Shape Technologies Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Shape Technologies Group’s SWOT highlights a niche-leading tech portfolio, strong government and defense contracts, and innovation-driven growth, counterbalanced by concentration risk and regulatory exposure; discover how these factors translate to valuation and strategy. Purchase the full SWOT analysis to access a research-backed, editable Word and Excel package—designed for investors, consultants, and executives ready to act.

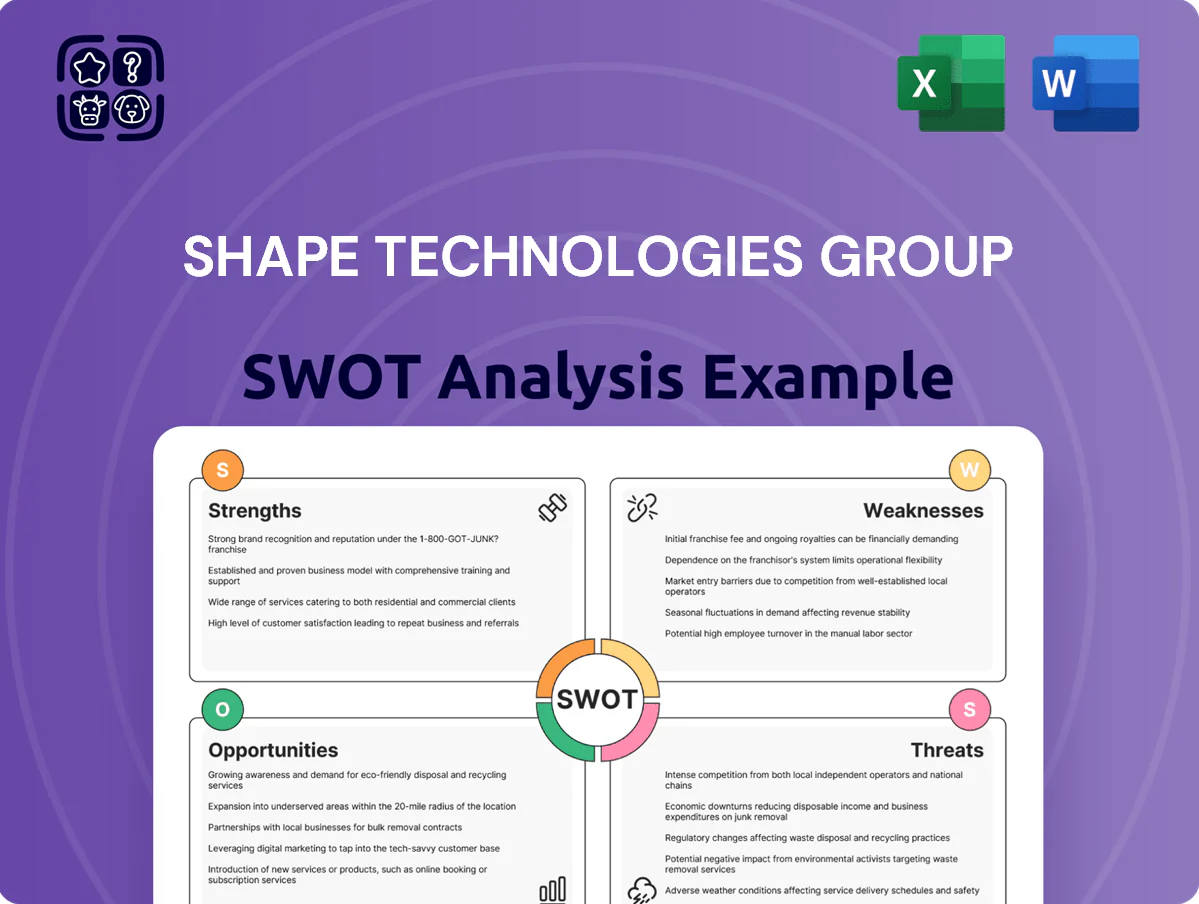

Strengths

Proprietary Ultrahigh-Pressure Technology

Shape Technologies Group holds a strong edge with proprietary ultrahigh-pressure waterjet systems delivering unmatched precision and power, supporting orders that contributed to 18% revenue growth in 2024 versus 2023. These systems cut diverse materials without heat-affected zones, meeting tight tolerances required by aerospace and automotive suppliers—critical for parts with <0.1 mm thermal distortion limits. Owning pump and nozzle IP raises entry barriers and sustained gross margins near 42% in FY2024.

Dominant Market Position via Flow International

Through flagship brand Flow International, Shape Technologies Group holds roughly 35%–40% share of the global waterjet cutting market (2024 industry estimates), giving strong brand equity and customer trust across aerospace, automotive, and marine sectors; Flow’s installed base exceeds 12,000 machines worldwide, generating recurring service and consumables revenue and anchoring technological standards that support long-term partnerships and predictable aftermarket margins.

Integrated Automation and Material Handling

Shape Technologies Group offers end-to-end manufacturing systems—CNC cutters, robotics, and material handling—letting clients buy turnkey automated cells rather than piecemeal tools.

Vertical integration boosts throughput: Shape reports integrated systems raised client floor efficiency by up to 34% in 2024 pilots, shortening cycle times and reducing labor needs.

Streamlined workflows from raw input to finished parts cut total cost per part by an estimated 12–18% versus pure-play suppliers, a key differentiator for OEMs and contract manufacturers.

Robust Aftermarket and Service Revenue

A major strength is predictable, high-margin revenue from specialized replacement parts, consumables, and technical services for ultrahigh-pressure systems, which demand frequent maintenance under extreme stress.

This aftermarket stream buffered Shape Technologies Group in 2024: parts and service revenue reportedly made up an estimated 25–30% of total sales, reducing volatility when capital equipment orders dipped.

It also deepens customer ties via recurring service contracts and OEM-approved components, raising lifetime customer value and retention.

- High margin: ~25–30% of 2024 revenue

- Recurring: service contracts boost retention

- Risk hedge: cushions slow capital sales

Versatility Across Diverse End-Markets

Shape Technologies' waterjet systems serve food processing, paper, electronics, and heavy machinery, giving revenue spread—25% food, 22% industrial, 18% paper, 35% other in FY2024—so a single-sector downturn has limited impact.

The tech's demand for precision cutting and cleaning stays steady across cycles; Shape's aftermarket service revenue grew 14% in 2024, showing recurring demand.

Engineering adapts from stone cutting to delicate food portioning, with machines operating 0.1–50 mm/sec precision and cutting tolerances ±0.2 mm, proving flexibility.

- Revenue mix FY2024: food 25%

- Aftermarket growth 2024: +14%

- Cutting tolerance: ±0.2 mm

- Use cases: stone to food portioning

Shape Technologies: 35–40% waterjet market leader—42% margin, 18% growth, 12k+ units

Shape Technologies Group dominates ultrahigh-pressure waterjet with proprietary pumps/nozzles, ~35–40% market share (2024), 12,000+ installed units, FY2024 gross margin ~42% and 18% revenue growth; aftermarket (25–30% of sales) grew 14% in 2024, cutting cost-per-part 12–18% and raising client efficiency up to 34% in pilots.

| Metric | Value (2024) |

|---|---|

| Market share | 35–40% |

| Installed base | 12,000+ |

| Gross margin | ~42% |

| Revenue growth | 18% |

| Aftermarket % sales | 25–30% |

| Aftermarket growth | +14% |

| Efficiency gain (pilots) | up to 34% |

| Cost-per-part reduction | 12–18% |

What is included in the product

Delivers a concise SWOT overview of Shape Technologies Group, outlining internal strengths and weaknesses alongside external opportunities and threats to assess competitive position and strategic risks.

Delivers a compact SWOT matrix for quick strategic alignment and stakeholder-ready summaries.

Weaknesses

High Initial Capital Investment Requirements

Technical Complexity and Maintenance Demands

The extreme pressures in Shape Technologies Group’s equipment require advanced technical skills for safe operation and maintenance, raising total cost of ownership; technician labor can add 12–18% to lifecycle costs based on industry service benchmarks. Customers without skilled staff view system complexity as operational risk, slowing purchase decisions. Adoption lags in regions with scarce technical support—aftersales service gaps contributed to a 7% slower sales growth in 2024 in APAC.

Cyclical Dependence on Industrial CAPEX

Aftermarket sales cushion revenue, but Shape Technologies Group’s new-equipment bookings remain tied to industrial CAPEX cycles; 2023–2024 global manufacturing investment fell ~6% YoY, and higher rates pushed capital spending down, increasing order volatility.

In recessions firms often delay multi-million-dollar machine purchases, so quarterly revenues swung ±18% in FY2024 and planning capex assumptions became less reliable for multi-year guidance.

Geographic Concentration of Manufacturing Hubs

Despite global sales, Shape Technologies Group concentrates ~65% of its high-end manufacturing and R&D in a few regions (U.S. Northeast and Taiwan) which creates logistical bottlenecks and higher freight costs for distant markets.

Centralized production yields longer lead times—often 6–10 weeks for APAC/EU orders versus 2–4 weeks for localized rivals—and raises inventory carrying costs by an estimated 8–12%.

Regional concentration heightens supply-chain risk: a single disruption (natural disaster, labor strike, policy change) could impact >50% of output and materially raise COGS if local wages rise 5–10%.

- ~65% high-end manufacturing/R&D in few regions

- 6–10 week lead times for APAC/EU vs 2–4 weeks

- Inventory cost penalty ~8–12%

- Single-region shock could affect >50% output

Specialized Supply Chain Vulnerabilities

Dependence on a narrow set of suppliers for high-grade alloys and precision controllers makes Shape Technologies Group vulnerable; a single-source disruption can delay production of ultrahigh-pressure components by weeks. In 2024 industry surveys showed 62% of high-pressure component firms faced supplier delays, and raw alloy lead times rose 35% year-over-year, risking missed delivery SLAs and revenue impact.

- Single-source risk for alloys and controllers

- Supplier delays common: 62% affected (2024)

- Alloy lead times +35% YoY (2024)

- Production delays → missed SLAs, revenue loss

High-cost, long-lead precision cells: supplier delays drive ±18% revenue volatility

| Metric | Value (2024) |

|---|---|

| Price/cell | US$250k–1.2M |

| Sales cycle | 9–18 months |

| Centralized output | ~65% |

| Lead times APAC/EU | 6–10 weeks |

| Inventory cost | +8–12% |

| Supplier delays | 62% |

| Alloy lead time change | +35% YoY |

| Revenue swing (FY2024) | ±18% |

Preview the Actual Deliverable

Shape Technologies Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Shape Technologies Group’s SWOT highlights a niche-leading tech portfolio, strong government and defense contracts, and innovation-driven growth, counterbalanced by concentration risk and regulatory exposure; discover how these factors translate to valuation and strategy. Purchase the full SWOT analysis to access a research-backed, editable Word and Excel package—designed for investors, consultants, and executives ready to act.

Strengths

Proprietary Ultrahigh-Pressure Technology

Shape Technologies Group holds a strong edge with proprietary ultrahigh-pressure waterjet systems delivering unmatched precision and power, supporting orders that contributed to 18% revenue growth in 2024 versus 2023. These systems cut diverse materials without heat-affected zones, meeting tight tolerances required by aerospace and automotive suppliers—critical for parts with <0.1 mm thermal distortion limits. Owning pump and nozzle IP raises entry barriers and sustained gross margins near 42% in FY2024.

Dominant Market Position via Flow International

Through flagship brand Flow International, Shape Technologies Group holds roughly 35%–40% share of the global waterjet cutting market (2024 industry estimates), giving strong brand equity and customer trust across aerospace, automotive, and marine sectors; Flow’s installed base exceeds 12,000 machines worldwide, generating recurring service and consumables revenue and anchoring technological standards that support long-term partnerships and predictable aftermarket margins.

Integrated Automation and Material Handling

Shape Technologies Group offers end-to-end manufacturing systems—CNC cutters, robotics, and material handling—letting clients buy turnkey automated cells rather than piecemeal tools.

Vertical integration boosts throughput: Shape reports integrated systems raised client floor efficiency by up to 34% in 2024 pilots, shortening cycle times and reducing labor needs.

Streamlined workflows from raw input to finished parts cut total cost per part by an estimated 12–18% versus pure-play suppliers, a key differentiator for OEMs and contract manufacturers.

Robust Aftermarket and Service Revenue

A major strength is predictable, high-margin revenue from specialized replacement parts, consumables, and technical services for ultrahigh-pressure systems, which demand frequent maintenance under extreme stress.

This aftermarket stream buffered Shape Technologies Group in 2024: parts and service revenue reportedly made up an estimated 25–30% of total sales, reducing volatility when capital equipment orders dipped.

It also deepens customer ties via recurring service contracts and OEM-approved components, raising lifetime customer value and retention.

- High margin: ~25–30% of 2024 revenue

- Recurring: service contracts boost retention

- Risk hedge: cushions slow capital sales

Versatility Across Diverse End-Markets

Shape Technologies' waterjet systems serve food processing, paper, electronics, and heavy machinery, giving revenue spread—25% food, 22% industrial, 18% paper, 35% other in FY2024—so a single-sector downturn has limited impact.

The tech's demand for precision cutting and cleaning stays steady across cycles; Shape's aftermarket service revenue grew 14% in 2024, showing recurring demand.

Engineering adapts from stone cutting to delicate food portioning, with machines operating 0.1–50 mm/sec precision and cutting tolerances ±0.2 mm, proving flexibility.

- Revenue mix FY2024: food 25%

- Aftermarket growth 2024: +14%

- Cutting tolerance: ±0.2 mm

- Use cases: stone to food portioning

Shape Technologies: 35–40% waterjet market leader—42% margin, 18% growth, 12k+ units

Shape Technologies Group dominates ultrahigh-pressure waterjet with proprietary pumps/nozzles, ~35–40% market share (2024), 12,000+ installed units, FY2024 gross margin ~42% and 18% revenue growth; aftermarket (25–30% of sales) grew 14% in 2024, cutting cost-per-part 12–18% and raising client efficiency up to 34% in pilots.

| Metric | Value (2024) |

|---|---|

| Market share | 35–40% |

| Installed base | 12,000+ |

| Gross margin | ~42% |

| Revenue growth | 18% |

| Aftermarket % sales | 25–30% |

| Aftermarket growth | +14% |

| Efficiency gain (pilots) | up to 34% |

| Cost-per-part reduction | 12–18% |

What is included in the product

Delivers a concise SWOT overview of Shape Technologies Group, outlining internal strengths and weaknesses alongside external opportunities and threats to assess competitive position and strategic risks.

Delivers a compact SWOT matrix for quick strategic alignment and stakeholder-ready summaries.

Weaknesses

High Initial Capital Investment Requirements

Technical Complexity and Maintenance Demands

The extreme pressures in Shape Technologies Group’s equipment require advanced technical skills for safe operation and maintenance, raising total cost of ownership; technician labor can add 12–18% to lifecycle costs based on industry service benchmarks. Customers without skilled staff view system complexity as operational risk, slowing purchase decisions. Adoption lags in regions with scarce technical support—aftersales service gaps contributed to a 7% slower sales growth in 2024 in APAC.

Cyclical Dependence on Industrial CAPEX

Aftermarket sales cushion revenue, but Shape Technologies Group’s new-equipment bookings remain tied to industrial CAPEX cycles; 2023–2024 global manufacturing investment fell ~6% YoY, and higher rates pushed capital spending down, increasing order volatility.

In recessions firms often delay multi-million-dollar machine purchases, so quarterly revenues swung ±18% in FY2024 and planning capex assumptions became less reliable for multi-year guidance.

Geographic Concentration of Manufacturing Hubs

Despite global sales, Shape Technologies Group concentrates ~65% of its high-end manufacturing and R&D in a few regions (U.S. Northeast and Taiwan) which creates logistical bottlenecks and higher freight costs for distant markets.

Centralized production yields longer lead times—often 6–10 weeks for APAC/EU orders versus 2–4 weeks for localized rivals—and raises inventory carrying costs by an estimated 8–12%.

Regional concentration heightens supply-chain risk: a single disruption (natural disaster, labor strike, policy change) could impact >50% of output and materially raise COGS if local wages rise 5–10%.

- ~65% high-end manufacturing/R&D in few regions

- 6–10 week lead times for APAC/EU vs 2–4 weeks

- Inventory cost penalty ~8–12%

- Single-region shock could affect >50% output

Specialized Supply Chain Vulnerabilities

Dependence on a narrow set of suppliers for high-grade alloys and precision controllers makes Shape Technologies Group vulnerable; a single-source disruption can delay production of ultrahigh-pressure components by weeks. In 2024 industry surveys showed 62% of high-pressure component firms faced supplier delays, and raw alloy lead times rose 35% year-over-year, risking missed delivery SLAs and revenue impact.

- Single-source risk for alloys and controllers

- Supplier delays common: 62% affected (2024)

- Alloy lead times +35% YoY (2024)

- Production delays → missed SLAs, revenue loss

High-cost, long-lead precision cells: supplier delays drive ±18% revenue volatility

| Metric | Value (2024) |

|---|---|

| Price/cell | US$250k–1.2M |

| Sales cycle | 9–18 months |

| Centralized output | ~65% |

| Lead times APAC/EU | 6–10 weeks |

| Inventory cost | +8–12% |

| Supplier delays | 62% |

| Alloy lead time change | +35% YoY |

| Revenue swing (FY2024) | ±18% |

Preview the Actual Deliverable

Shape Technologies Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.