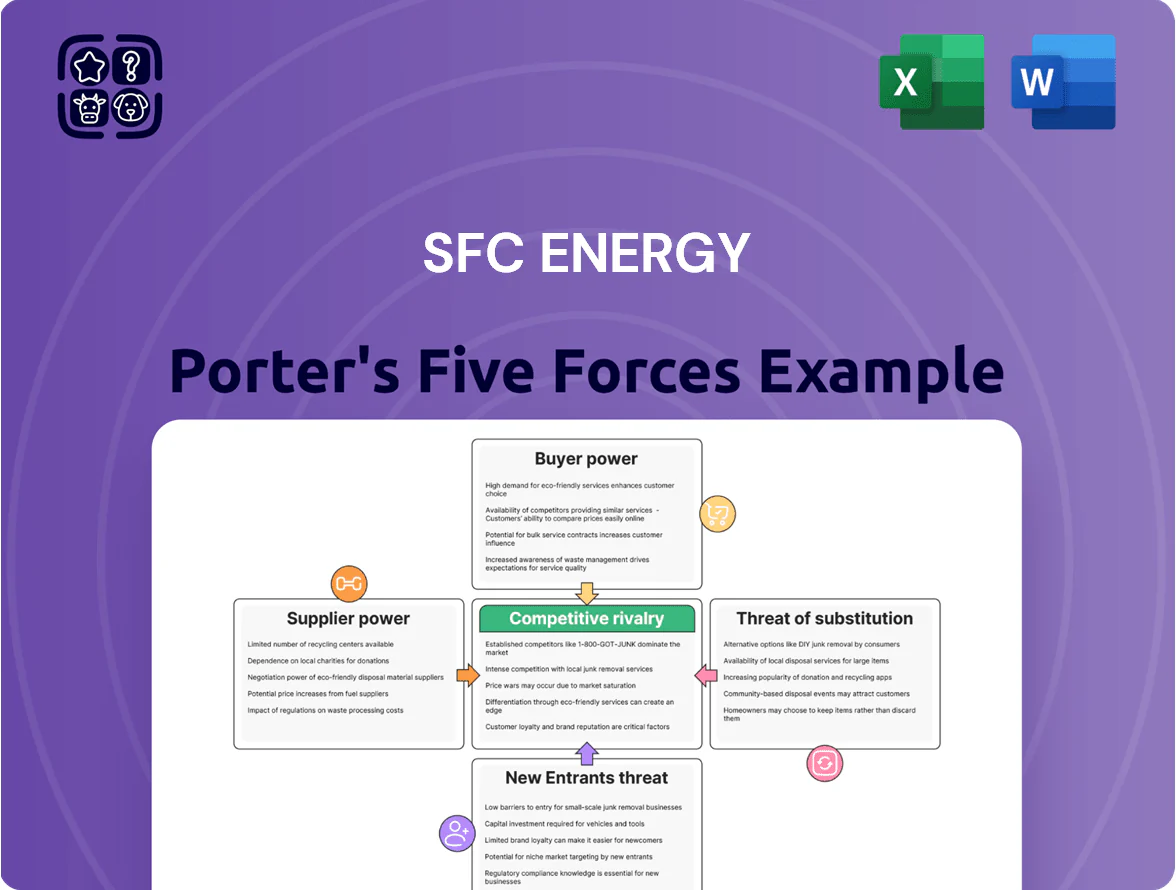

SFC Energy faces medium competitive rivalry with niche tech differentiation, supplier leverage from specialized fuel-cell components, and moderate buyer power driven by defense and industrial clients; threats from substitutes and new entrants are tempered by certifications and IP. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore SFC Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

The production of fuel cells needs precious metals like platinum and specialized proton exchange membranes supplied by a handful of global firms; platinum prices rose 8.3% in 2024 to about $1,050/oz, tightening input cost pressure.

SFC Energy depends on these high-grade inputs for EFOY fuel cell efficiency and lifespan, buying certified membrane stacks with long lead times—industry average lead times hit 20–28 weeks in 2025.

With few high-quality substitutes, suppliers exert strong pricing and delivery leverage; in 2024 supplier concentration saw the top 5 platinum producers control ~60% of mine supply, raising procurement risk for SFC.

Technical Component Uniqueness

SFC Energy uses proprietary electronic modules and custom fuel-cell stacks tied to select engineering partners; swapping suppliers would trigger redesigns and recertification that can cost tens of millions and add 12–24 months per product line, per industry averages. This high technical uniqueness raises supplier switching costs, concentrating bargaining power with incumbent vendors and pressuring SFC’s margins and lead times.

Energy Feedstock Consolidation

High-purity methanol and industrial H2 are critical inputs for SFC Energy fuel cell systems, and global suppliers like Methanex and Air Liquide control ~60–80% of market volume, setting regional prices and distribution rules; in 2024 methanol FOB Rotterdam averaged about $450/ton and industrial H2 pipeline prices ranged $3–7/kg, which directly shapes field operating costs. Supplier consolidation limits SFC’s customers’ total cost of ownership by constraining fuel access and price flexibility.

Supply Chain Resilience and Geopolitics

As of late 2025, higher geopolitical risk has pushed buyers toward localized or allied suppliers for critical energy minerals; suppliers in stable jurisdictions or with vertical integration can charge 10–25% premiums for guaranteed delivery.

SFC Energy must manage regional dependencies—Germany/Europe sourcing and US allies—to keep defense and industrial manufacturing lines running and avoid >5% revenue loss from single-source disruptions.

- Premiums: 10–25% for low-risk suppliers

- Revenue risk: >5% if single-source fails

- Mitigation: dual-sourcing, inventory buffers, vertical partners

Limited Forward Integration Threat

Suppliers hold pricing power for platinum-group catalysts and bipolar plates, but they lack systems-integration know-how to make complete fuel-cell systems; forward-integration risk is low. SFC Energy converts basic inputs into certified off-grid solutions, sustaining gross margins—23.6% in FY2024—that suppliers cannot match. This balance limits supplier leverage while keeping supply-cost exposure.

- Suppliers set raw-material prices

- Rare systems-integration expertise

- Low credible forward-integration threat

- SFC Energy FY2024 gross margin 23.6%

Supplier concentration, long lead times and high switching costs squeeze SFC margins

Suppliers hold strong leverage due to concentrated platinum and membrane supply, long lead times (20–28 weeks in 2025) and high switching costs (12–24 months, tens of millions EUR), pressuring SFC’s margins; FY2024 gross margin was 23.6%.

Mitigations—dual-sourcing, inventory buffers, local allied suppliers—reduce single-source revenue risk (>5%) but cost premiums (10–25%) for low-risk supply persist.

| Metric | Value |

|---|---|

| Platinum price (2024) | $1,050/oz (+8.3%) |

| Lead times (2025) | 20–28 weeks |

| Methanol (2024 FOB Rotterdam) | $450/ton |

| FY2024 gross margin | 23.6% |

What is included in the product

Tailored Porter's Five Forces analysis for SFC Energy, pinpointing competitive rivalry, buyer/supplier power, substitution risks, and barriers to entry with strategic insights on threats, opportunities, and implications for pricing and profitability.

Concise Porter's Five Forces view for SFC Energy—quickly spot competitive threats and opportunities to inform strategic moves.

Customers Bargaining Power

Concentration of Defense and Government Clients

Availability of Alternative Power Technologies

Customers choosing off-grid power can pick fuel cells, advanced lithium-ion batteries, or diesel generators, so buyers pressure SFC Energy by comparing cost and runtime; global lithium-ion pack prices fell ~85% from 2010 to $132/kWh in 2024, raising substitution risk.

High Information Transparency

Professional buyers in industrial and energy sectors access detailed data on fuel cell efficiency (SFC Energy’s EFOY Pro at ~48–52% system efficiency), lifecycle costs (total cost of ownership often 20–35% lower than diesel gensets over 10 years), and competitor pricing, cutting information asymmetry and limiting margin expansion. In 2024 procurement surveys 68% of buyers demanded SLA performance guarantees, so well-informed buyers secure tougher service terms and price concessions.

Low Switching Costs for New Projects

New projects face low switching costs from SFC Energy methanol cartridges to alternatives, so customers frequently choose other providers; SFC must re-prove value for each deployment.

Industrial bidding is highly competitive—tenders often prioritize total cost of ownership; in 2024 average project procurement cycles cut supplier margins by ~8–12% in Europe.

Sensitivity to Total Cost of Ownership

Industrial buyers now prioritize total cost of ownership (TCO), favoring solutions with lower lifecycle costs; for stationary fuel cells SFC Energy (SFC:XETRA) must beat diesel when TCO gap—typically 20–30% higher upfront for fuel cells—is offset by 30–50% lower fuel/maintenance over 10 years per industry studies (2024).

This forces SFC to cut $/kWh through efficiency gains and modular service contracts; a 10% drop in operating cost can shorten payback from ~8 years to ~5–6 years for telecom backup and remote power customers.

Concentrated buyers squeeze margins—TCO tilts fleet buyers toward fuel cells over lithium

Large, concentrated institutional buyers (≈40% revenue 2024) exert strong price and spec pressure; losing one contract (>10% sales) materially hits revenue. Buyers face low switching costs and compare fuel cells vs lithium ($132/kWh 2024) and diesel; TCO often decides—fuel cells show 30–50% lower fuel/maintenance over 10 years. Procurement cycles cut margins ~8–12% (Europe 2024).

| Metric | 2024 |

|---|---|

| Revenue from large contracts | ≈40% |

| Single contract risk | >10% sales |

| Lithium price | $132/kWh |

| Procurement margin hit (EU) | 8–12% |

Preview Before You Purchase

SFC Energy Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for SFC Energy that you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy, with clear assessment of rivalry, supplier power, buyer power, threats of new entrants, and substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

SFC Energy faces medium competitive rivalry with niche tech differentiation, supplier leverage from specialized fuel-cell components, and moderate buyer power driven by defense and industrial clients; threats from substitutes and new entrants are tempered by certifications and IP. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore SFC Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

The production of fuel cells needs precious metals like platinum and specialized proton exchange membranes supplied by a handful of global firms; platinum prices rose 8.3% in 2024 to about $1,050/oz, tightening input cost pressure.

SFC Energy depends on these high-grade inputs for EFOY fuel cell efficiency and lifespan, buying certified membrane stacks with long lead times—industry average lead times hit 20–28 weeks in 2025.

With few high-quality substitutes, suppliers exert strong pricing and delivery leverage; in 2024 supplier concentration saw the top 5 platinum producers control ~60% of mine supply, raising procurement risk for SFC.

Technical Component Uniqueness

SFC Energy uses proprietary electronic modules and custom fuel-cell stacks tied to select engineering partners; swapping suppliers would trigger redesigns and recertification that can cost tens of millions and add 12–24 months per product line, per industry averages. This high technical uniqueness raises supplier switching costs, concentrating bargaining power with incumbent vendors and pressuring SFC’s margins and lead times.

Energy Feedstock Consolidation

High-purity methanol and industrial H2 are critical inputs for SFC Energy fuel cell systems, and global suppliers like Methanex and Air Liquide control ~60–80% of market volume, setting regional prices and distribution rules; in 2024 methanol FOB Rotterdam averaged about $450/ton and industrial H2 pipeline prices ranged $3–7/kg, which directly shapes field operating costs. Supplier consolidation limits SFC’s customers’ total cost of ownership by constraining fuel access and price flexibility.

Supply Chain Resilience and Geopolitics

As of late 2025, higher geopolitical risk has pushed buyers toward localized or allied suppliers for critical energy minerals; suppliers in stable jurisdictions or with vertical integration can charge 10–25% premiums for guaranteed delivery.

SFC Energy must manage regional dependencies—Germany/Europe sourcing and US allies—to keep defense and industrial manufacturing lines running and avoid >5% revenue loss from single-source disruptions.

- Premiums: 10–25% for low-risk suppliers

- Revenue risk: >5% if single-source fails

- Mitigation: dual-sourcing, inventory buffers, vertical partners

Limited Forward Integration Threat

Suppliers hold pricing power for platinum-group catalysts and bipolar plates, but they lack systems-integration know-how to make complete fuel-cell systems; forward-integration risk is low. SFC Energy converts basic inputs into certified off-grid solutions, sustaining gross margins—23.6% in FY2024—that suppliers cannot match. This balance limits supplier leverage while keeping supply-cost exposure.

- Suppliers set raw-material prices

- Rare systems-integration expertise

- Low credible forward-integration threat

- SFC Energy FY2024 gross margin 23.6%

Supplier concentration, long lead times and high switching costs squeeze SFC margins

Suppliers hold strong leverage due to concentrated platinum and membrane supply, long lead times (20–28 weeks in 2025) and high switching costs (12–24 months, tens of millions EUR), pressuring SFC’s margins; FY2024 gross margin was 23.6%.

Mitigations—dual-sourcing, inventory buffers, local allied suppliers—reduce single-source revenue risk (>5%) but cost premiums (10–25%) for low-risk supply persist.

| Metric | Value |

|---|---|

| Platinum price (2024) | $1,050/oz (+8.3%) |

| Lead times (2025) | 20–28 weeks |

| Methanol (2024 FOB Rotterdam) | $450/ton |

| FY2024 gross margin | 23.6% |

What is included in the product

Tailored Porter's Five Forces analysis for SFC Energy, pinpointing competitive rivalry, buyer/supplier power, substitution risks, and barriers to entry with strategic insights on threats, opportunities, and implications for pricing and profitability.

Concise Porter's Five Forces view for SFC Energy—quickly spot competitive threats and opportunities to inform strategic moves.

Customers Bargaining Power

Concentration of Defense and Government Clients

Availability of Alternative Power Technologies

Customers choosing off-grid power can pick fuel cells, advanced lithium-ion batteries, or diesel generators, so buyers pressure SFC Energy by comparing cost and runtime; global lithium-ion pack prices fell ~85% from 2010 to $132/kWh in 2024, raising substitution risk.

High Information Transparency

Professional buyers in industrial and energy sectors access detailed data on fuel cell efficiency (SFC Energy’s EFOY Pro at ~48–52% system efficiency), lifecycle costs (total cost of ownership often 20–35% lower than diesel gensets over 10 years), and competitor pricing, cutting information asymmetry and limiting margin expansion. In 2024 procurement surveys 68% of buyers demanded SLA performance guarantees, so well-informed buyers secure tougher service terms and price concessions.

Low Switching Costs for New Projects

New projects face low switching costs from SFC Energy methanol cartridges to alternatives, so customers frequently choose other providers; SFC must re-prove value for each deployment.

Industrial bidding is highly competitive—tenders often prioritize total cost of ownership; in 2024 average project procurement cycles cut supplier margins by ~8–12% in Europe.

Sensitivity to Total Cost of Ownership

Industrial buyers now prioritize total cost of ownership (TCO), favoring solutions with lower lifecycle costs; for stationary fuel cells SFC Energy (SFC:XETRA) must beat diesel when TCO gap—typically 20–30% higher upfront for fuel cells—is offset by 30–50% lower fuel/maintenance over 10 years per industry studies (2024).

This forces SFC to cut $/kWh through efficiency gains and modular service contracts; a 10% drop in operating cost can shorten payback from ~8 years to ~5–6 years for telecom backup and remote power customers.

Concentrated buyers squeeze margins—TCO tilts fleet buyers toward fuel cells over lithium

Large, concentrated institutional buyers (≈40% revenue 2024) exert strong price and spec pressure; losing one contract (>10% sales) materially hits revenue. Buyers face low switching costs and compare fuel cells vs lithium ($132/kWh 2024) and diesel; TCO often decides—fuel cells show 30–50% lower fuel/maintenance over 10 years. Procurement cycles cut margins ~8–12% (Europe 2024).

| Metric | 2024 |

|---|---|

| Revenue from large contracts | ≈40% |

| Single contract risk | >10% sales |

| Lithium price | $132/kWh |

| Procurement margin hit (EU) | 8–12% |

Preview Before You Purchase

SFC Energy Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for SFC Energy that you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy, with clear assessment of rivalry, supplier power, buyer power, threats of new entrants, and substitutes.