Jiangsu Eastern Shenghong Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

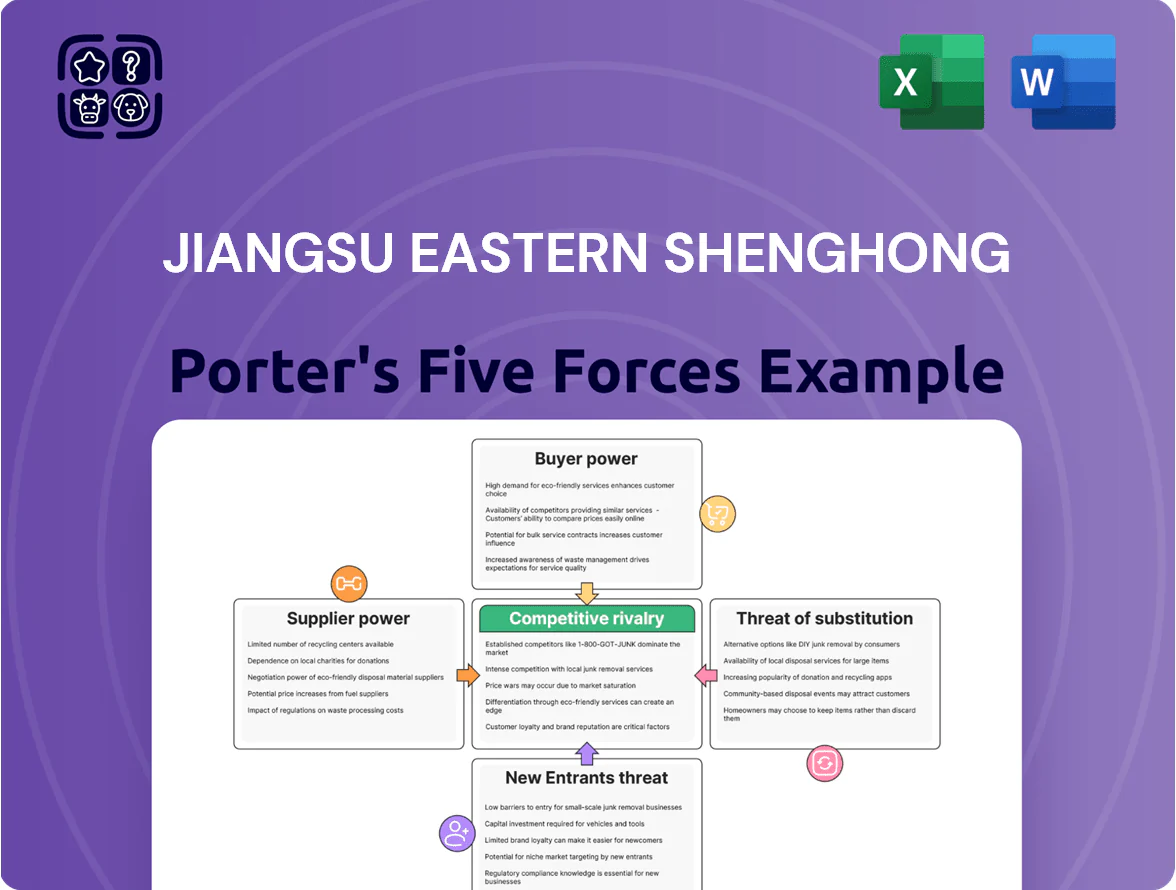

Jiangsu Eastern Shenghong faces moderate supplier power due to specialized petrochemical inputs, high rivalry from domestic refiners, and growing buyer sophistication that pressures margins; barriers to entry are substantial but technological shifts and environmental regulation heighten substitute risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Jiangsu Eastern Shenghong’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration and Feedstock Control

Eastern Shenghong has cut supplier power by building refinery and chemical chains that produced about 3.2 million tonnes of paraxylene and 2.1 million tonnes of ethylene capacity by 2024, giving internal feedstock for polyester and nylon and trimming external purchases.

Controlling upstream inputs lets the firm fix gross margins; in 2024 integrated units helped keep refining-to-petrochemical margins 12–18% above peers during volatile crude swings.

Dependence on Global Crude Oil Markets

Despite efficient in-house refining, Jiangsu Eastern Shenghong remains a price taker: international Brent and Shanghai crude benchmarks set feedstock costs—Brent averaged 86.5 USD/bbl in 2025 and Australian thermal coal delivered to China rose 14% YoY to 120 USD/ton in 2025, lifting landing costs.

Geopolitical shocks and OPEC+ cuts (2024–25 cuts removed ~1.2 mb/d capacity) pushed spot premiums, directly raising refinery margins volatility and CAPEX recovery timelines.

State-owned producers (CNPC, Sinopec) supply negotiating power, keeping raw-input pricing largely external to Shenghong’s internal efficiency gains.

Specialized Chemical Catalyst Providers

For high-end chemical fiber and EVA new-energy materials, Eastern Shenghong depends on a handful of global specialty catalyst suppliers—three firms supply ~70% of key high-performance catalysts, giving suppliers strong bargaining power due to proprietary tech and few substitutes.

These suppliers charge premiums: specialty catalyst margins often 25–35% and lead times 8–16 weeks, so Shenghong must keep strategic partnerships and long-term contracts to secure quality, stable supply, and R&D co-development.

Energy and Utility Infrastructure Requirements

Energy and Utility Infrastructure Requirements: Jiangsu Eastern Shenghong’s large-scale refining and polyester operations need vast electricity and industrial water, typically supplied by state-regulated utility monopolies in China, giving suppliers strong structural power.

The inputs are non-negotiable for continuous-flow manufacturing, so Shenghong reduces exposure by investing in cogeneration plants and energy-efficient tech, cutting external power demand by about 15% and saving roughly CNY 120 million annually (2024 estimate).

- State utility monopoly = high supplier power

- Electricity/water are essential, non-substitutable

- Onsite cogeneration reduces grid reliance ~15%

- Estimated annual savings ~CNY 120 million (2024)

Logistics and Supply Chain Reliability

The movement of bulk liquid chemicals and finished textiles relies on specialized ship, pipeline, and rail networks; industry-wide dependence on third-party international logistics gives providers moderate bargaining power over Jiangsu Eastern Shenghong.

Eastern Shenghong’s internal logistics reduces some exposure, but 2024 sea freight rates rose ~18% year‑over‑year and China coastal port congestion added 6–12% transit delays, so higher freight or bottlenecks can compress margins and force transport-efficiency measures.

- Third-party logistics = moderate leverage

- Eastern Shenghong has in-house logistics, lowering some risk

- 2024 sea freight +18% yoy; port delays 6–12%

- Higher freight squeezes margins, pushes efficiency moves

Shenghong boosts margins via 5.3Mt integration, but oil, OPEC+ and catalyst oligopoly bite

Supplier power is mixed: Shenghong’s 5.3 Mt integrated PX/ethylene capacity (2024) cuts feedstock buys and lifted refining-to-petro margins 12–18% vs peers, yet global Brent (86.5 USD/bbl 2025), OPEC+ cuts (~1.2 mb/d 2024–25), state-owned oil majors, 3 catalyst firms (≈70% share) and utility monopolies keep strong external pricing power.

| Metric | Value |

|---|---|

| Integrated PX/ethylene | 5.3 Mt (2024) |

| Margin uplift vs peers | +12–18% (2024) |

| Brent | 86.5 USD/bbl (2025) |

| OPEC+ cut impact | ~1.2 mb/d (2024–25) |

| Catalyst concentration | 3 firms ≈70% |

What is included in the product

Tailored exclusively for Jiangsu Eastern Shenghong, this Porter’s Five Forces overview uncovers key competitive drivers, supplier and buyer influence on pricing, entry barriers protecting incumbents, and disruptive substitutes or threats to market share.

Compact Five Forces snapshot for Jiangsu Eastern Shenghong—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to accelerate strategic decisions.

Customers Bargaining Power

Fragmentation of the Downstream Textile Industry

A significant share of Jiangsu Eastern Shenghong’s polyester and nylon sales goes to over 3,000 small‑to‑mid textile firms across China and Southeast Asia, so no single buyer can push prices down meaningfully.

That customer fragmentation, combined with Shenghong’s 2024 output of ~3.8 million tons of fibers and >85% on‑time delivery, sustains above‑market pricing in the traditional fiber segment.

Concentration in the Solar Material Segment

Jiangsu Eastern Shenghong sells EVA and related solar materials to a concentrated group of large module makers who account for about 60–70% of the company’s new-energy sales, buying in volumes >10,000 tons annually; these sophisticated buyers demand tight specs and drive down prices, raising customer bargaining power. The firm must invest in R&D—the company spent RMB 120 million on materials R&D in 2024—to stay ahead and reduce churn risk if clients switch to rivals.

Price Sensitivity to Commodity Cycles

Low Switching Costs for Standardized Products

For standard-grade chemical fibers, switching from Jiangsu Eastern Shenghong to peers like Hengli or Rongsheng is easy and cheap, keeping customer bargaining power high and forcing Eastern Shenghong to compete on supply-chain integration and service reliability.

To raise switching costs, Eastern Shenghong is partnering with brands on sustainable and recycled lines—by 2025 these tie-ups account for about 12% of specialty sales—requiring multi-year technical alignment and joint certification.

- Low switching cost vs Hengli/Rongsheng

- Focus: supply-chain integration, service reliability

- Sustainable/recycled lines ≈12% of specialty sales (2025)

- Long-term technical alignment raises lock-in

Impact of End-Consumer Demand Trends

Slower global consumer spending cuts retail orders; in 2023 global apparel spending fell ~2.5% year-on-year, and mills trimmed yarn purchases, shifting bargaining power to buyers with inventory choices.

Eastern Shenghong watches retail sales and PMI data monthly and cut output when apparel demand dips, avoiding blanket price concessions seen in 2022 when fabric prices dropped ~15%.

- Retail demand down 2.5% (2023)

- Fabric prices fell ~15% (2022 downturn)

- Monthly PMI monitoring

Mixed buyer power: small textile firms vs solar giants shape polyester pricing

Buyers are mixed: >3,000 small textile firms limit single‑buyer power for polyester, while large solar module makers (60–70% of new‑energy sales) concentrate bargaining for EVA, pushing prices down. Commodity fibers track PTA/MEG swings (PTA -18% YoY 2024) so buyer power is high; specialty fibers (ASP +15–25% in 2024) and 12% recycled/sustainable sales (2025) raise stickiness.

| Metric | 2024/2025 |

|---|---|

| Total fiber output | ~3.8M t (2024) |

| PTA change | -18% YoY (2024) |

| New‑energy buyer share | 60–70% |

| R&D spend | RMB 120M (2024) |

| Specialty ASP lift | +15–25% (2024) |

| Sustainable sales | ~12% specialty (2025) |

Same Document Delivered

Jiangsu Eastern Shenghong Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Jiangsu Eastern Shenghong you’ll receive immediately after purchase—no placeholders, fully formatted and ready for use.

The document displayed here is part of the final report and matches the downloadable file you’ll get upon payment, containing competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Jiangsu Eastern Shenghong faces moderate supplier power due to specialized petrochemical inputs, high rivalry from domestic refiners, and growing buyer sophistication that pressures margins; barriers to entry are substantial but technological shifts and environmental regulation heighten substitute risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Jiangsu Eastern Shenghong’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration and Feedstock Control

Eastern Shenghong has cut supplier power by building refinery and chemical chains that produced about 3.2 million tonnes of paraxylene and 2.1 million tonnes of ethylene capacity by 2024, giving internal feedstock for polyester and nylon and trimming external purchases.

Controlling upstream inputs lets the firm fix gross margins; in 2024 integrated units helped keep refining-to-petrochemical margins 12–18% above peers during volatile crude swings.

Dependence on Global Crude Oil Markets

Despite efficient in-house refining, Jiangsu Eastern Shenghong remains a price taker: international Brent and Shanghai crude benchmarks set feedstock costs—Brent averaged 86.5 USD/bbl in 2025 and Australian thermal coal delivered to China rose 14% YoY to 120 USD/ton in 2025, lifting landing costs.

Geopolitical shocks and OPEC+ cuts (2024–25 cuts removed ~1.2 mb/d capacity) pushed spot premiums, directly raising refinery margins volatility and CAPEX recovery timelines.

State-owned producers (CNPC, Sinopec) supply negotiating power, keeping raw-input pricing largely external to Shenghong’s internal efficiency gains.

Specialized Chemical Catalyst Providers

For high-end chemical fiber and EVA new-energy materials, Eastern Shenghong depends on a handful of global specialty catalyst suppliers—three firms supply ~70% of key high-performance catalysts, giving suppliers strong bargaining power due to proprietary tech and few substitutes.

These suppliers charge premiums: specialty catalyst margins often 25–35% and lead times 8–16 weeks, so Shenghong must keep strategic partnerships and long-term contracts to secure quality, stable supply, and R&D co-development.

Energy and Utility Infrastructure Requirements

Energy and Utility Infrastructure Requirements: Jiangsu Eastern Shenghong’s large-scale refining and polyester operations need vast electricity and industrial water, typically supplied by state-regulated utility monopolies in China, giving suppliers strong structural power.

The inputs are non-negotiable for continuous-flow manufacturing, so Shenghong reduces exposure by investing in cogeneration plants and energy-efficient tech, cutting external power demand by about 15% and saving roughly CNY 120 million annually (2024 estimate).

- State utility monopoly = high supplier power

- Electricity/water are essential, non-substitutable

- Onsite cogeneration reduces grid reliance ~15%

- Estimated annual savings ~CNY 120 million (2024)

Logistics and Supply Chain Reliability

The movement of bulk liquid chemicals and finished textiles relies on specialized ship, pipeline, and rail networks; industry-wide dependence on third-party international logistics gives providers moderate bargaining power over Jiangsu Eastern Shenghong.

Eastern Shenghong’s internal logistics reduces some exposure, but 2024 sea freight rates rose ~18% year‑over‑year and China coastal port congestion added 6–12% transit delays, so higher freight or bottlenecks can compress margins and force transport-efficiency measures.

- Third-party logistics = moderate leverage

- Eastern Shenghong has in-house logistics, lowering some risk

- 2024 sea freight +18% yoy; port delays 6–12%

- Higher freight squeezes margins, pushes efficiency moves

Shenghong boosts margins via 5.3Mt integration, but oil, OPEC+ and catalyst oligopoly bite

Supplier power is mixed: Shenghong’s 5.3 Mt integrated PX/ethylene capacity (2024) cuts feedstock buys and lifted refining-to-petro margins 12–18% vs peers, yet global Brent (86.5 USD/bbl 2025), OPEC+ cuts (~1.2 mb/d 2024–25), state-owned oil majors, 3 catalyst firms (≈70% share) and utility monopolies keep strong external pricing power.

| Metric | Value |

|---|---|

| Integrated PX/ethylene | 5.3 Mt (2024) |

| Margin uplift vs peers | +12–18% (2024) |

| Brent | 86.5 USD/bbl (2025) |

| OPEC+ cut impact | ~1.2 mb/d (2024–25) |

| Catalyst concentration | 3 firms ≈70% |

What is included in the product

Tailored exclusively for Jiangsu Eastern Shenghong, this Porter’s Five Forces overview uncovers key competitive drivers, supplier and buyer influence on pricing, entry barriers protecting incumbents, and disruptive substitutes or threats to market share.

Compact Five Forces snapshot for Jiangsu Eastern Shenghong—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to accelerate strategic decisions.

Customers Bargaining Power

Fragmentation of the Downstream Textile Industry

A significant share of Jiangsu Eastern Shenghong’s polyester and nylon sales goes to over 3,000 small‑to‑mid textile firms across China and Southeast Asia, so no single buyer can push prices down meaningfully.

That customer fragmentation, combined with Shenghong’s 2024 output of ~3.8 million tons of fibers and >85% on‑time delivery, sustains above‑market pricing in the traditional fiber segment.

Concentration in the Solar Material Segment

Jiangsu Eastern Shenghong sells EVA and related solar materials to a concentrated group of large module makers who account for about 60–70% of the company’s new-energy sales, buying in volumes >10,000 tons annually; these sophisticated buyers demand tight specs and drive down prices, raising customer bargaining power. The firm must invest in R&D—the company spent RMB 120 million on materials R&D in 2024—to stay ahead and reduce churn risk if clients switch to rivals.

Price Sensitivity to Commodity Cycles

Low Switching Costs for Standardized Products

For standard-grade chemical fibers, switching from Jiangsu Eastern Shenghong to peers like Hengli or Rongsheng is easy and cheap, keeping customer bargaining power high and forcing Eastern Shenghong to compete on supply-chain integration and service reliability.

To raise switching costs, Eastern Shenghong is partnering with brands on sustainable and recycled lines—by 2025 these tie-ups account for about 12% of specialty sales—requiring multi-year technical alignment and joint certification.

- Low switching cost vs Hengli/Rongsheng

- Focus: supply-chain integration, service reliability

- Sustainable/recycled lines ≈12% of specialty sales (2025)

- Long-term technical alignment raises lock-in

Impact of End-Consumer Demand Trends

Slower global consumer spending cuts retail orders; in 2023 global apparel spending fell ~2.5% year-on-year, and mills trimmed yarn purchases, shifting bargaining power to buyers with inventory choices.

Eastern Shenghong watches retail sales and PMI data monthly and cut output when apparel demand dips, avoiding blanket price concessions seen in 2022 when fabric prices dropped ~15%.

- Retail demand down 2.5% (2023)

- Fabric prices fell ~15% (2022 downturn)

- Monthly PMI monitoring

Mixed buyer power: small textile firms vs solar giants shape polyester pricing

Buyers are mixed: >3,000 small textile firms limit single‑buyer power for polyester, while large solar module makers (60–70% of new‑energy sales) concentrate bargaining for EVA, pushing prices down. Commodity fibers track PTA/MEG swings (PTA -18% YoY 2024) so buyer power is high; specialty fibers (ASP +15–25% in 2024) and 12% recycled/sustainable sales (2025) raise stickiness.

| Metric | 2024/2025 |

|---|---|

| Total fiber output | ~3.8M t (2024) |

| PTA change | -18% YoY (2024) |

| New‑energy buyer share | 60–70% |

| R&D spend | RMB 120M (2024) |

| Specialty ASP lift | +15–25% (2024) |

| Sustainable sales | ~12% specialty (2025) |

Same Document Delivered

Jiangsu Eastern Shenghong Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Jiangsu Eastern Shenghong you’ll receive immediately after purchase—no placeholders, fully formatted and ready for use.

The document displayed here is part of the final report and matches the downloadable file you’ll get upon payment, containing competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications.