Shell Plc Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

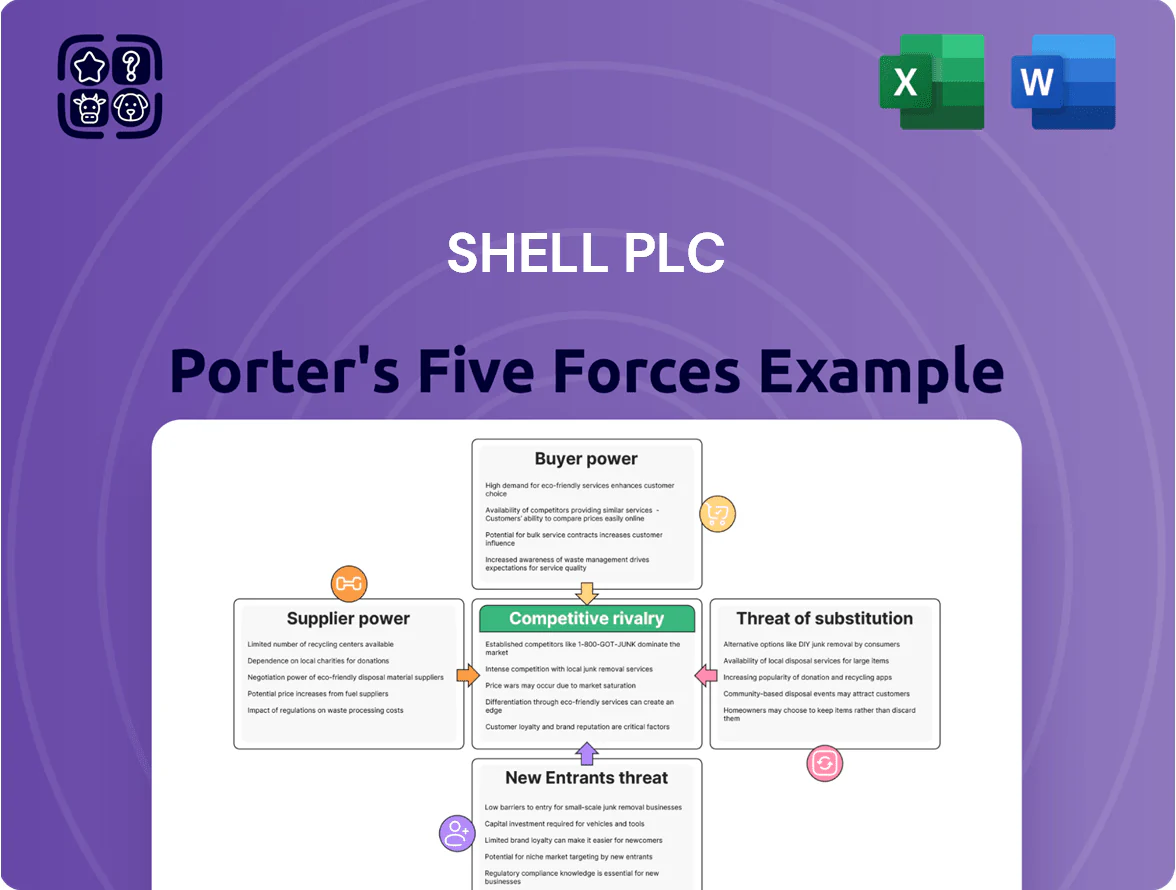

Shell Plc faces intense rivalry from integrated majors and NOCs, moderate supplier power mitigated by scale, growing buyer scrutiny on pricing and ESG, rising substitute threats from renewables and electrification, and high barriers deterring new entrants; this snapshot highlights strategic pressure points and resilience gaps that matter for investors and strategists—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Geopolitical Influence of OPEC Plus

The global crude supply remains driven by OPEC+ production quotas, with member states holding roughly 48% of proven reserves and controlling ~40% of daily output as of 2025; Shell therefore functions as a price taker in the commodities market. These state-led decisions set baseline feedstock costs that directly affect Shell’s refining margins and trading P&L, where crude accounts for ~60–70% of feedstock expense. By end-2025, coordinated cuts or increases shifted Brent prices by ±15–25% intra-year, forcing Shell to adjust hedges and trading positions.

Specialized Oilfield Service Providers

Specialized oilfield service firms concentrate technical know-how for deepwater drilling and carbon capture, and just five global players supplied over 60% of high-spec deepwater services in 2024, giving them substantial leverage over Shell’s high-margin upstream projects.

Critical Minerals for Green Energy

As Shell scales renewable power and battery storage, a concentrated supplier base for lithium, cobalt and copper—with China controlling ~60% of refined lithium-ion cathode production and 50%+ of global copper refining in 2024—gives suppliers strong pricing and delivery leverage.

In 2024 lithium prices jumped ~45% YoY and copper premiums widened, raising Shell’s capex risk and potential project delays for transition infrastructure.

Highly Skilled Technical Workforce

The energy transition has tightened competition for engineers skilled in both petroleum systems and low-carbon tech; global oil & gas skilled labor fell ~8% between 2019–2023 while renewables employment rose 20% to 13.6 million jobs in 2023, boosting supplier (workforce) bargaining power.

Shell must raise retention and pay: in 2024 Shell increased training spend and targeted hiring, but to secure dual-track IP it likely needs salary premiums of 10–25% and multi-year retention bonuses.

- Skilled labor scarcity ↑ bargaining power

- Renewables jobs: 13.6M (2023)

- Oil & gas skilled labor −8% (2019–2023)

- Estimated pay premium needed: 10–25%

Midstream and Logistics Constraints

Shell depends on a global web of third-party pipelines, tankers, and terminals; in 2024 midstream fees rose ~8% in Europe and 6% in APAC, squeezing margins on refined products and fuels.

Limited alternatives in many markets let midstream operators impose high transit fees and tight contracts; Shell’s 2024 operating costs showed logistics-related uplift of ~$1.2bn vs 2023.

Dependence is worst in LNG: cryogenic ships are scarce—global FSRU and LNG carrier utilization hit ~92% in 2024—giving suppliers pricing power.

- 2024 logistics cost rise: ~$1.2bn

- Europe midstream fee rise: ~8% (2024)

- LNG carrier utilization: ~92% (2024)

Supply Power Plays: OPEC+, China & Few Firms Squeeze Energy Costs, Forcing 10–25% Pay Rises

Suppliers hold strong leverage: OPEC+ drives crude price swings (±15–25% intra‑2025), five service firms supply >60% deepwater tech (2024), China controls ~60% refined Li‑ion cathodes (2024), LNG carrier/FSRU utilization ~92% (2024), logistics cost rise ~$1.2bn (2024); Shell faces higher feedstock, capex and labor costs requiring 10–25% pay premiums.

| Metric | Value |

|---|---|

| OPEC+ output control | ~40% daily (2025) |

| Deepwater service concentration | >60% by 5 firms (2024) |

| China cathode share | ~60% (2024) |

| LNG utilization | ~92% (2024) |

| Logistics cost rise | ~$1.2bn (2024) |

| Estimated pay premium | 10–25% |

What is included in the product

Tailored exclusively for Shell Plc, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive forces shaping Shell's pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Shell Plc—quickly identify competitive pressures and strategic levers for boardroom decisions.

Customers Bargaining Power

Retail Price Sensitivity

Individual consumers at Shell’s global retail network show high price sensitivity and weak brand loyalty; surveys in 2024 found 62% of motorists switch stations for a price difference under $0.10/litre. By late 2025, price-comparison apps reached ~200 million users globally, enabling instant switching and pushing Shell to match local competitors’ prices within 24 hours. Shell spent $1.1bn on loyalty and retail promotions in 2024 to defend market share.

Corporate Decarbonization Requirements

Large industrial clients controlling ~40% of global corporate energy demand are pressing suppliers for low-carbon solutions to meet 2030–2050 net-zero targets, giving them strong price and contract leverage over Shell.

These high-volume buyers negotiate favorable terms for green hydrogen, biofuels, and renewable PPAs; corporate PPA volume hit a record 41 GW in 2023, strengthening buyer bargaining power.

If Shell cannot scale certified sustainable supply—green hydrogen target 1–2 MtH2/yr by 2030—clients can shift to specialist renewables, risking margin pressure and contract attrition.

Government Procurement and Regulation

National governments are major Shell Plc customers—public-sector energy contracts and infrastructure projects accounted for roughly 12% of global oil and gas procurement spend in 2024, giving states strong bargaining power.

They use procurement rules to require strict ESG (environmental, social, governance) standards; for example the EU Green Public Procurement criteria raised low-carbon fuel requirements by 30% in 2025 tenders.

This forces Shell to change product mixes and pricing; complying with carbon-intensity rules added an estimated $3–6 per barrel-equivalent in 2024 compliance costs for major suppliers.

Low Switching Costs in Power Markets

As Shell shifts into integrated power, low switching costs let residential and small-business customers churn rapidly, capping domestic electricity pricing power.

Digital platforms and price comparison sites—used by roughly 40% of UK household energy switchers in 2024—amplify moves to cheaper or greener suppliers, squeezing margins for large incumbents like Shell.

- ~40% UK household switch rate source: Ofgem 2024

- High churn lowers ability to raise prices

- Digitalization raises transparency and supplier mobility

Transparency in Global Commodity Trading

Wholesale buyers of crude, gas, and chemicals use real-time price feeds (Platts, ICE) and alternatives, so Shell struggles to earn premiums on standardized B2B products; Brent-Dubai spreads averaged about 0.45 USD/bbl in 2024, tightening arbitrage.

The commoditized supply lets buyers invite competitive bids from supermajors and NOCs—top 5 suppliers controlled ~45% of seaborne crude in 2024—lifting buyer leverage.

- Real-time pricing reduces pricing power

- Brent spread ~0.45 USD/bbl (2024)

- Top 5 suppliers ~45% seaborne crude (2024)

Price-savvy consumers, corporate PPAs and tight markets squeeze fuel margins

Customers hold strong bargaining power: price-sensitive retail motorists (62% switch < $0.10/l in 2024) and 200M price-app users by 2025 compress margins; large corporates (~40% of corporate energy demand) and record 41 GW PPAs (2023) demand low‑carbon supply; governments (12% of public procurement 2024) enforce ESG rules; commoditized wholesale markets (Brent spread $0.45/bbl 2024) further limit premiums.

| Metric | Value |

|---|---|

| Retail switch sensitivity | 62% (<$0.10/l) 2024 |

| Price-app users | ~200M by 2025 |

| Corporate energy share | ~40% |

| Corporate PPA volume | 41 GW 2023 |

| Govt procurement share | ~12% 2024 |

| Brent-Dubai spread | $0.45/bbl 2024 |

Same Document Delivered

Shell Plc Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shell Plc you'll receive immediately after purchase—no placeholders, fully formatted and ready to use; it assesses supplier and buyer power, rivalry, threat of substitutes, and entry barriers with actionable insights and concise conclusions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Shell Plc faces intense rivalry from integrated majors and NOCs, moderate supplier power mitigated by scale, growing buyer scrutiny on pricing and ESG, rising substitute threats from renewables and electrification, and high barriers deterring new entrants; this snapshot highlights strategic pressure points and resilience gaps that matter for investors and strategists—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Geopolitical Influence of OPEC Plus

The global crude supply remains driven by OPEC+ production quotas, with member states holding roughly 48% of proven reserves and controlling ~40% of daily output as of 2025; Shell therefore functions as a price taker in the commodities market. These state-led decisions set baseline feedstock costs that directly affect Shell’s refining margins and trading P&L, where crude accounts for ~60–70% of feedstock expense. By end-2025, coordinated cuts or increases shifted Brent prices by ±15–25% intra-year, forcing Shell to adjust hedges and trading positions.

Specialized Oilfield Service Providers

Specialized oilfield service firms concentrate technical know-how for deepwater drilling and carbon capture, and just five global players supplied over 60% of high-spec deepwater services in 2024, giving them substantial leverage over Shell’s high-margin upstream projects.

Critical Minerals for Green Energy

As Shell scales renewable power and battery storage, a concentrated supplier base for lithium, cobalt and copper—with China controlling ~60% of refined lithium-ion cathode production and 50%+ of global copper refining in 2024—gives suppliers strong pricing and delivery leverage.

In 2024 lithium prices jumped ~45% YoY and copper premiums widened, raising Shell’s capex risk and potential project delays for transition infrastructure.

Highly Skilled Technical Workforce

The energy transition has tightened competition for engineers skilled in both petroleum systems and low-carbon tech; global oil & gas skilled labor fell ~8% between 2019–2023 while renewables employment rose 20% to 13.6 million jobs in 2023, boosting supplier (workforce) bargaining power.

Shell must raise retention and pay: in 2024 Shell increased training spend and targeted hiring, but to secure dual-track IP it likely needs salary premiums of 10–25% and multi-year retention bonuses.

- Skilled labor scarcity ↑ bargaining power

- Renewables jobs: 13.6M (2023)

- Oil & gas skilled labor −8% (2019–2023)

- Estimated pay premium needed: 10–25%

Midstream and Logistics Constraints

Shell depends on a global web of third-party pipelines, tankers, and terminals; in 2024 midstream fees rose ~8% in Europe and 6% in APAC, squeezing margins on refined products and fuels.

Limited alternatives in many markets let midstream operators impose high transit fees and tight contracts; Shell’s 2024 operating costs showed logistics-related uplift of ~$1.2bn vs 2023.

Dependence is worst in LNG: cryogenic ships are scarce—global FSRU and LNG carrier utilization hit ~92% in 2024—giving suppliers pricing power.

- 2024 logistics cost rise: ~$1.2bn

- Europe midstream fee rise: ~8% (2024)

- LNG carrier utilization: ~92% (2024)

Supply Power Plays: OPEC+, China & Few Firms Squeeze Energy Costs, Forcing 10–25% Pay Rises

Suppliers hold strong leverage: OPEC+ drives crude price swings (±15–25% intra‑2025), five service firms supply >60% deepwater tech (2024), China controls ~60% refined Li‑ion cathodes (2024), LNG carrier/FSRU utilization ~92% (2024), logistics cost rise ~$1.2bn (2024); Shell faces higher feedstock, capex and labor costs requiring 10–25% pay premiums.

| Metric | Value |

|---|---|

| OPEC+ output control | ~40% daily (2025) |

| Deepwater service concentration | >60% by 5 firms (2024) |

| China cathode share | ~60% (2024) |

| LNG utilization | ~92% (2024) |

| Logistics cost rise | ~$1.2bn (2024) |

| Estimated pay premium | 10–25% |

What is included in the product

Tailored exclusively for Shell Plc, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive forces shaping Shell's pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Shell Plc—quickly identify competitive pressures and strategic levers for boardroom decisions.

Customers Bargaining Power

Retail Price Sensitivity

Individual consumers at Shell’s global retail network show high price sensitivity and weak brand loyalty; surveys in 2024 found 62% of motorists switch stations for a price difference under $0.10/litre. By late 2025, price-comparison apps reached ~200 million users globally, enabling instant switching and pushing Shell to match local competitors’ prices within 24 hours. Shell spent $1.1bn on loyalty and retail promotions in 2024 to defend market share.

Corporate Decarbonization Requirements

Large industrial clients controlling ~40% of global corporate energy demand are pressing suppliers for low-carbon solutions to meet 2030–2050 net-zero targets, giving them strong price and contract leverage over Shell.

These high-volume buyers negotiate favorable terms for green hydrogen, biofuels, and renewable PPAs; corporate PPA volume hit a record 41 GW in 2023, strengthening buyer bargaining power.

If Shell cannot scale certified sustainable supply—green hydrogen target 1–2 MtH2/yr by 2030—clients can shift to specialist renewables, risking margin pressure and contract attrition.

Government Procurement and Regulation

National governments are major Shell Plc customers—public-sector energy contracts and infrastructure projects accounted for roughly 12% of global oil and gas procurement spend in 2024, giving states strong bargaining power.

They use procurement rules to require strict ESG (environmental, social, governance) standards; for example the EU Green Public Procurement criteria raised low-carbon fuel requirements by 30% in 2025 tenders.

This forces Shell to change product mixes and pricing; complying with carbon-intensity rules added an estimated $3–6 per barrel-equivalent in 2024 compliance costs for major suppliers.

Low Switching Costs in Power Markets

As Shell shifts into integrated power, low switching costs let residential and small-business customers churn rapidly, capping domestic electricity pricing power.

Digital platforms and price comparison sites—used by roughly 40% of UK household energy switchers in 2024—amplify moves to cheaper or greener suppliers, squeezing margins for large incumbents like Shell.

- ~40% UK household switch rate source: Ofgem 2024

- High churn lowers ability to raise prices

- Digitalization raises transparency and supplier mobility

Transparency in Global Commodity Trading

Wholesale buyers of crude, gas, and chemicals use real-time price feeds (Platts, ICE) and alternatives, so Shell struggles to earn premiums on standardized B2B products; Brent-Dubai spreads averaged about 0.45 USD/bbl in 2024, tightening arbitrage.

The commoditized supply lets buyers invite competitive bids from supermajors and NOCs—top 5 suppliers controlled ~45% of seaborne crude in 2024—lifting buyer leverage.

- Real-time pricing reduces pricing power

- Brent spread ~0.45 USD/bbl (2024)

- Top 5 suppliers ~45% seaborne crude (2024)

Price-savvy consumers, corporate PPAs and tight markets squeeze fuel margins

Customers hold strong bargaining power: price-sensitive retail motorists (62% switch < $0.10/l in 2024) and 200M price-app users by 2025 compress margins; large corporates (~40% of corporate energy demand) and record 41 GW PPAs (2023) demand low‑carbon supply; governments (12% of public procurement 2024) enforce ESG rules; commoditized wholesale markets (Brent spread $0.45/bbl 2024) further limit premiums.

| Metric | Value |

|---|---|

| Retail switch sensitivity | 62% (<$0.10/l) 2024 |

| Price-app users | ~200M by 2025 |

| Corporate energy share | ~40% |

| Corporate PPA volume | 41 GW 2023 |

| Govt procurement share | ~12% 2024 |

| Brent-Dubai spread | $0.45/bbl 2024 |

Same Document Delivered

Shell Plc Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shell Plc you'll receive immediately after purchase—no placeholders, fully formatted and ready to use; it assesses supplier and buyer power, rivalry, threat of substitutes, and entry barriers with actionable insights and concise conclusions.