Shell Plc Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

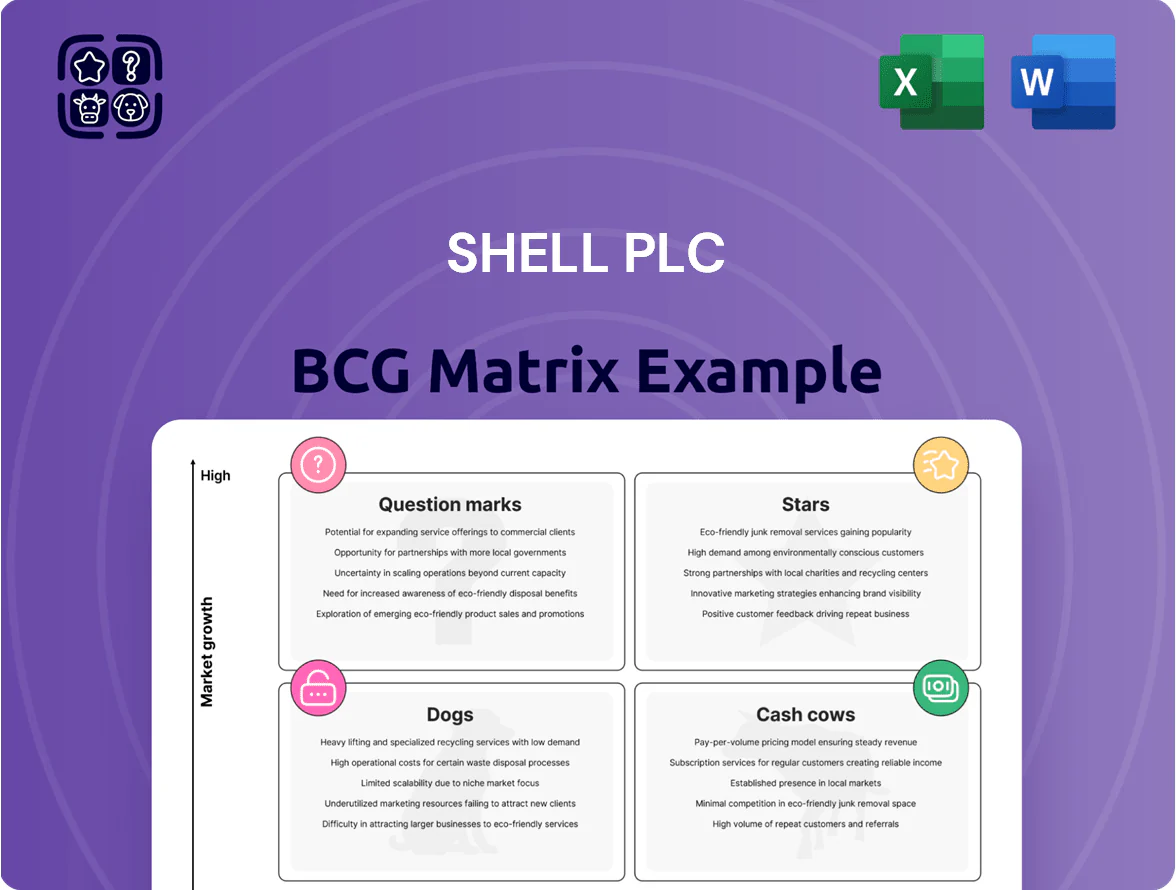

Shell Plc’s BCG Matrix snapshot shows a diversified portfolio balancing high-growth energy transition bets (Question Marks) with legacy upstream and downstream businesses that still generate strong cash flow (Cash Cows); a few lower-growth assets may sit in the Dogs quadrant as the company reallocates capital toward renewables and low-carbon solutions. This preview highlights strategic tension between maintaining dividend-supporting cash generators and investing in future Stars. Dive deeper into the full BCG Matrix to see quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide smarter capital allocation—purchase now for instant access.

Stars

Liquefied Natural Gas LNG Expansion

Shell Plc holds roughly 12% of global LNG market share in 2025, positioning liquefied natural gas (LNG) as a Star: high growth, high share in the BCG matrix.

Asian and European demand—China, Japan, South Korea, and EU imports up ~8% YoY in 2024—drives strong revenue; Shell reported LNG sales of $18.4 billion in 2024.

Shell is investing $6–8 billion through 2026 to add liquefaction capacity and FIDs, defending its lead against QatarEnergy and new U.S. exporters.

Electric Vehicle Charging Network

Shell Recharge, Shell Plc’s EV charging arm, has grown to ~100,000 charge points worldwide by end-2025, making it one of the largest global networks and supporting Shell’s push into mobility.

With ICE bans nearing in the EU (2035) and parts of the US states (2035–2040), the EV charging market is high-growth but capital intensive; Shell plans multibillion-dollar investment—Shell reported £2.5bn allocated to low-carbon mobility 2024–2026—to secure prime sites.

Shell treats Recharge as a strategic priority to capture shifting mobility share; target: scale utilization and network density to meet rising EV adoption, estimated global EV stock of 45m vehicles in 2025, so market share gains drive long-term fuel-replacement revenue.

Sustainable Aviation Fuel SAF

Shell Plc has positioned itself as a leader in bio-based Sustainable Aviation Fuel (SAF), aiming for 2.5 Mtpa SAF capacity by 2030 after its 2024 Neste JV and Rotterdam upgrades, capturing early-market share in a nascent, high-growth segment.

EU and US mandates—EU ReFuelEU Aviation (2025 blending targets) and California CFS—push airlines toward SAF, creating projected market demand of ~7–10 Mtpa by 2030, supporting premium margins vs jet A1.

Shell leverages existing refinery assets and €2.5–3.0 billion planned capex (2024–2030) to co-process and dedicated produce HEFA and alcohol-to-jet SAF, shifting cash from lower-margin fuels into higher-value renewables.

Integrated Power and Renewable Energy

Shell’s Integrated Power and Renewable Energy is a Star: since 2020 Shell added ~11 GW of renewables (solar/wind) and in 2024 had >3 TWh of power trading volume, showing rapid market share gains in green electrons.

High competition and capital intensity: the unit burned several hundred million dollars annually for scaling (Shell reported ~$0.8bn renewables capex in 2024), but integration of generation with trading and retail gives Shell a pricing and dispatch edge for its net-zero 2050 plan.

- Installed capacity growth: ~11 GW since 2020

- 2024 power trading: >3 TWh

- 2024 renewables capex: ~$0.8bn

- Strategic edge: integrated generation + trading

Convenience Retail in Emerging Markets

Shell’s convenience retail in India, China, and Southeast Asia is a Star: non-fuel retail grew ~18% CAGR 2020–2024, driven by rising consumer spend and demand for premium convenience hubs.

By bundling retail with fuel delivery, Shell captures leading share—roughly 25%+ in targeted urban forecourt markets—and saw retail margin contribution rise to ~12% of regional downstream profit in 2024.

- 18% CAGR non-fuel retail (2020–2024)

- 25%+ market share in urban forecourts

- Retail = ~12% of regional downstream profit (2024)

Shell’s Growth Engines: LNG, EV Charging, SAF & Renewables—High Capex, Big Targets

Shell’s Stars: LNG (12% global share, $18.4bn sales 2024, $6–8bn capex to 2026); EV charging (≈100,000 points end‑2025, £2.5bn low‑carbon mobility 2024–26); SAF (target 2.5 Mtpa by 2030, €2.5–3.0bn capex 2024–30); Renewables/Power (≈11 GW added since 2020, >3 TWh trading 2024, ~$0.8bn capex 2024).

| Business | 2024/25 | Capex/Target |

|---|---|---|

| LNG | 12% share; $18.4bn | $6–8bn to 2026 |

| EV Charging | ~100,000 points | £2.5bn 2024–26 |

| SAF | —; target 2.5 Mtpa by 2030 | €2.5–3.0bn |

| Renewables | +11 GW since 2020; >3 TWh | ~$0.8bn (2024) |

What is included in the product

BCG Matrix for Shell Plc: categorizes upstream renewables as Stars, downstream fuels as Cash Cows, new low‑carbon bets as Question Marks, and legacy noncore assets as Dogs.

One-page BCG matrix mapping Shell business units to quadrants for clear portfolio decisions and C-level presentations.

Cash Cows

Deepwater Oil Production

Shell’s deepwater operations in the Gulf of Mexico and Brazil produced about 650 kb/d (thousand barrels per day) in 2024, generating roughly $12–14 billion EBITDA annually due to low operating costs near $15–20/boe (barrel of oil equivalent).

These mature fields hold high market share, need little marketing spend versus renewables, and their free cash flow—around $8–10 billion in 2024—funds Shell’s energy transition capex and dividends.

Global Lubricants Leadership

Shell Plc has led global lubricants for ~20 years, holding roughly 12–14% market share in a mature $40bn lubricants market (2024 estimate), classifying it as a Cash Cow.

The unit posts high EBIT margins near 18% (2024 segment data) and low capex intensity (~2% of revenue), needing little investment to sustain share.

It generates stable free cash flow—about $1.2bn annually (2024)—helping cover corporate interest expense and support debt service.

Conventional Upstream Portfolio

Shell Plc’s conventional upstream portfolio—mature oil and gas units in stable jurisdictions—generates roughly $12–15 billion EBITDA annually (2024 guidance range), supplying strong free cash flow despite low growth prospects.

With improved recovery rates and digitalized reservoir management, lifting costs fell to about $8–12/boe in 2024, so Shell extracts value efficiently from declining volumes.

Management is milking these cash cows to fund low-carbon investments; Shell allocated $3.5 billion to renewables and hydrogen development in 2024 capex guidance.

Strategic Refining Hubs

Shell’s Strategic Refining Hubs consolidate refining into high-margin energy and chemical parks, boosting EBITDA margins; Shell Chemicals reported adjusted EBITDA of $6.3bn in 2024, reflecting integrations that lift returns.

These mature sites serve stable industrial markets, run at >90% utilization on average, and deliver predictable free cash flow used for dividends and low-carbon investments.

Integrated logistics and supply-chain efficiencies cut operating costs and inventory days, supporting steady cash generation and portfolio resilience.

- High-margin hubs drove Shell Chemicals adjusted EBITDA $6.3bn (2024)

- Typical utilization >90%

- Reliable free cash flow funds dividends and capex

- Integrated logistics reduce operating costs and inventory days

Global Brand Licensing and Marketing

The Shell brand drives high-margin licensing and fuel marketing deals across 70+ countries, contributing steady revenue despite low growth in traditional fuel retailing; Shell's downstream brand royalties and marketing fees represented roughly $2.1 billion in 2024, offering low-risk cash flows with minimal capex.

The segment holds strong market share in key markets (top-3 retail share in UK, Netherlands, Malaysia) while retail fuel volume growth was flat to -1% in 2024, making it a classic BCG Cash Cow: high share, low growth, high margin.

- 70+ countries presence

- ~$2.1B brand/license revenue (2024)

- Top-3 retail share in several markets

- Fuel retail volume growth ~0% to -1% (2024)

- High margins, low capex

Shell’s cash cows drove $22–26B EBITDA and ~$10–12B FCF in 2024, funding low‑carbon capex

Shell’s cash cows—conventional upstream, deepwater, lubricants, refining hubs, and brand/licensing—generated ~ $22–26bn EBITDA and ~$10–12bn free cash flow in 2024, with lifting costs $8–20/boe, lubricants share 12–14%, chemicals adj. EBITDA $6.3bn, brand/license ~$2.1bn, and >90% refinery utilization; proceeds fund $3.5bn 2024 low‑carbon capex and dividends.

| Asset | 2024 key |

|---|---|

| Upstream | $12–15bn EBITDA |

| Deepwater | 650 kb/d, $12–14bn EBITDA |

| Lubricants | 12–14% share, $1.2bn FCF |

| Chemicals | $6.3bn adj. EBITDA |

| Brand | $2.1bn revenue |

What You’re Viewing Is Included

Shell Plc BCG Matrix

The file you're previewing on this page is the final Shell Plc BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Shell Plc’s BCG Matrix snapshot shows a diversified portfolio balancing high-growth energy transition bets (Question Marks) with legacy upstream and downstream businesses that still generate strong cash flow (Cash Cows); a few lower-growth assets may sit in the Dogs quadrant as the company reallocates capital toward renewables and low-carbon solutions. This preview highlights strategic tension between maintaining dividend-supporting cash generators and investing in future Stars. Dive deeper into the full BCG Matrix to see quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide smarter capital allocation—purchase now for instant access.

Stars

Liquefied Natural Gas LNG Expansion

Shell Plc holds roughly 12% of global LNG market share in 2025, positioning liquefied natural gas (LNG) as a Star: high growth, high share in the BCG matrix.

Asian and European demand—China, Japan, South Korea, and EU imports up ~8% YoY in 2024—drives strong revenue; Shell reported LNG sales of $18.4 billion in 2024.

Shell is investing $6–8 billion through 2026 to add liquefaction capacity and FIDs, defending its lead against QatarEnergy and new U.S. exporters.

Electric Vehicle Charging Network

Shell Recharge, Shell Plc’s EV charging arm, has grown to ~100,000 charge points worldwide by end-2025, making it one of the largest global networks and supporting Shell’s push into mobility.

With ICE bans nearing in the EU (2035) and parts of the US states (2035–2040), the EV charging market is high-growth but capital intensive; Shell plans multibillion-dollar investment—Shell reported £2.5bn allocated to low-carbon mobility 2024–2026—to secure prime sites.

Shell treats Recharge as a strategic priority to capture shifting mobility share; target: scale utilization and network density to meet rising EV adoption, estimated global EV stock of 45m vehicles in 2025, so market share gains drive long-term fuel-replacement revenue.

Sustainable Aviation Fuel SAF

Shell Plc has positioned itself as a leader in bio-based Sustainable Aviation Fuel (SAF), aiming for 2.5 Mtpa SAF capacity by 2030 after its 2024 Neste JV and Rotterdam upgrades, capturing early-market share in a nascent, high-growth segment.

EU and US mandates—EU ReFuelEU Aviation (2025 blending targets) and California CFS—push airlines toward SAF, creating projected market demand of ~7–10 Mtpa by 2030, supporting premium margins vs jet A1.

Shell leverages existing refinery assets and €2.5–3.0 billion planned capex (2024–2030) to co-process and dedicated produce HEFA and alcohol-to-jet SAF, shifting cash from lower-margin fuels into higher-value renewables.

Integrated Power and Renewable Energy

Shell’s Integrated Power and Renewable Energy is a Star: since 2020 Shell added ~11 GW of renewables (solar/wind) and in 2024 had >3 TWh of power trading volume, showing rapid market share gains in green electrons.

High competition and capital intensity: the unit burned several hundred million dollars annually for scaling (Shell reported ~$0.8bn renewables capex in 2024), but integration of generation with trading and retail gives Shell a pricing and dispatch edge for its net-zero 2050 plan.

- Installed capacity growth: ~11 GW since 2020

- 2024 power trading: >3 TWh

- 2024 renewables capex: ~$0.8bn

- Strategic edge: integrated generation + trading

Convenience Retail in Emerging Markets

Shell’s convenience retail in India, China, and Southeast Asia is a Star: non-fuel retail grew ~18% CAGR 2020–2024, driven by rising consumer spend and demand for premium convenience hubs.

By bundling retail with fuel delivery, Shell captures leading share—roughly 25%+ in targeted urban forecourt markets—and saw retail margin contribution rise to ~12% of regional downstream profit in 2024.

- 18% CAGR non-fuel retail (2020–2024)

- 25%+ market share in urban forecourts

- Retail = ~12% of regional downstream profit (2024)

Shell’s Growth Engines: LNG, EV Charging, SAF & Renewables—High Capex, Big Targets

Shell’s Stars: LNG (12% global share, $18.4bn sales 2024, $6–8bn capex to 2026); EV charging (≈100,000 points end‑2025, £2.5bn low‑carbon mobility 2024–26); SAF (target 2.5 Mtpa by 2030, €2.5–3.0bn capex 2024–30); Renewables/Power (≈11 GW added since 2020, >3 TWh trading 2024, ~$0.8bn capex 2024).

| Business | 2024/25 | Capex/Target |

|---|---|---|

| LNG | 12% share; $18.4bn | $6–8bn to 2026 |

| EV Charging | ~100,000 points | £2.5bn 2024–26 |

| SAF | —; target 2.5 Mtpa by 2030 | €2.5–3.0bn |

| Renewables | +11 GW since 2020; >3 TWh | ~$0.8bn (2024) |

What is included in the product

BCG Matrix for Shell Plc: categorizes upstream renewables as Stars, downstream fuels as Cash Cows, new low‑carbon bets as Question Marks, and legacy noncore assets as Dogs.

One-page BCG matrix mapping Shell business units to quadrants for clear portfolio decisions and C-level presentations.

Cash Cows

Deepwater Oil Production

Shell’s deepwater operations in the Gulf of Mexico and Brazil produced about 650 kb/d (thousand barrels per day) in 2024, generating roughly $12–14 billion EBITDA annually due to low operating costs near $15–20/boe (barrel of oil equivalent).

These mature fields hold high market share, need little marketing spend versus renewables, and their free cash flow—around $8–10 billion in 2024—funds Shell’s energy transition capex and dividends.

Global Lubricants Leadership

Shell Plc has led global lubricants for ~20 years, holding roughly 12–14% market share in a mature $40bn lubricants market (2024 estimate), classifying it as a Cash Cow.

The unit posts high EBIT margins near 18% (2024 segment data) and low capex intensity (~2% of revenue), needing little investment to sustain share.

It generates stable free cash flow—about $1.2bn annually (2024)—helping cover corporate interest expense and support debt service.

Conventional Upstream Portfolio

Shell Plc’s conventional upstream portfolio—mature oil and gas units in stable jurisdictions—generates roughly $12–15 billion EBITDA annually (2024 guidance range), supplying strong free cash flow despite low growth prospects.

With improved recovery rates and digitalized reservoir management, lifting costs fell to about $8–12/boe in 2024, so Shell extracts value efficiently from declining volumes.

Management is milking these cash cows to fund low-carbon investments; Shell allocated $3.5 billion to renewables and hydrogen development in 2024 capex guidance.

Strategic Refining Hubs

Shell’s Strategic Refining Hubs consolidate refining into high-margin energy and chemical parks, boosting EBITDA margins; Shell Chemicals reported adjusted EBITDA of $6.3bn in 2024, reflecting integrations that lift returns.

These mature sites serve stable industrial markets, run at >90% utilization on average, and deliver predictable free cash flow used for dividends and low-carbon investments.

Integrated logistics and supply-chain efficiencies cut operating costs and inventory days, supporting steady cash generation and portfolio resilience.

- High-margin hubs drove Shell Chemicals adjusted EBITDA $6.3bn (2024)

- Typical utilization >90%

- Reliable free cash flow funds dividends and capex

- Integrated logistics reduce operating costs and inventory days

Global Brand Licensing and Marketing

The Shell brand drives high-margin licensing and fuel marketing deals across 70+ countries, contributing steady revenue despite low growth in traditional fuel retailing; Shell's downstream brand royalties and marketing fees represented roughly $2.1 billion in 2024, offering low-risk cash flows with minimal capex.

The segment holds strong market share in key markets (top-3 retail share in UK, Netherlands, Malaysia) while retail fuel volume growth was flat to -1% in 2024, making it a classic BCG Cash Cow: high share, low growth, high margin.

- 70+ countries presence

- ~$2.1B brand/license revenue (2024)

- Top-3 retail share in several markets

- Fuel retail volume growth ~0% to -1% (2024)

- High margins, low capex

Shell’s cash cows drove $22–26B EBITDA and ~$10–12B FCF in 2024, funding low‑carbon capex

Shell’s cash cows—conventional upstream, deepwater, lubricants, refining hubs, and brand/licensing—generated ~ $22–26bn EBITDA and ~$10–12bn free cash flow in 2024, with lifting costs $8–20/boe, lubricants share 12–14%, chemicals adj. EBITDA $6.3bn, brand/license ~$2.1bn, and >90% refinery utilization; proceeds fund $3.5bn 2024 low‑carbon capex and dividends.

| Asset | 2024 key |

|---|---|

| Upstream | $12–15bn EBITDA |

| Deepwater | 650 kb/d, $12–14bn EBITDA |

| Lubricants | 12–14% share, $1.2bn FCF |

| Chemicals | $6.3bn adj. EBITDA |

| Brand | $2.1bn revenue |

What You’re Viewing Is Included

Shell Plc BCG Matrix

The file you're previewing on this page is the final Shell Plc BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.