Sumitomo Heavy Industries Boston Consulting Group Matrix

Unlock Strategic Clarity

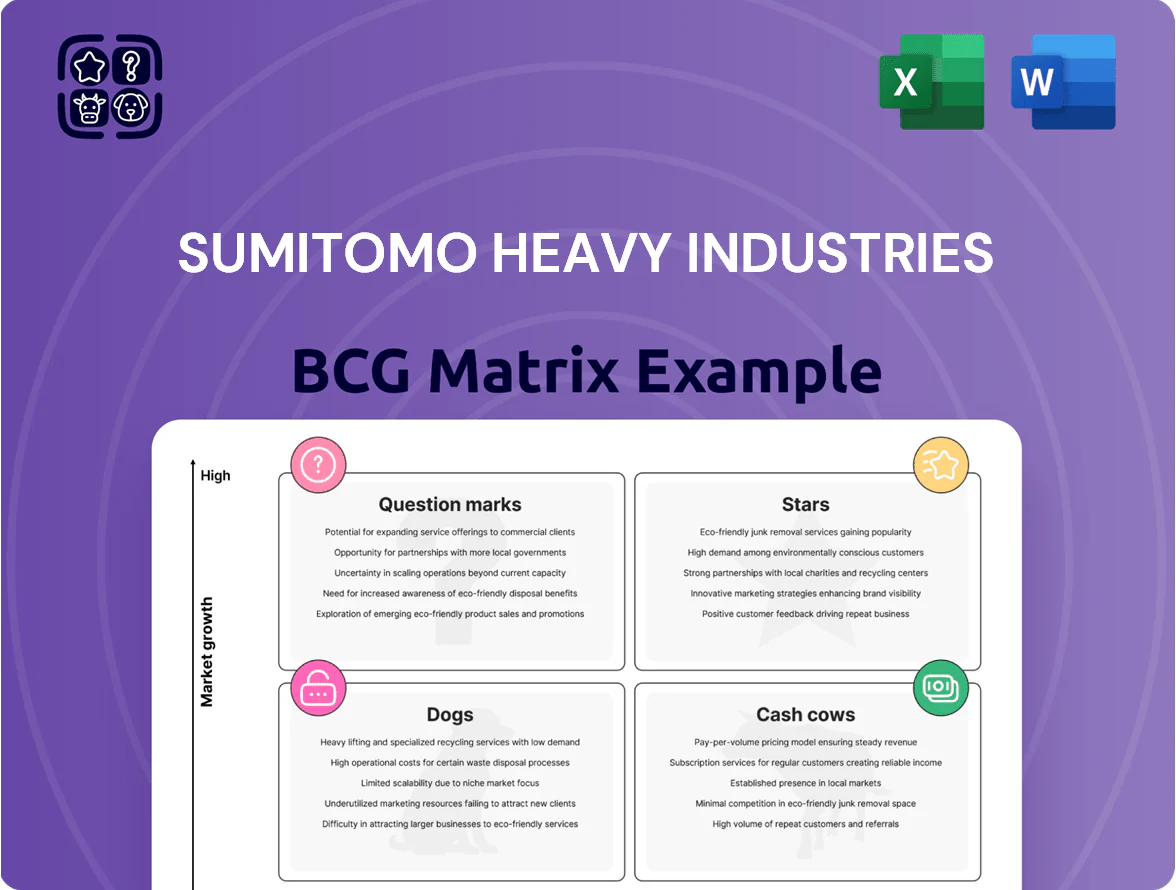

Sumitomo Heavy Industries spans diverse heavy-equipment and industrial segments with varying growth and market-share dynamics; this preview highlights potential Stars in niche machinery and possible Cash Cows in legacy infrastructure products, while newer tech lines may sit as Question Marks requiring capital decisions. The full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and a strategic roadmap to optimize portfolio allocation—purchase the complete report for the Word and Excel files that make execution immediate and confident.

Stars

Semiconductor Manufacturing Equipment

Semiconductor Manufacturing Equipment is a primary growth engine for Sumitomo Heavy Industries, driven by leadership in advanced laser annealing and ion implanter systems; under the Medium-Term Management Plan 2026 SHI integrated its laser business into Sumitomo Heavy Industries Ion Technology to sharpen the edge.

Global demand for next‑generation logic and power semiconductors—IDC estimates ~15% CAGR 2024–2028—supports high growth, and SHI reported ~20% segment revenue growth in FY2024, keeping a significant share in these fab tools.

Automated Port and Logistics Solutions

SHI leads automated Rubber Tired Gantry (RTG) cranes, with ~35% global share in automated RTG deployments as of 2025 and growing demand for hydrogen-convertible units; ports adopting automation rose 18% year-over-year through 2024.

Cryocoolers for Healthcare and Quantum Tech

SHI holds >90% global share in cryocoolers for MRI, driving ~¥70–90bn annual revenue in that unit in 2024 (company filings); MRI demand stays stable while unit prices rose ~5% in 2023–24.

These cryocoolers are critical for quantum computing and hydrogen tech, markets growing at ~20–30% CAGR (2024–29 estimates), adding high-margin, fast-growth channels.

With near-monopoly scale, deep IP, and cross-sector demand, this unit is a classic BCG star—high share, high market growth—supporting strong cash generation and strategic expansion.

Robotics and Automation Components

Robotics and Automation Components is a Star for Sumitomo Heavy Industries (SHI): 2024 sales in precision positioning and vacuum robots rose ~28% to ¥48.6bn, driven by semiconductor and EV supply chains, and 2025 US market entry targets $60bn industrial automation demand with specialized robots.

SHI’s precision reputation, 15% global market-share gains since 2022, and expanded distributor network are capturing smart manufacturing wins across Asia, Europe, and now the US.

- 2024 revenue: ¥48.6bn (+28%)

- 2022–2024 market-share gain: ~15%

- 2025 US entry targets $60bn automation market

- Key drivers: semiconductor, EV, smart factories

Zero-Backlash Precision Gearboxes

The DA Series zero-backlash gear heads, launched Q1 2025, strengthened Sumitomo Heavy Industries (SHI) in high-precision motion control, targeting machine tool and semiconductor segments where sub-micron positioning is required.

Higher automation and 2024–25 fab investments (global capex +18% to $120B in 2024) expand addressable market; SHI’s DA Series gives a tech edge to capture share from NSK and Nabtesco.

- DA Series launch: Q1 2025

- Target sectors: machine tools, semiconductors

- Semiconductor capex: ~$120B (2024)

- Competitive peers: NSK, Nabtesco

SHI Stars: Dominant cryocoolers, booming semiconductors, RTG automation & robotics surge

SHI Stars: semiconductor equipment, automated RTG cranes, cryocoolers, robotics—high market growth and leading shares (FY2024–25). Key metrics: semiconductor seg. rev +20% (FY2024); RTG auto share ~35% (2025); cryocooler rev ¥70–90bn (2024); robotics rev ¥48.6bn (+28%, 2024); DA Series launch Q1 2025.

| Unit | Share/Growth | 2024–25 |

|---|---|---|

| Semiconductor equip | High share | +20% rev |

| RTG cranes | ~35% auto share | Ports +18% YoY |

| Cryocoolers | >90% global | ¥70–90bn rev |

| Robotics | Share +15% (’22–’24) | ¥48.6bn (+28%) |

What is included in the product

Comprehensive BCG Matrix review of Sumitomo Heavy Industries' units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Sumitomo Heavy Industries business unit in a BCG quadrant for fast strategic review.

Cash Cows

Standard Power Transmission Equipment

The CYCLO Drive and standard gear reducers form SHI’s cash cow with roughly 30% global market share in industrial reducers and steady aftermarket demand; installed-base service and parts sales accounted for about ¥40 billion in FY2024 revenue (Sumitomo HI disclosures). The basic power-transmission market is mature, so marketing spend stays low while gross margins from parts/services remain above company average. That steady cash flow funds R&D in robotics and compressors.

Plastic Injection Molding Machines

Sumitomo Heavy Industries (SHI) leads in all-electric plastic injection molding machines, prized for precision and ~30% lower energy use versus hydraulic rivals; global market growth is ~3% CAGR through 2025, marking maturity.

SHI holds top share in high-end electronics and medical segments, with premium pricing supporting ~18–22% EBITDA margins and steady aftermarket revenue.

Strong global brand and 200+ service centers deliver dependable cash flow and liquidity, funding R&D and dividends.

After-Sales and Lifecycle Management Services

Sumitomo Heavy Industries’ installed base—over 120,000 machines worldwide as of 2025—creates a low-growth, high-margin after-sales market where maintenance, parts, and upgrades generate recurring revenue with gross margins often >40%.

Comprehensive lifecycle management, including remote monitoring and digital twin services rolled out in 2023, raises service attach rates to ~35% and boosts ARPU by ~18% year-over-year.

This service segment stabilizes EBIT, contributing roughly 22% of 2024 group operating profit and effectively milks equipment value independent of capital-equipment cycles.

Hydraulic Excavators and Construction Machinery

SHI’s hydraulic excavators and construction machinery deliver steady cash: global construction output fell 3% in 2023 but SHI held double-digit share in Japan and parts of Southeast Asia, producing ~¥120bn revenue from construction equipment in FY2024, so the segment funds R&D for greener infrastructure.

The product line is tech-mature with limited CAPEX needs; operating margin near 12% in FY2024 means reliable free cash flow to back EV and hydrogen investments.

- ¥120bn construction-equipment revenue FY2024

- ~12% operating margin FY2024

- High market share in Japan, parts of SE Asia

- Low incremental CAPEX; funds green tech R&D

Water Treatment and Environmental Plants

Sumitomo Heavy Industries (SHI) water treatment and environmental plants are cash cows: long-standing domestic contracts in Japan with municipalities and industries yield steady revenue and long-term service fees, producing predictable cash flow less tied to semiconductors or robotics swings; FY2024 service backlog ~¥120 billion supports near-term visibility.

These mature operations face high entry barriers—regulatory, tech, and service networks—driving stable procurement cycles and margins; FY2023 water-related operating margin ~8–10% vs group volatility.

- Stable revenue: long-term municipal contracts

- Backlog: ≈¥120 billion (FY2024)

- Operating margin: ~8–10% (FY2023)

- Low cyclicality vs semiconductors/robotics

SHI: CYCLO dominance, ¥40bn service cash flow & ¥120bn construction/water bases

SHI cash cows: CYCLO drives/gear reducers (~30% global share) and after-sales (~¥40bn FY2024); all‑electric injection molds (mature, ~3% CAGR) and high‑end electronics/medical (18–22% EBITDA); construction equipment (~¥120bn revenue FY2024, ~12% op margin); water plants backlog ≈¥120bn (FY2024, 8–10% margin).

| Segment | Key metric | FY/Year |

|---|---|---|

| CYCLO/Reducers | ~30% share; ¥40bn service rev | FY2024 |

| Injection molds | ~3% CAGR to 2025 | 2025 |

| Construction eqpt | ¥120bn; ~12% op margin | FY2024 |

| Water/env. | Backlog ≈¥120bn; 8–10% margin | FY2024/2023 |

Delivered as Shown

Sumitomo Heavy Industries BCG Matrix

The Sumitomo Heavy Industries BCG Matrix you're previewing is the exact final file you'll receive after purchase—no watermarks, no demo content, just a professionally formatted, analysis-ready report designed for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Sumitomo Heavy Industries spans diverse heavy-equipment and industrial segments with varying growth and market-share dynamics; this preview highlights potential Stars in niche machinery and possible Cash Cows in legacy infrastructure products, while newer tech lines may sit as Question Marks requiring capital decisions. The full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and a strategic roadmap to optimize portfolio allocation—purchase the complete report for the Word and Excel files that make execution immediate and confident.

Stars

Semiconductor Manufacturing Equipment

Semiconductor Manufacturing Equipment is a primary growth engine for Sumitomo Heavy Industries, driven by leadership in advanced laser annealing and ion implanter systems; under the Medium-Term Management Plan 2026 SHI integrated its laser business into Sumitomo Heavy Industries Ion Technology to sharpen the edge.

Global demand for next‑generation logic and power semiconductors—IDC estimates ~15% CAGR 2024–2028—supports high growth, and SHI reported ~20% segment revenue growth in FY2024, keeping a significant share in these fab tools.

Automated Port and Logistics Solutions

SHI leads automated Rubber Tired Gantry (RTG) cranes, with ~35% global share in automated RTG deployments as of 2025 and growing demand for hydrogen-convertible units; ports adopting automation rose 18% year-over-year through 2024.

Cryocoolers for Healthcare and Quantum Tech

SHI holds >90% global share in cryocoolers for MRI, driving ~¥70–90bn annual revenue in that unit in 2024 (company filings); MRI demand stays stable while unit prices rose ~5% in 2023–24.

These cryocoolers are critical for quantum computing and hydrogen tech, markets growing at ~20–30% CAGR (2024–29 estimates), adding high-margin, fast-growth channels.

With near-monopoly scale, deep IP, and cross-sector demand, this unit is a classic BCG star—high share, high market growth—supporting strong cash generation and strategic expansion.

Robotics and Automation Components

Robotics and Automation Components is a Star for Sumitomo Heavy Industries (SHI): 2024 sales in precision positioning and vacuum robots rose ~28% to ¥48.6bn, driven by semiconductor and EV supply chains, and 2025 US market entry targets $60bn industrial automation demand with specialized robots.

SHI’s precision reputation, 15% global market-share gains since 2022, and expanded distributor network are capturing smart manufacturing wins across Asia, Europe, and now the US.

- 2024 revenue: ¥48.6bn (+28%)

- 2022–2024 market-share gain: ~15%

- 2025 US entry targets $60bn automation market

- Key drivers: semiconductor, EV, smart factories

Zero-Backlash Precision Gearboxes

The DA Series zero-backlash gear heads, launched Q1 2025, strengthened Sumitomo Heavy Industries (SHI) in high-precision motion control, targeting machine tool and semiconductor segments where sub-micron positioning is required.

Higher automation and 2024–25 fab investments (global capex +18% to $120B in 2024) expand addressable market; SHI’s DA Series gives a tech edge to capture share from NSK and Nabtesco.

- DA Series launch: Q1 2025

- Target sectors: machine tools, semiconductors

- Semiconductor capex: ~$120B (2024)

- Competitive peers: NSK, Nabtesco

SHI Stars: Dominant cryocoolers, booming semiconductors, RTG automation & robotics surge

SHI Stars: semiconductor equipment, automated RTG cranes, cryocoolers, robotics—high market growth and leading shares (FY2024–25). Key metrics: semiconductor seg. rev +20% (FY2024); RTG auto share ~35% (2025); cryocooler rev ¥70–90bn (2024); robotics rev ¥48.6bn (+28%, 2024); DA Series launch Q1 2025.

| Unit | Share/Growth | 2024–25 |

|---|---|---|

| Semiconductor equip | High share | +20% rev |

| RTG cranes | ~35% auto share | Ports +18% YoY |

| Cryocoolers | >90% global | ¥70–90bn rev |

| Robotics | Share +15% (’22–’24) | ¥48.6bn (+28%) |

What is included in the product

Comprehensive BCG Matrix review of Sumitomo Heavy Industries' units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Sumitomo Heavy Industries business unit in a BCG quadrant for fast strategic review.

Cash Cows

Standard Power Transmission Equipment

The CYCLO Drive and standard gear reducers form SHI’s cash cow with roughly 30% global market share in industrial reducers and steady aftermarket demand; installed-base service and parts sales accounted for about ¥40 billion in FY2024 revenue (Sumitomo HI disclosures). The basic power-transmission market is mature, so marketing spend stays low while gross margins from parts/services remain above company average. That steady cash flow funds R&D in robotics and compressors.

Plastic Injection Molding Machines

Sumitomo Heavy Industries (SHI) leads in all-electric plastic injection molding machines, prized for precision and ~30% lower energy use versus hydraulic rivals; global market growth is ~3% CAGR through 2025, marking maturity.

SHI holds top share in high-end electronics and medical segments, with premium pricing supporting ~18–22% EBITDA margins and steady aftermarket revenue.

Strong global brand and 200+ service centers deliver dependable cash flow and liquidity, funding R&D and dividends.

After-Sales and Lifecycle Management Services

Sumitomo Heavy Industries’ installed base—over 120,000 machines worldwide as of 2025—creates a low-growth, high-margin after-sales market where maintenance, parts, and upgrades generate recurring revenue with gross margins often >40%.

Comprehensive lifecycle management, including remote monitoring and digital twin services rolled out in 2023, raises service attach rates to ~35% and boosts ARPU by ~18% year-over-year.

This service segment stabilizes EBIT, contributing roughly 22% of 2024 group operating profit and effectively milks equipment value independent of capital-equipment cycles.

Hydraulic Excavators and Construction Machinery

SHI’s hydraulic excavators and construction machinery deliver steady cash: global construction output fell 3% in 2023 but SHI held double-digit share in Japan and parts of Southeast Asia, producing ~¥120bn revenue from construction equipment in FY2024, so the segment funds R&D for greener infrastructure.

The product line is tech-mature with limited CAPEX needs; operating margin near 12% in FY2024 means reliable free cash flow to back EV and hydrogen investments.

- ¥120bn construction-equipment revenue FY2024

- ~12% operating margin FY2024

- High market share in Japan, parts of SE Asia

- Low incremental CAPEX; funds green tech R&D

Water Treatment and Environmental Plants

Sumitomo Heavy Industries (SHI) water treatment and environmental plants are cash cows: long-standing domestic contracts in Japan with municipalities and industries yield steady revenue and long-term service fees, producing predictable cash flow less tied to semiconductors or robotics swings; FY2024 service backlog ~¥120 billion supports near-term visibility.

These mature operations face high entry barriers—regulatory, tech, and service networks—driving stable procurement cycles and margins; FY2023 water-related operating margin ~8–10% vs group volatility.

- Stable revenue: long-term municipal contracts

- Backlog: ≈¥120 billion (FY2024)

- Operating margin: ~8–10% (FY2023)

- Low cyclicality vs semiconductors/robotics

SHI: CYCLO dominance, ¥40bn service cash flow & ¥120bn construction/water bases

SHI cash cows: CYCLO drives/gear reducers (~30% global share) and after-sales (~¥40bn FY2024); all‑electric injection molds (mature, ~3% CAGR) and high‑end electronics/medical (18–22% EBITDA); construction equipment (~¥120bn revenue FY2024, ~12% op margin); water plants backlog ≈¥120bn (FY2024, 8–10% margin).

| Segment | Key metric | FY/Year |

|---|---|---|

| CYCLO/Reducers | ~30% share; ¥40bn service rev | FY2024 |

| Injection molds | ~3% CAGR to 2025 | 2025 |

| Construction eqpt | ¥120bn; ~12% op margin | FY2024 |

| Water/env. | Backlog ≈¥120bn; 8–10% margin | FY2024/2023 |

Delivered as Shown

Sumitomo Heavy Industries BCG Matrix

The Sumitomo Heavy Industries BCG Matrix you're previewing is the exact final file you'll receive after purchase—no watermarks, no demo content, just a professionally formatted, analysis-ready report designed for strategic clarity and immediate use.