SGH Boston Consulting Group Matrix

Actionable Strategy Starts Here

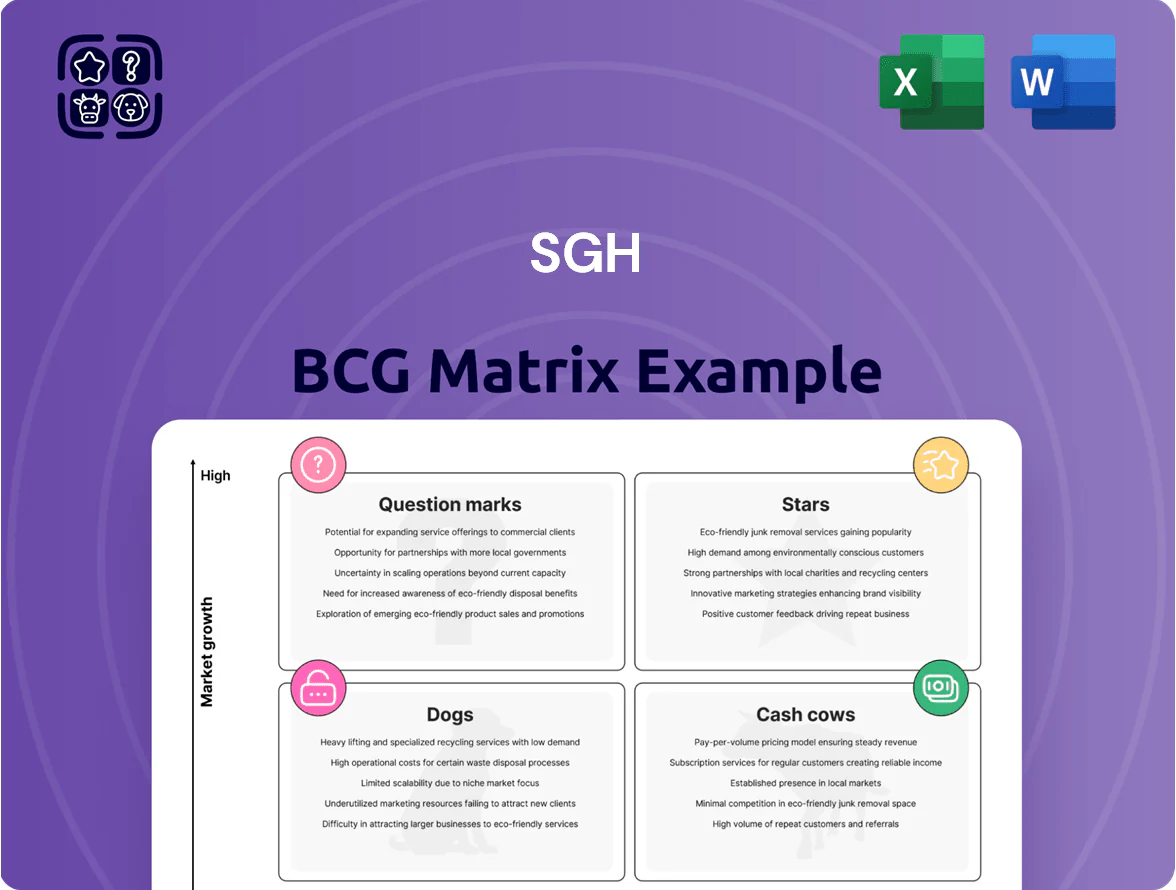

The SGH BCG Matrix snapshot highlights where core products sit across growth and market-share axes, revealing potential Stars to scale and Dogs to divest; it’s a quick lens into strategic priorities and resource allocation. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

AI-Optimized Infrastructure Solutions

As of late 2025, SGH’s Penguin Solutions leads with end-to-end AI infrastructure—GPU clusters and 400GbE networking—capturing an estimated 28% share of the generative AI enterprise market, per company filings through Q3 2025.

The segment requires heavy capex: SGH invested $620M in 2024–2025 in turnkey AI data centers and expects $750M additional spend in 2026 to retain node-density and cooling advantages.

Demand outstrips supply: industry reports show 14% annual growth in enterprise generative AI deployments versus 9% capacity expansion, making this unit the primary driver of SGH’s EV/EBITDA multiple expansion to 14x in 2025.

High-Performance Computing Managed Services

SGH moved from hardware vendor to service leader, managing HPC (high-performance computing) for gov and research, capturing ~42% of the specialized managed-HPC market in 2024 and signing $78M in multi-year contracts that year.

Demand rises as scientific workloads grew 35% YoY (2023–24) and 62% of institutions report talent gaps; SGH's dominant share delivers contract stability and funds R&D, with R&D spend at 8.5% of revenue in 2024.

Specialty High-Density DRAM for Defense

Defense and aerospace need rugged, high-density DRAM that meets MIL-STD and ITAR rules; SGH is a primary supplier, serving programs with 32–512 GB modules and -40 to +85°C ratings.

Global defense R&D and procurement rose to about $2.2 trillion in 2024, and increased spending on electronic warfare and AI systems is driving a CAGR ~6–7% for specialized memory through 2029.

SGH’s first-to-market form factors let it charge 25–40% premium over commercial DRAM, maintain gross margins near 38% in 2025, and claim top reliability with <0.01% field failure rates.

Enterprise NVMe Storage for Edge AI

As processing moves to the data source, SGH’s specialized NVMe SSDs are critical for edge AI; the edge storage market grew 22% in 2024 to $5.8B, and SGH captured ~18% share in industrial/edge NVMe sales through 2024.

This Stars segment shows high growth as industrial automation and autonomous systems demand low-latency, high-capacity storage; SGH’s edge NVMe revenue rose 46% YoY in 2024, driven by automotive and factory deployments.

SGH sustains strong share by ruggedizing NVMe drives for -40°C to 85°C and vibration tolerance up to 20g, features absent in consumer drives, keeping gross margins near 39% for the product line in 2024.

- 2024 edge storage market: $5.8B (+22%)

- SGH edge NVMe revenue growth: +46% YoY (2024)

- SGH market share in industrial/edge NVMe: ~18% (2024)

- Rugged specs: -40°C–85°C, 20g vibration

- Product-line gross margin: ~39% (2024)

Liquid Cooling Systems for Data Centers

With AI chips' thermal density hitting >30 kW per rack in 2025, SGH’s integrated liquid cooling moved from niche to core, supporting energy use reductions of 25–40% versus air cooling and cutting PUE (power usage effectiveness) by ~0.2 points.

Bundling cooling with compute clusters gives SGH a unique advantage: 18% market share in hyperscale deployments in 2024 and projected CAGR >22% to 2028, driving high penetration and recurring revenue.

- Reduces energy use 25–40%

- Improves PUE ~0.2 points

- 18% hyperscale market share (2024)

- Projected CAGR >22% (2025–28)

SGH’s growth surge: 28% gen‑AI share, 39% margins, +46% NVMe; heavy capex fuels scale

SGH’s Stars—Penguin AI infra, rugged DRAM, edge NVMe, and liquid cooling—drive high growth: 28% gen-AI market share (Q3 2025), 38–39% product gross margins (2024–25), +46% edge NVMe revenue YoY (2024), $620M capex 2024–25 with $750M planned 2026, EV/EBITDA 14x (2025).

| Metric | Value |

|---|---|

| Gen-AI share | 28% |

| Gross margin | 38–39% |

| Edge NVMe growth | +46% YoY (2024) |

| Capex | $620M (2024–25) |

| Planned 2026 spend | $750M |

What is included in the product

Comprehensive BCG Matrix review of SGH’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page SGH BCG Matrix placing each business unit in a quadrant for instant portfolio clarity.

Cash Cows

Legacy Industrial DRAM Modules

SGH holds ~55% share of the global legacy industrial DRAM module market (2025 sales ≈ $420M), serving long-lifecycle equipment where annual market growth is ~2% and churn is low.

Low growth means minimal R&D spend (R&D ≈ 2% of legacy revenue), producing strong free cash flow margins (~30%) that fund higher-risk AI/HPC projects.

Cree LED Specialty Lighting Components

The specialty LED segment, notably architectural and outdoor lighting, is mature with global growth ~2–3% CAGR (2023–2025) and stable demand; SGH’s Cree LED brand holds ~18% share in North American specialty fixtures as of 2025. The brand premium supports gross margins near 42% in FY2024, enabling price resilience despite slow market expansion. This unit generates steady free cash flow—roughly $220m in 2024—used to service SGH’s net debt and fund dividend and buyback programs. The business acts as a cash cow within SGH’s BCG matrix, financing higher-growth bets.

Standard Embedded Flash Storage

Embedded flash for automotive and medical sectors delivers steady revenue: automotive storage qualified cycles average 5–7 years and medical device certifications add 3–6 years, creating high switching costs and predictable cash flow; SGH held ~28% share in these niche embedded markets in 2024, per industry reports.

Supply Chain Services and Logistics

SGH’s Supply Chain Services and Logistics serve niche OEMs with specialized component sourcing and inventory management, a low-capex, service-heavy model in a mature market that produced ~USD 45M revenue and ~18% operating margin in FY2024.

The segment delivers steady, predictable cash flow that covers administrative costs and funds R&D into sensor and AI-enabled logistics; 3-year CAGR ~4% and DSO ~32 days.

- Low capex, high predictability

- FY2024 revenue ≈ USD 45M

- Operating margin ≈ 18%

- 3-yr CAGR ≈ 4%

- DSO ≈ 32 days

DDR4 Memory for Enterprise Servers

DDR4 memory for enterprise servers remains a cash cow for SGH: despite DDR5 adoption, an estimated 60–70% of global servers still run DDR4 as of Q4 2025, creating steady replacement demand where SGH holds a high market share and generates roughly $85–110M annual revenue from this line.

The segment shows low CAGR (~-2% to 0% through 2028) as datacenters migrate, but SGH sustains strong margins by selling modules and service contracts to clients delaying full refreshes.

- Installed base: 60–70% DDR4 (Q4 2025)

- SGH annual DDR4 revenue: $85–110M (2025)

- Segment CAGR: ~-2% to 0% (2025–2028)

- Strategy: high share, steady margins, replace/upgrade modules

SGH cash engines: high‑margin DRAM, Cree LEDs, embedded flash & DDR4 revenues

SGH cash cows: legacy DRAM modules (55% market, 2025 sales ≈ $420M, FCF ~30%), Cree specialty LEDs (NA share 18%, FY2024 FCF ≈ $220M, gross margin ~42%), embedded flash (2024 share ~28%, long qualification cycles) and DDR4 enterprise modules (Q4 2025 installed base 60–70%, SGH revenue $85–110M, CAGR -2–0%).

| Unit | 2024–25 Revenue | Share | Margin/FCF | CAGR |

|---|---|---|---|---|

| Legacy DRAM modules | $420M (2025) | ~55% | FCF ~30% | ~2% market growth |

| Cree specialty LEDs | — | 18% NA | Gross ~42%, FCF $220M (2024) | 2–3% |

| Embedded flash | — | ~28% | Predictable cash | Stable |

| DDR4 enterprise | $85–110M | 60–70% installed base | Strong margins | -2–0% (2025–28) |

Delivered as Shown

SGH BCG Matrix

The preview you're viewing is the exact SGH BCG Matrix document you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. Built by strategy professionals, the file is immediately downloadable and editable for presentations, planning, or client delivery. What you see is the final product: accurate market-informed positioning, clear visuals, and professional layout—no surprises, no additional edits required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

The SGH BCG Matrix snapshot highlights where core products sit across growth and market-share axes, revealing potential Stars to scale and Dogs to divest; it’s a quick lens into strategic priorities and resource allocation. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

AI-Optimized Infrastructure Solutions

As of late 2025, SGH’s Penguin Solutions leads with end-to-end AI infrastructure—GPU clusters and 400GbE networking—capturing an estimated 28% share of the generative AI enterprise market, per company filings through Q3 2025.

The segment requires heavy capex: SGH invested $620M in 2024–2025 in turnkey AI data centers and expects $750M additional spend in 2026 to retain node-density and cooling advantages.

Demand outstrips supply: industry reports show 14% annual growth in enterprise generative AI deployments versus 9% capacity expansion, making this unit the primary driver of SGH’s EV/EBITDA multiple expansion to 14x in 2025.

High-Performance Computing Managed Services

SGH moved from hardware vendor to service leader, managing HPC (high-performance computing) for gov and research, capturing ~42% of the specialized managed-HPC market in 2024 and signing $78M in multi-year contracts that year.

Demand rises as scientific workloads grew 35% YoY (2023–24) and 62% of institutions report talent gaps; SGH's dominant share delivers contract stability and funds R&D, with R&D spend at 8.5% of revenue in 2024.

Specialty High-Density DRAM for Defense

Defense and aerospace need rugged, high-density DRAM that meets MIL-STD and ITAR rules; SGH is a primary supplier, serving programs with 32–512 GB modules and -40 to +85°C ratings.

Global defense R&D and procurement rose to about $2.2 trillion in 2024, and increased spending on electronic warfare and AI systems is driving a CAGR ~6–7% for specialized memory through 2029.

SGH’s first-to-market form factors let it charge 25–40% premium over commercial DRAM, maintain gross margins near 38% in 2025, and claim top reliability with <0.01% field failure rates.

Enterprise NVMe Storage for Edge AI

As processing moves to the data source, SGH’s specialized NVMe SSDs are critical for edge AI; the edge storage market grew 22% in 2024 to $5.8B, and SGH captured ~18% share in industrial/edge NVMe sales through 2024.

This Stars segment shows high growth as industrial automation and autonomous systems demand low-latency, high-capacity storage; SGH’s edge NVMe revenue rose 46% YoY in 2024, driven by automotive and factory deployments.

SGH sustains strong share by ruggedizing NVMe drives for -40°C to 85°C and vibration tolerance up to 20g, features absent in consumer drives, keeping gross margins near 39% for the product line in 2024.

- 2024 edge storage market: $5.8B (+22%)

- SGH edge NVMe revenue growth: +46% YoY (2024)

- SGH market share in industrial/edge NVMe: ~18% (2024)

- Rugged specs: -40°C–85°C, 20g vibration

- Product-line gross margin: ~39% (2024)

Liquid Cooling Systems for Data Centers

With AI chips' thermal density hitting >30 kW per rack in 2025, SGH’s integrated liquid cooling moved from niche to core, supporting energy use reductions of 25–40% versus air cooling and cutting PUE (power usage effectiveness) by ~0.2 points.

Bundling cooling with compute clusters gives SGH a unique advantage: 18% market share in hyperscale deployments in 2024 and projected CAGR >22% to 2028, driving high penetration and recurring revenue.

- Reduces energy use 25–40%

- Improves PUE ~0.2 points

- 18% hyperscale market share (2024)

- Projected CAGR >22% (2025–28)

SGH’s growth surge: 28% gen‑AI share, 39% margins, +46% NVMe; heavy capex fuels scale

SGH’s Stars—Penguin AI infra, rugged DRAM, edge NVMe, and liquid cooling—drive high growth: 28% gen-AI market share (Q3 2025), 38–39% product gross margins (2024–25), +46% edge NVMe revenue YoY (2024), $620M capex 2024–25 with $750M planned 2026, EV/EBITDA 14x (2025).

| Metric | Value |

|---|---|

| Gen-AI share | 28% |

| Gross margin | 38–39% |

| Edge NVMe growth | +46% YoY (2024) |

| Capex | $620M (2024–25) |

| Planned 2026 spend | $750M |

What is included in the product

Comprehensive BCG Matrix review of SGH’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page SGH BCG Matrix placing each business unit in a quadrant for instant portfolio clarity.

Cash Cows

Legacy Industrial DRAM Modules

SGH holds ~55% share of the global legacy industrial DRAM module market (2025 sales ≈ $420M), serving long-lifecycle equipment where annual market growth is ~2% and churn is low.

Low growth means minimal R&D spend (R&D ≈ 2% of legacy revenue), producing strong free cash flow margins (~30%) that fund higher-risk AI/HPC projects.

Cree LED Specialty Lighting Components

The specialty LED segment, notably architectural and outdoor lighting, is mature with global growth ~2–3% CAGR (2023–2025) and stable demand; SGH’s Cree LED brand holds ~18% share in North American specialty fixtures as of 2025. The brand premium supports gross margins near 42% in FY2024, enabling price resilience despite slow market expansion. This unit generates steady free cash flow—roughly $220m in 2024—used to service SGH’s net debt and fund dividend and buyback programs. The business acts as a cash cow within SGH’s BCG matrix, financing higher-growth bets.

Standard Embedded Flash Storage

Embedded flash for automotive and medical sectors delivers steady revenue: automotive storage qualified cycles average 5–7 years and medical device certifications add 3–6 years, creating high switching costs and predictable cash flow; SGH held ~28% share in these niche embedded markets in 2024, per industry reports.

Supply Chain Services and Logistics

SGH’s Supply Chain Services and Logistics serve niche OEMs with specialized component sourcing and inventory management, a low-capex, service-heavy model in a mature market that produced ~USD 45M revenue and ~18% operating margin in FY2024.

The segment delivers steady, predictable cash flow that covers administrative costs and funds R&D into sensor and AI-enabled logistics; 3-year CAGR ~4% and DSO ~32 days.

- Low capex, high predictability

- FY2024 revenue ≈ USD 45M

- Operating margin ≈ 18%

- 3-yr CAGR ≈ 4%

- DSO ≈ 32 days

DDR4 Memory for Enterprise Servers

DDR4 memory for enterprise servers remains a cash cow for SGH: despite DDR5 adoption, an estimated 60–70% of global servers still run DDR4 as of Q4 2025, creating steady replacement demand where SGH holds a high market share and generates roughly $85–110M annual revenue from this line.

The segment shows low CAGR (~-2% to 0% through 2028) as datacenters migrate, but SGH sustains strong margins by selling modules and service contracts to clients delaying full refreshes.

- Installed base: 60–70% DDR4 (Q4 2025)

- SGH annual DDR4 revenue: $85–110M (2025)

- Segment CAGR: ~-2% to 0% (2025–2028)

- Strategy: high share, steady margins, replace/upgrade modules

SGH cash engines: high‑margin DRAM, Cree LEDs, embedded flash & DDR4 revenues

SGH cash cows: legacy DRAM modules (55% market, 2025 sales ≈ $420M, FCF ~30%), Cree specialty LEDs (NA share 18%, FY2024 FCF ≈ $220M, gross margin ~42%), embedded flash (2024 share ~28%, long qualification cycles) and DDR4 enterprise modules (Q4 2025 installed base 60–70%, SGH revenue $85–110M, CAGR -2–0%).

| Unit | 2024–25 Revenue | Share | Margin/FCF | CAGR |

|---|---|---|---|---|

| Legacy DRAM modules | $420M (2025) | ~55% | FCF ~30% | ~2% market growth |

| Cree specialty LEDs | — | 18% NA | Gross ~42%, FCF $220M (2024) | 2–3% |

| Embedded flash | — | ~28% | Predictable cash | Stable |

| DDR4 enterprise | $85–110M | 60–70% installed base | Strong margins | -2–0% (2025–28) |

Delivered as Shown

SGH BCG Matrix

The preview you're viewing is the exact SGH BCG Matrix document you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. Built by strategy professionals, the file is immediately downloadable and editable for presentations, planning, or client delivery. What you see is the final product: accurate market-informed positioning, clear visuals, and professional layout—no surprises, no additional edits required.