Shanghai Shenda SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Shanghai Shenda’s niche in textiles and integrated supply chains offers resilient domestic demand and export potential, but faces margin pressure from rising raw material costs and intense competition; governance and sustainability practices could unlock differentiation. Purchase the full SWOT analysis to access an editable, research-backed report and Excel matrix—perfect for investors and strategists seeking actionable insights.

Strengths

Dominant Global Automotive Interior Footprint

Robust State-Owned Enterprise Support

As a core firm under Shanghai SASAC (Shanghai State-owned Assets Supervision and Administration Commission), Shanghai Shenda gains reliable capital access—including a 2024 reported RMB 1.2 billion credit facility from state banks—and preferential entry to national projects like the 2025 smart-manufacturing initiative; this backing cuts refinancing risk during global downturns and aligns Shenda with Shanghai’s regional industrial plan, where state-owned firms accounted for roughly 42% of local fixed-asset investment in 2023.

Diversified Multi-Sector Business Model

Shanghai Shenda balances higher-growth automotive components (22% of 2024 revenue, faster margin expansion) with stable textile trade (38% of 2024 revenue), reducing exposure to any single sector and smoothing cash flow volatility.

Operating in both manufacturing and international trade lets Shenda cut supply-chain and logistics costs—management reported a 6.2% YoY reduction in consolidated freight and procurement expense in FY2024—creating internal synergies that bolster resilience.

Advanced Technical Textile Capabilities

Shanghai Shenda has invested over CNY 1.2 billion since 2019 in high-performance textile R&D, producing materials for aerospace, environmental protection, and geomaterials that fetch gross margins ~28–35% vs 12–18% for apparel in 2024.

These technical products weaken exposure to fashion cycles and align with a 2025 global industrial fiber demand growth forecast of ~4.5% CAGR, positioning Shenda to capture higher-margin industrial sales.

- R&D spend CNY 1.2B+ (2019–2024)

- Tech product gross margin 28–35% (2024)

- Apparel gross margin 12–18% (2024)

- Industrial fiber demand ~4.5% CAGR to 2025

Established International Trade Infrastructure

With over 30 years in textile import/export, Shanghai Shenda serves 120+ global clients and sources from 200+ suppliers, giving it deep market access and trade expertise.

The firm reported RMB 6.2 billion revenue in 2024 and a 12% gross margin, showing scale that deters smaller rivals from matching pricing and logistics reach.

Long-term reliability has made Shenda a preferred partner for major retailers like H&M and Decathlon, securing multi-year contracts that stabilize cash flow.

- 30+ years experience

- 120+ global clients

- 200+ supplier network

- RMB 6.2bn revenue (2024)

- 12% gross margin (2024)

Shanghai Shenda: $1.2bn Auria JV, 28–35% tech margins, RMB 6.2bn revenue, state-backed

Shanghai Shenda leverages a 49% stake in Auria (~$1.2bn JV revenue 2024), 28 plants across NA/EU/ASIA, RMB 6.2bn group revenue (2024) and CNY 1.2bn R&D (2019–24) to secure higher-margin industrial textile sales (28–35% gross margin 2024) while reducing risk via state backing (RMB 1.2bn 2024 credit) and 120+ global clients.

| Metric | Value |

|---|---|

| Auria JV revenue (2024) | $1.2bn |

| Group revenue (2024) | RMB 6.2bn |

| R&D spend (2019–24) | CNY 1.2bn |

| Tech product GM (2024) | 28–35% |

| State credit (2024) | RMB 1.2bn |

What is included in the product

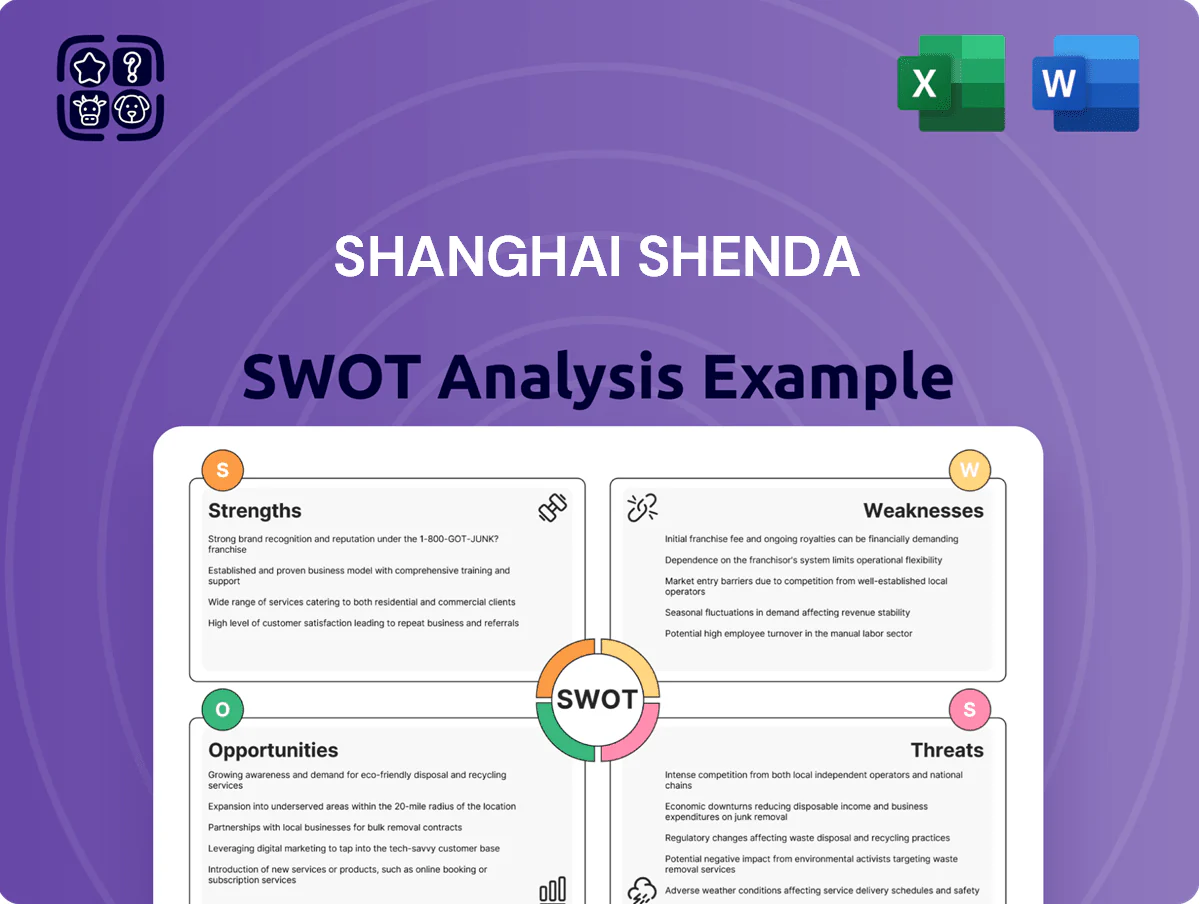

Provides a concise SWOT overview of Shanghai Shenda, mapping its internal strengths and weaknesses alongside external opportunities and threats to assess competitive position and strategic priorities.

Offers a concise SWOT snapshot of Shanghai Shenda to speed strategic alignment and stakeholder briefings.

Weaknesses

Persistent High Financial Leverage

Shanghai Shenda’s aggressive global expansion and acquisitions left net debt at about RMB 18.4 billion as of FY2024, keeping leverage (net debt/EBITDA) near 4.2x, which strains liquidity and credit metrics.

High interest expense—roughly RMB 680 million in 2024—consumed about 28% of operating profit, cutting funds available for CAPEX or strategic M&A.

Management faces a clear task: cut leverage to below 3.0x to lift net margins and improve the company’s credit profile and borrowing costs.

Low Profitability in Core Trade Segments

The traditional textile and garment export arm faces a commoditized market with razor-thin margins—China apparel export unit margins fell below 4% in 2024 according to Ministry of Commerce data—while rising labor and fixed costs (wage growth ~5–7% annually in Jiangsu, 2022–24) have further squeezed profits; without faster moves into design-led, branded, or service offerings, the trade division risks underperforming the more profitable manufacturing business and dragging consolidated ROE down.

Heavy Sensitivity to Automotive Cycles

A large share of Shanghai Shenda’s market value stems from its automotive interior trim units, so its results swing with global vehicle output—world car production fell 6% to 75.7 million units in 2023 and industry forecasts in Jan 2025 still showed only gradual recovery to ~79 million in 2025, stressing Shenda’s revenue base.

When global or Chinese passenger vehicle sales drop, Shenda’s order books shrink quickly; in 2023 Shenda’s auto-related revenue declined about 8% year-on-year, amplifying earnings swings.

This cyclicality raises earnings volatility—Shenda’s trailing-12-month EBITDA margin swung ±350 basis points in 2022–24—making the stock less attractive to risk-averse, long-horizon investors.

Operational Complexity of Global Subsidiaries

- 18% higher SG&A/rev (2024)

- $24m extra compliance spend (2024)

- ~6% annual capex on integration

Exposure to Foreign Exchange Risks

- 28% of 2024 revenue from exports

- $2.1bn foreign assets (2024)

- $47m hedging gains in 2024

- Hedging limits long-term structural risk

High leverage and weak margins squeeze liquidity as auto downturn and high SG&A bite

High leverage (net debt ~RMB18.4bn, net debt/EBITDA ~4.2x in FY2024) and RMB680m interest cost in 2024 squeeze liquidity and capex; export textiles show sub-4% margins and rising wages (Jiangsu wage growth ~5–7% 2022–24); auto cyclicality cuts revenue (auto sales down 6% global 2023; Shenda auto rev −8% YoY 2023) and SG&A/rev was 18% above peers in 2024.

| Metric | 2024 |

|---|---|

| Net debt | RMB18.4bn |

| Net debt/EBITDA | 4.2x |

| Interest expense | RMB680m |

| Textile margin | <4% |

| Auto rev change | −8% YoY (2023) |

| SG&A/rev vs peers | +18% |

What You See Is What You Get

Shanghai Shenda SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Shanghai Shenda’s niche in textiles and integrated supply chains offers resilient domestic demand and export potential, but faces margin pressure from rising raw material costs and intense competition; governance and sustainability practices could unlock differentiation. Purchase the full SWOT analysis to access an editable, research-backed report and Excel matrix—perfect for investors and strategists seeking actionable insights.

Strengths

Dominant Global Automotive Interior Footprint

Robust State-Owned Enterprise Support

As a core firm under Shanghai SASAC (Shanghai State-owned Assets Supervision and Administration Commission), Shanghai Shenda gains reliable capital access—including a 2024 reported RMB 1.2 billion credit facility from state banks—and preferential entry to national projects like the 2025 smart-manufacturing initiative; this backing cuts refinancing risk during global downturns and aligns Shenda with Shanghai’s regional industrial plan, where state-owned firms accounted for roughly 42% of local fixed-asset investment in 2023.

Diversified Multi-Sector Business Model

Shanghai Shenda balances higher-growth automotive components (22% of 2024 revenue, faster margin expansion) with stable textile trade (38% of 2024 revenue), reducing exposure to any single sector and smoothing cash flow volatility.

Operating in both manufacturing and international trade lets Shenda cut supply-chain and logistics costs—management reported a 6.2% YoY reduction in consolidated freight and procurement expense in FY2024—creating internal synergies that bolster resilience.

Advanced Technical Textile Capabilities

Shanghai Shenda has invested over CNY 1.2 billion since 2019 in high-performance textile R&D, producing materials for aerospace, environmental protection, and geomaterials that fetch gross margins ~28–35% vs 12–18% for apparel in 2024.

These technical products weaken exposure to fashion cycles and align with a 2025 global industrial fiber demand growth forecast of ~4.5% CAGR, positioning Shenda to capture higher-margin industrial sales.

- R&D spend CNY 1.2B+ (2019–2024)

- Tech product gross margin 28–35% (2024)

- Apparel gross margin 12–18% (2024)

- Industrial fiber demand ~4.5% CAGR to 2025

Established International Trade Infrastructure

With over 30 years in textile import/export, Shanghai Shenda serves 120+ global clients and sources from 200+ suppliers, giving it deep market access and trade expertise.

The firm reported RMB 6.2 billion revenue in 2024 and a 12% gross margin, showing scale that deters smaller rivals from matching pricing and logistics reach.

Long-term reliability has made Shenda a preferred partner for major retailers like H&M and Decathlon, securing multi-year contracts that stabilize cash flow.

- 30+ years experience

- 120+ global clients

- 200+ supplier network

- RMB 6.2bn revenue (2024)

- 12% gross margin (2024)

Shanghai Shenda: $1.2bn Auria JV, 28–35% tech margins, RMB 6.2bn revenue, state-backed

Shanghai Shenda leverages a 49% stake in Auria (~$1.2bn JV revenue 2024), 28 plants across NA/EU/ASIA, RMB 6.2bn group revenue (2024) and CNY 1.2bn R&D (2019–24) to secure higher-margin industrial textile sales (28–35% gross margin 2024) while reducing risk via state backing (RMB 1.2bn 2024 credit) and 120+ global clients.

| Metric | Value |

|---|---|

| Auria JV revenue (2024) | $1.2bn |

| Group revenue (2024) | RMB 6.2bn |

| R&D spend (2019–24) | CNY 1.2bn |

| Tech product GM (2024) | 28–35% |

| State credit (2024) | RMB 1.2bn |

What is included in the product

Provides a concise SWOT overview of Shanghai Shenda, mapping its internal strengths and weaknesses alongside external opportunities and threats to assess competitive position and strategic priorities.

Offers a concise SWOT snapshot of Shanghai Shenda to speed strategic alignment and stakeholder briefings.

Weaknesses

Persistent High Financial Leverage

Shanghai Shenda’s aggressive global expansion and acquisitions left net debt at about RMB 18.4 billion as of FY2024, keeping leverage (net debt/EBITDA) near 4.2x, which strains liquidity and credit metrics.

High interest expense—roughly RMB 680 million in 2024—consumed about 28% of operating profit, cutting funds available for CAPEX or strategic M&A.

Management faces a clear task: cut leverage to below 3.0x to lift net margins and improve the company’s credit profile and borrowing costs.

Low Profitability in Core Trade Segments

The traditional textile and garment export arm faces a commoditized market with razor-thin margins—China apparel export unit margins fell below 4% in 2024 according to Ministry of Commerce data—while rising labor and fixed costs (wage growth ~5–7% annually in Jiangsu, 2022–24) have further squeezed profits; without faster moves into design-led, branded, or service offerings, the trade division risks underperforming the more profitable manufacturing business and dragging consolidated ROE down.

Heavy Sensitivity to Automotive Cycles

A large share of Shanghai Shenda’s market value stems from its automotive interior trim units, so its results swing with global vehicle output—world car production fell 6% to 75.7 million units in 2023 and industry forecasts in Jan 2025 still showed only gradual recovery to ~79 million in 2025, stressing Shenda’s revenue base.

When global or Chinese passenger vehicle sales drop, Shenda’s order books shrink quickly; in 2023 Shenda’s auto-related revenue declined about 8% year-on-year, amplifying earnings swings.

This cyclicality raises earnings volatility—Shenda’s trailing-12-month EBITDA margin swung ±350 basis points in 2022–24—making the stock less attractive to risk-averse, long-horizon investors.

Operational Complexity of Global Subsidiaries

- 18% higher SG&A/rev (2024)

- $24m extra compliance spend (2024)

- ~6% annual capex on integration

Exposure to Foreign Exchange Risks

- 28% of 2024 revenue from exports

- $2.1bn foreign assets (2024)

- $47m hedging gains in 2024

- Hedging limits long-term structural risk

High leverage and weak margins squeeze liquidity as auto downturn and high SG&A bite

High leverage (net debt ~RMB18.4bn, net debt/EBITDA ~4.2x in FY2024) and RMB680m interest cost in 2024 squeeze liquidity and capex; export textiles show sub-4% margins and rising wages (Jiangsu wage growth ~5–7% 2022–24); auto cyclicality cuts revenue (auto sales down 6% global 2023; Shenda auto rev −8% YoY 2023) and SG&A/rev was 18% above peers in 2024.

| Metric | 2024 |

|---|---|

| Net debt | RMB18.4bn |

| Net debt/EBITDA | 4.2x |

| Interest expense | RMB680m |

| Textile margin | <4% |

| Auto rev change | −8% YoY (2023) |

| SG&A/rev vs peers | +18% |

What You See Is What You Get

Shanghai Shenda SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.