SGS PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

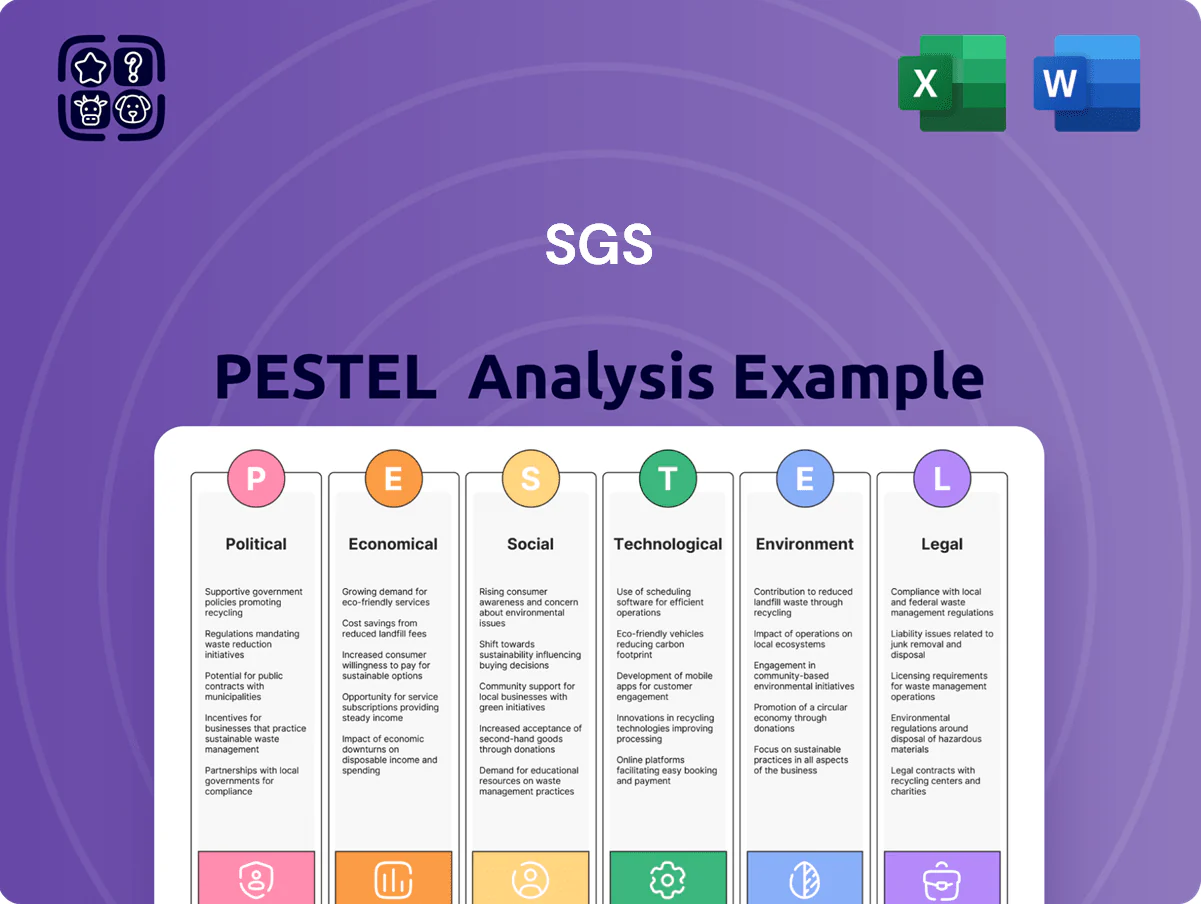

Unlock strategic clarity with our SGS PESTLE Analysis—distilling political, economic, social, technological, legal, and environmental forces that will shape SGS’s next moves; ideal for investors, consultants, and executives seeking actionable intelligence. Purchase the full report to get a fully sourced, editable deep dive that saves research time and powers confident decisions—download instantly and start applying insights today.

Political factors

Geopolitical trade tensions

As of late 2025 persistent geopolitical rivalries and rising trade protectionism have fragmented supply chains, with WTO reporting global trade growth slowing to 1.2% in 2024–25; SGS faces shifting tariffs and localized barriers that altered cross-border inspection volumes by an estimated 6–9% year-on-year. SGS acts as a critical intermediary, enabling compliance with over 140 regional regulatory regimes and supporting clients through inspection, testing and certification to sustain international trade.

Government infrastructure investment

Regulatory harmonization efforts

Political initiatives to harmonize technical standards between trading blocs—e.g., EU-US talks and RCEP alignment—have reduced certification overlaps, cutting compliance time by up to 20% for global manufacturers; in 2024 SGS reported a 12% rise in cross-border testing volumes tied to such reforms.

Energy security and policy

National policies driving energy independence and renewables are reshaping utilities; the EU aims for 42.5% renewable electricity by 2030 and the US Inflation Reduction Act directs ~$369bn (2024–2031) to clean energy, increasing demand for SGS verification across projects.

SGS verifies nuclear safety, inspects hydrogen systems and tests fuel cells—markets where hydrogen demand could reach 78 Mt H2 by 2050 (IEA Net Zero), prompting more certification work.

Stricter efficiency mandates (e.g., EU Ecodesign, US appliance/industrial rules) boost need for independent energy audits; SGS revenue from energy-related testing and certification grew ~6–8% in 2024 across peers, signaling rising market opportunity.

- Policy-driven renewable targets (EU 42.5% by 2030) and US $369bn IRA funding

- Hydrogen demand projection ~78 Mt H2 by 2050 supports testing/certification

- Stronger efficiency mandates increase independent audit demand; sector revenues up ~6–8% in 2024

Support for domestic manufacturing

Many governments offered >$200bn in reshoring incentives in 2024–25, driving new plant builds that need local HSE certification; SGS can deliver site-specific audits, commissioning inspections and certification to meet national standards. In 2025 SGS reported strong demand growth in industrial services tied to reshoring projects, supporting quality control across setup and operational phases.

- >$200bn global reshoring incentives (2024–25)

- Increased demand for HSE certification and commissioning

- SGS provides audits, QC, commissioning inspections

Trade frictions slow growth; infrastructure & reshoring spur testing, certification surge

Geopolitical trade frictions slowed global trade to ~1.2% (2024–25), shifting tariffs and raising inspection volumes ~6–9%; public infrastructure spending ~$1.5tn (2024–25) lifted SGS infrastructure revenue ~7% (2024); harmonized standards cut compliance time up to 20% and drove a 12% rise in cross-border testing (2024); reshoring incentives >$200bn (2024–25) increased HSE/certification demand.

| Metric | Value |

|---|---|

| Global trade growth (2024–25) | ~1.2% |

| Infrastructure spending | $1.5tn |

| SGS infra rev growth (2024) | ~7% |

| Cross-border testing rise (2024) | 12% |

| Reshoring incentives (2024–25) | >$200bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect SGS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses SGS’s full PESTLE into a clean, shareable summary that’s visually segmented by category and editable for local context, enabling quick alignment across teams and seamless insertion into presentations or strategy packs.

Economic factors

Global inflationary trends

Continued fluctuations in global inflation—with OECD consumer prices up 5.0% in 2024 vs 3.8% in 2023—raise operational costs for SGS, notably for specialized lab equipment and skilled technicians.

SGS offsets margin pressure through dynamic pricing and a shift to high-value services; testing and certification revenue grew 7% in 2024, aiding margin resilience.

Profitability hinges on balancing cost structure against rising energy (+8% in industrial electricity prices 2024) and consumables inflation, requiring ongoing pricing discipline and supply-chain optimization.

Emerging market growth

Economic expansion in Southeast Asia and parts of Africa—with IMF 2024 GDP growth forecasts of 4.9% for Southeast Asia and 3.8% for Sub-Saharan Africa in 2025—drives demand for testing and certification as firms industrialize.

Local exporters increasingly seek international accreditation to access markets; SGS reported 6% revenue growth in Asia in 2024, reflecting this trend.

SGS is expanding labs and field services in high-growth markets to capture rising needs in food safety, mining and manufacturing inspections, where inspection volumes rose ~8% regionally in 2024.

Commodity price volatility

The economic health of mining and oil & gas drives demand for SGS’s natural resource services; global mining investment fell 6% in 2024 to about $360bn, pressuring exploration spends. Commodity price swings—copper down ~18% and Brent crude averaging $82/bbl in 2024—directly affect client activity levels. SGS reduces exposure by diversifying into agriculture and consumer goods, where testing and inspection revenue grew ~7% in 2024.

Currency exchange rate fluctuations

As a Swiss-headquartered firm in 140+ countries, SGS faces material currency translation risk; a 10% appreciation of the Swiss franc vs the USD would reduce reported USD revenues materially (e.g., CHF strengthened ~3.5% vs USD in 2024 ytd impacting margins).

SGS uses hedging and 60-70% local-currency billing in many markets and reported a 2024 FX impact adjustment of roughly CHF 50–100m on operating income.

- Exposure: 140+ countries; major pairs CHF/USD, CHF/EUR

- Mitigation: hedging strategies plus ~60–70% local-currency billing

- 2024 illustrative FX effect: ~CHF 50–100m on operating income

Shift toward service-based economies

The shift to service-based economies—services accounted for about 77% of global GDP in 2024—raises demand for inspections of intangible assets like data security, service quality, and governance, changing SGS's client needs.

SGS is expanding digital and process-oriented audits: in 2025 its certification and digital assurance services grew ~12% YoY as enterprises prioritize cloud security and ESG governance verification.

- Services ~77% of global GDP (2024)

- SGS digital assurance growth ~12% YoY (2025)

- Focus: data security, service quality, governance

Inflation, FX and energy squeeze margins as testing growth and EM demand cushion SGS

Inflationary pressure (OECD CPI 5.0% in 2024) raises SGS operating costs while testing/certification revenue grew 7% in 2024 to offset margins; energy +8% (industrial electricity 2024) and consumables inflation require pricing and supply optimization. Regional GDP: SE Asia 4.9% (IMF 2024), Sub‑Saharan Africa 3.8% (2025), driving demand; mining capex fell 6% to ~$360bn (2024). FX: CHF up ~3.5% vs USD in 2024, 2024 FX hit ~CHF50–100m.

| Metric | Value |

|---|---|

| OECD CPI (2024) | +5.0% |

| Testing & certification rev growth (2024) | +7% |

| Industrial electricity (2024) | +8% |

| SE Asia GDP (2024) | 4.9% |

| Sub‑Saharan Africa GDP (2025) | 3.8% |

| Global mining investment (2024) | ~$360bn (-6%) |

| CHF vs USD (2024) | +3.5% |

| 2024 FX impact on OI | ~CHF50–100m |

Preview the Actual Deliverable

SGS PESTLE Analysis

The preview shown here is the exact SGS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our SGS PESTLE Analysis—distilling political, economic, social, technological, legal, and environmental forces that will shape SGS’s next moves; ideal for investors, consultants, and executives seeking actionable intelligence. Purchase the full report to get a fully sourced, editable deep dive that saves research time and powers confident decisions—download instantly and start applying insights today.

Political factors

Geopolitical trade tensions

As of late 2025 persistent geopolitical rivalries and rising trade protectionism have fragmented supply chains, with WTO reporting global trade growth slowing to 1.2% in 2024–25; SGS faces shifting tariffs and localized barriers that altered cross-border inspection volumes by an estimated 6–9% year-on-year. SGS acts as a critical intermediary, enabling compliance with over 140 regional regulatory regimes and supporting clients through inspection, testing and certification to sustain international trade.

Government infrastructure investment

Regulatory harmonization efforts

Political initiatives to harmonize technical standards between trading blocs—e.g., EU-US talks and RCEP alignment—have reduced certification overlaps, cutting compliance time by up to 20% for global manufacturers; in 2024 SGS reported a 12% rise in cross-border testing volumes tied to such reforms.

Energy security and policy

National policies driving energy independence and renewables are reshaping utilities; the EU aims for 42.5% renewable electricity by 2030 and the US Inflation Reduction Act directs ~$369bn (2024–2031) to clean energy, increasing demand for SGS verification across projects.

SGS verifies nuclear safety, inspects hydrogen systems and tests fuel cells—markets where hydrogen demand could reach 78 Mt H2 by 2050 (IEA Net Zero), prompting more certification work.

Stricter efficiency mandates (e.g., EU Ecodesign, US appliance/industrial rules) boost need for independent energy audits; SGS revenue from energy-related testing and certification grew ~6–8% in 2024 across peers, signaling rising market opportunity.

- Policy-driven renewable targets (EU 42.5% by 2030) and US $369bn IRA funding

- Hydrogen demand projection ~78 Mt H2 by 2050 supports testing/certification

- Stronger efficiency mandates increase independent audit demand; sector revenues up ~6–8% in 2024

Support for domestic manufacturing

Many governments offered >$200bn in reshoring incentives in 2024–25, driving new plant builds that need local HSE certification; SGS can deliver site-specific audits, commissioning inspections and certification to meet national standards. In 2025 SGS reported strong demand growth in industrial services tied to reshoring projects, supporting quality control across setup and operational phases.

- >$200bn global reshoring incentives (2024–25)

- Increased demand for HSE certification and commissioning

- SGS provides audits, QC, commissioning inspections

Trade frictions slow growth; infrastructure & reshoring spur testing, certification surge

Geopolitical trade frictions slowed global trade to ~1.2% (2024–25), shifting tariffs and raising inspection volumes ~6–9%; public infrastructure spending ~$1.5tn (2024–25) lifted SGS infrastructure revenue ~7% (2024); harmonized standards cut compliance time up to 20% and drove a 12% rise in cross-border testing (2024); reshoring incentives >$200bn (2024–25) increased HSE/certification demand.

| Metric | Value |

|---|---|

| Global trade growth (2024–25) | ~1.2% |

| Infrastructure spending | $1.5tn |

| SGS infra rev growth (2024) | ~7% |

| Cross-border testing rise (2024) | 12% |

| Reshoring incentives (2024–25) | >$200bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect SGS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses SGS’s full PESTLE into a clean, shareable summary that’s visually segmented by category and editable for local context, enabling quick alignment across teams and seamless insertion into presentations or strategy packs.

Economic factors

Global inflationary trends

Continued fluctuations in global inflation—with OECD consumer prices up 5.0% in 2024 vs 3.8% in 2023—raise operational costs for SGS, notably for specialized lab equipment and skilled technicians.

SGS offsets margin pressure through dynamic pricing and a shift to high-value services; testing and certification revenue grew 7% in 2024, aiding margin resilience.

Profitability hinges on balancing cost structure against rising energy (+8% in industrial electricity prices 2024) and consumables inflation, requiring ongoing pricing discipline and supply-chain optimization.

Emerging market growth

Economic expansion in Southeast Asia and parts of Africa—with IMF 2024 GDP growth forecasts of 4.9% for Southeast Asia and 3.8% for Sub-Saharan Africa in 2025—drives demand for testing and certification as firms industrialize.

Local exporters increasingly seek international accreditation to access markets; SGS reported 6% revenue growth in Asia in 2024, reflecting this trend.

SGS is expanding labs and field services in high-growth markets to capture rising needs in food safety, mining and manufacturing inspections, where inspection volumes rose ~8% regionally in 2024.

Commodity price volatility

The economic health of mining and oil & gas drives demand for SGS’s natural resource services; global mining investment fell 6% in 2024 to about $360bn, pressuring exploration spends. Commodity price swings—copper down ~18% and Brent crude averaging $82/bbl in 2024—directly affect client activity levels. SGS reduces exposure by diversifying into agriculture and consumer goods, where testing and inspection revenue grew ~7% in 2024.

Currency exchange rate fluctuations

As a Swiss-headquartered firm in 140+ countries, SGS faces material currency translation risk; a 10% appreciation of the Swiss franc vs the USD would reduce reported USD revenues materially (e.g., CHF strengthened ~3.5% vs USD in 2024 ytd impacting margins).

SGS uses hedging and 60-70% local-currency billing in many markets and reported a 2024 FX impact adjustment of roughly CHF 50–100m on operating income.

- Exposure: 140+ countries; major pairs CHF/USD, CHF/EUR

- Mitigation: hedging strategies plus ~60–70% local-currency billing

- 2024 illustrative FX effect: ~CHF 50–100m on operating income

Shift toward service-based economies

The shift to service-based economies—services accounted for about 77% of global GDP in 2024—raises demand for inspections of intangible assets like data security, service quality, and governance, changing SGS's client needs.

SGS is expanding digital and process-oriented audits: in 2025 its certification and digital assurance services grew ~12% YoY as enterprises prioritize cloud security and ESG governance verification.

- Services ~77% of global GDP (2024)

- SGS digital assurance growth ~12% YoY (2025)

- Focus: data security, service quality, governance

Inflation, FX and energy squeeze margins as testing growth and EM demand cushion SGS

Inflationary pressure (OECD CPI 5.0% in 2024) raises SGS operating costs while testing/certification revenue grew 7% in 2024 to offset margins; energy +8% (industrial electricity 2024) and consumables inflation require pricing and supply optimization. Regional GDP: SE Asia 4.9% (IMF 2024), Sub‑Saharan Africa 3.8% (2025), driving demand; mining capex fell 6% to ~$360bn (2024). FX: CHF up ~3.5% vs USD in 2024, 2024 FX hit ~CHF50–100m.

| Metric | Value |

|---|---|

| OECD CPI (2024) | +5.0% |

| Testing & certification rev growth (2024) | +7% |

| Industrial electricity (2024) | +8% |

| SE Asia GDP (2024) | 4.9% |

| Sub‑Saharan Africa GDP (2025) | 3.8% |

| Global mining investment (2024) | ~$360bn (-6%) |

| CHF vs USD (2024) | +3.5% |

| 2024 FX impact on OI | ~CHF50–100m |

Preview the Actual Deliverable

SGS PESTLE Analysis

The preview shown here is the exact SGS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll be able to download immediately after payment.